Envision Your Drive: The Ultimate Guide to Securing Your Ideal Car Loan

Envision Your Drive: The Ultimate Guide to Securing Your Ideal Car Loan Carloan.Guidemechanic.com

The dream of a new car often starts with a vision – the perfect model, the ideal color, the feeling of freedom on the open road. But between that dream and reality lies a crucial step: financing. Navigating the world of car loans can feel like a complex maze, filled with jargon, endless options, and potential pitfalls. This is where the concept of an "Envision Car Loan" comes into play. It’s not just about getting approved; it’s about strategically planning and executing your car financing journey to secure the best possible terms, ensuring your dream car doesn’t become a financial burden.

This comprehensive guide will demystify the entire car loan process, transforming uncertainty into confidence. We’ll delve deep into every facet, from pre-application preparation to post-approval management, equipping you with the knowledge to make informed decisions. Our ultimate goal is to empower you to envision and then achieve a car loan experience that aligns perfectly with your financial goals and driving aspirations. Prepare to embark on a journey that will not only help you secure a great auto loan but also lay a strong foundation for your financial future.

Envision Your Drive: The Ultimate Guide to Securing Your Ideal Car Loan

What Does It Mean to "Envision" Your Car Loan? The Foundation of Success

An "Envision Car Loan" goes far beyond merely filling out an application and hoping for the best. It’s a proactive, strategic approach that treats your car loan as a significant financial commitment, deserving of careful planning and research. This philosophy emphasizes understanding every variable, anticipating challenges, and making choices that serve your long-term financial health.

Think of it as building a house. You wouldn’t just start laying bricks; you’d meticulously plan the blueprints, secure permits, and choose the right materials. Similarly, an Envision Car Loan begins with a clear blueprint of your financial situation and your automotive needs. This foundational step is critical because it sets the stage for a smooth, advantageous borrowing experience. It’s about taking control of the narrative, rather than simply reacting to lender offers.

The Pre-Approval Power Play: Your First Step Towards an Envision Car Loan

One of the most powerful tools in your car loan arsenal is pre-approval. This isn’t just a suggestion; it’s a strategic move that fundamentally shifts the power dynamic from the dealership to you. Seeking pre-approval from a bank, credit union, or online lender before you even set foot on a car lot is a game-changer for your Envision Car Loan.

Why Pre-Approval is Crucial

When you walk into a dealership with a pre-approval letter in hand, you’re no longer just a potential buyer; you’re a cash-equivalent customer. You know exactly how much you can afford, what interest rate you qualify for, and what your monthly payments will look like. This knowledge prevents you from falling in love with a car outside your budget and allows you to negotiate the vehicle price with confidence, knowing your financing is already secured. Based on my experience, buyers who secure pre-approval often report feeling less pressure and achieving better overall deals.

How it Strengthens Your Negotiating Position

With pre-approval, the dealership knows you have options. They understand you’re not solely reliant on their in-house financing, which might not always be the most competitive. This often prompts them to try and beat your pre-approved rate, effectively making lenders compete for your business. It transforms the conversation from "Can I afford this car?" to "What’s the best price you can offer on this car, knowing I already have financing?" This subtle but significant shift is invaluable for achieving your Envision Car Loan.

Common Misconceptions About Pre-Approval

Many people confuse pre-approval with pre-qualification. Pre-qualification is a soft inquiry on your credit that gives you an estimate, but it’s not a firm offer. Pre-approval, on the other hand, involves a hard credit inquiry and results in a concrete loan offer, subject to final verification. Another misconception is that you must take the pre-approved loan. Not at all! It serves as a benchmark. If the dealership can offer something better, fantastic. If not, you have a solid backup.

Decoding Your Credit Score: The Heart of Your Envision Car Loan

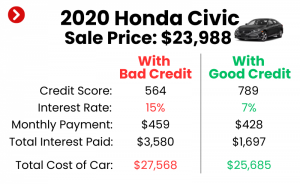

Your credit score is arguably the single most influential factor in securing favorable terms for your Envision Car Loan. Lenders use it as a primary indicator of your creditworthiness and your ability to repay debt. A higher score translates directly into lower interest rates, saving you potentially thousands of dollars over the life of the loan. Understanding and optimizing your credit score is therefore a cornerstone of our Envision strategy.

How Credit Scores Impact Rates

A robust credit score, typically above 700, signals to lenders that you are a low-risk borrower. This allows them to offer you their most competitive interest rates, as they have a high degree of confidence in your repayment. Conversely, a lower score suggests a higher risk, leading to higher interest rates to compensate the lender for that perceived risk. This isn’t just a few decimal points; the difference between a good and poor credit score could mean your interest rate doubles or even triples, drastically increasing your total cost of ownership.

Steps to Improve Your Score Before Applying

If your credit score isn’t where you want it to be, don’t despair! There are actionable steps you can take. First, obtain copies of your credit reports from all three major bureaus (Equifax, Experian, TransUnion) and dispute any errors. Pay down existing credit card balances to reduce your credit utilization ratio, which is a significant factor. Make sure all your payments are on time – payment history is the most important element. If you have any overdue accounts, bring them current. Even a few months of diligent effort can make a noticeable difference.

Understanding Credit Reports

Your credit report is a detailed history of your borrowing and repayment activities. It includes personal information, accounts opened and closed, payment history, public records (like bankruptcies), and inquiries. Familiarizing yourself with its contents is vital. It allows you to spot inaccuracies and understand the factors contributing to your score. For an even deeper dive into this crucial topic, consider checking out our detailed guide on .

The Down Payment Dilemma: How Much is Enough?

The down payment is the initial amount of money you pay upfront for your car. While not always strictly required, making a substantial down payment is a strategic move that can significantly enhance your Envision Car Loan terms and overall financial well-being. It’s a powerful lever you can pull to reduce your borrowing costs and build equity faster.

The Benefits of a Substantial Down Payment

A larger down payment immediately reduces the principal amount you need to borrow, which directly translates to lower monthly payments and less interest paid over the life of the loan. It also provides a buffer against depreciation. Cars lose value rapidly, especially in the first few years. A larger down payment means you’re less likely to be "upside down" on your loan, where you owe more than the car is worth. This financial stability is a key component of an Envision Car Loan.

When a Smaller Down Payment Might Be Acceptable

While a larger down payment is generally advisable, there are situations where a smaller one (or even no down payment) might be acceptable. If you have an exceptionally high credit score and can secure an incredibly low-interest rate, the benefit of tying up a large sum of cash might be less impactful. Additionally, if you plan to pay off the loan very quickly, the total interest savings from a huge down payment might be marginal. However, proceed with caution here; a zero down payment often comes with higher monthly payments and a greater risk of negative equity.

Calculating Your Ideal Down Payment

A common recommendation is to aim for at least 10% of the car’s purchase price, with 20% being even better, especially for new vehicles. To calculate your ideal amount, consider your monthly budget, how much cash you have readily available without depleting your emergency fund, and the interest rate you anticipate receiving. Use online car loan calculators to see how different down payment amounts affect your monthly payments and total interest paid. This informed calculation is part of envisioning your ideal loan.

Navigating Loan Terms and Interest Rates: What to Look For

Beyond the initial approval, the specific terms of your car loan – particularly the interest rate and loan term – will dictate your financial commitment for years to come. Understanding these elements thoroughly is paramount for an Envision Car Loan, ensuring you don’t commit to unfavorable conditions.

APR vs. Interest Rate: The Crucial Difference

While often used interchangeably, the Annual Percentage Rate (APR) and the interest rate are distinct. The interest rate is the cost of borrowing money, expressed as a percentage of the principal. The APR, however, includes the interest rate plus any additional fees associated with the loan, such as administrative charges or origination fees. Pro tips from us: Always compare APRs when evaluating loan offers. The APR provides a more accurate picture of the total annual cost of your loan, allowing for a true apples-to-apples comparison between different lenders.

Loan Term Length: Short vs. Long

The loan term refers to the duration over which you will repay the loan. Common terms range from 36 to 84 months. A shorter loan term (e.g., 36 or 48 months) means higher monthly payments but significantly less interest paid over time. You’ll own the car outright much faster. A longer loan term (e.g., 72 or 84 months) offers lower monthly payments, making the car seem more affordable upfront. However, you’ll pay substantially more in total interest and face a higher risk of being upside down on your loan. For an Envision Car Loan, balance affordability with the total cost and your desired ownership timeline.

Fixed vs. Variable Rates

Most car loans come with a fixed interest rate, meaning your rate and monthly payment remain constant throughout the loan term. This provides predictability and stability, which is highly desirable for budgeting. Variable rates, while less common for car loans, fluctuate based on a benchmark index. While they might start lower, they carry the risk of increasing over time, making your payments unpredictable. For the stability and peace of mind central to an Envision Car Loan, a fixed-rate loan is almost always the preferred choice.

The Application Process: Smooth Sailing with Your Envision Plan

Once you’ve done your homework, prepared your credit, and secured pre-approval, the actual application process for your Envision Car Loan becomes much smoother. Knowing what to expect and having your documents ready will minimize stress and potential delays.

Gathering Necessary Documents

Lenders require specific documents to verify your identity, income, and financial stability. Before applying, gather:

- Proof of Identity: Driver’s license, state ID.

- Proof of Income: Recent pay stubs (last 2-3 months), W-2 forms, tax returns (if self-employed).

- Proof of Residence: Utility bill, lease agreement.

- Proof of Insurance: You’ll need to show proof of auto insurance before driving off the lot.

- Social Security Number: For credit checks.

Having these organized will streamline your application significantly.

Online vs. In-Person Applications

You have options for where to apply. Online lenders often offer competitive rates and a quick application process, allowing you to compare multiple offers from the comfort of your home. Traditional banks and credit unions provide a more personal touch and existing relationship benefits. Dealership financing is convenient but might not always offer the best rates unless they’re competing with your pre-approval. For your Envision Car Loan, consider exploring multiple avenues to find the most advantageous offer.

What Lenders Look For

Beyond your credit score, lenders assess several factors. They want to see a stable employment history, a debt-to-income ratio that indicates you can comfortably manage new payments, and a history of responsible financial behavior. They’ll also consider the loan-to-value (LTV) ratio of the car, comparing the loan amount to the car’s market value. A lower LTV (meaning a larger down payment) is generally more attractive to lenders.

Common mistakes to avoid are: applying to too many lenders at once (which can ding your credit score with multiple hard inquiries), not disclosing all debts, and rushing through the application without understanding the terms. Take your time, be honest, and ask questions.

Understanding the Fine Print: Beyond the Monthly Payment

The monthly payment is what most people focus on, but an Envision Car Loan demands a deeper look. The true cost and flexibility of your loan are often hidden in the fine print. Ignoring these details can lead to unexpected expenses and limitations.

Hidden Fees and Charges

Beyond the principal and interest, car loans can come with various fees. These might include origination fees, documentation fees, processing fees, or even late payment fees. While some are unavoidable, others can be negotiated or avoided by choosing a different lender. Always request a full breakdown of all costs associated with the loan. This transparency is crucial for an Envision Car Loan, allowing you to accurately budget and compare offers.

Early Payoff Penalties

Some loan agreements include "prepayment penalties," which are fees charged if you pay off your loan ahead of schedule. While less common with auto loans than other types of financing, it’s vital to check for this clause, especially if you plan to make extra payments or pay off the loan early. An Envision Car Loan should offer flexibility, not penalize you for being financially responsible. Ensure your loan allows for penalty-free early payoffs.

Gap Insurance and Extended Warranties: Are They Worth It?

Dealerships often push additional products like GAP (Guaranteed Asset Protection) insurance and extended warranties. GAP insurance covers the difference between what you owe on your loan and what your car is worth if it’s totaled or stolen. It can be valuable, especially if you made a small down payment. Extended warranties cover mechanical breakdowns beyond the manufacturer’s warranty. While both can offer peace of mind, they are often marked up significantly at the dealership. Consider purchasing GAP insurance from your auto insurer or a third-party provider, and research independent extended warranty options before committing. An Envision Car Loan means making informed choices about all associated costs. For more information on understanding your auto loan contract, the Consumer Financial Protection Bureau (CFPB) offers excellent resources.

Managing Your Envision Car Loan: Post-Approval Strategies

Securing your ideal Envision Car Loan is a significant achievement, but the journey doesn’t end there. Effective post-approval management is key to maximizing the benefits of your loan and safeguarding your financial health. This phase focuses on smart repayment strategies and staying vigilant for future opportunities.

Setting Up Automatic Payments

One of the simplest yet most effective strategies is to set up automatic payments from your bank account. This ensures your payments are always made on time, every time, preventing late fees and negative impacts on your credit score. Many lenders even offer a small interest rate discount for enrolling in auto-pay. It removes the stress of remembering due dates and contributes to a disciplined financial routine, which is integral to an Envision Car Loan.

Paying Extra When Possible

If your budget allows, making additional payments whenever possible can dramatically reduce the total interest you pay and shorten your loan term. Even small extra contributions, like rounding up your payment each month or applying your tax refund, can have a substantial cumulative effect. Ensure your loan terms allow for extra payments to be applied directly to the principal balance, rather than just towards future interest. This accelerates your path to debt-free car ownership.

Refinancing Opportunities

The car loan market is dynamic, and interest rates can change. If your credit score has improved significantly since you took out your initial loan, or if market rates have dropped, you might be eligible for refinancing. Refinancing means taking out a new loan to pay off your old one, ideally at a lower interest rate or with more favorable terms. Regularly reviewing your loan’s competitiveness is a smart move for any Envision Car Loan holder.

The Impact of Timely Payments on Your Credit

Every on-time payment you make positively contributes to your credit history, reinforcing your credit score. This consistent positive behavior is invaluable for future financial endeavors, whether it’s buying a home, securing a personal loan, or even getting better insurance rates. Your Envision Car Loan isn’t just about the car; it’s a building block for your overall financial reputation.

The Future of Your Envision Car Loan: Beyond Ownership

Your relationship with your Envision Car Loan doesn’t necessarily end when the last payment is made. Planning for future vehicle needs and understanding how your current loan impacts those decisions is a crucial, often overlooked, aspect of long-term financial strategy.

Selling or Trading In a Financed Car

Life changes, and you might find yourself needing to sell or trade in your car before the loan is fully paid off. This is where understanding your car’s market value versus your outstanding loan balance becomes critical. If you owe more than the car is worth (negative equity), you’ll need to cover that difference out of pocket, roll it into your next car loan (which is generally ill-advised), or leverage your GAP insurance if applicable. A well-managed Envision Car Loan helps minimize this risk by reducing your principal balance efficiently.

Planning for Your Next Vehicle

As you approach the end of your current loan term, it’s an opportune time to start envisioning your next car purchase. By consistently making on-time payments and potentially paying extra, you’ve not only improved your credit but also gained valuable experience in managing an auto loan. This puts you in an even stronger position for your next vehicle purchase, allowing you to secure even better terms and continue your cycle of smart financial decisions.

Conclusion: Drive Confidently with Your Envision Car Loan

Securing a car loan doesn’t have to be a stressful ordeal. By adopting the principles of an "Envision Car Loan," you transform a potentially overwhelming process into a strategic, empowering journey. From meticulously preparing your credit and understanding pre-approval to dissecting loan terms and managing your debt responsibly, every step contributes to a more favorable outcome.

Remember, an Envision Car Loan is about more than just the lowest monthly payment; it’s about the total cost of ownership, your financial flexibility, and the long-term impact on your financial health. By being proactive, informed, and diligent, you can confidently navigate the complexities of auto financing and drive away not just with your dream car, but with peace of mind. Start planning your Envision Car Loan journey today, and take control of your automotive future.