Driving Your Dreams: The Ultimate Guide to Securing a Car Loan (Your 24 Apr Compass)

Driving Your Dreams: The Ultimate Guide to Securing a Car Loan (Your 24 Apr Compass) Carloan.Guidemechanic.com

The thrill of a new car, the freedom of the open road – for many, it’s a quintessential part of the modern dream. But bringing that dream to life often starts with a crucial step: securing a car loan. Whether you’re eyeing a shiny new model or a reliable pre-owned vehicle, understanding the intricacies of auto financing is paramount. As we approach April 24th, or perhaps as you read this comprehensive guide on that very day, the landscape of car loans might seem complex, but with the right knowledge, you can navigate it with confidence and secure the best deal possible.

This isn’t just another article; it’s your definitive compass, meticulously crafted to guide you through every twist and turn of the car loan journey. We’ll delve deep into the preparation, application, and management of vehicle financing, ensuring you’re equipped with the insights needed to make informed decisions. Our ultimate goal is to empower you to drive away with not just a car, but a smart financial choice that aligns perfectly with your budget and aspirations. Let’s embark on this journey together.

Driving Your Dreams: The Ultimate Guide to Securing a Car Loan (Your 24 Apr Compass)

Understanding the Car Loan Landscape: Your Financial Foundation

Before you even step foot into a dealership or browse online listings, it’s vital to grasp the fundamental concepts of a car loan. This foundational knowledge will serve as your shield against confusing terms and ensure you’re speaking the same language as lenders. A car loan, at its core, is a secured loan used specifically to purchase a vehicle. The car itself acts as collateral, meaning if you fail to make your payments, the lender has the right to repossess it.

This understanding is critical because it directly impacts the lender’s risk assessment and, consequently, the terms they offer you. Unlike an unsecured personal loan, where no collateral is involved, a car loan typically offers lower interest rates due to this reduced risk for the lender. Knowing this distinction helps you evaluate different financing options more effectively. It’s the first step in becoming an empowered borrower.

What is a Car Loan, Really?

A car loan is essentially an agreement between you (the borrower) and a financial institution (the lender) where the lender provides you with a sum of money to purchase a vehicle. In return, you agree to repay that sum, known as the principal, plus an additional amount, which is the interest, over a predetermined period. This repayment is typically structured into fixed monthly installments.

The duration of this repayment period, known as the loan term, can vary significantly, often ranging from 24 months to as long as 84 months, or even more in some cases. Each payment you make chips away at both the principal amount borrowed and the interest accrued. A clear understanding of this basic mechanism allows you to project your long-term financial commitment.

Decoding Key Terms: APR, Principal, Interest, and Loan Term

Navigating car loan offers requires familiarity with specific financial jargon. The Annual Percentage Rate (APR) is perhaps the most crucial figure. It represents the total cost of borrowing money over a year, expressed as a percentage. Unlike a simple interest rate, the APR includes not only the interest charged but also any additional fees, such as origination fees, rolled into the loan. This makes APR a more accurate measure for comparing different loan offers.

The principal is the initial amount of money you borrow to purchase the car. If you borrow $25,000, that’s your principal. Interest is the cost of borrowing that principal, expressed as a percentage of the principal over a year. The loan term is the duration over which you agree to repay the loan, usually measured in months. A shorter loan term means higher monthly payments but less interest paid overall, while a longer term offers lower monthly payments but accrues more total interest. Comprehending these terms empowers you to truly compare apples to apples when reviewing loan offers.

The Foundation: Preparing for Your Car Loan Journey

Securing a favorable car loan isn’t a spontaneous act; it’s a meticulously planned endeavor. The groundwork you lay before even applying can significantly influence the rates and terms you’re offered. This preparatory phase involves self-assessment, financial hygiene, and strategic planning. Skipping these crucial steps is a common mistake that can lead to higher costs and less desirable outcomes.

Based on my experience in the financial sector, the most successful car loan applicants are those who approach the process with diligence and foresight. They understand that lenders assess risk, and by proactively addressing potential concerns, they present themselves as reliable borrowers. This proactive approach saves both time and money in the long run.

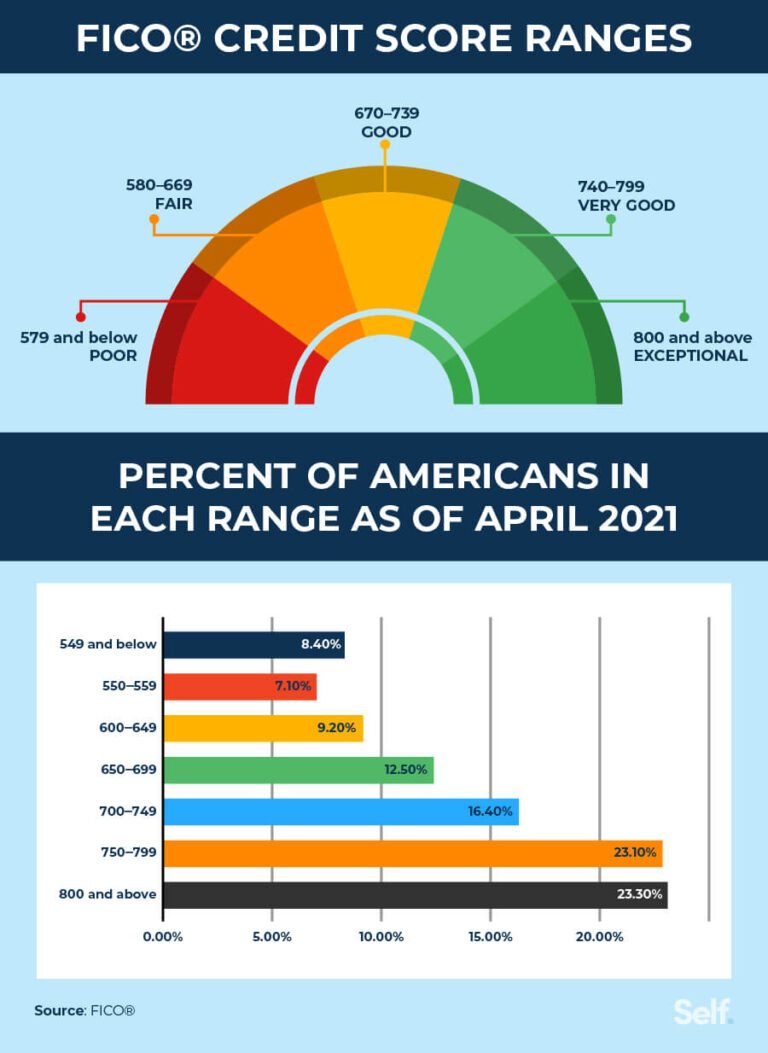

Your Credit Score: The Unsung Hero of Car Loans

Your credit score is arguably the single most influential factor in determining your car loan eligibility and interest rate. It’s a three-digit number that summarizes your creditworthiness, reflecting your history of borrowing and repaying debt. Lenders use this score as a quick indicator of how likely you are to repay your new car loan on time. A higher credit score signals lower risk to lenders, which typically translates into lower interest rates and more favorable terms for you.

Conversely, a lower credit score might still allow you to get a loan, but often at significantly higher interest rates, increasing the overall cost of your vehicle. It’s not just about getting approved; it’s about getting approved for a loan that doesn’t burden you excessively. Understanding your credit score is the first step towards leveraging it to your advantage.

How to Check and Improve Your Credit Score

Before applying for any loan, obtain a copy of your credit report from all three major credit bureaus (Equifax, Experian, and TransUnion). You can do this for free annually through AnnualCreditReport.com. Review these reports meticulously for any errors or inaccuracies, as even small mistakes can negatively impact your score. Disputing errors promptly can lead to a quick boost in your score.

To improve your score, focus on consistent, on-time payments for all your existing debts. Reduce your credit card balances to lower your credit utilization ratio, ideally keeping it below 30%. Avoid opening new credit accounts unnecessarily in the months leading up to your car loan application, as this can temporarily lower your score. Patience and disciplined financial habits are key to cultivating a strong credit profile. For more detailed strategies on boosting your financial standing, you might find our article on Improving Your Financial Health Before Major Purchases particularly helpful.

Budgeting Wisely: Knowing What You Can Truly Afford

One of the most common mistakes prospective car buyers make is falling in love with a car they can’t genuinely afford. Your car loan payment is just one piece of the puzzle. You also need to factor in insurance, fuel, maintenance, registration, and potential repairs. A wise budget considers all these ongoing costs, not just the monthly loan installment.

Pro tips from us: Create a comprehensive budget that includes all your monthly income and expenses. Calculate how much disposable income you genuinely have available for a car payment and all related vehicle expenses. A good rule of thumb is that your total vehicle expenses (loan, insurance, fuel, maintenance) should not exceed 10-15% of your gross monthly income. This realistic assessment prevents future financial strain.

The Power of a Down Payment

Making a substantial down payment is one of the smartest moves you can make when financing a car. A larger down payment immediately reduces the principal amount you need to borrow, which in turn lowers your monthly payments and the total interest you’ll pay over the life of the loan. It also signals to lenders that you are a serious and responsible borrower, potentially leading to better interest rates.

Furthermore, a significant down payment helps you avoid becoming "upside down" on your loan, a situation where you owe more on the car than it’s worth. This commonly happens early in the loan term due to depreciation. Aiming for at least 10-20% of the car’s purchase price as a down payment is often recommended, with 20% or more being ideal for new cars. This financial cushion offers both immediate and long-term benefits.

Navigating the Application Process: Your Path to Approval

Once you’ve done your homework and solidified your financial position, it’s time to engage with lenders. This phase involves gathering necessary documentation, exploring different lending avenues, and understanding the strategic advantage of pre-approval. Approaching the application process systematically can significantly streamline your experience and increase your chances of securing favorable terms.

Remember, the goal isn’t just to get approved, but to get approved for a loan that aligns with your financial well-being. By being prepared and proactive, you maintain control over the process, rather than being at the mercy of the lender or dealership. This control is your most valuable asset during this stage.

Pre-Approval: Your Secret Weapon in Car Buying

Obtaining a car loan pre-approval is arguably the most powerful tool a car buyer can possess. Pre-approval means a lender has reviewed your financial information and provisionally agreed to lend you a specific amount of money at a particular interest rate, before you’ve even chosen a car. It gives you a firm offer in hand, acting like cash when you walk into a dealership.

Why is it so crucial? Firstly, it separates the financing negotiation from the car price negotiation. You can focus purely on getting the best deal on the vehicle, knowing your financing is already secured. Secondly, it provides a benchmark. If the dealership offers you financing, you’ll have your pre-approval to compare against, ensuring you don’t accept a less favorable rate. This empowers you to walk away from high-pressure sales tactics.

Gathering Your Documents: A Checklist for Success

Lenders require a specific set of documents to process your car loan application. Having these readily available will expedite the process and demonstrate your preparedness. While requirements can vary slightly between lenders, a common checklist includes:

- Proof of Identity: Government-issued ID (driver’s license, passport).

- Proof of Income: Recent pay stubs (typically 1-2 months), W-2 forms, tax returns (especially for self-employed individuals).

- Proof of Residence: Utility bills, lease agreement, or mortgage statement.

- Social Security Number: For credit checks.

- Bank Account Information: For setting up automatic payments.

Ensure all documents are current and accurate. Presenting a complete and organized application package signals responsibility and can make a positive impression on lenders. This attention to detail reflects your seriousness as a borrower.

Where to Apply: Exploring Your Lending Options

You have several avenues when it comes to securing a car loan, and each comes with its own set of advantages and disadvantages. Exploring all these options before committing is a smart strategy to find the best fit for your needs.

- Banks: Traditional banks are a common source for auto loans. They often offer competitive rates, especially if you’re an existing customer with a good relationship. They provide a sense of security and often have established online application processes.

- Credit Unions: These member-owned financial cooperatives are renowned for offering some of the lowest interest rates on car loans. Their focus is on member benefits rather than shareholder profits. Joining a credit union is often straightforward and worth exploring.

- Online Lenders: The digital age has brought forth numerous online lenders specializing in auto loans. They often offer quick approvals and competitive rates, with the convenience of applying from home. Companies like LightStream or Capital One Auto Finance are popular examples.

- Dealership Financing: While convenient, securing financing directly through the dealership can sometimes lead to higher interest rates, as they may add a markup to the loan offered by their partner lenders. However, dealerships occasionally offer promotional rates or incentives, particularly for new vehicles, which can be attractive. Always compare their offer with your pre-approval.

By comparing offers from at least three different sources, you significantly increase your chances of finding the most favorable terms available to you.

Understanding Loan Offers and Terms: The Fine Print Matters

Once you start receiving loan offers, the real work of comparison begins. It’s not enough to just look at the monthly payment; a deep dive into the underlying terms and conditions is essential. Overlooking critical details can lead to unexpected costs and long-term financial implications. This is where your financial literacy truly pays off.

Common mistakes to avoid are focusing solely on the lowest monthly payment without considering the total cost of the loan. A seemingly low monthly payment over a very long term can result in significantly more interest paid overall. Always look at the bigger picture and understand every clause of the agreement.

APR vs. Interest Rate: Why the Difference is Critical

We touched on this earlier, but it bears repeating: the APR (Annual Percentage Rate) is the true cost of borrowing, while the interest rate is just one component of that cost. The interest rate is the percentage charged on the principal amount of your loan. However, the APR includes the interest rate plus any additional fees associated with the loan, such as processing fees or administrative charges.

When comparing loan offers, always use the APR as your primary metric. A loan with a slightly lower interest rate but high fees could end up being more expensive than a loan with a slightly higher interest rate but no additional fees. The APR gives you the most accurate snapshot of the total annual cost of your credit. It’s the standard metric for a reason.

The Impact of Loan Term: Short vs. Long

The loan term, or the duration of your repayment period, profoundly impacts both your monthly payment and the total cost of the loan.

- Shorter Loan Terms (e.g., 36 or 48 months): These typically come with higher monthly payments because you’re repaying the principal over a shorter period. However, you’ll pay significantly less interest over the life of the loan. This option is ideal if you can comfortably afford the higher payments and want to be debt-free sooner.

- Longer Loan Terms (e.g., 60, 72, or 84 months): These offer lower monthly payments, making the car seem more affordable on a month-to-month basis. The trade-off is that you’ll pay substantially more in total interest over the longer term. You also risk owing more than the car is worth for a longer period due to depreciation. This option might be necessary for budget constraints but should be approached with caution.

Carefully consider your financial situation and long-term goals when choosing a loan term. Balancing affordability with the total cost of the loan is key.

Hidden Fees to Watch Out For

While the APR helps encompass many fees, some charges can still catch unsuspecting borrowers off guard. Always scrutinize your loan agreement for these potential hidden costs:

- Origination Fees: A fee charged by the lender for processing the loan.

- Prepayment Penalties: Some loans penalize you for paying off your loan early. This is less common with auto loans but still worth checking.

- Late Payment Fees: Standard across most loans, but understand the grace period and fee amount.

- Documentation Fees (Doc Fees): Often charged by dealerships for preparing paperwork. These can sometimes be negotiable.

- Gap Insurance: While not a "fee" in the traditional sense, it’s an optional add-on that protects you if your car is totaled and you owe more than its market value. While potentially valuable, ensure you understand its cost and whether it’s truly necessary for your situation.

Reading every line of the loan contract before signing is non-negotiable. Don’t hesitate to ask questions about anything you don’t understand.

Beyond Approval: Finalizing and Managing Your Loan

Congratulations, you’ve been approved! But the journey isn’t over yet. The final stages involve careful review of documents, smart negotiation, and responsible loan management. These steps ensure that the positive experience of getting approved translates into a smooth and financially sound ownership period. This is where you lock in all the hard work you’ve put in.

Based on my experience, many people get excited at this stage and rush through the final paperwork. This is a critical error. A moment of haste can lead to years of regret. Take your time, stay diligent, and protect your interests.

Reading the Fine Print: What to Scrutinize Before Signing

Before you put pen to paper, meticulously review every detail of the loan agreement. This document is legally binding, and once signed, it’s difficult to alter. Pay close attention to:

- The agreed-upon APR: Does it match what you were offered?

- The total loan amount: Is it correct?

- The loan term: Is the number of months accurate?

- Monthly payment amount: Double-check this figure.

- Payment due date: Ensure it aligns with your pay schedule.

- Any additional fees or charges: Are there any surprises?

- Prepayment penalty clause: Confirm whether one exists.

- Details about the collateral (the car): VIN, make, model.

If anything seems amiss or unclear, ask for clarification. Do not sign until you are 100% confident in every aspect of the agreement. This diligence is your final safeguard.

Negotiating Your Deal: Beyond the Sticker Price

Many people assume that once a loan is approved, there’s no more room for negotiation. This isn’t always true, especially when dealing with dealership financing. While your pre-approval sets a benchmark, you can still leverage it.

Use your pre-approval offer to negotiate with the dealership’s finance department. They might be able to beat your outside offer to earn your business. Additionally, don’t forget to negotiate the price of the car itself. A lower car price means a lower loan amount, which translates to less interest paid. Remember to negotiate the car price first, then discuss financing. Trying to negotiate both simultaneously can become confusing and disadvantageous.

Managing Your Loan: On-Time Payments and Refinancing Options

Once the papers are signed and you drive off the lot, your responsibility shifts to diligent loan management. The most crucial aspect is making all your payments on time, every time. Late payments not only incur fees but also negatively impact your credit score, making future borrowing more expensive. Set up automatic payments to ensure you never miss a due date.

Pro tips from us: Regularly review your budget to ensure your car payment remains affordable. If your financial situation improves, consider making extra principal payments. Even small additional payments can significantly reduce the total interest paid and shorten your loan term.

Furthermore, keep an eye on interest rates. If market rates drop significantly, or if your credit score has improved since you took out the loan, refinancing your existing car loan might be a smart move. Refinancing involves taking out a new loan to pay off your current one, often at a lower interest rate or with a different loan term. This can save you thousands over the life of the loan. For more insights on when and how to refinance, check out our detailed guide on Optimizing Your Existing Auto Loan.

Special Considerations: Tailoring Your Car Loan Strategy

Not all car loan journeys are the same. Certain circumstances require specialized knowledge and tailored strategies. Whether you’re facing credit challenges or buying a car for the very first time, understanding these nuances can make a significant difference in your outcome. We aim to provide practical advice for every scenario.

The landscape of car financing is vast, and specific situations demand particular attention. By addressing these common scenarios, we ensure this guide remains comprehensive and truly valuable to a broad audience.

Bad Credit Car Loans: Strategies and Realistic Expectations

Having a less-than-perfect credit score doesn’t necessarily disqualify you from getting a car loan, but it does mean you’ll face higher interest rates and potentially stricter terms. Lenders perceive higher risk with lower credit scores, and they compensate for that risk by charging more.

Strategies for securing a bad credit car loan include:

- Saving a larger down payment: This reduces the amount you need to borrow and signals commitment.

- Finding a co-signer: A co-signer with good credit can significantly improve your chances and lower your interest rate, but they become equally responsible for the debt.

- Shopping around with subprime lenders: These lenders specialize in working with borrowers with lower credit scores. However, be extra vigilant about their terms and rates.

- Considering a less expensive car: A smaller loan amount is easier to get approved for and more manageable to repay.

Set realistic expectations: your first loan with bad credit will likely be more expensive. The goal should be to make consistent, on-time payments to rebuild your credit, positioning you for a better loan (perhaps through refinancing) in the future.

First-Time Car Buyers: Specific Advice for a Major Milestone

For first-time car buyers, the entire process can feel overwhelming. It’s a significant financial commitment, often made without prior experience. Here’s some tailored advice:

- Don’t rush: Take your time researching both vehicles and financing options.

- Prioritize reliability and affordability: Your first car doesn’t need to be your dream car. Focus on a vehicle that’s dependable and fits your budget.

- Get pre-approved: This is even more crucial for first-timers, as it gives you confidence and a clear budget.

- Bring a trusted advisor: If possible, bring a friend or family member with car-buying experience to the dealership.

- Understand insurance costs: Insurance for young, first-time drivers can be very expensive. Get insurance quotes before committing to a car.

This initial experience sets the stage for your financial future. Make it a positive and informed one.

Refinancing Your Existing Car Loan: When and Why it’s a Good Idea

Refinancing your car loan means replacing your current auto loan with a new one, typically from a different lender. This can be a savvy financial move under several circumstances:

- Improved Credit Score: If your credit score has significantly improved since you initially took out the loan, you might qualify for a much lower interest rate.

- Lower Market Interest Rates: If overall interest rates have dropped, you could secure a better deal.

- Wanting a Different Loan Term: You might want to shorten your loan term to save on interest or lengthen it to lower your monthly payments (though this increases total interest).

- Removing a Co-signer: If your credit has improved, you might be able to refinance and remove a co-signer from the loan.

Before refinancing, compare offers from multiple lenders and calculate the total savings. Ensure the new loan doesn’t have hidden fees that negate the benefits. This strategy can significantly reduce your financial burden over time. For more information on car loan refinancing, a reliable external source like the Consumer Financial Protection Bureau (CFPB) offers excellent guidance on Understanding Auto Loan Refinancing.

Conclusion: Driving Forward with Confidence

Securing a car loan is a significant financial undertaking, but it doesn’t have to be a daunting one. By understanding the fundamentals, diligently preparing, and strategically navigating the application and approval processes, you can empower yourself to make intelligent choices. From checking your credit score and budgeting wisely to understanding APRs and scrutinizing loan terms, every step you take contributes to a more favorable outcome.

Remember, whether you’re reading this on April 24th or any other day, the best time to prepare for a car loan is always now. Knowledge is your most powerful tool, transforming what might seem like a complex financial maze into a clear path towards driving your dream vehicle. Equip yourself with this comprehensive guide, ask informed questions, and negotiate with confidence. Your smart financial decisions today will pave the way for a smoother, more enjoyable ride tomorrow. Start your journey with clarity and drive away with peace of mind.