Empower Your Journey: The Ultimate Guide to Securing and Managing Your Car Loan

Empower Your Journey: The Ultimate Guide to Securing and Managing Your Car Loan Carloan.Guidemechanic.com

The open road, the scent of a new car interior, the thrill of a fresh start – owning a vehicle is a cornerstone of modern life for many. Yet, beneath the excitement lies a complex world of financing. For countless individuals, securing a car loan can feel like navigating a labyrinth, filled with confusing jargon and hidden pitfalls. But what if you could approach this process not with trepidation, but with knowledge and confidence?

This comprehensive guide is designed to help you do just that. We believe in the concept of an "Empower Car Loan" – a loan secured through informed decisions, strategic planning, and a deep understanding of the terms involved. Our mission is to transform you from a passive borrower into an active participant, ensuring you drive away not just with a new car, but with a smart financial decision. Let’s embark on this empowering journey together.

Empower Your Journey: The Ultimate Guide to Securing and Managing Your Car Loan

1. What Exactly is an "Empower Car Loan"? Redefining Your Approach to Auto Financing

When we talk about an "Empower Car Loan," we’re not referring to a specific product from a particular bank. Instead, it’s a philosophy, a strategic mindset that puts you, the borrower, firmly in the driver’s seat of your auto financing journey. It’s about taking control, understanding every facet of your loan, and making choices that genuinely serve your long-term financial well-being.

This approach moves beyond the traditional idea of simply accepting the first loan offer that comes your way. It encourages proactive research, smart comparison shopping, and a willingness to negotiate. An empowered borrower knows their credit standing, understands the implications of different loan terms, and is prepared to challenge unfavorable conditions. Ultimately, an Empower Car Loan is about securing financing that aligns perfectly with your budget and financial goals, ensuring your vehicle ownership experience is a source of freedom, not financial strain.

2. Why Understanding Your Car Loan is Your Ultimate Power Move

Ignorance is certainly not bliss when it comes to financial commitments. A car loan, often one of the largest debts many people take on after a mortgage, has significant long-term financial implications. Understanding its nuances is not just smart; it’s absolutely crucial for your financial health.

By thoroughly grasping the terms of your car loan, you can avoid common pitfalls that cost borrowers thousands of dollars over the life of the loan. This knowledge protects you from predatory lending practices, allows you to identify hidden fees, and empowers you to negotiate for better rates and terms. Based on my experience as a financial content writer, many individuals express regret over past car loans precisely because they didn’t fully understand what they were signing up for. Empowering yourself with knowledge ensures you make decisions you’ll be happy with for years to come.

3. Decoding the Anatomy of a Car Loan: Key Terms You Must Know

Before you even start looking at cars, it’s essential to familiarize yourself with the core components of any car loan. These terms directly impact how much you pay, for how long, and the overall cost of your vehicle.

The Principal: The Core of Your Loan

The principal is the actual amount of money you borrow to purchase the car. This figure is influenced by the vehicle’s selling price, minus any down payment you make or trade-in value you apply. Every payment you make chipping away at this principal amount, alongside the interest.

Understanding the principal is vital because it’s the foundation upon which your interest charges are calculated. A higher principal means more interest paid over the life of the loan, emphasizing the importance of a solid down payment.

Interest Rate (APR): The True Cost of Borrowing

The interest rate is arguably the most critical factor determining the total cost of your loan. It’s expressed as a percentage of the principal and represents the cost of borrowing money from the lender. However, it’s not just the interest rate you need to watch; it’s the Annual Percentage Rate (APR).

The APR provides a more comprehensive picture of your loan’s cost, as it includes not only the interest rate but also any additional fees or charges associated with the loan, such as origination fees. Comparing APRs from different lenders gives you an accurate, apples-to-apples comparison of loan offers. A lower APR translates directly to less money paid over the loan term, saving you significant funds.

Loan Term: How Long Will You Be Paying?

The loan term refers to the duration over which you agree to repay the loan, typically expressed in months (e.g., 36, 48, 60, 72, or even 84 months). The length of your loan term has a direct impact on your monthly payment and the total interest you’ll pay.

A shorter loan term means higher monthly payments but significantly less interest paid over time. Conversely, a longer loan term results in lower monthly payments, making the car seem more affordable upfront, but you’ll end up paying substantially more in interest over the life of the loan. Pro tips from us: Always consider the total cost, not just the monthly payment, when choosing a loan term.

Down Payment: Your Upfront Investment

A down payment is an initial lump sum of money you pay towards the purchase of a car, reducing the amount you need to borrow. This upfront investment is a powerful tool in securing an Empower Car Loan.

Making a substantial down payment can lower your monthly payments, reduce the total interest you pay, and even help you qualify for a better interest rate. It also instantly reduces your loan-to-value (LTV) ratio, which lenders view favorably.

Trade-in Value: Leveraging Your Current Vehicle

If you have an existing vehicle, its trade-in value can act as a form of down payment. Dealers will assess your car’s condition and market value, offering you a credit that reduces the purchase price of your new vehicle.

While convenient, it’s crucial to research your current car’s market value beforehand. Common mistakes to avoid are accepting the first trade-in offer without independent valuation, as this can leave money on the table.

4. Navigating the Landscape: Different Types of Car Loans

The world of auto financing isn’t one-size-fits-all. Different situations call for different types of loans. Understanding these distinctions is key to finding the right fit for your needs and securing an Empower Car Loan.

New Car Loans: The Latest Models

New car loans are specifically for brand-new vehicles purchased from a dealership. They typically come with the lowest interest rates and can offer longer loan terms compared to used car loans. Lenders often see new cars as less risky due to their predictable depreciation and lack of previous ownership issues.

However, new cars also depreciate rapidly, meaning you might owe more than the car is worth, especially in the early years of the loan. This is often referred to as being "upside down" or having negative equity.

Used Car Loans: Pre-Owned Opportunities

Used car loans are for vehicles that have had previous owners. While they can still be secured through dealerships or private sellers, the interest rates tend to be slightly higher than new car loans. This is because used cars are perceived as carrying more risk due to their age, mileage, and potential for unforeseen mechanical issues.

The loan terms for used cars are also often shorter. Despite the potentially higher rates, buying a used car can be a financially savvy move, as you avoid the steepest depreciation hit that new cars experience.

Refinance Car Loans: Optimizing Your Existing Loan

A refinance car loan allows you to replace your current auto loan with a new one, often with a different lender. People typically refinance to secure a lower interest rate, reduce their monthly payments, or change the loan term. This can be a powerful tool for an Empower Car Loan if your financial situation has improved since you first took out your original loan.

Perhaps your credit score has increased, or interest rates have dropped since you initially financed your vehicle. Refinancing can unlock significant savings over the remaining life of your loan. We’ll delve deeper into this later.

Private Party Loans: Buying from an Individual

When you purchase a car directly from an individual seller rather than a dealership, it’s known as a private party sale. Financing these purchases often requires a specific type of loan. Many traditional lenders offer private party auto loans, but they might have different requirements or interest rates compared to dealership loans.

The key difference is that the lender will typically need to appraise the vehicle to ensure its value aligns with the loan amount. This process helps protect both the borrower and the lender.

Dealership Financing vs. Bank/Credit Union: Where to Get Your Loan

You have two primary avenues for securing an auto loan: through the dealership or directly from a bank or credit union. Each has its own set of advantages and disadvantages.

Dealership financing can be convenient, as it’s a one-stop shop where you can select your car and arrange financing simultaneously. Dealers often work with multiple lenders and might offer promotional rates. However, they can also mark up interest rates to earn a profit.

Banks and credit unions, on the other hand, offer direct lending. Securing pre-approval from these institutions gives you significant leverage at the dealership, allowing you to walk in with your own financing offer. Credit unions, in particular, are known for offering competitive rates to their members. Based on countless client interactions, having pre-approval in hand is one of the strongest negotiation tactics you can employ.

5. The Step-by-Step Journey: How to Secure Your Empower Car Loan

Securing an Empower Car Loan is a methodical process that requires preparation and strategic thinking. By following these steps, you can ensure you’re making the best decision for your financial future.

Step 1: Budgeting and Financial Health Check

Before you even think about specific car models, sit down and honestly assess your finances. What is your comfortable maximum monthly payment? Factor in not just the loan payment, but also insurance, fuel, maintenance, and potential registration fees.

Understand your income, expenses, and savings. This crucial first step prevents you from overextending yourself and ensures your car purchase enhances, rather than burdens, your lifestyle.

Step 2: Credit Score Assessment

Your credit score is the single most significant factor influencing the interest rate you’ll be offered. Before applying for any loan, obtain a copy of your credit report from all three major bureaus (Equifax, Experian, TransUnion) and check your score. Many credit card companies and banks now offer free credit score access.

Look for any errors or discrepancies that could negatively impact your score. Resolving these issues before applying can significantly improve your chances of securing a lower interest rate. For more in-depth advice on improving your credit score, check out our article on "Building a Strong Credit Profile for Auto Loans". (Simulated internal link)

Step 3: Pre-Approval Power

This is a game-changer in the Empower Car Loan process. Apply for pre-approval with several banks and credit unions before you set foot in a dealership. Pre-approval means a lender has reviewed your credit and income and is willing to lend you a specific amount at a particular interest rate, typically for a set period (e.g., 30-60 days).

Walking into a dealership with a pre-approval letter transforms you into a cash buyer. You’re no longer dependent on their financing, giving you immense negotiation power over the car’s price. You can then compare the dealership’s financing offer against your pre-approved rate.

Step 4: Car Shopping (Smartly)

With your budget and pre-approval in hand, you can now focus on finding the right car. Remember to negotiate the total price of the car first, separate from any financing discussions. This prevents dealers from manipulating figures to make a higher-priced car seem affordable with a long-term loan.

Test drive multiple vehicles, research reliability, and check market values using sites like Kelley Blue Book or Edmunds. Focus on value and need, not just desire.

Step 5: Reviewing the Loan Offer

Once you’ve settled on a car and have a loan offer (either your pre-approval or the dealer’s), meticulously review all the terms. Pay close attention to the APR, loan term, total interest paid, and any additional fees.

Ensure there are no hidden charges or unexpected additions. Don’t be pressured into signing anything until you fully understand and agree with every detail.

Step 6: Finalizing the Deal

When you’re satisfied with both the car’s price and the loan terms, you can finalize the purchase. Take your time during this stage. Read every document carefully before signing.

Ask questions about anything you don’t understand. A truly empowered borrower takes their time and ensures everything is transparent and accurate.

6. Your Credit Score: The Unseen Force Behind Your Loan Approval

Your credit score is much more than just a number; it’s a powerful financial indicator that significantly influences the terms of your Empower Car Loan. Lenders use your score to assess your creditworthiness – essentially, how likely you are to repay your debt.

How Credit Scores are Calculated

Credit scores, like the FICO score, are typically calculated based on several key factors:

- Payment History (35%): Your track record of paying bills on time. Late payments severely damage your score.

- Amounts Owed (30%): How much debt you carry relative to your credit limits (credit utilization). Lower utilization is better.

- Length of Credit History (15%): The older your accounts, the better.

- New Credit (10%): How many new credit accounts you’ve opened recently. Too many can be a red flag.

- Credit Mix (10%): Having a healthy mix of different credit types (e.g., credit cards, installment loans).

The Direct Link Between Score and Interest Rates

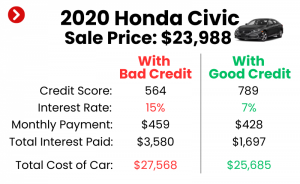

A higher credit score signals to lenders that you are a responsible borrower, making you a lower risk. Lower risk translates directly to lower interest rates on your car loan. Conversely, a lower credit score indicates higher risk, leading to higher interest rates and potentially stricter loan terms. The difference between an excellent score and a good score can mean thousands of dollars saved over the life of a car loan.

Pro Tips from Us: How to Improve Your Score Before Applying

If your credit score isn’t where you want it to be, don’t despair. Here are some actionable steps to improve it before applying for an Empower Car Loan:

- Pay bills on time, every time: This is the most impactful step. Set up auto-pay if necessary.

- Reduce credit card balances: Aim for credit utilization below 30%, ideally even lower.

- Avoid opening new credit accounts: This can temporarily drop your score.

- Check your credit report regularly: Dispute any errors promptly.

- Consider a secured credit card: If you have limited credit history, this can help build it.

7. Mastering the Art of Negotiation: Getting the Best Empower Car Loan Deal

Negotiation is a skill, and it’s particularly valuable when securing an Empower Car Loan. Many people feel intimidated by the process, but with the right strategy, you can significantly improve your outcome.

Separate the Car Price from the Loan Terms

This is a golden rule. Dealers often try to bundle these discussions, which can obscure the true cost of the vehicle and the loan. Insist on negotiating the car’s purchase price first. Once you’ve agreed on a fair price for the vehicle itself, then you can move on to discussing financing options.

This separation allows you to clearly see if you’re getting a good deal on the car and a good deal on the loan independently.

Leverage Pre-Approval

As mentioned, walking in with a pre-approval letter from an outside lender gives you immense power. It establishes a baseline interest rate and loan amount. You can tell the dealer, "I’m pre-approved for X amount at Y% APR."

This forces the dealer to either match or beat your existing offer if they want your financing business. If they can’t, you simply use your pre-approved loan.

Be Willing to Walk Away

This is perhaps the most difficult, yet most effective, negotiation tactic. If a deal doesn’t feel right, if the numbers don’t add up, or if you feel pressured, be prepared to walk out. There are always other cars and other dealerships.

The willingness to walk away signals to the dealer that you are serious about getting a fair deal and won’t be swayed by high-pressure tactics.

Common Mistakes to Avoid: Focusing Only on Monthly Payments

A classic dealer trick is to constantly steer the conversation towards the "affordable" monthly payment. While monthly payments are important for budgeting, focusing solely on them can lead you to accept a longer loan term, a higher interest rate, or unnecessary add-ons, all of which dramatically increase the total cost of the car.

Always ask for the total price of the car and the total cost of the loan (principal plus all interest and fees). This holistic view ensures you’re making a truly empowered decision.

8. Red Flags and Common Mistakes to Avoid When Getting a Car Loan

Even with the best intentions, borrowers can fall victim to common pitfalls. Being aware of these red flags and mistakes is crucial for securing a truly Empower Car Loan.

Not Checking Your Credit Report

As discussed, your credit report can contain errors that negatively impact your score and loan eligibility. Failing to review it means you could be denied a loan or offered a higher interest rate due to incorrect information. Always check your report from all three bureaus annually.

Skipping Pre-Approval

We cannot stress this enough. Not getting pre-approved from an external lender before visiting the dealership is one of the biggest mistakes you can make. It strips you of significant negotiation leverage and leaves you at the mercy of the dealer’s financing options.

Focusing Only on Monthly Payments

This is a recurring theme because it’s such a pervasive and costly mistake. Dealers love to talk about low monthly payments because they can achieve them by extending the loan term to 72 or 84 months, or by adding expensive extras. While the monthly payment looks small, the total interest paid skyrockets, and you risk being "upside down" on your loan for a much longer period.

Adding Unnecessary Extras

Dealerships often push add-ons like extended warranties, GAP insurance, paint protection, or fabric protection. While some of these might have value, many are overpriced or unnecessary. If you decide you need an extended warranty or GAP insurance, research third-party providers for potentially better deals. Always ask for the cost of each add-on separately and consider if it truly provides value.

Not Reading the Fine Print

Loan documents can be dense, but it’s your responsibility to read every single word. Look for prepayment penalties, late payment fees, default clauses, and any other terms that could impact you. Common mistakes to avoid are feeling rushed and signing without full comprehension. If you don’t understand something, ask for clarification until you do.

Based on my experience, these mistakes collectively lead to significant buyer’s remorse and can turn the excitement of a new car into a long-term financial headache.

9. The Power of Refinancing: When and Why to Consider It

Securing an Empower Car Loan isn’t just about the initial purchase; it’s also about managing your loan effectively over its lifetime. Refinancing can be a powerful tool to optimize your existing auto loan and save money.

Lower Interest Rates

The most common reason to refinance is to secure a lower interest rate. If your credit score has improved significantly since you first took out your loan, or if general interest rates have dropped, you might qualify for a much better rate now. Even a percentage point or two can save you hundreds, if not thousands, of dollars over the life of the loan.

Lower Monthly Payments

By extending your loan term or securing a lower interest rate, refinancing can reduce your monthly payments. This can be a lifesaver if your financial situation has changed and you need more breathing room in your budget. However, be cautious: extending the term can also mean paying more interest overall.

Shorter Loan Term (Pay Off Faster)

Conversely, if your financial situation has improved, you might choose to refinance into a shorter loan term with higher monthly payments. This allows you to pay off your car loan faster, significantly reducing the total interest paid and freeing you from debt sooner.

When is it a Good Idea?

Consider refinancing if:

- Your credit score has improved: A higher score makes you eligible for better rates.

- Interest rates have dropped: The market might offer better rates now than when you first borrowed.

- Your financial situation has changed: You need lower payments, or you can afford higher payments to pay off faster.

- You’re unhappy with your current lender: Refinancing allows you to switch to a lender with better customer service or terms.

- You want to remove a co-signer: If your credit has improved, you might be able to qualify on your own.

10. Post-Loan Management: Keeping Your Empower Car Loan on Track

Getting the loan is just the beginning. Effective post-loan management ensures you maintain your empowered position throughout the repayment period.

Making Payments on Time

This might seem obvious, but consistently making your payments on time is paramount. Late payments not only incur fees but also negatively impact your credit score, making future borrowing more expensive. Set up automatic payments to avoid missing due dates.

Understanding Early Payoff Options

Many car loans do not have prepayment penalties, meaning you can pay off your loan early without extra fees. If you have extra cash, consider making additional principal payments. Even small extra payments can shave months off your loan term and save you significant interest.

Budgeting for Maintenance and Insurance

An Empower Car Loan isn’t just about the monthly payment; it’s about the total cost of car ownership. Always budget for ongoing maintenance (oil changes, tires, repairs) and comprehensive car insurance. Unexpected costs can derail your budget if not planned for. If you’re curious about different financing options beyond traditional loans, explore our guide: "Leasing vs. Buying: Which Car Option is Right for You?" (Simulated internal link)

11. Pro Tips for Maximizing Your Car Loan Experience

To truly solidify your Empower Car Loan strategy, here are some final expert tips:

- Get Multiple Quotes: Don’t settle for the first loan offer. Shop around and compare at least three to five offers from different lenders (banks, credit unions, online lenders). This competition often leads to better terms.

- Understand Lender Types: Be aware that some lenders specialize in borrowers with excellent credit, while others cater to those with less-than-perfect scores. Knowing which type of lender you’re approaching can streamline the process.

- Don’t Be Afraid to Ask Questions: If any part of the loan agreement is unclear, ask for clarification. A reputable lender will be happy to explain everything in detail. If they rush you or avoid questions, that’s a major red flag.

- Consider a Shorter Term If Possible: While longer terms offer lower monthly payments, a shorter term saves you substantial money in interest over the loan’s life. If your budget allows, opt for the shortest term you can comfortably afford.

- Utilize Online Calculators: Before you even talk to a lender, use online car loan calculators to estimate monthly payments, total interest, and the impact of different down payments or loan terms. This helps you set realistic expectations.

For more in-depth information on understanding your auto loan, consider consulting resources like the Consumer Financial Protection Bureau (CFPB) which offers valuable, unbiased information on financial products. Learn more about auto loans from the CFPB. (External link)

Conclusion: Drive Away with Confidence

The journey to securing an "Empower Car Loan" is ultimately a journey of knowledge, preparation, and confidence. By understanding the core components of a loan, knowing how your credit score impacts your options, and mastering the art of negotiation, you transform a potentially stressful experience into a strategic financial win. You move from being a recipient of a loan to being an architect of your own financing.

Remember, the goal isn’t just to get a car; it’s to get a car on terms that genuinely benefit your financial future. Apply these principles, ask the right questions, and don’t be afraid to walk away from a bad deal. When you finally drive off the lot, you’ll do so with the peace of mind that comes from making an informed, intelligent, and truly empowered decision. Happy driving!