Easy Car Loan Approval: Your Ultimate Guide to Driving Away Stress-Free

Easy Car Loan Approval: Your Ultimate Guide to Driving Away Stress-Free Carloan.Guidemechanic.com

Securing a car loan might seem like a daunting journey, filled with complex terms, stringent requirements, and the ever-present fear of rejection. Many aspiring car owners believe that easy car loan approval is an elusive dream, reserved only for those with impeccable financial histories. However, this perception couldn’t be further from the truth.

In reality, achieving quick and easy car loan approval is not about luck; it’s about preparation, understanding the process, and knowing precisely what lenders are looking for. This comprehensive guide is designed to demystify the car loan application process, providing you with actionable strategies and expert insights to navigate your path to car ownership with confidence. We’ll explore everything from boosting your credit score to finding the right lender, ensuring you’re well-equipped to drive away in your dream car without unnecessary stress.

Easy Car Loan Approval: Your Ultimate Guide to Driving Away Stress-Free

Understanding the Landscape: What Lenders Really Look For

Before we dive into the strategies for easy car loan approval, it’s crucial to understand the fundamental criteria lenders use to assess your application. They aren’t just looking at your credit score; they’re evaluating your overall financial reliability. Think of it as a holistic review of your ability and willingness to repay the loan.

Based on my experience in the financial sector, many applicants mistakenly focus solely on one aspect, like their credit score, while neglecting other critical factors. A lender’s decision is often a blend of several key elements, all contributing to your risk profile. Mastering these areas significantly boosts your chances of approval.

The Pillars of Lender Assessment

Lenders typically evaluate several core areas, often referred to as the "5 Cs of Credit," though the specific terminology might vary. These pillars form the foundation of their decision-making process:

- Character: This refers to your credit history – your past payment behavior. Lenders want to see a consistent record of paying debts on time.

- Capacity: Your ability to repay the loan, primarily judged by your income and existing debt obligations. They’re looking at your debt-to-income ratio.

- Capital: Any money you’re personally investing in the purchase, such as a down payment or trade-in value. This shows your commitment and reduces the loan amount.

- Collateral: The car itself serves as collateral for the loan. Lenders assess its value to ensure it can cover the loan amount if you default.

- Conditions: This includes the purpose of the loan, the current economic climate, and the interest rate environment. These external factors can influence lending decisions.

Understanding these intertwined factors is the first step towards preparing an application that stands out. By proactively addressing each of these areas, you can transform a potentially complex application into one that sails smoothly through the approval process.

The Cornerstone of Easy Approval: Your Credit Score

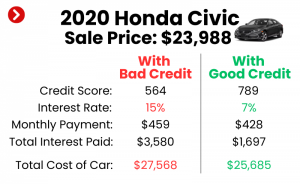

Without a doubt, your credit score is one of the most significant determinants of your car loan approval chances and the interest rate you’ll receive. A strong credit score signals to lenders that you are a responsible borrower with a history of managing debt effectively. Conversely, a low score can raise red flags, making approval harder and rates higher.

Pro tips from us: Regularly monitoring your credit score and report is not just a good habit; it’s a strategic move for anyone seeking financing. It allows you to identify and rectify errors, and understand areas for improvement long before you apply.

What is a "Good" Credit Score for a Car Loan?

While there’s no universal magic number, generally, a FICO score of 660 and above is considered "good" for a car loan, opening doors to more competitive interest rates. Scores between 700 and 749 are often categorized as "very good," while anything 750 and above is "excellent," qualifying you for the absolute best rates available.

Even with a lower score, approval is possible, but you might face higher interest rates or require a larger down payment. The goal is always to present the strongest possible credit profile.

Steps to Improve Your Credit Score Before Applying

If your credit score isn’t where you want it to be, don’t despair. There are concrete steps you can take to improve it:

- Pay Bills on Time: Payment history accounts for 35% of your FICO score. Late payments are detrimental, so ensure all your bills, not just credit cards, are paid punctually.

- Reduce Credit Card Balances: Your credit utilization ratio (how much credit you’re using versus how much you have available) is another significant factor. Aim to keep your balances below 30% of your credit limit, ideally even lower.

- Avoid Opening New Credit Accounts: Resist the urge to open multiple new credit cards or loans in the months leading up to your car loan application. Each new application can temporarily lower your score.

- Check for Errors: Obtain your free credit reports from Equifax, Experian, and TransUnion. Dispute any inaccuracies immediately, as they can unfairly drag down your score.

By focusing on these areas, you can significantly enhance your credit standing, paving the way for easier car loan approval and more favorable terms. This proactive approach demonstrates financial discipline to potential lenders.

Beyond Credit: Other Key Factors for Quick Approval

While your credit score is a crucial element, it’s just one piece of the puzzle. Lenders consider several other significant factors when evaluating your application for easy car loan approval. Overlooking these can undermine even a strong credit score.

Common mistakes to avoid are underestimating the impact of your income stability or neglecting to save for a substantial down payment. These non-credit factors paint a fuller picture of your financial health and repayment capacity.

Income and Employment Stability: Your Ability to Pay

Lenders want assurance that you have a steady, reliable source of income to comfortably cover your monthly car payments. They typically look for consistent employment history, often preferring applicants who have been at their current job for at least six months to a year. Stable employment demonstrates your financial consistency.

Your income level also plays a role in determining how much you can borrow. Lenders assess your gross monthly income against your proposed car payment and existing debts to ensure you’re not overextending yourself.

Debt-to-Income Ratio (DTI): Are You Overburdened?

Your Debt-to-Income (DTI) ratio is a critical metric for lenders. It compares your total monthly debt payments (including the new car payment) to your gross monthly income. A lower DTI indicates that you have more disposable income available to manage new debt, making you a less risky borrower.

Generally, lenders prefer a DTI ratio of 36% or lower, though some may approve loans with a DTI up to 43% for applicants with strong credit. Keeping your DTI in check is vital for demonstrating your financial capacity for easy car loan approval.

The Power of a Down Payment

Making a significant down payment is one of the most effective strategies for boosting your chances of easy car loan approval and securing better terms. A larger down payment reduces the amount you need to borrow, which in turn lowers your monthly payments and the total interest paid over the life of the loan.

It also signals to lenders your commitment to the purchase and reduces their risk, as you have more "skin in the game." Aim for at least 10-20% of the car’s purchase price, if possible.

Trade-in Value: Leveraging Your Current Asset

If you have an existing vehicle, trading it in can function similarly to a down payment. The value of your trade-in is subtracted from the new car’s price, effectively reducing the loan amount required. This can make your application more attractive to lenders.

Be sure to research your car’s trade-in value beforehand using reliable sources like Kelley Blue Book or Edmunds, so you go into negotiations well-informed.

Vehicle Choice: Impact on Approval

The type, age, and price of the car you choose can also influence your loan approval. Lenders are generally more comfortable financing newer, more reliable vehicles because they hold their value better as collateral. While it might seem counterintuitive, an excessively old or high-mileage vehicle can be harder to finance due to higher perceived risk and depreciation.

Choosing a car that fits comfortably within your budget, rather than stretching for the most expensive option, also demonstrates financial prudence to lenders. This careful consideration contributes to a smoother approval process.

Strategic Preparation for a Seamless Application

The secret to easy car loan approval often lies in meticulous preparation before you even set foot in a dealership or click "apply" online. A well-prepared applicant projects confidence and reliability, making the lender’s job easier and your approval more likely.

This stage involves gathering all necessary information, understanding your financial limits, and strategically approaching potential lenders. Think of it as laying the groundwork for a successful outcome.

Gathering Your Documents: A Comprehensive Checklist

Being organized with your paperwork saves time and avoids delays in the approval process. Have these documents ready before you apply:

- Proof of Identity: Valid driver’s license, state ID, or passport.

- Proof of Income: Recent pay stubs (last 2-3 months), W-2 forms, tax returns (if self-employed), or bank statements.

- Proof of Residence: Utility bill, lease agreement, or mortgage statement with your current address.

- Proof of Insurance: You’ll need valid car insurance before driving off the lot.

- Credit Report & Score: While lenders will pull their own, having yours reviewed helps you understand your position.

Having these documents neatly organized demonstrates your seriousness and efficiency, streamlining the application.

Getting Pre-Approved: A Game-Changer

One of the most powerful steps you can take for easy car loan approval is to get pre-approved for a loan before you start shopping for a car. Pre-approval means a lender has reviewed your financial information and tentatively agreed to lend you a certain amount, up to a specific limit, at a particular interest rate.

The benefits are numerous:

- Know Your Budget: You’ll know exactly how much you can afford, preventing you from falling in love with a car outside your price range.

- Stronger Negotiating Position: You walk into the dealership as a cash buyer, giving you leverage to negotiate on the car’s price, not just the monthly payment.

- Faster Process: It significantly speeds up the car-buying process, as the financing is already largely secured.

You can seek pre-approval from banks, credit unions, and online lenders.

Budgeting: Knowing What You Can Truly Afford

Before committing to a loan, create a realistic budget that includes all potential car ownership costs, not just the monthly payment. Factor in insurance, fuel, maintenance, and potential repairs. For more details on budgeting for a car, check out our guide on .

A responsible budget ensures you can comfortably manage your car loan payments without straining your other financial obligations. This financial foresight is key to long-term satisfaction.

Researching Lenders: Comparison Shopping is Key

Don’t settle for the first loan offer you receive, especially if it’s from a dealership without prior research. Different lenders offer varying rates and terms based on your credit profile and their internal policies.

Explore options from:

- Banks: Often offer competitive rates for well-qualified borrowers.

- Credit Unions: Known for lower rates and more flexible terms, especially for members.

- Online Lenders: Can provide quick approvals and a wide range of options, sometimes catering to specific credit situations.

By comparing offers, you can find the best deal that aligns with your financial situation, leading to genuinely easy car loan approval on favorable terms.

Navigating Special Situations: Bad Credit or No Credit?

The phrase "easy car loan approval" might sound like an oxymoron if you have a less-than-perfect credit history or no credit history at all. However, from my perspective, even with a less-than-perfect credit history, achieving car loan approval is absolutely within reach. It simply requires a more strategic approach and perhaps a bit more patience.

It’s about demonstrating your current financial stability and commitment, even if past mistakes or a lack of history currently obscure it. Don’t let a low score deter you from exploring your options.

Strategies for Bad Credit Applicants

If your credit score is struggling, these tactics can significantly improve your chances:

- Secure a Co-Signer: A co-signer with good credit can lend their financial strength to your application. Their credit history and income reassure the lender, reducing their risk and increasing your approval odds.

- Make a Larger Down Payment: As discussed, a substantial down payment reduces the loan amount and shows your commitment. This is even more impactful when you have bad credit, as it offsets some of the perceived risk.

- Seek Out Subprime Lenders: These lenders specialize in working with borrowers who have lower credit scores. While their interest rates might be higher, they offer a pathway to approval and an opportunity to rebuild your credit.

- Consider a Less Expensive Vehicle: Opting for a more affordable car reduces the total loan amount, making it a less risky proposition for lenders and potentially lowering your monthly payments to a more manageable level.

Remember, the goal is not just approval but also to secure a loan you can comfortably repay, which will help improve your credit over time.

Strategies for No Credit Applicants

For those new to borrowing, establishing credit can feel like a "chicken and egg" problem. Here’s how to navigate a no-credit situation for car loan approval:

- First-Time Buyer Programs: Many dealerships and lenders offer programs specifically designed for individuals with no prior credit history. These programs often have specific requirements but can be a great starting point.

- Secured Loans: Some lenders may offer secured car loans where the car itself serves as collateral. This can make them more willing to lend to those without a credit history.

- Small, Installment Loans First: If time permits, consider taking out a small, easily repayable installment loan (like a credit-builder loan) and diligently making payments to build a positive credit history before applying for a car loan.

- Proof of Income and Stability: Emphasize your consistent employment history, stable income, and low debt-to-income ratio. Lenders will lean heavily on these factors in the absence of a credit history.

Building credit takes time, but starting with a car loan you can successfully repay is an excellent way to lay a strong financial foundation.

The Application Process: Dos and Don’ts for Success

Once you’ve done your homework and gathered your documents, the actual application for easy car loan approval is the final hurdle. How you approach this stage can significantly impact the outcome. It’s not just about filling out forms; it’s about making informed decisions and avoiding common missteps.

This is where your preparation truly pays off, allowing you to move through the process confidently and efficiently.

Filling Out the Application Correctly and Honestly

Accuracy is paramount. Double-check all information before submitting your application. Any discrepancies, even minor ones, can raise red flags and delay or even derail your approval. Be truthful about your income, employment, and financial history. Lenders verify this information, and misrepresentation can lead to rejection or more serious consequences.

A transparent and accurate application signals trustworthiness, which is highly valued by lenders.

Negotiating Terms: Beyond the Sticker Price

Once approved, don’t just accept the first offer. You have room to negotiate, especially if you’ve secured pre-approval from another lender. Focus on key terms:

- Interest Rate (APR): Even a small difference in the Annual Percentage Rate can save you hundreds or thousands over the life of the loan.

- Loan Term: A shorter term means higher monthly payments but less interest paid overall. A longer term means lower monthly payments but more total interest. Choose what fits your budget and financial goals.

- Additional Fees: Be aware of any origination fees, documentation fees, or other charges that might be added to the loan.

Comparing offers from multiple lenders (including your pre-approval) gives you leverage to secure the best possible deal. For an unbiased view on current interest rates, consult resources like .

Reading the Fine Print: Know What You’re Signing

This cannot be stressed enough: always read the entire loan agreement before signing. Understand every clause, especially those related to:

- Prepayment Penalties: Check if there are any fees for paying off your loan early.

- Late Payment Fees: Know the charges for missed or late payments.

- Default Clauses: Understand the conditions under which the lender can repossess your vehicle.

If anything is unclear, ask questions until you fully comprehend the terms. A signed contract is legally binding, so ensure you’re comfortable with all its provisions.

Avoiding Common Pitfalls

- Multiple Hard Credit Inquiries: While rate shopping, try to keep all your applications within a short timeframe (typically 14-45 days, depending on the scoring model). This allows them to be counted as a single inquiry, minimizing the impact on your credit score.

- Impulse Buying: Avoid making emotional decisions. Stick to your budget and research, even when faced with a seemingly irresistible offer.

- Ignoring the Total Cost: Focus on the total cost of the loan (principal + interest + fees), not just the monthly payment. A low monthly payment over an extended term can mean paying significantly more in the long run.

By being diligent and informed, you can navigate the application process smoothly and achieve the easy car loan approval you’ve worked for.

Post-Approval: Maintaining Your Financial Health

Congratulations! You’ve secured your car loan and driven off in your new vehicle. While the initial goal of easy car loan approval has been met, your financial journey with this loan is just beginning. How you manage your loan payments going forward will have a lasting impact on your credit health and future financial opportunities.

This stage is about responsible stewardship, ensuring that your car loan becomes an asset for building a strong credit history, not a burden.

Making Timely Payments: The Golden Rule

This is the most crucial aspect of managing any loan. Consistently making your car loan payments on time, every time, is paramount. Payment history is the largest factor in your credit score, and a record of punctual payments will steadily improve your credit standing.

Consider setting up automatic payments from your bank account to ensure you never miss a due date. This removes the risk of forgetfulness and helps build a solid financial track record.

Impact on Your Credit Score

Every on-time payment you make positively contributes to your credit score. Over time, this demonstrates your reliability as a borrower, making it easier to qualify for other forms of credit (like a mortgage or personal loans) at better rates in the future.

Conversely, even a single late payment can significantly damage your credit score, setting back your financial progress. Protect your newly acquired credit by being diligent.

Refinancing Options: Seizing Better Opportunities

As you make consistent payments and your credit score improves, you might become eligible for better loan terms down the line. Refinancing your car loan means taking out a new loan to pay off your existing one, often at a lower interest rate or with a different loan term.

If market interest rates drop or your credit score has substantially improved since you first financed, refinancing could save you a significant amount of money over the remaining life of the loan. It’s always worth exploring this option after a year or two of on-time payments.

If you’re thinking about managing your finances post-loan, our article on offers great insights into building overall financial health.

Conclusion: Your Path to Stress-Free Car Ownership

Achieving easy car loan approval is not a matter of luck but a testament to thorough preparation, informed decision-making, and a strategic approach. By understanding what lenders look for, meticulously preparing your financial profile, and navigating the application process with confidence, you can significantly increase your chances of securing favorable car financing.

From bolstering your credit score and managing your debt-to-income ratio to making a solid down payment and getting pre-approved, each step contributes to a smoother, less stressful path to car ownership. Even with credit challenges, there are viable strategies to help you get behind the wheel. Remember, your car loan is not just a means to an end; it’s an opportunity to build a stronger financial future.

Armed with the insights from this comprehensive guide, you are now well-equipped to approach the car loan process with knowledge and power. Take control of your car buying journey today, secure that easy car loan approval, and drive away with peace of mind.