Driving Your Dreams: The Ultimate Guide to Securing a Car Loan in Illinois

Driving Your Dreams: The Ultimate Guide to Securing a Car Loan in Illinois Carloan.Guidemechanic.com

The open road, the freedom of movement, the convenience of a reliable vehicle – for many, owning a car is an essential part of daily life. Whether you’re commuting to work in Chicago, exploring the scenic routes downstate, or simply need a dependable family transporter, securing the right Car Loan Illinois is often the first step. But navigating the world of auto financing can feel like a complex journey in itself, filled with jargon, varying rates, and a multitude of options.

As an expert in auto financing, my goal with this comprehensive guide is to demystify the process for you. We’ll explore everything you need to know about obtaining a car loan in the Prairie State, from understanding your credit to finding the best rates and avoiding common pitfalls. By the time you finish reading, you’ll be equipped with the knowledge and confidence to make an informed decision and drive off with a deal that truly works for you. Let’s hit the road!

Driving Your Dreams: The Ultimate Guide to Securing a Car Loan in Illinois

Understanding the Landscape: Car Loans in Illinois

A car loan is essentially an agreement where a lender provides you with funds to purchase a vehicle, and you agree to repay that amount, plus interest, over a set period. In Illinois, the auto loan market is vibrant and competitive, offering a wide array of choices for consumers. However, specific state regulations and economic factors can influence your options and the terms you receive.

Based on my experience, understanding these foundational elements is crucial. It’s not just about getting approved; it’s about getting approved for a loan that aligns with your financial health and future goals. A well-structured Illinois auto loan can be a stepping stone to financial stability, while a poorly chosen one can create unnecessary stress.

Types of Car Loans Available in Illinois

Before diving into the application process, it’s helpful to understand the different types of car loans you might encounter. Each serves a specific purpose and comes with its own set of considerations.

1. New Car Loans

These loans are designed for purchasing brand-new vehicles directly from a dealership. Typically, new car loans offer lower interest rates and longer terms due to the vehicle’s higher value and perceived reliability. Lenders view new cars as lower risk, which translates to better terms for borrowers with good credit.

The depreciation curve for new cars is steepest in the first few years. While you might get a great rate, be mindful of how quickly the car loses value compared to your loan balance. This is an important consideration when evaluating the total cost of ownership.

2. Used Car Loans

Used car loans are for pre-owned vehicles, whether purchased from a dealership or a private seller. These loans often come with slightly higher interest rates than new car loans, as older vehicles can carry a higher risk for lenders due to potential mechanical issues and depreciation.

However, the principal amount borrowed for a used car is generally lower, making the overall loan more affordable. It’s crucial to consider the age and mileage of the used car, as these factors directly impact loan terms and eligibility in Illinois.

3. Refinancing Car Loans

Refinancing involves replacing your existing car loan with a new one, often with different terms and a lower interest rate. This can be a smart move if interest rates have dropped since you originally financed your car, if your credit score has significantly improved, or if you simply want to adjust your monthly payments.

Many Illinois residents don’t realize the potential savings from refinancing. Pro tips from us: Even a small reduction in your interest rate can save you hundreds, if not thousands, of dollars over the life of your Illinois car financing agreement.

4. Leasing vs. Buying (A Brief Consideration)

While not a loan in the traditional sense, leasing is a popular alternative to buying. When you lease, you’re essentially paying to use the vehicle for a set period, usually 2-4 years. You don’t own the car, and at the end of the lease, you return it or have the option to buy it.

Leasing often results in lower monthly payments compared to buying, and you typically get to drive a new car more frequently. However, mileage restrictions and wear-and-tear clauses are common. For a detailed comparison, considering whether buying or leasing is right for you? Our detailed article, , explores both options thoroughly.

Key Factors Affecting Your Car Loan in Illinois

Several critical elements come into play when lenders evaluate your application for an Illinois auto loan. Understanding these factors can help you prepare and position yourself for the best possible terms.

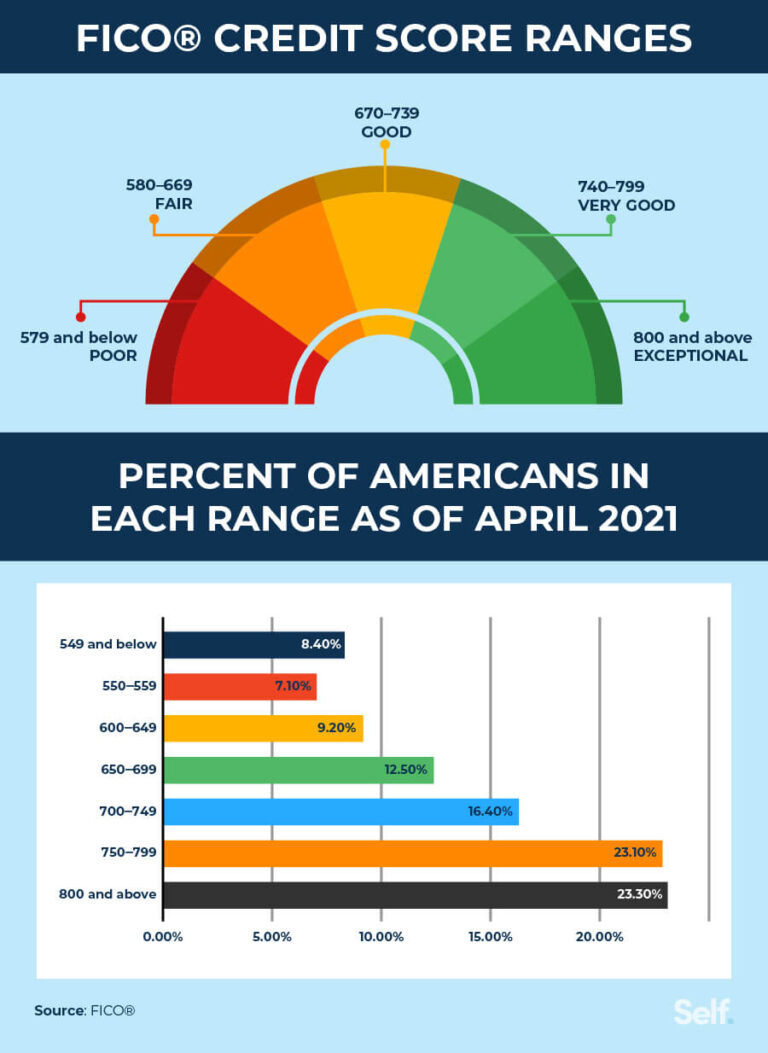

1. Your Credit Score: The Cornerstone of Approval

Your credit score is arguably the most influential factor in securing a car loan. This three-digit number, generated from your credit report, tells lenders about your financial reliability and history of debt repayment. In Illinois, as elsewhere, a higher credit score generally translates to lower interest rates and more favorable loan terms.

- Excellent Credit (720+): You’ll qualify for the most competitive rates and best offers.

- Good Credit (660-719): Still strong, you’ll likely receive good rates, though perhaps not the absolute lowest.

- Fair Credit (600-659): You might face slightly higher interest rates, but approval is still very possible.

- Poor Credit (Below 600): Securing a loan can be challenging, often requiring higher interest rates, a larger down payment, or a co-signer.

Based on my experience, improving your credit score even by a few points before applying can significantly impact your interest rate. For a deeper dive into improving your credit score before applying for an auto loan, check out our comprehensive guide on .

2. The Down Payment: Your Initial Investment

A down payment is the initial amount of money you pay upfront towards the purchase of your vehicle. While not always mandatory, making a substantial down payment can significantly benefit your car loan terms. A larger down payment reduces the amount you need to borrow, which in turn lowers your monthly payments and the total interest paid over the life of the loan.

Furthermore, a healthy down payment signals to lenders that you are a serious and responsible borrower, potentially leading to better interest rates. It also helps you avoid being "upside down" on your loan, meaning you owe more than the car is worth, a common issue with no-money-down loans.

3. Loan Term: How Long Will You Pay?

The loan term refers to the length of time you have to repay the loan, typically expressed in months (e.g., 36, 48, 60, 72 months). A shorter loan term means higher monthly payments but less interest paid overall. Conversely, a longer loan term leads to lower monthly payments but accrues more interest over time.

It’s a balancing act: you want monthly payments that are comfortable, but you also want to avoid extending the loan so long that you pay excessive interest or find yourself underwater on the car. Carefully consider your budget and the car’s expected lifespan when choosing a loan term.

4. Interest Rate (APR): The Cost of Borrowing

The interest rate, often expressed as an Annual Percentage Rate (APR), is the cost you pay to borrow money. It’s added to your principal loan amount. A lower APR means lower monthly payments and less money paid overall. This is where your credit score plays a huge role.

Understanding the APR is crucial. It’s not just the interest rate; it also includes certain fees charged by the lender, giving you a more complete picture of the total cost of your Illinois car loan. Always compare APRs, not just interest rates, when evaluating offers.

5. Debt-to-Income (DTI) Ratio

Lenders will also look at your debt-to-income (DTI) ratio, which compares your total monthly debt payments to your gross monthly income. A lower DTI ratio indicates that you have more disposable income to cover your car loan payments, making you a less risky borrower.

While there isn’t a strict universal cutoff, most lenders prefer a DTI ratio below 43%. A high DTI can make it harder to get approved or might lead to less favorable terms, even if your credit score is decent.

The Application Process for a Car Loan in Illinois

Securing an Illinois vehicle financing package involves a few key steps. Being prepared can streamline the process and reduce stress.

1. Pre-approval vs. Dealership Financing

One of the most valuable pieces of advice I can offer is to seek pre-approval from multiple lenders before you visit a dealership. Pre-approval involves a soft credit pull (which doesn’t harm your score) and gives you a clear idea of how much you can borrow, at what interest rate, and what your estimated monthly payments will be.

- Benefits of Pre-approval:

- You know your budget before you shop, preventing you from falling in love with a car you can’t afford.

- It gives you leverage when negotiating with dealerships. You have an outside offer to compare against their financing options.

- It separates the car-buying decision from the financing decision, making each clearer.

Dealerships also offer financing, often through their network of lenders. While convenient, it’s always best to have a pre-approval in hand to ensure you’re getting a competitive rate. Don’t assume the dealership’s first offer is the best one.

2. Required Documentation

When applying for a car loan, whether directly with a bank or through a dealership, you’ll typically need to provide several documents. Gathering these in advance can speed up the approval process.

- Proof of Identity: Driver’s license or state ID.

- Proof of Income: Pay stubs (from the last 1-2 months), W-2 forms, tax returns (if self-employed).

- Proof of Residency: Utility bill, lease agreement, or mortgage statement.

- Social Security Number: For credit checks.

- Vehicle Information: If you’ve already chosen a car (VIN, make, model, year, mileage).

- Insurance Information: Proof of auto insurance is usually required before you can drive off the lot.

3. Steps to Apply

- Check Your Credit: Obtain your credit report and score from all three major bureaus (Experian, Equifax, TransUnion). Correct any errors.

- Determine Your Budget: Realistically assess how much you can afford for a monthly payment, factoring in insurance, fuel, and maintenance.

- Gather Documents: Collect all necessary paperwork as listed above.

- Shop Around for Lenders: Contact banks, credit unions, and online lenders for pre-approval. Get at least 2-3 offers.

- Compare Offers: Look beyond just the monthly payment. Compare APRs, loan terms, and any associated fees.

- Visit Dealerships (or Private Sellers): With your pre-approval in hand, negotiate the car price. Then, compare the dealership’s financing offer with your pre-approval.

- Finalize the Loan: Once you’ve chosen a car and a loan, review all documents carefully before signing.

Finding the Best Car Loan Rates in Illinois

Securing a competitive interest rate for your Illinois car loan can save you thousands of dollars over the life of the loan. This is where diligent shopping around truly pays off.

1. Shopping Around: Don’t Settle for the First Offer

- Banks: Traditional banks often offer competitive rates, especially if you have an existing relationship with them.

- Credit Unions: Known for their member-focused approach, credit unions often provide some of the lowest interest rates. Consider joining one if you’re eligible.

- Online Lenders: A growing number of online platforms specialize in auto loans, offering quick approvals and competitive rates, often with streamlined application processes.

- Dealerships: While convenient, dealership financing should be compared against external offers. They may have incentives, but sometimes their rates are higher.

Pro tips from us: Always get a pre-approval from at least two different lenders before stepping foot in a dealership. This empowers you with leverage and ensures you have a benchmark against which to compare any offers from the dealer.

2. Negotiating Tips

Negotiating the car price and the loan terms are separate but related processes. Focus on one at a time. First, negotiate the best possible price for the vehicle. Once that’s settled, then discuss financing.

Be prepared to walk away if the terms aren’t favorable. There are always other cars and other lenders. Don’t feel pressured into a deal that doesn’t feel right.

Navigating Bad Credit Car Loans in Illinois

Having a less-than-perfect credit score doesn’t mean you can’t get an Illinois auto loan. It simply means the process might require a different strategy and you might face higher interest rates.

Is It Possible? Yes!

Many lenders specialize in "subprime" loans for individuals with poor credit. While these loans come with higher APRs to offset the increased risk, they can be a crucial step towards rebuilding your credit. Making timely payments on a bad credit car loan can significantly improve your credit score over time.

Strategies for Approval with Bad Credit

- Larger Down Payment: A substantial down payment reduces the loan amount and signals to lenders that you’re committed, lowering their risk.

- Co-signer: A co-signer with good credit can significantly improve your chances of approval and help you secure a lower interest rate. Their credit history will be used to back the loan, so choose someone you trust and who understands the responsibility.

- Secured Loan: Some lenders might offer a secured loan, using the car itself as collateral. This can make approval easier, but be aware of the implications if you default.

- Subprime Lenders: Seek out lenders who specifically cater to borrowers with bad credit. They are more accustomed to these situations and have tailored programs.

- Smaller Loan Amount: Consider a more affordable, used vehicle to keep the loan amount lower, reducing the lender’s risk.

Common mistakes to avoid when seeking a bad credit car loan in Illinois include: only applying at one place, not having any down payment, and agreeing to exorbitant interest rates without understanding the long-term cost. Always compare offers, even with bad credit.

Understanding Your Car Loan Agreement in Illinois

Once you’ve been approved, carefully reviewing your loan agreement is paramount. This legal document outlines all the terms and conditions of your Illinois car financing. Don’t rush through it!

Key Terms to Look For:

- Principal Loan Amount: The actual amount of money you are borrowing for the car.

- Interest Rate/APR: The annual cost of your loan, including certain fees.

- Loan Term: The duration of your repayment period.

- Monthly Payment: The fixed amount you’ll pay each month.

- Total Cost of Loan: The sum of the principal and all interest/fees over the entire loan term. This figure reveals the true expense of your financing.

- Prepayment Penalties: Check if there are any fees for paying off your loan early. Many modern auto loans do not have these, but it’s essential to confirm.

- Late Payment Fees: Understand the penalties for missed or late payments.

- Default Clauses: Know what constitutes a default on the loan and the consequences.

Illinois has specific consumer protection laws related to auto financing. For example, the state’s Predatory Lending Database Program aims to protect consumers from abusive lending practices. Always ensure your lender is licensed and adheres to state regulations. If anything seems unclear or unfair, ask questions or seek independent advice.

Refinancing Your Car Loan in Illinois

Refinancing an existing car loan Illinois can be a smart financial move under certain circumstances. It’s essentially taking out a new loan to pay off your current one, ideally with more favorable terms.

When and Why to Consider It:

- Improved Credit Score: If your credit score has significantly increased since you first took out the loan, you likely qualify for a lower interest rate.

- Lower Interest Rates: The market interest rates may have dropped, making refinancing an attractive option.

- Reduced Monthly Payments: If your financial situation has changed and you need lower monthly payments, refinancing with a longer term can achieve this (though you’ll pay more interest overall).

- Remove a Co-signer: If your credit has improved, you might be able to refinance and remove a co-signer from the loan.

The Process:

The refinancing process is similar to applying for an initial car loan. You’ll need to shop around with different lenders, submit an application, and provide documentation. Once approved for the new loan, the funds will be used to pay off your old loan, and you’ll begin making payments to your new lender.

Common Pitfalls and How to Avoid Them

Based on my experience working with countless car buyers in Illinois, one of the most critical steps often overlooked is simply being informed. Avoid these common mistakes:

- Not Reading the Fine Print: Never sign a document you haven’t thoroughly read and understood. Ask questions until everything is clear.

- Ignoring Your Credit Score: Your credit score is your financial resume. Knowing it and working to improve it before applying can save you a lot of money.

- Focusing Only on Monthly Payments: Dealerships might try to "stretch" the loan term to make monthly payments seem affordable, even if it means paying significantly more in interest over time. Always consider the total cost of the loan.

- Impulse Buying: Buying a car is a major financial decision. Take your time, research, compare, and don’t let emotion override logic.

- Neglecting Pre-approval: Walking into a dealership without a pre-approval is like going to a battle without armor. You lose valuable negotiating power.

Resources for Illinois Car Buyers

For additional information and to ensure you’re compliant with all state regulations, here are some helpful resources:

- Illinois Secretary of State (SOS) – Vehicle Services: The official source for information on vehicle titling, registration, and driver services in Illinois. This is crucial for understanding the post-purchase paperwork.

- Consumer Financial Protection Bureau (CFPB): A federal agency that provides resources and information on various financial products, including auto loans.

- Illinois Attorney General’s Office: Offers consumer protection resources and can be a point of contact for complaints regarding unfair business practices.

Driving Forward with Confidence

Securing a Car Loan Illinois doesn’t have to be a daunting task. By understanding the different types of loans, the factors that influence your eligibility and rates, and the application process, you can approach the experience with confidence and make choices that serve your financial best interests.

Remember to shop around, compare offers, and never hesitate to ask questions. Your journey to car ownership in Illinois should be as smooth and enjoyable as the open road ahead. Happy driving!