Driving Your Dreams: The Ultimate Guide to Securing a Quality Acceptance Car Loan

Driving Your Dreams: The Ultimate Guide to Securing a Quality Acceptance Car Loan Carloan.Guidemechanic.com

The open road, the freedom of movement, the convenience of personal transport – owning a car is a significant milestone for many. But the journey to get behind the wheel often involves navigating the complex world of auto financing. It’s not just about getting any car loan; it’s about securing a Quality Acceptance Car Loan – one that aligns with your financial health and sets you up for success, not stress.

This comprehensive guide will demystify the process, offering you an in-depth look at what it takes to not just get approved, but to get approved on favorable terms. We’ll explore everything from understanding lender expectations to mastering negotiation, ensuring you drive away with confidence. Let’s embark on this journey together to transform your car ownership dreams into a financially sound reality.

Driving Your Dreams: The Ultimate Guide to Securing a Quality Acceptance Car Loan

What Exactly is a "Quality Acceptance Car Loan"? (And Why It Matters So Much)

Many people focus solely on the "approval" part of a car loan. They just want to hear "yes." However, securing a Quality Acceptance Car Loan goes far beyond a simple approval. It means getting approved for an auto loan with terms that are sustainable, fair, and contribute positively to your long-term financial well-being.

This isn’t just about the lowest interest rate, although that’s certainly a key factor. It encompasses a manageable monthly payment, a reasonable loan term, and an overall agreement that doesn’t burden your budget or expose you to predatory practices. A quality acceptance means the lender views you as a responsible borrower, even if your credit history isn’t perfect.

Based on my experience working in auto financing, many individuals, especially those with past credit challenges, often feel they have to accept the first offer they receive. This can lead to high interest rates, extended loan terms, and ultimately, a much more expensive car than anticipated. Understanding what constitutes a "quality" acceptance empowers you to make informed decisions and advocate for yourself. It’s about ensuring the loan works for you, not against you.

The Foundations of Car Loan Approval: Understanding Lender Perspectives

To secure a Quality Acceptance Car Loan, you first need to understand what lenders look for. They are assessing risk – the likelihood that you will repay the loan as agreed. By understanding their criteria, you can better prepare your application and present yourself as a reliable borrower.

Here are the critical factors lenders evaluate:

Your Credit Score: The Financial Report Card

Your credit score is arguably the most significant factor in car loan approval. It’s a numerical representation of your creditworthiness, based on your payment history, amounts owed, length of credit history, new credit, and credit mix. A higher score generally indicates lower risk to lenders.

Lenders use scores like FICO and VantageScore to quickly gauge your financial responsibility. A strong score (typically 670 and above) often unlocks the best interest rates and loan terms, as lenders compete for low-risk borrowers. Conversely, a lower score will signal higher risk, potentially leading to higher interest rates or stricter approval conditions.

Income and Employment Stability: Can You Afford It?

Lenders want to see a steady, verifiable source of income. This demonstrates your ability to make consistent monthly payments. They typically look for stable employment, often preferring applicants who have been at their current job for at least six months to a year.

Your income must be sufficient to cover the proposed car payment along with your existing financial obligations. Lenders will ask for proof of income, such as pay stubs, tax returns, or bank statements, to verify your earning capacity. Stability in your employment history is a strong indicator of your ability to maintain payments over the loan term.

Debt-to-Income Ratio (DTI): Balancing Your Books

Your Debt-to-Income (DTI) ratio is another crucial metric. It compares your total monthly debt payments to your gross monthly income. For instance, if your total monthly debt (rent/mortgage, credit card payments, student loans, etc.) is $1,500 and your gross monthly income is $4,500, your DTI is 33%.

Lenders prefer a lower DTI, typically below 43%, as it suggests you have enough disposable income to comfortably handle a new car payment. A high DTI can signal that you’re already stretched thin financially, making a new car loan a higher risk. Understanding and, if possible, improving your DTI before applying can significantly enhance your chances of a Quality Acceptance Car Loan.

The Power of a Down Payment: Reducing Lender Risk and Your Loan Amount

A down payment is the initial amount of money you pay upfront for the car. This reduces the total amount you need to borrow, which in turn lowers your monthly payments and the total interest paid over the life of the loan. From a lender’s perspective, a larger down payment signals greater commitment and reduces their risk.

It also helps to mitigate the impact of depreciation, the rate at which a car loses value. Pro tips from us: aiming for at least 10-20% of the car’s purchase price as a down payment can significantly improve your loan terms, especially if you have a less-than-perfect credit score. It shows the lender you have "skin in the game."

Vehicle Choice: Not All Cars Are Created Equal in a Lender’s Eyes

The car you choose also plays a role in the loan approval process. Lenders consider the vehicle’s age, mileage, make, model, and overall value. Newer cars with lower mileage generally pose less risk to lenders because they are more reliable and hold their value better. This means they are better collateral for the loan.

Older or high-mileage vehicles might be harder to finance, or come with higher interest rates, because their resale value is lower and the risk of mechanical issues is higher. Always choose a vehicle that aligns with your financial capacity and the lender’s comfort level. This approach increases your likelihood of securing a Quality Acceptance Car Loan.

Navigating Challenges: Getting a Quality Acceptance Car Loan with Less-Than-Perfect Credit

The reality is that not everyone has a pristine credit history. Life happens, and credit scores can take a hit. However, a less-than-perfect credit score doesn’t automatically close the door on getting a car loan. It just means you need a more strategic approach to secure a quality acceptance.

Lenders offering "bad credit car loans" or "subprime auto loans" exist, but it’s crucial to approach them with caution to avoid predatory terms. The goal is to improve your position as much as possible before applying.

Here are effective strategies for improving your chances:

- Improve Your Credit Score (Even Slightly): Before you apply, take steps to boost your score. Pay down existing credit card balances, address any errors on your credit report, and make all payments on time. Even a small improvement can make a difference in the interest rate you’re offered.

- Make a Larger Down Payment: As discussed, a substantial down payment mitigates risk for lenders. If your credit is challenged, offering a larger upfront sum can significantly improve your loan terms and approval chances. It shows genuine commitment and reduces the amount you need to borrow.

- Consider a Co-signer (with Caution): A co-signer with good credit can strengthen your application by adding their creditworthiness to yours. This can help you secure a better interest rate. However, understand that a co-signer is equally responsible for the loan, so choose someone you trust and ensure you can make payments reliably to protect their credit.

- Choose a Realistic Vehicle: Instead of aiming for a brand-new luxury car, consider a more affordable, reliable used vehicle. Lenders are more comfortable financing a lower-priced car for a borrower with challenged credit, as it reduces their financial exposure. This also means a lower monthly payment for you.

- Explore Secured Car Loans: While less common for new car purchases, some lenders offer secured personal loans where an asset (like savings) is used as collateral. This can sometimes be an option if traditional auto loans are out of reach, but carefully weigh the implications.

Common mistakes to avoid are applying to multiple lenders indiscriminately, which can negatively impact your credit score with numerous hard inquiries. Another pitfall is accepting the first offer without understanding the full terms or shopping around. Based on my experience, patience and thorough preparation are your best allies when dealing with challenged credit.

The Step-by-Step Process to Secure Your Quality Acceptance Car Loan

Securing a car loan doesn’t have to be daunting. By following a structured process, you can navigate the financing landscape with confidence and increase your chances of a quality outcome.

Step 1: Assess Your Financial Health and Set a Realistic Budget

Before you even look at cars, look at your finances. This is the cornerstone of a Quality Acceptance Car Loan. Understand your current income, expenses, and existing debt obligations. Use a budgeting tool to determine how much you can comfortably afford for a monthly car payment, insurance, fuel, and maintenance.

Don’t forget to factor in potential down payment savings. A clear understanding of your budget prevents you from overextending yourself financially. For a deeper dive into preparing your finances, you might find our article on "How to Prepare Your Finances for a Car Loan" helpful.

Step 2: Get Pre-Approved from Multiple Lenders

Pre-approval is a game-changer. It means a lender has conditionally agreed to lend you a certain amount at a specific interest rate, based on a preliminary review of your credit and income. This process is usually a "soft inquiry" on your credit, which doesn’t harm your score.

Seek pre-approval from various sources:

- Banks and Credit Unions: Often offer competitive rates and personalized service.

- Online Lenders: Many reputable online platforms specialize in auto financing and can provide quick quotes.

- Dealership Financing: While convenient, it’s best to have outside pre-approvals in hand to use as leverage.

Pro tips from us: Pre-approval gives you powerful bargaining chips. You walk into the dealership knowing your financing limits and what constitutes a good rate, separating the car price negotiation from the loan negotiation.

Step 3: Choose the Right Vehicle That Aligns with Your Budget

With your pre-approval in hand and a clear budget, you can now confidently shop for a car. Focus on vehicles that fall within your approved loan amount and fit your lifestyle. Remember to consider not just the purchase price, but also ongoing costs like insurance, fuel efficiency, and potential maintenance.

A thorough vehicle history report (like CarFax or AutoCheck) is essential for used cars to understand its past. Ensure the car’s value aligns with the loan amount you’re seeking to avoid being "upside down" on your loan.

Step 4: Understand All Loan Terms and Conditions

When comparing loan offers, look beyond just the monthly payment. Scrutinize the following:

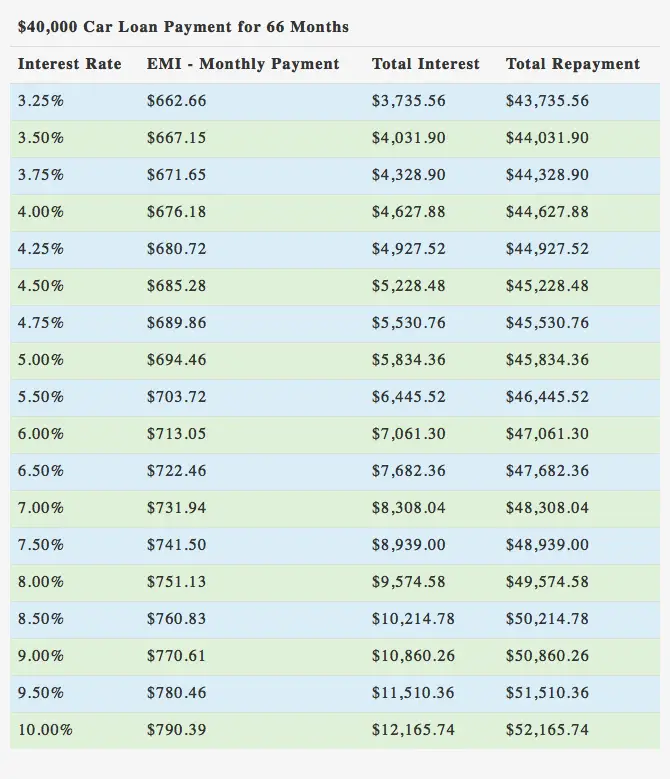

- Interest Rate (APR): The annual percentage rate (APR) reflects the total cost of borrowing, including interest and some fees. This is the most crucial number.

- Loan Term: The length of time you have to repay the loan (e.g., 36, 48, 60, 72 months). Shorter terms mean higher monthly payments but less interest paid overall.

- Fees: Look for origination fees, documentation fees, or prepayment penalties. A Quality Acceptance Car Loan should have transparent and minimal fees.

- Prepayment Penalties: Ensure there are no penalties for paying off your loan early, which is a common feature of consumer-friendly loans.

Step 5: Negotiate Wisely (Both Car Price and Loan Terms)

This is where your preparation pays off. First, negotiate the best possible price for the car itself. Once you’ve agreed on a price, then address the financing. Use your pre-approval offers as leverage to negotiate with the dealership’s finance department. They may be able to beat your outside offers, but you’ll know if their offer is truly competitive.

Don’t be afraid to walk away if the terms aren’t favorable. A Quality Acceptance Car Loan means you feel good about both the car you’re buying and the financial commitment you’re making.

Beyond Approval: Maintaining and Improving Your Financial Journey

Securing a Quality Acceptance Car Loan is a significant achievement, but the journey doesn’t end there. How you manage your loan can have a lasting impact on your financial health and credit score.

Making Payments On Time: The Golden Rule of Credit Building

This cannot be stressed enough: consistently making your car loan payments on time is paramount. Your payment history is the most influential factor in your credit score. Every on-time payment helps build a positive credit history, demonstrating reliability to future lenders.

Conversely, even a single late payment can significantly damage your credit score and incur late fees. Set up automatic payments or calendar reminders to ensure you never miss a due date.

Refinancing Opportunities: When and Why to Consider It

As you make on-time payments, your credit score may improve, or market interest rates might drop. This creates an opportunity for refinancing your car loan. Refinancing means taking out a new loan, often with a lower interest rate or different terms, to pay off your existing car loan.

This can lead to lower monthly payments, reduced total interest paid, or a shorter loan term. Pro tips from us: If your credit score has improved since you first got your loan, or if you secured your initial loan with challenged credit, actively explore refinancing options after 6-12 months of consistent payments.

Building a Positive Payment History: Long-Term Benefits

A car loan, when managed responsibly, is an excellent tool for building a strong credit profile. A diverse credit mix (including installment loans like auto loans) and a history of on-time payments contribute to a higher credit score. This improved score will benefit you in future financial endeavors, such as securing a mortgage, personal loans, or even better rates on insurance.

Common mistakes to avoid are overspending on the car initially, which makes payments a constant struggle. Another is neglecting to check your credit report periodically for accuracy. Your car loan is a stepping stone to greater financial freedom if handled correctly. For more insights into responsible borrowing, consider checking resources from the Consumer Financial Protection Bureau (CFPB) https://www.consumerfinance.gov/consumer-tools/auto-loans/.

Pro Tips for Achieving a "Quality Acceptance" Outcome

Achieving a Quality Acceptance Car Loan requires diligence and an informed approach. Here are some final, actionable tips from our experts to help you succeed:

- Do Your Homework: Research lenders, vehicle reliability, and your own credit standing extensively. Knowledge is your most powerful tool. Understand current market interest rates so you know what’s reasonable.

- Be Realistic About Your Budget: Don’t let emotion drive your car purchase. Stick to what you can truly afford, not what you wish you could afford. Overspending leads to financial strain and buyer’s remorse.

- Build a Strong Application: Gather all necessary documents (proof of income, identification, residence) beforehand. Ensure all information is accurate and consistent to streamline the approval process.

- Don’t Settle – Shop Around: Never accept the first car loan offer you receive. Compare offers from at least three different lenders to ensure you’re getting the most competitive interest rate and terms.

- Consider a Shorter Loan Term (If Affordable): While a longer loan term means lower monthly payments, it also means paying significantly more in interest over time. If your budget allows, opt for the shortest loan term possible to save money. For more on this, our article "Understanding Car Loan Interest Rates and How to Lower Them" can provide further insights.

- Read the Fine Print: Before signing any documents, meticulously read the entire loan agreement. Understand every clause, fee, and condition. If something is unclear, ask for clarification until you are fully satisfied.

Driving Forward with Confidence

Securing a Quality Acceptance Car Loan is more than just a transaction; it’s a strategic financial move that can empower your car ownership journey and strengthen your overall financial health. By understanding the factors lenders consider, diligently preparing your finances, and actively negotiating for the best terms, you transform yourself from a passive applicant into an informed and powerful borrower.

Remember, the goal isn’t just to get approved for a car loan, but to get approved for one that you can comfortably afford, that helps build your credit, and that ultimately contributes to your financial freedom. Take these steps, arm yourself with knowledge, and drive away not just with a new car, but with the confidence that you’ve made a smart, quality financial decision.

Start your journey today by assessing your financial health and taking the first step towards a truly quality auto financing experience. Your dream car, on your terms, is within reach!