Easy Car Loans For Bad Credit: Your Comprehensive Guide to Getting Approved

Easy Car Loans For Bad Credit: Your Comprehensive Guide to Getting Approved Carloan.Guidemechanic.com

Securing a car loan when your credit score isn’t pristine can feel like an uphill battle. Many people find themselves in this challenging situation, believing that "easy car loans for bad credit" are nothing more than a myth. However, while the path might require a bit more preparation and understanding, it is absolutely possible to get approved for the financing you need.

This in-depth guide is designed to empower you with the knowledge and strategies to navigate the world of auto financing, even with a less-than-perfect credit history. We’ll explore how to improve your chances, where to look for lenders, and what common pitfalls to avoid. Our goal is to provide you with a roadmap to drive away in your new (or new-to-you) vehicle, all while rebuilding your financial standing.

Easy Car Loans For Bad Credit: Your Comprehensive Guide to Getting Approved

Understanding Bad Credit and Car Loans

Before diving into solutions, it’s essential to understand what "bad credit" signifies in the lending world. Your credit score is a numerical representation of your creditworthiness, based on your payment history, outstanding debts, length of credit history, and other factors. A lower score typically indicates a higher risk to lenders.

What Does "Bad Credit" Really Mean for Lenders?

For most auto lenders, a credit score below 600-620 is generally considered "subprime" or "bad credit." This means they perceive you as having a higher likelihood of defaulting on your loan payments. Consequently, they often offset this perceived risk by offering higher interest rates or requiring more stringent terms.

Based on my experience, many individuals get discouraged at this stage, assuming no one will lend to them. This isn’t true. While traditional banks might be hesitant, a whole segment of the lending industry specializes in providing car financing for bad credit. They understand that life happens, and past financial difficulties shouldn’t permanently sideline your ability to secure essential transportation.

Why Are Car Loans Harder With Poor Credit?

Lenders are in the business of assessing risk. When your credit history shows missed payments, bankruptcies, or high debt utilization, it signals to them that lending you money carries a greater risk of non-repayment. This doesn’t mean you’re a bad person; it simply means you need to demonstrate your current ability and commitment to repay.

The key to finding easy car loans for bad credit isn’t about tricking lenders. Instead, it’s about presenting yourself as the most responsible borrower possible, despite your credit history. It also involves knowing where to look and how to prepare.

Preparing for Your Car Loan Application: Crucial Steps for Success

Preparation is paramount when seeking car financing with bad credit. The more organized and informed you are, the better your chances of approval and securing favorable terms. Think of this as laying the groundwork for your financial success.

1. Check Your Credit Report and Score

Your credit report is the detailed history lenders will review. Before approaching any lender, obtain copies of your credit report from all three major bureaus: Equifax, Experian, and TransUnion. You can get free copies annually from AnnualCreditReport.com.

Carefully review each report for any inaccuracies or errors. Incorrect information can unfairly lower your score. If you find discrepancies, dispute them immediately with the credit bureau. Correcting even small errors can sometimes boost your score enough to make a difference in loan offers.

2. Know Your Budget Inside and Out

Before you even think about a car, determine how much you can truly afford each month. This isn’t just about the car payment. Factor in insurance, fuel, maintenance, and potential repair costs. A common mistake to avoid is focusing solely on the monthly payment without considering the total cost of ownership.

Pro tips from us: Create a detailed budget spreadsheet. List all your income and expenses. Be realistic about what you can comfortably pay without stretching your finances thin. This helps prevent future financial strain and ensures your car loan becomes an asset, not a burden.

3. Save for a Significant Down Payment

A substantial down payment is one of the most powerful tools you have when seeking car loans for bad credit. It reduces the amount you need to borrow, which lowers the lender’s risk. It also shows your commitment and financial responsibility.

Aim for at least 10-20% of the car’s purchase price, if possible. Even a 5% down payment can make a difference. The more cash you put down upfront, the better your loan terms are likely to be, and the less interest you’ll pay over the life of the loan.

4. Gather All Necessary Documents

Lenders will require specific documentation to verify your identity, income, and residence. Having these ready will streamline the application process.

Common documents include:

- Proof of Identity: Driver’s license, state ID.

- Proof of Income: Recent pay stubs (last 2-3 months), W-2s, tax returns (if self-employed), bank statements.

- Proof of Residence: Utility bills, lease agreement.

- References: Sometimes required, especially for subprime lenders.

Being prepared with these documents demonstrates your seriousness and efficiency to potential lenders.

Where to Find Car Loans for Bad Credit

Not all lenders are created equal, especially when it comes to financing options for those with less-than-perfect credit. Knowing where to look can significantly impact your success and the terms you receive.

Dealerships Specializing in Bad Credit (Buy Here, Pay Here)

"Buy Here, Pay Here" (BHPH) dealerships can offer easy car loans for bad credit because they often act as both the seller and the lender. This can be convenient, as approval is often quick and based more on your income than your credit score.

However, be cautious. Interest rates at BHPH dealerships are typically much higher, and the vehicle selection might be limited or older. They can be a last resort, but it’s crucial to understand the full terms and conditions before signing.

Subprime Lenders

These lenders specialize in offering loans to individuals with poor credit scores. They have specific programs and criteria tailored to high-risk borrowers. While their interest rates are higher than prime lenders, they are often more competitive than BHPH dealerships.

You can often find subprime lenders through online marketplaces or by asking traditional dealerships if they work with such institutions. These lenders are designed to provide accessible car financing for bad credit.

Online Lenders and Loan Marketplaces

The internet has revolutionized the loan application process. Many online platforms and lenders specialize in connecting bad credit borrowers with suitable financing options. These platforms often allow you to pre-qualify without a hard credit inquiry, letting you compare offers from multiple lenders.

This can be a great way to find easy car loans for bad credit from the comfort of your home. Always research the lender’s reputation and read reviews before applying.

Credit Unions

Credit unions are member-owned financial institutions known for their customer-centric approach. They often have more flexible lending criteria than traditional banks and may be more willing to work with members who have bad credit, especially if you have an existing relationship with them.

If you’re a member of a credit union, or eligible to join one, it’s worth exploring their auto loan options. They can sometimes offer more favorable terms than other subprime lenders.

Traditional Banks

While more challenging, it’s not impossible to get a car loan from a traditional bank with bad credit, especially if you have mitigating factors. For instance, if you have a long-standing relationship with the bank, a significant down payment, or a co-signer, they might be more amenable.

Don’t dismiss your existing bank without inquiring. They might surprise you with an offer, or at least provide valuable advice.

Strategies to Increase Your Approval Chances

Even with bad credit, there are proactive steps you can take to make your application more attractive to lenders. These strategies demonstrate your reliability and reduce the lender’s perceived risk.

1. Consider a Co-signer

A co-signer is someone with good credit who agrees to take on the responsibility of the loan if you fail to make payments. This significantly reduces the lender’s risk, as they have a second, creditworthy individual to pursue. This can make securing easy car loans for bad credit much more feasible.

Based on my experience, a co-signer can often be the difference between approval and rejection, and can even lead to better interest rates. Ensure your co-signer understands their full legal obligation, as their credit will also be affected by your payment history.

2. Opt for a Used Car

New cars depreciate rapidly and carry a higher price tag. A used car, especially one a few years old, will have a lower purchase price, meaning you need to borrow less money. This reduces your monthly payments and makes the loan less risky for the lender.

Choosing a more affordable, reliable used vehicle is a smart move when your priority is getting approved for car financing with bad credit. It helps you get on the road sooner and can be a stepping stone to better credit.

3. Choose a Realistic Vehicle

Resist the urge to buy the most expensive or luxurious car you can find. Lenders will be more comfortable approving a loan for an economy car that aligns with your income. A practical, affordable vehicle demonstrates financial prudence.

Focus on getting reliable transportation first. You can always upgrade once your credit improves and your financial situation stabilizes.

4. Show Proof of Stable Income

Lenders want to see a consistent and reliable source of income. Even with bad credit, proof of steady employment and sufficient income to cover the monthly payments (and other expenses) is a strong indicator of your ability to repay.

Have your pay stubs, bank statements, or other income verification documents ready. The longer your employment history, the better.

5. Explain Your Credit History (If Applicable)

Sometimes, there’s a legitimate reason for your bad credit – a medical emergency, job loss, or divorce. If you can proactively and honestly explain the circumstances to a lender, it can sometimes work in your favor.

Pro tips from us: Be concise, honest, and focus on what you’ve done to improve your situation since. Don’t make excuses, but provide context. This shows maturity and responsibility, which can positively influence a lender’s decision.

Understanding the Loan Terms: What to Look Out For

When you’re offered car loans for bad credit, it’s crucial to scrutinize the loan terms carefully. Higher interest rates are expected, but you need to ensure the overall agreement is fair and manageable.

Interest Rates

Expect higher interest rates with bad credit. This is how lenders compensate for the increased risk. While you won’t get prime rates, you should still compare offers to ensure you’re not paying an exorbitant amount. Even a percentage point or two difference can save you hundreds or thousands over the life of the loan.

Understand that the Annual Percentage Rate (APR) includes both the interest rate and certain fees, giving you a truer picture of the loan’s cost. Always compare APRs, not just interest rates.

Loan Term

The loan term is the length of time you have to repay the loan. Longer terms mean lower monthly payments, which might seem appealing when seeking easy car loans for bad credit. However, a longer term also means you’ll pay significantly more in total interest over time.

Common mistakes to avoid are extending the loan term too much. While a shorter term means higher monthly payments, it drastically reduces the total interest paid and helps you pay off the car faster. Strive for the shortest term you can comfortably afford.

Fees and Charges

Read the fine print for any hidden fees. These can include origination fees, documentation fees, or prepayment penalties. Some fees are standard, but others can inflate the cost of your loan.

Ask for a clear breakdown of all charges. Don’t hesitate to question anything you don’t understand. A reputable lender will be transparent about all costs.

Prepayment Penalties

Some loans include penalties for paying off your loan early. This can negate some of the benefits of making extra payments to save on interest. While less common with auto loans, it’s something to check for.

Ideally, look for a loan that allows you to make extra payments or pay off the loan early without any additional charges. This flexibility can be very beneficial for rebuilding your credit.

Common Mistakes to Avoid When Getting a Bad Credit Car Loan

Navigating the world of car financing with bad credit can be tricky, and certain missteps can cost you significantly. Being aware of these common pitfalls can help you avoid them.

- Not Checking Your Credit Report: As mentioned, errors can exist. Failing to review and correct them means you might be applying with a lower score than you deserve.

- Not Budgeting Properly: Overestimating what you can afford leads to missed payments, further damaging your credit, and potentially losing your vehicle. Always factor in all costs, not just the monthly payment.

- Accepting the First Offer: It’s tempting to take the first approval you get, especially after rejections. However, comparing multiple offers is crucial. You might find significantly better terms elsewhere.

- Falling for Predatory Lenders: Be wary of lenders promising guaranteed approval with no questions asked, or those pressuring you into signing without reading the terms. High-pressure sales tactics are a red flag.

- Ignoring the Fine Print: Every detail in your loan agreement matters. From interest rates to fees and payment schedules, understand everything before you sign. Common mistakes to avoid are rushing this critical step.

Rebuilding Your Credit Through an Auto Loan

One of the significant benefits of successfully obtaining car loans for bad credit is the opportunity to rebuild your credit score. This is a crucial step toward achieving greater financial stability.

How On-Time Payments Help

Every on-time payment you make is reported to the credit bureaus. Consistent, timely payments demonstrate your reliability as a borrower. This positive payment history will gradually improve your credit score over time.

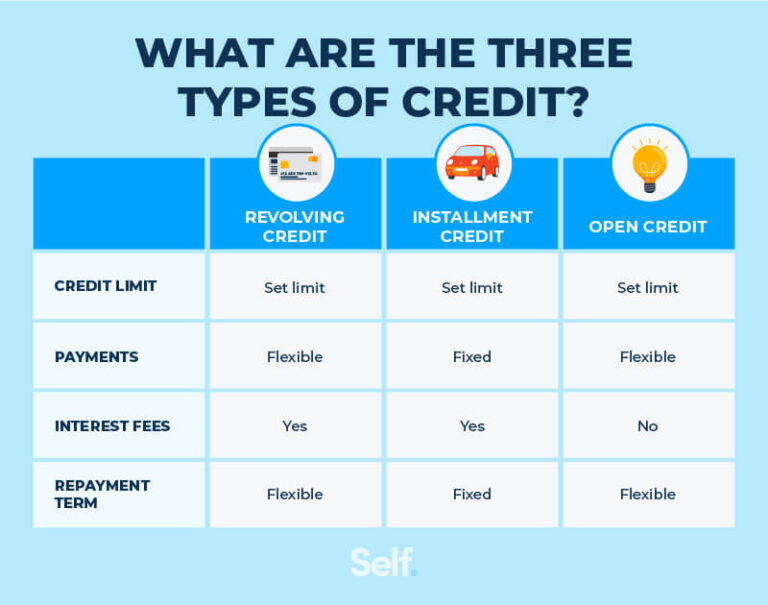

An auto loan is an installment loan, which diversifies your credit mix if you also have revolving credit (like credit cards). This diversity is another factor that can positively impact your score. To learn more about improving your score, consider reading our comprehensive "Guide to Improving Your Credit Score" .

The Importance of Consistency

It’s not just about making payments, but making them consistently and on time, every single month. Set up automatic payments or calendar reminders to ensure you never miss a due date. Even one late payment can set back your credit repair efforts.

Treat this car loan as a major tool for financial recovery. Your diligence now will pay dividends in the future, opening doors to better rates on mortgages, credit cards, and future auto loans.

The Road Ahead: Long-Term Financial Health

Securing easy car loans for bad credit is a significant achievement, but it’s also a stepping stone. Your ultimate goal should be long-term financial health, which extends far beyond this single loan.

Continue to practice sound financial habits. Keep budgeting, managing your debt responsibly, and regularly checking your credit report. Over time, you’ll see your financial standing transform. Understanding how interest rates work across different loans can also be beneficial for future financial decisions; our "Understanding Auto Loan Interest Rates" article provides deeper insights.

Conclusion: Your Journey to Car Ownership with Bad Credit

Getting approved for car loans for bad credit is not just a pipe dream. It requires preparation, diligence, and a strategic approach, but it is entirely achievable. By understanding your credit situation, preparing your finances, knowing where to seek lenders, and avoiding common pitfalls, you can secure the transportation you need.

Remember, "easy" is relative; it doesn’t mean effortless. It means that with the right knowledge and proactive steps, the process can be straightforward and successful. Use this opportunity to not only get a car but also to demonstrate your financial responsibility and pave the way for a stronger credit future. Start planning today, and you’ll be on the road to car ownership and improved financial health.