Driving Your Dreams: Your Comprehensive Guide to Getting a Car Loan with a 540 Credit Score

Driving Your Dreams: Your Comprehensive Guide to Getting a Car Loan with a 540 Credit Score Carloan.Guidemechanic.com

Securing an auto loan can feel like an uphill battle when your credit score hovers around 540. Many people believe a low credit score automatically disqualifies them from car ownership. However, this isn’t necessarily true. While it presents unique challenges, getting a car loan with a 540 credit score is absolutely possible with the right approach, knowledge, and a bit of persistence.

This article is designed to be your ultimate guide, offering deep insights and practical strategies to navigate the subprime auto loan market. We’ll explore what a 540 credit score means for car financing, reveal effective tactics to improve your chances of approval, and arm you with the knowledge to secure the best possible terms. Our goal is to empower you to drive away in a reliable vehicle, turning a perceived obstacle into a manageable journey.

Driving Your Dreams: Your Comprehensive Guide to Getting a Car Loan with a 540 Credit Score

Understanding Your 540 Credit Score and Auto Loans

A 540 credit score falls squarely into the "bad credit" or "subprime" category. This classification signals to lenders that you may have a history of missed payments, high debt, or limited credit history. For financial institutions, a lower score translates directly to a higher perceived risk.

Lenders use credit scores to assess the likelihood of a borrower defaulting on a loan. When your score is 540, they see a greater chance of non-payment compared to someone with excellent credit. This doesn’t mean you’re a lost cause, but it does mean lenders will exercise more caution.

Based on my experience, individuals with scores in this range often face higher interest rates and less favorable loan terms. Lenders offset their increased risk by charging more for the money they lend. It’s crucial to understand this dynamic before you even start shopping.

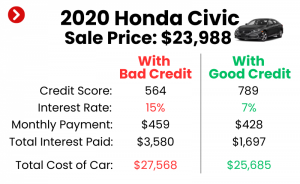

The primary impact of a 540 credit score on a car loan is the interest rate you’ll be offered. While someone with a score above 700 might get an APR in the single digits, you could be looking at rates well into the double digits. This significantly increases the total cost of the car over the life of the loan.

Furthermore, lenders might be less willing to offer flexible repayment terms or longer loan durations. They might also require a larger down payment or a co-signer to mitigate their risk. Knowing these realities upfront helps you prepare and strategize effectively.

Is Getting a Car Loan with a 540 Credit Score Possible? The Good News!

Despite the challenges, the answer is a resounding yes: getting a car loan with a 540 credit score is entirely possible. Many lenders specialize in working with borrowers who have less-than-perfect credit. The key is knowing where to look and how to present yourself as a responsible borrower.

The auto loan market is vast, encompassing a wide range of lenders catering to different credit profiles. While traditional banks might be a tougher sell, credit unions, online subprime lenders, and dealership finance departments often have programs specifically designed for individuals with lower credit scores. These lenders understand that life happens and people need second chances.

It’s important, however, to set realistic expectations. You might not qualify for the lowest interest rates or the most luxurious car. The immediate goal should be to secure reliable transportation at an affordable monthly payment that you can consistently manage. This initial loan, if handled responsibly, can also serve as a powerful tool to rebuild your credit over time.

Think of this as an opportunity. A successfully paid-off car loan can significantly boost your credit score, opening doors to better financial products in the future. It’s a stepping stone towards greater financial stability and lower borrowing costs down the line.

Key Strategies to Secure a Car Loan with a 540 Credit Score

Navigating the car loan process with a 540 credit score requires a proactive and strategic approach. You need to demonstrate to lenders that you are a reliable borrower, despite your credit history. Here are some of the most effective strategies to improve your chances of approval and secure more favorable terms.

1. Save for a Significant Down Payment

One of the most powerful tools at your disposal is a substantial down payment. When you put a significant amount of money down, you immediately reduce the lender’s risk. This is because the loan amount is smaller, and you have more equity in the vehicle from day one.

A larger down payment signals to lenders that you are serious about your purchase and have the financial discipline to save. It also means you’ll be borrowing less money, which can translate to lower monthly payments and a reduced total interest paid over the life of the loan. For someone with a 540 credit score, aiming for at least 10-20% of the car’s purchase price is highly recommended.

Pro tips from us: If you can afford more, do it. Every extra dollar you put down strengthens your position. A 25% down payment can drastically improve your loan terms, even with a low credit score. Consider delaying your purchase for a few months if it means saving up more for this crucial step.

Furthermore, a significant down payment can help you avoid being "upside down" on your loan, where you owe more than the car is worth. This is a common problem for subprime borrowers, and a good down payment offers a protective buffer. It’s a clear demonstration of your commitment and financial readiness.

2. Find a Co-Signer with Good Credit

If you have a trusted friend or family member with a strong credit history, asking them to co-sign your car loan can dramatically increase your chances of approval. A co-signer essentially guarantees the loan, promising to make payments if you default. Their good credit rating helps offset your lower score.

Lenders view a co-signer as an additional layer of security. This can lead to approval for loans you might otherwise be denied, and potentially at more favorable interest rates. The co-signer’s credit profile effectively "lifts" your application.

However, choosing a co-signer is a serious decision that carries significant responsibility for both parties. The co-signer’s credit will be impacted by your payments, both positively and negatively. If you miss payments, their credit score will also suffer, and they will be legally obligated to pay the remaining balance.

Common mistakes to avoid are not fully understanding the co-signer’s responsibilities or taking their help for granted. Always ensure open communication and a clear agreement with your co-signer. This arrangement should be entered into with mutual trust and a clear understanding of the risks involved.

3. Choose the Right Vehicle (Affordability is Key)

When you have a 540 credit score, affordability should be your guiding principle, not luxury. Focus on purchasing a reliable, used vehicle that fits comfortably within your budget. Avoid the temptation of expensive new cars or high-end models, as these will come with higher price tags and thus larger loan amounts.

A more affordable car means a smaller loan, which reduces the lender’s risk and your monthly payment. This makes it easier to keep up with payments, which is crucial for rebuilding your credit. Consider vehicles known for their reliability and lower maintenance costs.

Pro tips from us: Research used car values thoroughly using resources like Kelley Blue Book or Edmunds. Don’t just look at the sticker price; factor in insurance costs, potential maintenance, and fuel efficiency. A car that is slightly older but well-maintained can be a much smarter financial decision than a brand-new model.

Resist the urge to stretch your budget to its absolute limit. Leave some financial breathing room for unexpected expenses or emergencies. Over-extending yourself financially on a car purchase is a common pitfall that can lead to missed payments and further damage to your credit score.

4. Explore Different Lender Types

Not all lenders are created equal, especially when it comes to subprime auto loans. You’ll need to cast a wider net than someone with excellent credit. Here are the types of lenders to consider:

- Dealership Financing (Special Finance Departments): Many dealerships have relationships with multiple lenders, including those specializing in bad credit car loans. They often have "special finance" departments designed to help customers with lower scores. They can sometimes offer "buy here, pay here" options, where the dealership itself is the lender. While convenient, these often come with higher interest rates.

- Online Subprime Lenders: A growing number of online lenders focus exclusively on bad credit auto loans. Companies like Carvana, Capital One Auto Finance, and others have platforms that can pre-qualify you with a soft credit pull, allowing you to compare offers without impacting your score initially.

- Credit Unions: Often overlooked, credit unions are member-owned and tend to be more flexible and understanding than traditional banks. They might be more willing to work with members who have a 540 credit score, especially if you have an existing relationship with them. Their interest rates can also be more competitive.

- Traditional Banks: While tougher to get approved, it’s still worth inquiring with your existing bank. Sometimes, a long-standing relationship can provide a slight advantage, though expectations should be tempered.

Based on my experience, applying to several lenders (within a short timeframe to minimize credit score impact) can help you compare offers and find the most favorable terms. Don’t limit yourself to just one option.

5. Get Pre-Approved (with caution)

Seeking pre-approval from multiple lenders can be a smart move, but it requires understanding the difference between soft and hard credit inquiries. Many online lenders offer a "pre-qualification" process that uses a soft credit pull, which doesn’t affect your credit score. This allows you to see potential loan terms without commitment.

Once you have a few pre-approval offers, you’ll have a clearer picture of the interest rates and loan amounts you might qualify for. This knowledge is invaluable when you visit a dealership, as it gives you leverage in negotiations. You’ll know what a reasonable offer looks like and won’t be as easily swayed by high-pressure sales tactics.

Be aware that a formal pre-approval (after pre-qualification) or a loan application will typically involve a hard credit inquiry. However, FICO scores group multiple inquiries for the same type of loan (like auto loans) within a 14-45 day window as a single inquiry, minimizing the impact on your score. So, shop around for rates within a short period.

Common mistakes to avoid are letting multiple hard inquiries spread out over several months. Focus your rate shopping into a focused period to protect your credit score.

What to Expect: Interest Rates and Loan Terms

With a 540 credit score, you should prepare for higher interest rates. This is an unavoidable reality of subprime lending. While prime borrowers might see rates below 5%, you could be looking at an Annual Percentage Rate (APR) ranging from 10% to 20% or even higher, depending on the lender, the car, and your specific financial situation.

Understanding APR is crucial. It represents the true annual cost of borrowing, including interest and certain fees. A higher APR means your monthly payments will be larger, and you’ll pay significantly more over the life of the loan. For example, on a $15,000 loan over five years, a 5% APR might cost you around $2,000 in interest, while a 15% APR could cost over $6,000.

Lenders might also offer longer loan terms, such as 72 or even 84 months, to make monthly payments seem more affordable. While this can reduce your immediate cash outflow, it drastically increases the total amount of interest you’ll pay. Longer terms also mean you’re more likely to be upside down on your loan, owing more than the car is worth, for a longer period.

Pro tips from us: Always focus on the total cost of the loan, not just the monthly payment. Use online loan calculators to compare different scenarios. If you can afford slightly higher monthly payments on a shorter term, it will save you thousands in the long run.

Negotiating the APR might be challenging, but it’s not impossible. If you have a strong down payment or a co-signer, you have more leverage. Be prepared to walk away if the terms are simply too unfavorable and unsustainable for your budget.

Essential Documents and Information You’ll Need

Being prepared with all the necessary documentation can streamline the car loan application process. Lenders, especially those working with subprime credit, will want to thoroughly verify your financial stability. Having everything ready shows you are organized and serious.

Here’s a typical list of documents and information you should gather:

- Proof of Income: This is paramount. Lenders want to ensure you have a stable source of income to make payments. Bring recent pay stubs (usually the last two or three), W-2 forms, or tax returns if you’re self-employed.

- Proof of Residence: Utility bills (electricity, water, gas), a lease agreement, or mortgage statements are commonly accepted to verify your address. They want to know you have a stable living situation.

- Identification: A valid government-issued ID, such as a driver’s license or state ID, is required.

- Social Security Number: This is necessary for the lender to run a credit check.

- References: Some lenders, particularly "buy here, pay here" dealerships, might ask for personal references (not family members) who can vouch for your character.

- Down Payment Funds: Have proof of funds available for your down payment, whether it’s bank statements or a cashier’s check.

- Trade-in Information (if applicable): If you’re trading in a vehicle, bring its title, registration, and any relevant loan payoff information.

Having these documents neatly organized and readily available will make the application process much smoother. It demonstrates responsibility and helps the lender quickly assess your eligibility.

Boosting Your Credit Score While You Drive (Long-Term Strategy)

Getting a car loan with a 540 credit score is just the first step; the ultimate goal should be to use this opportunity to improve your credit score. A successfully managed auto loan can be a powerful tool for credit rebuilding.

The most critical factor in improving your credit score is making all your payments on time, every time. Payment history accounts for 35% of your FICO score. Set up automatic payments or calendar reminders to ensure you never miss a due date. Consistency is key here.

Secondly, work on reducing other debts, especially high-interest credit card balances. Lowering your credit utilization ratio (the amount of credit you’re using compared to your total available credit) can significantly boost your score. Aim to keep credit card balances below 30% of your limit, or ideally, pay them off entirely.

Regularly monitor your credit report for errors. You’re entitled to a free credit report from each of the three major bureaus (Experian, Equifax, TransUnion) annually via AnnualCreditReport.com. Dispute any inaccuracies you find, as these can negatively impact your score. For more tips on boosting your credit score, check out our guide on .

By consistently making on-time payments on your car loan and managing your other credit responsibly, you’ll see your 540 credit score steadily climb. This will open doors to better financial opportunities and lower borrowing costs in the future.

Common Mistakes to Avoid When Getting a Car Loan with a 540 Credit Score

Navigating the subprime auto loan market can be tricky. Many individuals with lower credit scores fall into common traps that can worsen their financial situation. Being aware of these pitfalls can save you significant money and stress.

1. Not Budgeting Properly: A major mistake is not having a realistic budget before you start shopping. Don’t just consider the monthly car payment; factor in insurance, fuel, maintenance, and potential repair costs. Overextending yourself can lead to missed payments, which further damages your credit.

2. Accepting the First Offer: It’s tempting to take the first loan offer you get when you have a 540 credit score, especially after facing rejections. However, this can be a costly mistake. Always compare offers from multiple lenders, even if they are all subprime. A slight difference in APR can save you thousands over the loan term.

3. Falling for "Guaranteed Approval" Scams: Be extremely wary of any lender promising "guaranteed approval" regardless of your credit score. These often come with predatory interest rates, hidden fees, or unfavorable terms designed to trap borrowers. Reputable lenders will always perform some level of credit assessment.

4. Ignoring the Total Cost of the Loan: As discussed, focusing solely on the monthly payment can be misleading. Always calculate the total amount you will pay over the life of the loan, including all interest and fees. A lower monthly payment often means a longer loan term and a much higher total cost.

5. Not Understanding the Fine Print: Never sign a loan agreement without thoroughly reading and understanding every clause. Ask questions about anything unclear, especially regarding prepayment penalties, late fees, and repossession terms. Don’t let pressure from a salesperson rush you into a commitment you don’t fully comprehend.

Pro Tips from Us: Navigating the Process with Confidence

Getting a car loan with a 540 credit score requires a blend of preparation, patience, and assertiveness. Here are some final professional tips to help you succeed and make the best decision for your financial future.

1. Be Honest About Your Financial Situation: Transparency with lenders is crucial. Don’t try to hide financial challenges or inflate your income. Lenders appreciate honesty and are more likely to work with you if you’re upfront about your situation. They can often tailor solutions when they have the full picture.

2. Negotiate, But Be Realistic: While your negotiation power is limited with a 540 credit score, it’s not non-existent. You can still negotiate the car’s price, the down payment, and possibly some fees. However, be realistic about the interest rates you’ll receive. Focus your negotiation on areas where you have the most leverage.

3. Read Everything Carefully, Twice: Before you sign any document, read it meticulously. This includes the loan agreement, sales contract, and any add-ons. If you’re unsure, ask for clarification. If possible, take the documents home to review them without pressure or even have a trusted advisor look them over.

4. Don’t Be Afraid to Walk Away: This is perhaps the most important tip. If a deal doesn’t feel right, the terms are unsustainable, or you feel pressured, be prepared to walk away. There will always be other cars and other lenders. Making a bad financial decision now will haunt you for years. Your long-term financial health is more important than driving away in a car today.

5. Monitor Your Credit Diligently: After securing your loan, continue to monitor your credit reports and scores regularly. This vigilance will help you track your progress and quickly identify any potential issues. You can monitor your credit score for free using resources like AnnualCreditReport.com, as recommended by the Consumer Financial Protection Bureau (CFPB).

Conclusion: Driving Towards a Brighter Financial Future

Obtaining a car loan with a 540 credit score can feel daunting, but as we’ve explored, it’s a completely achievable goal with the right strategy. It requires understanding your financial standing, preparing thoroughly, and approaching the process with realistic expectations. While higher interest rates and stricter terms are likely, the opportunity to secure reliable transportation and, crucially, rebuild your credit, is invaluable.

By focusing on a significant down payment, considering a co-signer, choosing an affordable vehicle, exploring various lenders, and diligently managing your payments, you can turn a challenging situation into a stepping stone towards financial improvement. Remember, this isn’t just about getting a car; it’s about demonstrating financial responsibility and paving the way for a stronger credit profile in the future.

Don’t let a low credit score deter you from pursuing your needs. Arm yourself with knowledge, apply these strategies, and approach the market with confidence. Your journey to securing a car loan with a 540 credit score starts now, and with every on-time payment, you’re driving towards a brighter financial future.