Driving Your Dreams: The Ultimate Guide to Securing a Used Car Loan

Driving Your Dreams: The Ultimate Guide to Securing a Used Car Loan Carloan.Guidemechanic.com

The open road beckons, and for many, a used car represents the perfect blend of affordability and adventure. But turning that dream into a reality often involves navigating the world of financing. Securing a used car loan can feel like a complex maze, filled with jargon and endless options.

As an expert blogger and professional SEO content writer, my mission is to demystify this process for you. This comprehensive guide will equip you with the knowledge, strategies, and insider tips you need to confidently secure the best used car loan, ensuring you drive away happy and financially sound. We’ll dive deep into every aspect, from understanding eligibility to negotiating terms, making this your go-to resource for everything related to financing your next pre-loved vehicle.

Driving Your Dreams: The Ultimate Guide to Securing a Used Car Loan

Why Choose a Used Car? The Smart Financial Advantage

Before we delve into the intricacies of loans, let’s briefly touch upon why a used car often makes excellent financial sense. New cars depreciate rapidly, losing a significant portion of their value the moment they leave the dealership lot. This immediate drop can be a major financial hit.

A used car, on the other hand, has already taken that initial depreciation hit. This means you can often acquire a well-maintained vehicle at a substantially lower price. Lower purchase prices translate directly to lower loan amounts, which in turn means smaller monthly payments and less interest paid over the life of the loan.

Furthermore, insurance costs are typically lower for used cars compared to their brand-new counterparts. This adds to the overall savings, making the decision to opt for a pre-owned vehicle a financially savvy choice for many individuals and families. It’s about getting more car for your money.

Understanding Used Car Loans: What Are They Exactly?

A used car loan is essentially a type of secured installment loan designed specifically for purchasing a pre-owned vehicle. Unlike personal loans, the car itself serves as collateral for the loan. This means that if you fail to make your payments, the lender has the right to repossess the vehicle to recover their losses.

The core principle is simple: a lender provides you with a lump sum of money to buy a car, and you agree to repay that amount, plus interest, over a predetermined period. This repayment is typically structured into fixed monthly installments. The terms of these loans, including interest rates and repayment periods, can vary significantly depending on several factors, which we will explore in detail.

It’s crucial to understand that used car loans differ from new car loans in a few key aspects. Lenders might impose stricter age or mileage limits on the vehicles they’re willing to finance, and interest rates can sometimes be slightly higher for used cars due to perceived higher risk. However, with the right approach, you can still secure highly favorable terms.

Types of Used Car Loans: Finding Your Best Fit

When seeking financing for a used car, you’ll encounter several common sources. Each has its own advantages and disadvantages, and understanding them is key to making an informed decision. Shopping around is not just recommended; it’s essential.

Dealership Financing

Many dealerships offer in-house financing or work with a network of lenders to provide loan options. This can be convenient, as you can often complete the car purchase and financing in one location. The dealership acts as an intermediary, streamlining the process.

While convenient, it’s important to approach dealership financing with caution. Their primary goal is to sell you a car, and sometimes their loan offers might not be the most competitive. Always compare their offers with those from independent lenders before signing any paperwork.

Bank Loans

Traditional banks are a popular source for used car loans. They often offer competitive interest rates, especially if you have a strong banking relationship with them. Banks typically have a structured application process and transparent terms.

Applying for a used car loan through your bank can be a straightforward process, particularly if you’re an existing customer. They already have a history with you, which can sometimes expedite approval. However, their approval criteria can be quite stringent, especially regarding credit scores and vehicle age.

Credit Union Loans

Credit unions are member-owned financial institutions known for their customer-centric approach. They often offer some of the most competitive interest rates on used car loans, frequently beating out larger banks. Their focus is on serving their members, not maximizing profits.

To qualify for a credit union loan, you typically need to become a member, which usually involves meeting certain eligibility criteria (e.g., living in a specific area, working for a particular employer, or being part of an association). If you qualify, joining a credit union for a car loan can be a very smart financial move.

Online Lenders

The digital age has brought forth a plethora of online lenders specializing in auto loans. These platforms offer convenience, allowing you to apply and get pre-approved from the comfort of your home. They often cater to a wider range of credit scores, including those with less-than-perfect credit.

Online lenders can be incredibly efficient, providing quick decisions and competitive rates. However, it’s crucial to verify their reputation and read reviews before committing. Look for lenders that are transparent about their fees and terms.

Personal Loans (As a Last Resort for Cars)

While technically possible, using an unsecured personal loan to buy a used car is generally not recommended. Personal loans are not secured by the vehicle, which means lenders often charge higher interest rates to compensate for the increased risk. The lack of collateral makes them riskier for the lender.

Only consider a personal loan for a used car if you have exhausted all other options and the interest rate is surprisingly competitive. Even then, be mindful of the higher costs and less favorable terms compared to a dedicated auto loan.

Eligibility Criteria for a Used Car Loan: Are You Ready?

Lenders assess several factors to determine your eligibility and the terms of your used car loan. Understanding these criteria beforehand allows you to prepare and improve your chances of approval for favorable rates.

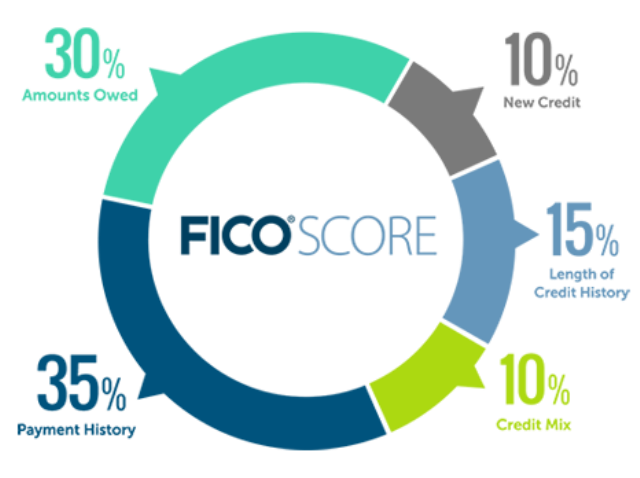

Credit Score

Your credit score is arguably the most critical factor. It’s a numerical representation of your creditworthiness, reflecting your history of borrowing and repayment. A higher credit score (generally above 670 for FICO) indicates lower risk to lenders, leading to better interest rates and terms.

Lenders use your credit score to gauge how likely you are to repay the loan. If your score is low, you might still get approved, but expect higher interest rates to compensate the lender for the increased risk they’re taking. This is why improving your credit score is often the first step in securing an affordable loan.

Income and Employment Stability

Lenders want to see that you have a stable source of income sufficient to cover your monthly loan payments. They will typically ask for proof of income, such as pay stubs, tax returns, or bank statements. Steady employment demonstrates your ability to consistently meet your financial obligations.

Consistent employment history, ideally for at least six months to a year at your current job, strengthens your application. If you’re self-employed, lenders will look for several years of consistent income and may require more extensive documentation to verify your earnings.

Debt-to-Income Ratio (DTI)

Your debt-to-income (DTI) ratio is another key metric lenders examine. It’s calculated by dividing your total monthly debt payments (including the proposed car loan payment) by your gross monthly income. A lower DTI ratio indicates that you have more disposable income to comfortably manage additional debt.

Lenders generally prefer a DTI ratio below 43%, though some might accept slightly higher depending on other factors. A high DTI can signal that you’re overextended financially, making lenders hesitant to approve new credit.

Age of Vehicle and Mileage

Unlike new car loans, used car loans often have restrictions based on the vehicle itself. Lenders may have limits on the maximum age of the car they will finance (e.g., no older than 10 years) or its maximum mileage (e.g., under 100,000-120,000 miles). This is because older, higher-mileage vehicles are considered higher risk due to potential mechanical issues and lower resale value.

These restrictions protect the lender’s collateral. If the car breaks down or its value plummets, their ability to recoup losses through repossession is diminished. Be sure to check a lender’s specific vehicle requirements before you start car shopping.

Down Payment

While not always strictly mandatory, making a down payment significantly improves your chances of loan approval and securing better terms. A larger down payment reduces the amount you need to borrow, thereby decreasing your monthly payments and the total interest paid over the loan term.

Based on my experience, a down payment of at least 10-20% of the vehicle’s purchase price is ideal. It shows the lender your commitment and reduces their risk, often translating into lower interest rates for you. It also helps you avoid being "upside down" on your loan (owing more than the car is worth) early on.

The Application Process: Step-by-Step Guide to Approval

Navigating the used car loan application process doesn’t have to be daunting. Following these steps will help you stay organized and maximize your chances of approval.

1. Assess Your Financial Health

Before even looking at cars, take an honest look at your finances. Check your credit score and review your credit report for any errors. Calculate your budget, determining how much you can realistically afford for a monthly car payment, including insurance, fuel, and maintenance.

Understanding your financial standing is the foundation. It helps you set realistic expectations for the type of loan and vehicle you can afford without straining your budget.

2. Get Pre-Approved (Crucial Step!)

Pro tips from us: Do not skip pre-approval! This is perhaps the most important step in the entire process. Pre-approval means a lender has conditionally agreed to lend you a certain amount of money at a specific interest rate, based on a preliminary review of your credit and finances.

Pre-approval gives you immense bargaining power at the dealership. You walk in as a cash buyer, knowing exactly how much you can spend and what your interest rate will be. This allows you to negotiate the car’s price separately from the financing, often leading to a better overall deal.

3. Shop for Your Car

With pre-approval in hand, you can now confidently shop for your used car. Focus on vehicles that fit within your pre-approved loan amount. Remember to consider not just the sticker price, but also the total cost of ownership.

Always request a vehicle history report (like CarFax or AutoCheck) and, ideally, arrange for a pre-purchase inspection by an independent mechanic. This due diligence can save you from costly surprises down the road.

4. Gather Documentation

Once you’ve found the right car, you’ll need to finalize your loan application. Lenders will typically require documentation to verify your identity, income, and residency. This usually includes:

- Government-issued ID (driver’s license)

- Proof of income (pay stubs, tax returns)

- Proof of residency (utility bill, lease agreement)

- Social Security Number

- Vehicle information (VIN, make, model, year, mileage)

Having these documents ready will significantly speed up the application process. Being prepared shows responsibility and helps the lender process your request efficiently.

5. Submit Your Application

With all your documents and vehicle details, submit your formal loan application to your chosen lender(s). Even if you have a pre-approval, you’ll still need to complete the full application with the specific vehicle details. The lender will then perform a hard inquiry on your credit, which might temporarily lower your score by a few points.

Don’t worry about multiple inquiries if done within a short period (typically 14-45 days, depending on the credit scoring model) for the same type of loan. Credit bureaus understand you’re rate shopping, and they often count multiple inquiries for an auto loan as a single inquiry.

6. Review Loan Offers

Once approved, carefully review all loan offers. Pay close attention to the interest rate (APR), loan term, monthly payment, and any associated fees. Don’t just look at the monthly payment; calculate the total cost of the loan over its entire term.

Negotiate if possible, especially if you have multiple offers. Sometimes, a lender might be willing to match or beat a competitor’s rate. Ensure you understand every clause before you sign on the dotted line.

Key Factors Affecting Your Used Car Loan Interest Rate

The interest rate is arguably the most significant factor determining the total cost of your loan. Several elements influence the rate you’re offered.

Credit Score

As mentioned, your credit score is paramount. Borrowers with excellent credit scores (720+) typically qualify for the lowest interest rates, sometimes even under 5%. Those with good credit (670-719) will still get competitive rates, while fair (580-669) or poor (below 580) credit will see significantly higher rates, potentially in the double digits.

A lower credit score tells lenders that there’s a higher risk of default. To offset this risk, they charge more interest. This makes building and maintaining good credit a crucial financial habit.

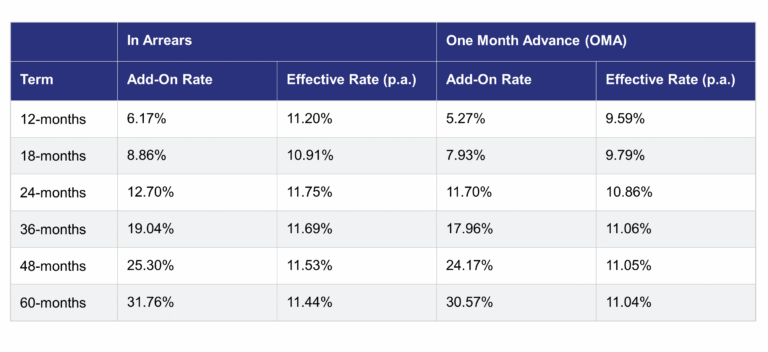

Loan Term

The loan term, or the length of time you have to repay the loan, also impacts your interest rate. Shorter loan terms (e.g., 36 or 48 months) typically come with lower interest rates because the lender’s money is tied up for a shorter period, reducing their risk. However, shorter terms mean higher monthly payments.

Conversely, longer loan terms (e.g., 60 or 72 months) often have higher interest rates but lower monthly payments. While a lower monthly payment might seem appealing, it means you’ll pay more in interest over the life of the loan and build equity in the car more slowly.

Down Payment Size

A larger down payment reduces the principal loan amount, which lowers the lender’s risk. This reduced risk often translates into a lower interest rate for you. It also means you’ll pay less interest overall because you’re borrowing less money.

Based on my experience, a substantial down payment can sometimes offset a slightly less-than-perfect credit score, giving you a better chance at a competitive rate. It demonstrates your financial commitment and capability.

Vehicle Age/Mileage

Lenders consider the age and mileage of the used car when setting interest rates. Older vehicles with higher mileage are perceived as higher risk because they are more prone to mechanical issues and depreciate faster. This can lead to higher interest rates compared to financing a newer used car.

Some lenders might even refuse to finance vehicles beyond a certain age or mileage threshold. Always verify these limits with potential lenders before you fall in love with a car.

Lender Type

As discussed earlier, different types of lenders offer varying rates. Credit unions are often known for their competitive rates, followed by banks, and then online lenders. Dealership financing can be competitive but requires careful scrutiny.

Shopping around and comparing offers from at least three different lenders is a pro tip from us to ensure you secure the best possible interest rate for your specific situation.

Current Market Rates

Interest rates are influenced by the broader economic environment, including the Federal Reserve’s benchmark rates. When overall interest rates are high, car loan rates will generally be higher, and vice versa. While you can’t control market rates, being aware of them helps you understand why rates might be higher or lower than you expected.

Used Car Loans with Less-Than-Perfect Credit: Is It Possible?

Having a low credit score can make securing a used car loan more challenging, but it’s certainly not impossible. There are specific strategies and options available for borrowers with less-than-perfect credit.

Understand Your Options

First, recognize that your options might be more limited, and the interest rates will likely be higher. Subprime lenders specialize in loans for borrowers with lower credit scores, but they compensate for the increased risk with higher rates and potentially stricter terms.

Don’t be discouraged, but be realistic. Focus on finding a loan you can comfortably afford, even if the interest rate isn’t ideal, and plan to refinance later.

Improve Your Credit Score

Before applying, take steps to improve your credit score. Pay down existing debts, especially credit card balances, as high utilization can negatively impact your score. Make all payments on time, as payment history is the most significant factor in credit scoring.

Even a small improvement in your score can sometimes unlock better loan offers. Every point counts when it comes to interest rates.

Consider a Co-Signer

If you have a trusted family member or friend with excellent credit who is willing to co-sign your loan, this can significantly increase your chances of approval and help you secure a lower interest rate. A co-signer essentially guarantees the loan, promising to make payments if you default.

However, co-signing is a serious responsibility. If you miss payments, it impacts both your credit and your co-signer’s, and they become legally responsible for the debt. Ensure both parties fully understand the implications.

Increase Your Down Payment

Making a larger down payment is even more critical when you have bad credit. It reduces the amount of money you need to borrow, thereby lowering the lender’s risk and making them more likely to approve your loan. It also helps reduce your monthly payments.

A substantial down payment shows the lender your commitment and financial responsibility, which can be a strong counter-argument to a low credit score.

Explore "Bad Credit" Lenders

Some online lenders and credit unions specifically cater to borrowers with bad credit. While their rates will be higher than those offered to prime borrowers, they might be more accessible than traditional banks. Research these lenders carefully, read reviews, and compare their terms.

Beware of predatory lenders who offer "guaranteed approval" with exorbitant interest rates and hidden fees. Always read the fine print.

Navigating the Used Car Market: What to Look For in a Vehicle

While this article focuses on loans, the car you choose directly impacts your loan terms. A smart car choice can lead to a better loan.

Vehicle History Report (CarFax/AutoCheck)

Always obtain a comprehensive vehicle history report. This report provides crucial information about the car’s past, including accident history, salvage titles, odometer rollbacks, service records, and previous ownership. It’s an indispensable tool for uncovering potential red flags.

Ignoring a vehicle history report is one of the common mistakes to avoid. It can save you from buying a car with hidden damage or a problematic past, which could lead to expensive repairs and impact the car’s resale value, potentially leaving you underwater on your loan.

Pre-Purchase Inspection

Even if a vehicle history report looks clean, a pre-purchase inspection (PPI) by a trusted, independent mechanic is non-negotiable. A mechanic can identify existing mechanical issues, potential future problems, and signs of poor maintenance that might not show up on a report.

This small investment (typically $100-$200) can save you thousands in future repairs and give you leverage in negotiating the car’s price. If a seller refuses a PPI, consider it a major red flag.

Research Market Value

Before making an offer, research the car’s market value using resources like Kelley Blue Book (KBB), Edmunds, or NADAguides. These tools provide an estimated value based on the car’s year, make, model, mileage, condition, and features.

Knowing the market value ensures you don’t overpay for the car, which directly impacts the amount you need to borrow and your loan-to-value ratio. Overpaying can also make it harder to get approved for the full amount you need.

Common Mistakes to Avoid When Getting a Used Car Loan

Even experienced buyers can fall prey to common pitfalls. Being aware of these mistakes can save you time, money, and frustration.

Not Getting Pre-Approved

As discussed, failing to get pre-approved before stepping onto a dealership lot is a significant error. It strips you of negotiating power and forces you to discuss financing at the same time as the car price, often leading to a less favorable overall deal.

Dealers prefer to bundle these conversations because it makes it harder for you to discern where the extra costs are coming from. Always secure your financing first.

Focusing Only on Monthly Payments

While a low monthly payment is appealing, fixating solely on it can lead to bad decisions. Dealers might extend the loan term (e.g., to 72 or 84 months) to lower your monthly payment, but this significantly increases the total interest you pay over time.

Always consider the total cost of the loan, including all interest and fees, rather than just the monthly installment. A lower monthly payment for a longer term often means paying much more in the long run.

Ignoring the Total Cost

Beyond the monthly payment, many people overlook the total cost of ownership. This includes insurance, registration fees, taxes, fuel, and potential maintenance. A cheap car might have high insurance premiums or be known for expensive repairs.

Factor in all these costs when budgeting for your used car. Your car loan is just one piece of the financial puzzle.

Skipping a Pre-Purchase Inspection

This bears repeating: skipping a professional inspection is a high-risk gamble. A used car’s history report tells you about its past, but a mechanic tells you about its present and potential future. Without it, you could be buying a money pit.

A small investment in an inspection can prevent major headaches and expensive repair bills down the line, ensuring the car is worth the loan you’re taking out.

Accepting the First Offer

Whether it’s the dealership’s financing offer or the first loan rate you receive from a bank, never accept it without comparison. Lenders are competing for your business. Always shop around and compare at least three different offers.

This due diligence can save you hundreds, if not thousands, of dollars in interest over the life of the loan. It’s your money, so be proactive in finding the best terms.

Pro Tips for Securing the Best Used Car Loan

Here are some actionable strategies from our experience to help you land the most favorable used car loan possible.

Boost Your Credit Score

Even a few points can make a difference. Before applying, dedicate a few months to improving your credit. Pay all bills on time, reduce credit card balances, and avoid opening new lines of credit. A higher score translates directly to lower interest rates.

Consider using tools like Experian Boost or similar services that allow utility and rent payments to contribute to your credit history, potentially increasing your score.

Save for a Larger Down Payment

The more money you put down upfront, the less you need to borrow, and the less risk the lender takes. This often results in a lower interest rate and lower monthly payments. Aim for at least 10-20% of the car’s purchase price.

A larger down payment also reduces the chances of becoming "upside down" on your loan, where you owe more than the car is worth, especially given the depreciation of used vehicles.

Shop Around for Lenders

Don’t limit yourself to the first lender you encounter. Get quotes from banks, credit unions, and online lenders. Compare their interest rates, fees, and loan terms. Use pre-approval offers from multiple sources to leverage against each other.

Based on my experience, a difference of just one or two percentage points on your interest rate can save you hundreds or even thousands of dollars over the life of a typical used car loan. This step is non-negotiable.

Negotiate Everything

Negotiate the car’s price, the trade-in value (if applicable), and even the loan terms. If you have multiple pre-approval offers, use the best one to negotiate with the dealership’s finance department. They may be able to beat it to secure your business.

Remember, every aspect of the deal is potentially negotiable. Don’t be afraid to ask for a better price or a lower rate.

Understand All Terms and Conditions

Before signing any loan agreement, read every single line. Understand the annual percentage rate (APR), the total amount you’ll pay, any prepayment penalties, late fees, and what happens if you miss a payment. If you have questions, ask until you fully understand.

Don’t let the excitement of a new car rush you into signing something you don’t fully comprehend. It’s your financial future on the line.

Refinancing Your Used Car Loan: When and Why?

Even after you’ve secured a used car loan, your financial journey doesn’t necessarily end there. Refinancing can be a smart move in certain situations, allowing you to improve your loan terms.

Lower Interest Rates

If interest rates have dropped since you took out your original loan, or if your credit score has significantly improved, you might qualify for a lower interest rate. Refinancing can replace your existing loan with a new one at a more favorable rate, reducing your total interest paid and potentially your monthly payments.

Many people refinance a year or two after purchasing their car if they’ve diligently worked on improving their credit. This is a powerful strategy to save money.

Reduce Monthly Payments

Refinancing can also help reduce your monthly payments, either by securing a lower interest rate or by extending the loan term. While extending the term means paying more interest overall, it can provide much-needed breathing room in your monthly budget during a financial crunch.

Be mindful of how much you extend the term. Try to keep it as short as possible to minimize the total interest paid.

Change Loan Terms

Perhaps you want to switch from a variable interest rate to a fixed rate, or you want to remove a co-signer now that your credit is strong. Refinancing allows you to renegotiate and alter the terms of your original agreement to better suit your current financial situation.

It’s always worth exploring refinancing options, especially if your financial circumstances have improved since you first obtained your loan. Check with different lenders to see what rates you qualify for.

Used Car Loan vs. New Car Loan: A Quick Comparison

While this article focuses on used car loans, a brief comparison can highlight their distinct advantages.

| Feature | Used Car Loan | New Car Loan |

|---|---|---|

| Purchase Price | Generally much lower | Higher |

| Depreciation | Slower, initial hit already absorbed | Rapid in the first few years |

| Loan Amount | Lower principal | Higher principal |

| Monthly Payment | Typically lower | Typically higher |

| Interest Rate | Can be slightly higher (due to vehicle risk) | Generally lower (due to lower vehicle risk) |

| Loan Terms | Often shorter (e.g., 36-60 months) | Can be longer (e.g., 60-84 months) |

| Insurance | Usually lower premiums | Usually higher premiums |

| Vehicle Choice | Wider variety of makes/models within budget | Latest models, more customization |

As you can see, used car loans generally offer a more budget-friendly path to vehicle ownership, particularly when considering the overall financial impact.

Drive Away Confidently

Securing a used car loan doesn’t have to be a stressful ordeal. By understanding the process, knowing your financial standing, and diligently shopping around, you can secure a loan that fits your budget and helps you get behind the wheel of your ideal pre-owned vehicle. Remember to leverage pre-approval, always get a pre-purchase inspection, and negotiate every aspect of the deal.

With the insights provided in this comprehensive guide, you are now well-equipped to navigate the world of used car financing like a seasoned expert. Go forth, find your perfect ride, and enjoy the journey!