Driving Your Dreams: The Ultimate Guide to State Employees Car Loans

Driving Your Dreams: The Ultimate Guide to State Employees Car Loans Carloan.Guidemechanic.com

Securing a new or used vehicle is a significant financial decision for anyone. For state employees, however, this journey often comes with unique advantages that many are unaware of. Your dedicated service to the public sector can open doors to better financing options, making your dream car more accessible and affordable.

This comprehensive guide will delve deep into the world of car loans tailored for state employees. We’ll explore why you’re a preferred borrower, where to find the best deals, and how to navigate the application process to ensure you get the most favorable terms. Our goal is to empower you with the knowledge to make informed decisions and drive away with confidence.

Driving Your Dreams: The Ultimate Guide to State Employees Car Loans

Why State Employees Are a Lender’s Preferred Choice

It might not always be explicitly advertised as a "State Employees Car Loan," but the reality is that your employment status often gives you a distinct edge in the financing market. Lenders view government employees, whether at the state or federal level, as highly desirable clients. This preference isn’t arbitrary; it’s rooted in several fundamental financial principles.

Firstly, job stability is a cornerstone of your appeal. State employees typically enjoy secure employment with consistent paychecks, significantly reducing the risk of loan default. This reliability is a huge comfort to lenders, who are always assessing a borrower’s ability to repay.

Secondly, the nature of government work often translates to predictable income. Unlike some private sector roles that might be subject to economic fluctuations, state positions generally offer stable salaries and benefits. This steady income stream further reinforces your reliability as a borrower.

Finally, your dedication to public service often comes with an unspoken trust. Lenders recognize the integrity associated with government roles, contributing to a positive perception of your financial responsibility. All these factors combine to position state employees as a low-risk, high-value demographic for auto financing.

Unlocking the Exclusive Benefits: What Special Car Loan Terms Mean for You

When lenders view you as a low-risk borrower, they are often willing to extend more attractive terms. This is where the real advantages of being a state employee come into play, even if the loan isn’t explicitly branded as a "State Employees Car Loan." These benefits can significantly impact the overall cost and manageability of your car loan.

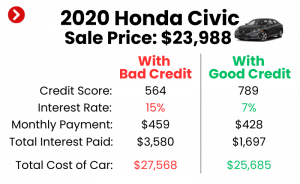

One of the most significant perks is access to lower interest rates. Because lenders perceive less risk, they can afford to offer more competitive Annual Percentage Rates (APRs). Even a fractional reduction in your interest rate can save you hundreds, or even thousands, of dollars over the life of the loan. Based on my experience, comparing offers can reveal surprising differences in rates.

Another key advantage is flexible repayment terms. You might find lenders willing to offer longer repayment periods without penalizing you with higher interest rates, or conversely, shorter terms with even lower rates if that suits your financial strategy. This flexibility allows you to tailor your monthly payments to fit comfortably within your budget.

Furthermore, some institutions may offer higher loan amounts or be more lenient with down payment requirements. This can be particularly beneficial if you’re looking at a slightly more expensive vehicle or prefer to keep more cash on hand. It provides greater purchasing power and less upfront financial strain.

Finally, certain financial institutions, especially credit unions, may offer streamlined application processes and even exclusive discounts specifically for public sector employees. These aren’t always widely advertised, making it crucial to know where to look and what questions to ask.

Eligibility: What Lenders Look for in a State Employee Borrower

While your state employment status is a powerful asset, it’s not the only factor lenders consider. To secure the best "State Employees Car Loan" terms, you’ll still need to meet standard eligibility criteria, though some aspects might be viewed more favorably due to your occupation. Understanding these requirements will help you prepare a strong application.

The most crucial piece of evidence is, of course, proof of employment. Lenders will require recent pay stubs, an employment verification letter from your HR department, or other official documentation confirming your current role and tenure. The longer you’ve been in your position, the better, as it demonstrates greater stability.

Your credit score remains a significant factor. A higher credit score signals a history of responsible borrowing and timely payments. While state employment can sometimes compensate for a slightly lower score, aiming for a good to excellent score (generally 670 and above) will always unlock the most favorable rates. Pro tips from us include checking your credit report regularly for errors.

Lenders will also evaluate your debt-to-income (DTI) ratio. This ratio compares your total monthly debt payments to your gross monthly income. A lower DTI indicates that you have ample income to cover new loan payments without financial strain. State employees often have manageable DTI ratios due to stable incomes, but it’s wise to assess yours before applying.

Finally, you’ll need to provide proof of residency and a valid driver’s license. These are standard requirements across all loan applications, ensuring you are a verifiable individual residing at a stable address. Being prepared with all these documents will make your application process smooth and efficient.

Where to Find the Best Car Loans for State Employees

Knowing where to look is key to leveraging your state employee status for a great car loan. Not every lender advertises specific "State Employees Car Loan" programs, but many offer preferential treatment or tailored products once they know your employment type.

Credit Unions are often the top recommendation for public sector employees. Many credit unions were founded specifically to serve government workers and their families. They typically offer highly competitive rates, lower fees, and a more personalized service compared to larger banks. Look for credit unions affiliated with your state, county, or specific government agencies. For example, a credit union named "Public Service Credit Union" or "Government Employees Federal Credit Union" would be an excellent starting point.

Traditional Banks can also be a viable option. While they may not have explicitly named "State Employees Car Loan" products, many large banks have internal policies that offer better rates to stable borrowers, including state employees. It’s always worth getting a quote and explicitly mentioning your employment type during the application process. Don’t assume they’ll automatically know or offer you the best deal; you often need to inquire.

Online Lenders and Comparison Sites offer convenience and the ability to compare multiple offers quickly. While some online lenders might not have specific programs for state employees, many use sophisticated algorithms that factor in job stability and income reliability, indirectly favoring government workers. Using comparison tools can help you cast a wide net and identify competitive rates.

Finally, don’t overlook Dealership Financing. While often seen as a less favorable option, some dealerships work with specific lenders who might be keen on state employee customers. It’s always worth getting a quote, but ensure you compare it against pre-approvals you’ve secured elsewhere. Common mistakes to avoid are accepting the first offer without shopping around.

The Application Process: A Step-by-Step Guide for State Employees

Applying for a car loan, especially when aiming to leverage your state employee status, requires a systematic approach. Following these steps will help you streamline the process and increase your chances of securing the best "State Employees Car Loan" terms.

Step 1: Gather Your Documents. Before you even start looking at cars, assemble all necessary paperwork. This includes your driver’s license, proof of residency (utility bill, lease agreement), recent pay stubs (at least two or three), an employment verification letter (if available or easily obtained from HR), and bank statements. Having these ready will save you time and prevent delays.

Step 2: Check Your Credit Score and Report. Obtain a copy of your credit report from all three major bureaus (Equifax, Experian, TransUnion) and review them carefully for any errors. Your credit score significantly impacts the interest rate you’ll be offered. If you find discrepancies, dispute them immediately. You can typically get a free report annually from AnnualCreditReport.com.

Step 3: Get Pre-Approved. This is a crucial step for state employees. Apply for pre-approval with several lenders, especially credit unions known for serving public sector employees. Pre-approval gives you a clear idea of how much you can borrow and at what interest rate, empowering you to negotiate at the dealership. It also shows sellers you’re a serious buyer.

Step 4: Shop for Your Car. With a pre-approval in hand, you can now confidently shop for a vehicle within your budget. Focus on the car’s price, not just the monthly payment, to ensure you’re getting a good deal on the vehicle itself. Remember, your pre-approval gives you leverage.

Step 5: Finalize Your Loan. Once you’ve chosen your car, compare the dealer’s financing offer with your pre-approved loan. Sometimes, dealers can beat your pre-approval, especially if they have special incentives or work with lenders eager for state employee customers. Choose the offer with the lowest interest rate and most favorable terms. Read all paperwork carefully before signing.

Pro Tips for Securing the Absolute Best Deal

Beyond the standard application process, there are several strategies state employees can employ to maximize their savings and secure the most advantageous car loan. These pro tips come from years of observing successful financial moves.

Firstly, shop around aggressively. Do not settle for the first offer you receive, even if it seems good. Get quotes from at least three to five different lenders, including credit unions, banks, and potentially online providers. This competitive approach is your best weapon for securing the lowest interest rate and most favorable terms.

Secondly, negotiate everything. The price of the car, the trade-in value of your old vehicle, and the terms of your loan are all negotiable. Dealers expect you to negotiate. Be firm, polite, and always be prepared to walk away if the deal isn’t right. Leverage your pre-approval as a negotiation tool.

Consider making a down payment, even if it’s not strictly required. A larger down payment reduces the amount you need to borrow, which can lead to lower monthly payments and less interest paid over the life of the loan. It also signals greater financial commitment to lenders.

If your credit score isn’t ideal, take steps to improve your credit score before applying. Pay off small debts, dispute errors on your report, and ensure all your payments are on time. Even a small bump in your score can translate to significant savings on interest. You can find more tips on this in our article:

Finally, don’t forget about car insurance. The cost of insurance can significantly impact your overall monthly car expenses. Get quotes from multiple insurance providers before finalizing your car purchase to factor this into your budget. For more insights, check out our guide:

Common Mistakes State Employees Make When Applying for Car Loans

Even with the inherent advantages, state employees can sometimes fall into common traps when seeking auto financing. Being aware of these pitfalls can help you avoid costly errors and ensure you fully leverage your employment status.

A significant mistake is not explicitly leveraging their employment status. Some state employees assume lenders will automatically know or offer them special terms. It’s crucial to mention your state employment early in the conversation with lenders and dealerships, as it can prompt them to offer more favorable rates or direct you to specific programs.

Another common error is only checking with one lender. As mentioned, shopping around is vital. Relying solely on your primary bank or the dealership’s financing can mean missing out on significantly better offers from credit unions or other specialized lenders. Complacency can be expensive.

Many borrowers also make the mistake of not understanding the full loan terms. Focus solely on the monthly payment can be misleading. Always look at the total interest paid over the life of the loan, any hidden fees, and prepayment penalties. A low monthly payment might hide a much longer loan term and higher overall cost.

Buying more car than they can afford is a universal mistake, but state employees might feel overconfident due to their stable income. While your income is reliable, it’s essential to stick to a budget that comfortably accommodates not just the car payment, but also insurance, maintenance, and fuel. Overextending yourself can lead to financial stress down the line.

Lastly, ignoring their credit report before applying can be detrimental. Errors on your report can unfairly lower your score, leading to higher interest rates. Taking the time to review and correct any inaccuracies can save you a substantial amount of money. For more information on managing your credit, you can refer to external resources like the Consumer Financial Protection Bureau (CFPB) auto loan guide:

Beyond the Loan: Additional Perks for State Employees

The benefits of being a state employee often extend beyond just the car loan itself. While not directly part of the financing, these additional perks can further reduce the overall cost of vehicle ownership.

Some insurance companies offer discounts on car insurance specifically for government employees. These "affinity discounts" recognize the same low-risk profile that lenders do, potentially saving you a considerable amount on your premiums each year. It’s always worth inquiring about these when getting insurance quotes.

You might also find discounts on vehicle maintenance, parts, or accessories through employee benefit programs or partnerships with local businesses. Check your state’s employee benefits portal or ask your HR department if any such programs exist. These small savings can add up over time, making car ownership even more affordable.

These extra advantages underscore the value of your public service. Always remember to ask about any available discounts or special programs tailored for state employees, as they can significantly enhance your financial well-being.

Driving Forward with Confidence

As a state employee, your dedicated service not only contributes to the community but also positions you favorably in the financial landscape. When it comes to securing a car loan, you possess a unique advantage that can lead to lower interest rates, more flexible terms, and a smoother application process. By understanding why lenders prefer you and knowing where to look for the best offers, you can unlock significant savings.

Remember to leverage your employment status, shop around diligently, prepare your documents, and never hesitate to negotiate. Avoid common pitfalls by being informed and proactive. With this comprehensive guide, you are now equipped to navigate the world of car loans with confidence, ensuring you drive away with a deal that truly reflects your value as a state employee. Start exploring your options today and make your dream car a reality!