Driving Your Dreams: Unlocking Car Loans with No Credit History

Driving Your Dreams: Unlocking Car Loans with No Credit History Carloan.Guidemechanic.com

Getting your first car is a significant milestone, a symbol of independence and freedom. But for many, the journey to ownership hits a roadblock: no credit history. You might be a recent graduate, new to the country, or simply someone who has never needed to borrow money before. Lenders rely heavily on credit scores to assess risk, so when you have a "thin file" or no file at all, securing a car loan can feel like an impossible task.

But here’s the good news: impossible it is not. While challenging, there are legitimate avenues and strategic approaches to help you secure a car loan even without an established credit score. This comprehensive guide will illuminate the places to get a car loan with no credit, equipping you with the knowledge and confidence to navigate the process successfully. We’ll dive deep into each option, offering practical advice and insider tips to help you drive away in your new vehicle.

Driving Your Dreams: Unlocking Car Loans with No Credit History

Understanding the "No Credit" Conundrum

Before exploring solutions, it’s crucial to understand why "no credit" poses a challenge for lenders. When you apply for a loan, lenders want to see evidence of your ability and willingness to repay debt. Your credit report and score are their primary tools for this assessment.

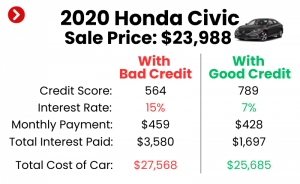

"No credit" means you haven’t used credit products like credit cards, mortgages, or previous loans. This differs significantly from having "bad credit," where you have a history of missed payments or defaults. While bad credit shows a history of poor financial management, no credit simply means you’re an unknown entity to lenders. This lack of data makes you a higher perceived risk, as there’s no track record to predict your repayment behavior.

Based on my experience working with countless first-time buyers, the biggest hurdle is often just getting a lender to take that initial leap of faith. They prefer predictability, and a blank slate offers none. However, by understanding this perspective, you can proactively address their concerns.

Paving Your Way: Essential Strategies for No-Credit Car Loans

Even before you approach a lender, there are proactive steps you can take to significantly improve your chances of approval. These strategies demonstrate responsibility and reduce the perceived risk for lenders.

1. The Power of a Down Payment

Saving up a substantial down payment is perhaps the most impactful step you can take when seeking a car loan with no credit. A down payment reduces the amount you need to borrow, thereby lowering the lender’s risk. It shows commitment and financial discipline.

Lenders see a significant down payment as a sign that you are serious about the purchase and less likely to default. It also creates immediate equity in the vehicle, which is reassuring for the lender. Aim for at least 10-20% of the car’s purchase price, but the more you can put down, the better your chances and potentially your interest rate.

2. Enlisting a Co-signer: A Bridge to Approval

A co-signer can be a game-changer for individuals with no credit history. A co-signer is someone with good credit who agrees to take on legal responsibility for the loan if you fail to make payments. This significantly reduces the lender’s risk because they have another reliable party to pursue if you default.

Finding a co-signer, typically a parent, trusted family member, or close friend, can open doors to better interest rates and more favorable loan terms than you would qualify for on your own. However, it’s crucial to understand the commitment involved for both parties. The co-signer’s credit will be affected if you miss payments, so ensure clear communication and a solid plan for repayment. for more detailed insights on navigating this option.

3. Start Small: Opting for an Affordable Vehicle

While a brand-new luxury car might be tempting, starting with a more modest and affordable used car is a wise strategy when you have no credit. Lenders are more willing to approve smaller loan amounts, as the risk is inherently lower. A lower price point means a smaller loan, potentially a smaller monthly payment, and a reduced likelihood of defaulting.

This approach not only makes approval more accessible but also provides an excellent opportunity to build your credit responsibly. Once you’ve established a positive payment history, you’ll be in a much stronger position to finance a more expensive vehicle in the future.

4. Demonstrating Income Stability and Employment

Even without a credit score, lenders need assurance that you have the financial capacity to repay the loan. Providing proof of stable income and consistent employment can go a long way. This includes recent pay stubs, bank statements showing regular deposits, and potentially a letter from your employer.

The longer you’ve been at your current job, the better. Lenders look for stability, as it indicates a reliable source of income for loan payments. If you’re self-employed, be prepared with tax returns and detailed financial records to prove your income stream.

Pro tips from us: Create a comprehensive financial dossier before you even start looking for a loan. Include proof of income, residency, utility bills in your name, and any other documentation that shows you are a reliable and stable individual. This preparedness impresses lenders and streamlines the application process.

Where to Find Your No-Credit Car Loan: Your Options Explored

Now that you’ve armed yourself with strategies, let’s explore the specific places to get a car loan with no credit. Each option comes with its own set of advantages and considerations, so understanding them is key to making an informed decision.

A. Dealership Financing: A Common Starting Point

Many individuals with no credit history find success directly through car dealerships. Dealerships often have relationships with various lenders, including those specializing in "subprime" or "bad credit" loans, which can also extend to no-credit situations.

1. Buy Here, Pay Here (BHPH) Dealerships

BHPH dealerships are often the most accessible option for those with no credit or very poor credit. These dealerships act as both the seller and the lender, meaning you make your car payments directly to them. They often have less stringent approval criteria compared to traditional lenders, as they prioritize your income and ability to make payments over your credit history.

- Pros: High approval rates, even with no credit. The application process is often quick and straightforward. You can typically drive away the same day.

- Cons: These loans usually come with significantly higher interest rates than conventional loans, sometimes reaching the maximum allowed by state law. Vehicle selection might be limited, and the cars sold are often older or have higher mileage. Crucially, some BHPH dealerships do not report payments to credit bureaus, which defeats the purpose if your goal is to build credit.

- Common mistakes to avoid are: Not asking if they report to all three major credit bureaus (Experian, Equifax, TransUnion). If they don’t, while you get a car, you won’t be building the credit history you need for future financial endeavors. Always read the contract carefully for hidden fees or restrictive terms.

2. Dealerships Working with Subprime Lenders

Beyond BHPH, many standard dealerships partner with a network of external lenders, some of whom specialize in loans for borrowers with limited or no credit history. These are often referred to as subprime lenders. While their rates will still be higher than prime loans, they are typically more competitive than BHPH options.

- How it works: You apply for financing through the dealership, and they submit your application to various lenders in their network. Lenders who specialize in higher-risk loans will consider factors beyond just your credit score, such as your income stability, down payment, and employment history.

- Pros: Wider selection of vehicles compared to BHPH. Lenders in this category almost always report to credit bureaus, making it an excellent opportunity to build credit. You might secure a more competitive interest rate than a BHPH loan.

- Cons: Interest rates will still be elevated due to the perceived risk. It can take a bit longer for approval compared to BHPH.

B. Credit Unions: Your Member-Owned Advantage

Credit unions are non-profit financial institutions owned by their members. Unlike traditional banks, which are for-profit, credit unions often have more flexible lending criteria and a greater willingness to work with members who have unique financial situations, including those with no credit history.

Based on my experience, credit unions are often overlooked but can be a fantastic resource for first-time car buyers with no credit. Their mission is to serve their members, not just maximize profits. This often translates to more personalized service and a focus on building long-term relationships.

- Pros: Potentially lower interest rates and fees compared to banks or subprime lenders. They may be more willing to approve loans based on factors like your income stability, length of membership, and a solid down payment, even without a robust credit file. They are generally more understanding and offer financial counseling.

- Cons: You need to become a member to apply for a loan. Membership requirements vary but often involve living in a specific geographic area, working for a particular employer, or belonging to certain organizations. The application process might be a bit more involved than a quick online application.

- Pro tip: If you have an existing relationship with a credit union (e.g., you have a checking or savings account there), leverage that. They already have some history with you, which can be beneficial.

C. Online Lenders Specializing in No Credit/Bad Credit

The digital age has brought forth a plethora of online lenders, many of whom specialize in serving borrowers with less-than-perfect credit or no credit history. These platforms often use alternative data points and proprietary algorithms to assess creditworthiness, making them a viable option.

- How it works: You typically fill out a single online application, and the platform either directly lends to you or acts as a marketplace, connecting you with multiple lenders who might be willing to approve your loan. The process is often fast, with pre-approvals available in minutes.

- Pros: Convenience of applying from anywhere, often with quick approval decisions. Many online lenders are transparent about their rates and terms. They can be a good way to compare offers from multiple lenders without visiting physical locations.

- Cons: Interest rates can still be high, especially if you have no credit. It’s crucial to research the lender’s reputation thoroughly to avoid predatory loans. Always ensure they report to all major credit bureaus.

- Common mistakes to avoid are: Falling for "guaranteed approval" claims without scrutinizing the terms. While some lenders are more lenient, no legitimate lender can truly guarantee approval without any assessment. Also, be wary of excessive fees or requests for upfront payments.

D. Traditional Banks (with Caveats)

While generally more challenging, traditional banks like Chase, Bank of America, or Wells Fargo can be a possibility for those with no credit, but usually under specific circumstances.

- Why it’s harder: Traditional banks typically have stricter lending criteria and rely heavily on established credit scores. Without one, you’re often automatically filtered out.

- When they might consider it:

- Existing Relationship: If you’ve been a long-time customer with a substantial checking or savings account, the bank may be more willing to consider you, especially if you have a significant down payment.

- Co-signer: Bringing a co-signer with excellent credit dramatically increases your chances of approval with a traditional bank and can secure you their best rates.

- Secured Loan: Some banks might offer a secured car loan where you put down a significant amount of cash as collateral, or even use other assets. This reduces their risk.

- Pros: If approved, traditional banks often offer the most competitive interest rates. They are highly regulated and reputable.

- Cons: Approval is much less likely without a co-signer or a strong existing banking relationship.

E. Peer-to-Peer (P2P) Lending (Limited for Cars)

Peer-to-peer lending platforms connect individual borrowers directly with individual investors. While more common for personal loans, some platforms might facilitate car loans.

- How it works: Investors review loan requests and fund them based on risk assessment.

- Pros: Can sometimes be more flexible than traditional lenders.

- Cons: Not a primary source for car loans, interest rates can still vary widely, and it’s less common to find direct auto loans through these platforms. It’s typically not the first place we recommend for car loans, especially for those with no credit.

Building Your Credit While Getting a Car Loan

One of the most significant advantages of securing a car loan, especially with no prior credit, is the opportunity it presents to build a positive credit history. This single loan can be your stepping stone to future financial stability.

To ensure your car loan helps build your credit, verify that the lender reports your payments to all three major credit bureaus: Experian, Equifax, and TransUnion. Timely and consistent payments on your car loan will demonstrate your reliability as a borrower. This positive payment history will then be reflected in your credit report, gradually contributing to the development of a credit score. This is a crucial step towards qualifying for better interest rates on future loans, credit cards, and even mortgages.

for more information on how credit scores are built and maintained.

Navigating the Road Ahead: Red Flags and Pro Tips

Even when exploring options for no-credit car loans, vigilance is key. Not all offers are created equal, and some can lead to financial distress.

What to Watch Out For: Common Mistakes to Avoid Are:

- "Guaranteed Approval" Claims: Be extremely skeptical of any lender promising "guaranteed approval" regardless of your credit history. While some lenders are very lenient, legitimate lenders always have some form of criteria. These claims often mask predatory loans with exorbitant interest rates or hidden fees.

- Excessively High Interest Rates: While higher rates are expected with no credit, compare offers. If an interest rate seems astronomical (e.g., above 20-25% without extreme circumstances), pause and reassess. High interest rates significantly increase the total cost of your vehicle.

- Hidden Fees and Clauses: Always read the entire loan agreement before signing. Look for prepayment penalties, excessive origination fees, or other charges that inflate the loan’s cost.

- Lenders Who Don’t Report to Credit Bureaus: As mentioned, if your goal is to build credit, a lender that doesn’t report payments is counterproductive. Confirm this detail explicitly before committing.

- Pressure Tactics: Don’t let a salesperson or loan officer rush you into a decision. Take your time, ask questions, and if something feels off, walk away.

Pro Tips for Boosting Your Approval Chances:

- Gather All Your Documents: Have your driver’s license, proof of income (pay stubs, tax returns), proof of residency (utility bills), and bank statements ready. Being organized shows responsibility.

- Get Pre-Approved (If Possible): Some online lenders and credit unions offer pre-approval with a soft credit inquiry, which doesn’t hurt your non-existent credit score. This gives you an idea of what you can afford and strengthens your negotiation position at the dealership.

- Understand the Total Cost: Focus not just on the monthly payment, but the total amount you’ll pay over the life of the loan, including interest. Use online calculators to compare scenarios.

- Be Transparent: Honesty about your financial situation, including your lack of credit, builds trust with lenders who are willing to work with you.

- Consider a Shorter Loan Term: While this means higher monthly payments, it results in less interest paid over time and you’ll own the car outright sooner. Lenders also prefer shorter terms as it reduces their risk exposure.

For further insights into responsible borrowing and managing your finances, we highly recommend exploring resources from the Consumer Financial Protection Bureau. They offer invaluable, unbiased information on all aspects of consumer finance. Link to: Consumer Financial Protection Bureau – Auto Loans

Conclusion: Your Journey to Car Ownership Starts Here

Securing a car loan with no credit history might seem daunting at first, but it is absolutely achievable with the right strategies and knowledge. By understanding the concerns of lenders, taking proactive steps like saving a down payment or finding a co-signer, and knowing the specific places to get a car loan with no credit, you can confidently navigate the path to car ownership.

Remember, this first loan is not just about getting a car; it’s a powerful opportunity to establish a positive credit history, opening doors to future financial opportunities. Choose your lender wisely, understand all terms, and commit to timely payments. With diligence and smart choices, you’ll soon be driving your dreams and building a solid financial future, proving that a blank credit slate is just a starting point, not a barrier.