Driving Your Dreams: The Ultimate Guide to Online Bank Car Loans

Driving Your Dreams: The Ultimate Guide to Online Bank Car Loans Carloan.Guidemechanic.com

The open road awaits, and for many, the path to owning a new or pre-owned vehicle has shifted dramatically. Gone are the days when car financing meant endless hours at dealerships or numerous in-person bank visits. Today, the digital age has revolutionized how we secure auto loans, placing the power of choice and convenience firmly in your hands. Welcome to the world of online bank car loans – a modern, efficient, and often more advantageous way to finance your next ride.

In this comprehensive guide, we’ll explore every facet of securing an online bank car loan. We’ll delve into the unparalleled benefits, demystify the application process, uncover critical factors affecting your approval, and share expert insights to help you navigate this landscape successfully. Our mission is to equip you with the knowledge to make informed decisions, ensuring you not only drive away in your dream car but do so with the best possible financing terms.

Driving Your Dreams: The Ultimate Guide to Online Bank Car Loans

The Digital Revolution of Car Financing: What is an Online Bank Car Loan?

At its core, an online bank car loan is simply a vehicle financing option offered by a bank, but with the entire application, approval, and often even the closing process conducted remotely through their digital platforms. Instead of stepping into a physical branch, you interact with the bank via their website, mobile app, or secure online portals. This shift from brick-and-mortar to clicks-and-code has transformed the lending landscape, making it more accessible and streamlined than ever before.

This modern approach to auto financing reflects a broader trend in banking towards digital services. Banks are heavily investing in robust online infrastructures to cater to consumers who prefer the speed and flexibility of managing their finances from anywhere, at any time. For car buyers, this means no more rushing to beat bank closing times or enduring lengthy face-to-face meetings.

While the fundamental principles of a car loan – borrowing money to purchase a vehicle and repaying it with interest over a set period – remain unchanged, the online delivery method introduces a host of distinct advantages. It empowers consumers with greater control, transparency, and often, more competitive offers. Understanding this foundational concept is the first step towards leveraging its full potential.

Unpacking the Advantages: Why Choose an Online Bank Car Loan?

The shift towards digital financing isn’t just a matter of convenience; it offers tangible benefits that can significantly improve your car buying experience and financial outcome. Based on my experience in the automotive and financial sectors, these advantages are often what truly sets online bank loans apart from traditional methods.

Unmatched Convenience and Accessibility

One of the most compelling reasons to consider an online bank car loan is the sheer convenience it offers. You can research lenders, compare rates, and submit your application from the comfort of your home, office, or even while on the go. This means no more rigid bank hours or geographical limitations.

This round-the-clock accessibility allows you to fit the loan application process into your own schedule, rather than having to disrupt your day. Whether you’re an early bird or a night owl, the digital doors of banks are always open, making the process stress-free and truly on your terms.

Highly Competitive Interest Rates

Online banks often have lower operating costs compared to their traditional counterparts with extensive branch networks. These savings can frequently be passed on to consumers in the form of more competitive interest rates and lower fees. This can translate into significant savings over the life of your loan.

Furthermore, the online environment fosters greater transparency and encourages more thorough rate shopping. With just a few clicks, you can compare offers from multiple banks, pushing lenders to provide their most attractive rates to win your business. This competitive dynamic is a huge win for the borrower.

Speed and Efficiency in Approvals

The digital nature of online applications typically leads to much faster processing times. Many online banks leverage advanced algorithms and automated systems to review applications, often providing pre-approval decisions within minutes or hours, rather than days. This rapid turnaround is invaluable when you’re ready to make a purchase.

This swift process means you can walk into a dealership with pre-approved financing in hand, effectively transforming you into a cash buyer. This not only speeds up the purchase process at the dealership but also gives you significant leverage in price negotiations.

Enhanced Transparency and Clear Terms

Online platforms are generally designed to present loan terms, conditions, and disclosures in a clear, digestible format. You have ample time to review all documentation at your leisure, without feeling rushed or pressured by a salesperson or loan officer. This clarity helps you understand exactly what you’re agreeing to.

The ability to easily access and re-read loan agreements and FAQs online promotes a more informed decision-making process. You can print documents, share them with advisors, and truly grasp the full scope of your financial commitment before signing on the dotted line.

A Wider Pool of Lenders and Options

By expanding your search beyond local banks, you gain access to a national or even international network of online lenders. This broadens your options significantly, increasing your chances of finding a loan product that perfectly matches your specific financial situation and needs.

Whether you’re looking for flexible payment terms, specific loan amounts, or options for unique credit profiles, the online marketplace offers a diversity that traditional, localized lending often cannot. This wider selection ensures you’re not settling for the only option available but choosing the best one for you.

Navigating the Application Process: A Step-by-Step Guide

Securing an online bank car loan might seem daunting at first, but it’s a straightforward process once you understand the steps involved. Based on my experience, a methodical approach will yield the best results and reduce stress.

Step 1: Research and Compare Lenders

Before you even think about filling out an application, dedicate ample time to researching various online banks that offer auto loans. Don’t just look at the big names; many smaller, digitally-focused banks and credit unions also provide excellent rates and customer service. Focus on banks renowned for their online capabilities.

Look beyond just the advertised interest rates. Investigate their customer reviews, transparency regarding fees, and the ease of their online application portal. A user-friendly interface and responsive customer support can make a world of difference throughout your loan term.

Step 2: Gather Your Documents

Preparation is key to a smooth application process. Before you start, compile all necessary documents and information. This typically includes proof of identity (driver’s license, social security number), proof of income (pay stubs, tax returns, bank statements), and residence verification (utility bills).

You’ll also need details about your credit history, though this will primarily be accessed by the lender directly. If you already have a specific vehicle in mind, gather its information, such as the make, model, year, VIN, and estimated price. Having these ready will significantly speed up your application.

Step 3: Get Pre-Approved (Highly Recommended!)

One of the most powerful tools in your car buying arsenal is getting pre-approved for a loan. This involves a preliminary review of your financial information by a lender, resulting in an offer for a maximum loan amount and an estimated interest rate. Pro tips from us: always get pre-approved before stepping foot in a dealership.

Pre-approval offers several critical advantages. It gives you a firm budget, letting you know exactly how much car you can afford. More importantly, it transforms you into a cash buyer at the dealership, giving you significant leverage in negotiating the vehicle’s price, rather than just focusing on the monthly payment. Remember, most pre-approvals involve a "soft" credit inquiry, which won’t impact your credit score. A "hard" inquiry only happens when you finalize the loan.

Step 4: Complete the Full Application

Once you’ve selected a lender and are ready to proceed (perhaps after getting pre-approved and finding your desired vehicle), you’ll complete the full online loan application. This will be more detailed than a pre-approval and will require you to input all the information you gathered in Step 2. Be meticulous and ensure all information is accurate to avoid delays.

During this stage, you’ll typically upload your supporting documents directly through the bank’s secure online portal. Most online banks have encrypted systems to protect your personal and financial data. Double-check every entry before submission.

Step 5: Review and Sign the Loan Agreement

If your application is approved, the bank will send you the final loan agreement. This is a critical juncture where common mistakes to avoid are rushing through the document. Take your time to thoroughly review every clause, especially the Annual Percentage Rate (APR), the loan term, any associated fees (origination fees, late payment fees), and prepayment penalties.

Ensure that the terms match what you were offered during pre-approval and that you understand your repayment schedule and obligations. If anything is unclear, do not hesitate to contact the bank’s customer service for clarification before electronically signing the agreement. Once signed, the funds are typically disbursed directly to the dealership or, in some cases, to you for a private sale.

Key Factors Influencing Your Online Bank Car Loan Approval and Rates

Several critical factors weigh heavily on whether your online bank car loan application is approved and what interest rate you ultimately receive. Understanding these elements can help you prepare and potentially improve your loan terms.

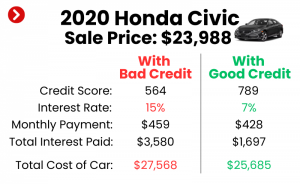

Your Credit Score

Undoubtedly, your credit score is the most significant determinant. A higher credit score signals to lenders that you are a reliable borrower with a history of responsible debt management. This typically translates into lower interest rates and more favorable loan terms. Lenders use scores like FICO or VantageScore to assess your creditworthiness.

Conversely, a lower credit score might lead to higher interest rates or even require a co-signer to secure approval. It’s always a good practice to check your credit score and report well before applying for a car loan to identify and rectify any errors.

Debt-to-Income Ratio (DTI)

Your DTI ratio is another crucial metric lenders scrutinize. It represents the percentage of your gross monthly income that goes towards paying your monthly debt payments. A low DTI indicates that you have sufficient income to comfortably manage additional debt, like a car loan.

Lenders generally prefer a DTI of 36% or less, though some may approve loans with a DTI up to 43% or even higher, especially for applicants with excellent credit. A high DTI suggests you might be overextended, making you a riskier borrower in the eyes of the bank.

Loan Amount and Term

The total amount you wish to borrow and the duration over which you plan to repay it (the loan term) also play a role. Larger loan amounts or longer terms can sometimes carry slightly higher interest rates due to increased risk for the lender. However, a longer term often results in lower monthly payments, which can be appealing.

It’s a delicate balance: while a longer term reduces monthly payments, it also means you’ll pay more interest over the life of the loan. Pro tips from us: aim for the shortest loan term you can comfortably afford to minimize total interest paid.

Your Down Payment

Making a substantial down payment can significantly improve your chances of approval and secure a better interest rate. A larger down payment reduces the amount you need to borrow, thereby lowering the lender’s risk. It also demonstrates your financial commitment to the purchase.

Furthermore, a significant down payment helps you avoid being "upside down" on your loan, which means owing more than the car is worth. This can happen quickly with depreciation, and a strong down payment provides a buffer.

Vehicle Age and Type

The vehicle you intend to purchase also influences the loan terms. Newer, less depreciated vehicles are often seen as less risky collateral by lenders, potentially leading to better rates. Older vehicles or those with high mileage may be subject to higher rates or shorter loan terms.

Some lenders might also have restrictions on the types of vehicles they finance, particularly for classic cars, heavily modified vehicles, or certain luxury models. Always confirm the bank’s policies regarding the specific vehicle you have in mind.

Interest Rates: Fixed vs. Variable

When evaluating loan offers, you’ll encounter two main types of interest rates: fixed and variable. A fixed interest rate remains constant throughout the life of your loan, providing predictable monthly payments. This stability is often preferred by borrowers for budgeting purposes.

A variable interest rate, on the other hand, can fluctuate based on market conditions, typically tied to an index like the prime rate. While a variable rate might start lower, it carries the risk of increasing your monthly payments if rates rise. For car loans, fixed rates are far more common and generally recommended for stability.

Demystifying Online Bank Car Loan Options for Different Credit Scores

Your credit score is a major gatekeeper in the world of lending, but it doesn’t always close the door entirely. Online banks offer solutions tailored to various credit profiles, from pristine to challenging.

Excellent/Good Credit: The Fast Track to Top Rates

If you boast an excellent (750+) or good (670-749) credit score, the online bank car loan landscape is largely in your favor. You’ll qualify for the lowest interest rates, enjoy the most flexible terms, and have a wide array of lenders competing for your business. This is where pre-approval truly shines, allowing you to pick the best offer.

With strong credit, you can focus on securing the shortest loan term possible to minimize total interest paid, or choose a comfortable monthly payment that fits your budget perfectly. Lenders view you as a low-risk borrower, making the approval process swift and smooth.

Fair/Average Credit: Navigating the Middle Ground

For those with fair (580-669) or average credit, securing an online bank car loan is still very much achievable, though the terms might not be as stellar as for those with excellent credit. You might encounter slightly higher interest rates, but online banks are often more willing to work with this credit tier than some traditional lenders.

Strategies for borrowers with fair credit include making a larger down payment, choosing a more affordable vehicle, or exploring credit unions which can sometimes be more forgiving. It’s also an ideal time to consider improving your credit score before applying, as even a small bump can make a difference. For detailed strategies on improving your credit, you might want to check out our article on Strategies for Improving Your Credit Score Before a Loan.

Bad Credit: Finding Solutions (With Caution)

Even with bad credit (below 580), an online bank car loan isn’t entirely out of reach, but it requires a more strategic approach and careful consideration. Online lenders specializing in subprime loans exist, but their interest rates will be significantly higher to offset the increased risk.

If you have bad credit, consider options like adding a creditworthy co-signer, which can significantly improve your chances of approval and secure a better rate. A larger down payment also demonstrates your commitment and reduces the lender’s risk. Always be wary of predatory lenders and excessively high interest rates; ensure the loan is truly affordable. Researching online lenders that specifically cater to bad credit borrowers can open doors, but always read the fine print.

Refinancing Your Online Bank Car Loan: Is It Worth It?

Securing your initial car loan is just the beginning. Over time, your financial situation can change, and so can market interest rates. This is where refinancing your online bank car loan comes into play, offering a valuable opportunity to potentially save money or adjust your monthly payments.

What is Car Loan Refinancing?

Refinancing a car loan means taking out a new loan to pay off your existing one. The goal is typically to secure a better interest rate, lower your monthly payments, or change the loan term. It’s essentially replacing your old loan with a brand-new one, often from a different lender.

When to Consider Refinancing

There are several compelling reasons why you might consider refinancing your online bank car loan. If your credit score has significantly improved since you first took out the loan, you might qualify for a much lower interest rate now. Similarly, if market interest rates have dropped, refinancing can help you capitalize on the more favorable environment.

You might also consider refinancing if you want to lower your monthly payments by extending the loan term, though be mindful that this will increase the total interest paid. Conversely, if you want to pay off your loan faster and can afford higher payments, you could refinance to a shorter term. For a deeper dive, our "Ultimate Guide to Car Loan Refinancing" provides comprehensive insights.

The Online Refinancing Process

The process for refinancing an online bank car loan mirrors that of applying for a new one. You’ll research lenders, gather your financial documents, apply online, and if approved, review and sign the new loan agreement. The new lender will then pay off your old loan, and you’ll begin making payments to them under the new terms. Many online banks streamline this process, making it as convenient as the initial loan application.

Common Pitfalls and How to Avoid Them When Getting an Online Car Loan

While online bank car loans offer numerous advantages, there are common mistakes that borrowers can make. Being aware of these pitfalls is crucial for a smooth and financially sound experience.

Not Comparing Enough Offers

One of the biggest mistakes is settling for the first loan offer you receive. The convenience of online applications means you can easily get quotes from multiple banks and credit unions. Failing to shop around means you could be missing out on significantly better interest rates or more favorable terms. Common mistakes to avoid are thinking all banks offer the same deal.

Take the time to compare at least three to five offers. Even a half-percentage point difference in interest can save you hundreds, if not thousands, of dollars over the life of your loan. This due diligence is effortless in the online environment.

Ignoring the Fine Print

The excitement of getting approved can sometimes lead borrowers to skim over the detailed loan agreement. However, the fine print contains crucial information about fees, penalties, and specific terms that could impact you. Overlooking these details can lead to unexpected costs or restrictions down the line.

Always review the APR, all associated fees (origination, late payment, prepayment), and the exact repayment schedule. If you have any questions, contact the lender for clarification before signing.

Stretching the Loan Term Too Long

While a longer loan term reduces your monthly payments, it significantly increases the total amount of interest you’ll pay over the life of the loan. It also prolongs the period you are in debt and increases the risk of being "upside down" on your car loan.

Based on my experience, aim for the shortest loan term you can comfortably afford without straining your budget. A 60-month loan is generally a good balance for most borrowers, but if you can manage 48 months, the savings can be substantial.

Not Getting Pre-Approved

As discussed earlier, skipping the pre-approval step puts you at a disadvantage at the dealership. Without a pre-approved loan, you might be tempted to accept dealership financing that isn’t the best deal, or you might struggle to negotiate the car’s price effectively.

Pre-approval arms you with a clear budget and allows you to negotiate the car’s price separately from the financing, empowering you to make smarter financial decisions.

Falling for Predatory Lenders

While reputable online banks offer legitimate and fair loans, the digital space also hosts less scrupulous lenders. Be wary of offers that seem too good to be true, extremely high-pressure sales tactics, or lenders that guarantee approval regardless of credit history without any verification.

Always verify the lender’s credentials, read reviews, and ensure they are transparent about all fees and terms. A legitimate online bank will never ask for upfront fees or guarantee a loan without reviewing your financial information. Stick to well-known, established financial institutions when possible.

Beyond the Basics: Advanced Tips for Securing the Best Online Bank Car Loan

To truly optimize your online bank car loan experience, consider these advanced strategies that can further enhance your terms and overall satisfaction.

Consider a Co-Signer (If Applicable)

If you have a lower credit score or a high debt-to-income ratio, bringing in a co-signer with excellent credit can significantly improve your chances of approval and secure a better interest rate. A co-signer shares the legal responsibility for the loan, reducing the lender’s risk.

However, be mindful of the implications for your co-signer. If you default on payments, their credit score will be negatively impacted, and they will be legally obligated to repay the loan. This decision should only be made with a full understanding and strong trust between both parties.

Automate Your Payments

Many online banks offer incentives, such as a slight interest rate reduction, for setting up automatic payments. This not only saves you money but also ensures you never miss a payment, which is crucial for maintaining a good credit history.

Automating payments provides peace of mind and frees you from remembering due dates, reducing the risk of late fees and negative impacts on your credit score. It’s a simple, effective strategy that benefits both you and the lender.

Understand the Difference Between APR and Interest Rate

While often used interchangeably, the interest rate and the Annual Percentage Rate (APR) are distinct. The interest rate is simply the cost of borrowing money. The APR, however, includes the interest rate plus any additional fees associated with the loan, such as origination fees.

The APR provides a more accurate picture of the total annual cost of your loan. When comparing loan offers, always use the APR to ensure you’re making an apples-to-apples comparison. This comprehensive figure helps you understand the true expense of your financing. For more financial literacy, trusted external resources like the Consumer Financial Protection Bureau (CFPB) offer excellent guides on understanding loan terms.

Leverage Manufacturer Incentives with Bank Financing

Sometimes, car manufacturers offer low-interest financing deals directly through their captive finance companies. While these can be attractive, they might not always be the absolute best deal, especially if you have excellent credit. Always compare manufacturer offers with online bank loan rates.

In some cases, manufacturers offer cash rebates or other incentives if you opt out of their special financing. It might be more financially advantageous to take the rebate and finance through an online bank with a highly competitive rate, rather than taking the manufacturer’s financing. Do the math to see which option saves you more money overall.

Conclusion: Your Road to Smart Car Financing Starts Online

The world of online bank car loans offers an unprecedented level of convenience, transparency, and competitive advantage for today’s car buyer. By embracing the digital shift, you gain access to a wider array of options, often at better rates, all from the comfort of your home. From seamless applications and rapid pre-approvals to understanding the nuances of your credit score and smart refinancing strategies, the power to secure optimal financing is truly at your fingertips.

Remember, the key to a successful online bank car loan experience lies in thorough research, meticulous preparation, and a keen eye for detail. Don’t rush the process, compare multiple offers, understand every clause in your loan agreement, and always prioritize your long-term financial health. Armed with the insights from this guide, you are now well-equipped to navigate the digital auto loan landscape with confidence and drive away in your dream car, knowing you’ve made a smart, informed financial decision. Start exploring your online bank car loan options today – your journey to smart car ownership begins now!