Driving Your Dreams: The Ultimate Guide to Securing a Car Loan Under $10,000

Driving Your Dreams: The Ultimate Guide to Securing a Car Loan Under $10,000 Carloan.Guidemechanic.com

The dream of owning a reliable vehicle doesn’t always have to come with a hefty price tag. For many, a car priced under $10,000 represents the perfect balance of affordability and functionality. Whether you’re a first-time buyer, looking for a dependable second car, or simply aiming to keep your monthly expenses low, financing a pre-owned vehicle can be a smart move.

However, navigating the world of car loans under $10k can seem daunting. From understanding your credit score to finding the right lender, there are many factors to consider. This comprehensive guide is designed to empower you with the knowledge and strategies needed to secure an affordable car loan, drive away with confidence, and make a financially sound decision.

Driving Your Dreams: The Ultimate Guide to Securing a Car Loan Under $10,000

Why a Car Under $10,000 Makes Smart Financial Sense

Choosing a vehicle in the sub-$10,000 range isn’t about compromising; it’s about making a strategic financial decision. There are compelling reasons why this budget often proves to be an excellent sweet spot for many buyers. Understanding these benefits can solidify your choice and provide peace of mind.

Cost-Effectiveness and Depreciation Savings

One of the most significant advantages of buying a used car, especially one under $10,000, is avoiding the steepest depreciation curve. New cars lose a substantial portion of their value in the first few years. By letting someone else absorb that initial drop, you get more car for your money.

This means your investment holds its value better over time. You’re essentially buying into the "sweet spot" where the car has depreciated significantly but still has plenty of life left. It’s a smart way to get reliable transportation without the rapid value loss associated with brand-new models.

Lower Insurance Premiums and Registration Fees

Generally, the older and less expensive a vehicle is, the lower its insurance premiums will be. Insurance companies assess risk based on the car’s value, repair costs, and theft rates. A car under $10,000 often translates to noticeable savings on your monthly or annual insurance payments.

Similarly, many states base registration fees on a vehicle’s value or age. A more affordable car typically means lower registration costs, further reducing your overall ownership expenses. These small savings add up, making your budget go further.

Ideal for First-Time Buyers or as a Second Vehicle

For those new to car ownership, a sub-$10,000 vehicle offers an excellent entry point. It allows you to build credit, understand the responsibilities of car ownership, and gain driving experience without a massive financial commitment. It’s a lower-stakes way to get on the road.

Moreover, if you need a reliable second car for commuting, running errands, or for a new driver in the family, a budget-friendly option is perfect. It serves its purpose effectively without straining your household budget, providing flexibility and convenience.

What to Look For in a Sub-$10k Vehicle

Finding a reliable car under $10,000 requires a keen eye and a strategic approach. It’s not just about the price tag; it’s about the value, longevity, and overall condition of the vehicle. Prioritizing certain characteristics can save you from future headaches and unexpected repair bills.

Prioritize Reliability and Reputation

Based on my experience, certain car manufacturers consistently produce vehicles known for their longevity and lower maintenance costs. Brands like Toyota, Honda, Mazda, and some Ford and Chevrolet models often prove to be excellent choices in the used car market. These brands have a track record of building durable engines and robust components.

While any car can have issues, models from these manufacturers generally offer a better chance of trouble-free ownership. Research specific models and their common issues before you even step foot on a dealership lot. Online forums and consumer reports are invaluable resources for this.

Mileage Considerations: Not Just a Number

High mileage doesn’t always equate to a bad car, especially if it’s highway mileage and has been well-maintained. Conversely, low mileage on a very old car might indicate it sat unused for long periods, which can lead to its own set of problems. The key is balance and context.

A car with 100,000 to 150,000 miles can still have many years of life left if it has a documented service history. What truly matters is how those miles were accumulated and how well the car was cared for. Don’t immediately dismiss a car based solely on its odometer reading.

The Indispensable Maintenance History

This is perhaps the most crucial factor when buying any used car, particularly one under $10,000. A detailed maintenance history tells you a story about the car’s past. Look for records of regular oil changes, tire rotations, fluid flushes, and any major repairs.

A car with a complete service record, even if it has higher mileage, is often a safer bet than a lower-mileage car with no history. It shows the previous owner took care of their investment, indicating a higher likelihood of future reliability. Don’t be afraid to ask for these records.

The Car Loan Under $10k Application Process – Your Roadmap to Approval

Securing a car loan under $10k requires preparation and a clear understanding of the lending landscape. Knowing what lenders look for and how to present yourself as a reliable borrower can significantly improve your chances of approval and help you snag the best rates.

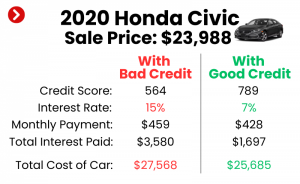

Understanding Your Credit Score: The Foundation of Your Loan

Your credit score is a numerical representation of your creditworthiness. It tells lenders how responsibly you’ve managed debt in the past. For a car loan, especially one under $10,000, a good credit score (typically 670 and above) can unlock lower interest rates and better terms.

Even with a lower score, approval is possible, but you might face higher interest rates. It’s crucial to check your credit score and report before applying for any loan. You can get free copies of your credit report annually from Equifax, Experian, and TransUnion. Review it for any errors that could be negatively impacting your score.

Budgeting Realistically: Beyond the Car Price

When planning for a car loan under $10k, it’s vital to consider the total cost of ownership, not just the purchase price and monthly loan payment. Factor in ongoing expenses like insurance premiums, fuel costs, routine maintenance (oil changes, tire rotations), and potential repairs.

Pro tips from us: Create a detailed monthly budget that includes all these costs. This realistic financial picture will help you determine an affordable monthly payment and ensure you can comfortably manage your new vehicle without financial strain. Overlooking these additional costs is a common mistake.

Gathering Necessary Documents: Be Prepared

Lenders require specific documents to verify your identity, income, and residence. Having these ready before you apply can streamline the process. Common documents include:

- Proof of Identity: Driver’s license or state ID.

- Proof of Income: Recent pay stubs (usually 2-3 months), W-2s, or tax returns if self-employed.

- Proof of Residence: Utility bill, lease agreement, or mortgage statement.

- Social Security Number: For credit checks.

Being organized and presenting all required information promptly demonstrates your seriousness and reliability as a borrower. This preparation can make a big difference in how quickly your loan application is processed.

Exploring Loan Options: Banks, Credit Unions, Online Lenders, and Dealerships

You have several avenues for securing a car loan under $10k. Each has its own advantages:

- Banks: Traditional banks often offer competitive rates for borrowers with good credit. They provide a sense of security and established processes.

- Credit Unions: Known for their member-focused approach, credit unions often have more flexible lending criteria and potentially lower interest rates, especially for members.

- Online Lenders: These lenders have grown in popularity due to their quick application processes and ability to cater to a wider range of credit scores. Some specialize in bad credit car loans.

- Dealership Financing: While convenient, dealership financing sometimes includes markups on interest rates. However, they can also offer promotional rates or work with a network of lenders to find an option.

It’s wise to shop around and get pre-approved from a few different sources before visiting a dealership. This gives you leverage and a clear understanding of what kind of rate you qualify for.

Down Payments: Boosting Your Approval Chances

While not always mandatory for a car loan under $10k, making a down payment significantly strengthens your application. A down payment reduces the amount you need to borrow, which in turn lowers your monthly payments and the total interest paid over the life of the loan.

Lenders view down payments favorably because they reduce their risk and show your commitment. Even a small down payment of 10-20% can make a substantial difference, especially if your credit score isn’t perfect. It demonstrates financial responsibility and reduces the loan-to-value ratio.

Interest Rates: What Influences Them and How to Get the Best Rate

Interest rates on car loans under $10k are influenced by several factors:

- Your Credit Score: The higher your score, the lower your rate.

- Loan Term: Shorter loan terms generally have lower interest rates.

- Loan Amount: Smaller loans sometimes have slightly higher rates due to administrative costs.

- Market Conditions: Overall economic factors can impact rates.

- Lender: Different lenders have different rate structures.

To secure the best rate, focus on improving your credit score, making a down payment, and shopping around. Don’t be afraid to negotiate, especially if you have pre-approval offers from multiple lenders.

Loan Terms: Finding the Right Balance

For a car loan under $10k, you’ll typically see loan terms ranging from 24 to 60 months. A shorter term (e.g., 24-36 months) means higher monthly payments but less interest paid overall. A longer term (e.g., 48-60 months) reduces your monthly payment, making it more affordable in the short term, but you’ll pay more interest over time.

Consider your budget and financial goals when choosing a loan term. Pro tips from us: Aim for the shortest term you can comfortably afford to minimize interest costs. For an affordable vehicle, avoiding a stretched-out loan term can save you hundreds in the long run.

Common Mistakes to Avoid When Seeking a Car Loan Under $10k

Even with careful planning, it’s easy to fall into common traps when seeking an affordable car loan. Being aware of these pitfalls can help you steer clear of financial missteps and ensure a smoother purchasing experience.

Not Checking Your Credit Score First

One of the most common mistakes to avoid are diving into the loan application process without knowing your credit standing. Your credit score dictates the interest rates and terms you’ll be offered. Not knowing it means you can’t accurately budget or negotiate effectively.

Always pull your credit report and score first. This allows you to identify any errors, understand your position, and even take steps to improve your score if needed before applying. It’s your financial report card.

Ignoring the Total Cost of Ownership

As discussed, focusing solely on the monthly payment or the car’s sticker price is a major oversight. Insurance, fuel, maintenance, registration, and potential repair costs can quickly add up, turning an "affordable" car into a financial burden.

Always factor in these ongoing expenses. A car might seem cheap upfront, but if its parts are expensive, or it’s known for frequent breakdowns, it won’t be cheap in the long run. Comprehensive budgeting is key.

Skipping a Pre-Purchase Inspection (PPI)

For any used car, especially one under $10,000, neglecting a professional pre-purchase inspection is a gamble. What looks good on the surface might hide costly mechanical issues underneath. This is an absolutely non-negotiable step.

A reputable independent mechanic can identify existing problems or potential future issues, giving you valuable negotiating power or helping you avoid a lemon. Think of it as an insurance policy for your used car purchase. For more in-depth information, check out our guide on .

Rushing into the First Loan Offer

It’s tempting to accept the first car loan under $10k offer you receive, especially if you’re eager to get a car. However, different lenders will offer different rates and terms based on their risk assessment and business models. This is where comparison shopping becomes vital.

Take the time to compare offers from at least three different lenders: your bank, a credit union, and an online lender. This comparison shopping can save you hundreds, if not thousands, of dollars in interest over the life of the loan. Don’t let convenience override common sense.

Pro Tips for Securing the Best Deal

Getting a great deal on your car loan under $10k goes beyond simply finding a low-priced vehicle. Strategic planning and informed negotiation can significantly improve your overall outcome.

Get Pre-Approved Before You Shop

One of the most powerful tools in your arsenal is a pre-approval letter from a bank or credit union. This tells you exactly how much you can borrow and at what interest rate before you even step foot in a dealership. It puts you in a strong negotiating position.

With pre-approval, you walk into the dealership as a cash buyer, focusing solely on the car’s price rather than being swayed by financing options. It gives you confidence and leverage.

Negotiate the Car Price Before Discussing Financing

This is a classic negotiation strategy. Always finalize the vehicle’s purchase price before you start talking about financing. If you combine both negotiations, a salesperson might shift costs around, making it difficult to tell if you’re getting a good deal on the car or the loan.

Focus on getting the lowest possible price for the vehicle first. Once that’s settled, then you can present your pre-approved loan offer and compare it to any financing the dealership might offer.

Be Wary of Add-Ons and Extended Warranties

Dealerships often try to upsell buyers on various add-ons like extended warranties, paint protection, or VIN etching. While some might offer legitimate value for certain vehicles, many are overpriced and cut into the affordability of your car loan under $10k.

Carefully evaluate any add-on. Ask if it’s truly necessary and if the cost justifies the benefit. Often, you can purchase similar protection from third parties for less. Remember, every add-on increases your loan amount and thus your interest payments.

Consider a Co-Signer if Your Credit Needs a Boost

If your credit score is on the lower side, or you’re a young borrower with limited credit history, a co-signer can significantly improve your chances of getting approved for a car loan under $10k and securing a better interest rate.

A co-signer is someone with good credit who agrees to be equally responsible for the loan if you default. This reduces the lender’s risk. However, ensure both parties understand the full implications, as it impacts the co-signer’s credit as well.

The Importance of a Pre-Purchase Inspection (PPI)

We’ve touched on this before, but its importance cannot be overstated, especially when dealing with a car loan under $10k. These vehicles, by nature of their price point, are older and likely have more miles, making a thorough inspection absolutely critical.

Why It’s Non-Negotiable for Used Cars

A PPI provides an objective assessment of the vehicle’s condition from an independent mechanic. The seller might highlight the car’s good points, but a mechanic will uncover potential problems, worn components, or signs of past accidents that might not be visible to the untrained eye. This prevents you from inheriting someone else’s problems.

It’s about protecting your investment and ensuring that the car you’re about to finance is mechanically sound. Spending a small fee (typically $100-$200) on a PPI can save you thousands in unexpected repairs down the line. It’s truly money well spent.

What a Mechanic Looks For

During a PPI, the mechanic will perform a comprehensive check of the vehicle, including:

- Engine & Transmission: Checking for leaks, unusual noises, fluid condition, and overall performance.

- Brakes: Pads, rotors, lines, and fluid levels.

- Suspension & Steering: Shocks, struts, tie rods, and power steering system.

- Tires: Tread depth, uneven wear, and overall condition.

- Electrical System: Lights, battery, alternator, and any warning lights on the dashboard.

- Frame & Body: Signs of rust, accident damage, or shoddy repairs.

- Fluids: Oil, coolant, brake fluid, transmission fluid.

- Diagnostic Scan: Checking for any stored error codes.

This detailed report will give you a clear picture of the car’s health. You can use any identified issues to negotiate a lower price or decide to walk away from a problematic vehicle.

After the Loan: Smart Ownership of Your Under-$10k Car

Securing your car loan under $10k is a significant achievement, but the journey doesn’t end there. Smart ownership practices are essential to maximize the lifespan of your vehicle, keep running costs low, and protect your investment.

Establish a Regular Maintenance Schedule

Older cars thrive on consistent care. Adhering to the manufacturer’s recommended maintenance schedule is paramount. This includes regular oil changes, tire rotations, fluid checks, and timely replacement of wear-and-tear items like spark plugs and air filters.

Based on my experience, preventative maintenance is far cheaper than reactive repairs. A small investment in routine servicing can prevent major, costly breakdowns. Keep meticulous records of all maintenance performed.

Build an Emergency Fund for Repairs

Even the most reliable used cars will eventually need repairs. It’s an unavoidable part of car ownership. Having an emergency fund specifically for vehicle repairs can save you from financial stress and potentially going into further debt.

Aim to set aside a few hundred dollars specifically for car-related emergencies. This financial cushion ensures you can address unexpected issues promptly, preventing minor problems from escalating into major ones.

Revisit Your Insurance Considerations

While your insurance premiums might be lower for a car under $10,000, it’s still crucial to have adequate coverage. Review your policy periodically to ensure it meets your needs and budget. Consider factors like collision coverage deductibles and roadside assistance.

As the car ages and its value potentially decreases, you might consider adjusting your coverage levels. However, always ensure you’re protected against major financial losses. For more details on vehicle valuation, a trusted external source like Kelley Blue Book (KBB.com) can provide useful insights into your car’s worth.

Conclusion: Driving Forward with Confidence

Securing a car loan under $10k is an achievable goal for many, opening doors to reliable transportation without breaking the bank. By approaching the process with knowledge, preparation, and a strategic mindset, you can navigate the complexities of financing and drive away with a vehicle that perfectly suits your needs and budget.

Remember to prioritize a thorough vehicle inspection, understand your credit, shop around for the best loan terms, and always consider the total cost of ownership. With these insights, you’re not just buying a car; you’re making a smart, informed investment in your mobility and financial future. Drive confidently, knowing you’ve made a well-researched and savvy decision.