Escape the Auto Loan Trap: Your Comprehensive Guide on How To Get Out Of A Bad Car Loan

Escape the Auto Loan Trap: Your Comprehensive Guide on How To Get Out Of A Bad Car Loan Carloan.Guidemechanic.com

Finding yourself trapped in a bad car loan can feel like driving through thick fog – disorienting, stressful, and making it hard to see the road ahead. Many car owners experience this frustration, grappling with high interest rates, overwhelming monthly payments, or a car that’s worth far less than what they owe. It’s a common financial predicament that can severely impact your budget and overall peace of mind.

But here’s the good news: you are not stuck. As an expert in automotive finance and consumer advocacy, I’ve seen countless individuals navigate these challenges successfully. This comprehensive guide is designed to empower you with the knowledge and strategies needed to break free from a bad car loan, improve your financial standing, and drive towards a more secure future. We’ll dive deep into practical solutions, reveal common pitfalls to avoid, and equip you with the insights to make informed decisions.

Escape the Auto Loan Trap: Your Comprehensive Guide on How To Get Out Of A Bad Car Loan

What Exactly Defines a "Bad Car Loan"?

Before we explore solutions, it’s crucial to understand what makes a car loan "bad." It’s not always about the car itself, but often the terms and conditions that create a significant financial burden. Recognizing these signs is the first step toward taking control.

A loan can be considered "bad" if it features an exorbitantly high interest rate, meaning you’re paying far more for the privilege of borrowing than you should. Another major red flag is negative equity, often referred to as being "upside down" on your loan. This occurs when you owe more on the vehicle than its current market value, leaving you in a tricky position if you need to sell or trade it.

Furthermore, an unmanageably high monthly payment that strains your budget or a prolonged loan term (like 72 or even 84 months) can also signal trouble. Long terms often lead to paying significantly more interest over time and can keep you in debt long after the car’s value has depreciated. Lastly, being pressured into unnecessary add-ons like extended warranties or GAP insurance you don’t need can inflate your loan principal without providing real value.

Before You Act: Crucial Initial Steps

Successfully getting out of a bad car loan requires a strategic approach, starting with a thorough assessment of your current situation. This initial groundwork is vital for understanding your options and negotiating effectively. Based on my experience, rushing into a solution without proper preparation can often lead to further complications.

1. Know Your Numbers Inside and Out

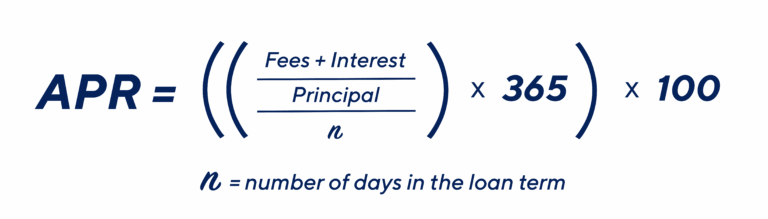

The first step is to gather all the essential details about your current loan. You need to know your exact current loan balance, the annual percentage rate (APR) you’re paying, and your precise monthly payment. Don’t forget to review your original loan agreement for any hidden clauses, such as prepayment penalties, which could affect your strategy.

Next, get an accurate estimate of your car’s current market value. Websites like Kelley Blue Book (KBB.com), Edmunds, or NADAguides are excellent resources for this. Be honest about your car’s condition to get the most accurate appraisal. This comparison between your loan balance and your car’s value will reveal if you have positive or negative equity.

2. Assess Your Credit Score

Your credit score plays a significant role in many of the solutions we’ll discuss, especially refinancing. Obtain a copy of your credit report from one of the three major bureaus (Experian, Equifax, TransUnion) and check your score. Many credit card companies and banks now offer free credit score monitoring, or you can use services like Credit Karma.

A higher credit score opens doors to better interest rates and more favorable loan terms. If your score has improved since you first took out the bad loan, you’re in a much stronger position. Conversely, if it’s declined, you might need to focus on rebuilding it first. For more insights on improving your financial health, consider reading our guide on Understanding Your Credit Score and How to Improve It.

3. Analyze Your Budget and Financial Situation

Take a hard look at your overall budget. Where can you realistically cut expenses to free up extra cash? Even small adjustments can make a big difference in the long run. Understanding your monthly income versus expenses will help you determine how much extra you can afford to put towards your car loan, or if you can comfortably take on a new payment structure.

This exercise isn’t just about finding extra money; it’s about gaining clarity on your financial capacity. It helps you set realistic goals and choose a solution that won’t just replace one financial strain with another. A common mistake to avoid is underestimating your ongoing expenses and overcommitting to a new payment plan.

Strategies to Get Out of a Bad Car Loan

Now that you’ve done your homework, let’s explore the most effective strategies for escaping a bad car loan. Each option has its own benefits and considerations, and the best path for you will depend on your unique financial situation.

1. Refinancing Your Car Loan

Refinancing is often the first and most effective strategy for many people looking to get out of a bad car loan. It involves taking out a new loan to pay off your existing one, ideally with more favorable terms. The goal is typically to secure a lower interest rate, reduce your monthly payments, or shorten your loan term.

How Refinancing Works

To refinance, you’ll apply for a new car loan, usually from a different lender than your original one. This new lender will assess your creditworthiness, just as they did for your initial loan. If approved, the new loan funds are used to pay off your old loan, and you begin making payments to the new lender under the new terms. This can significantly reduce the total amount of interest you pay over the life of the loan.

When Refinancing is a Good Option

Refinancing is particularly beneficial if your credit score has improved since you first took out the loan. A better score makes you eligible for lower interest rates. It’s also a strong option if interest rates in the market have generally dropped, or if you were initially given a very high rate due to limited credit history or poor negotiation. Pro tips from us: always shop around with multiple lenders – banks, credit unions, and online lenders – to compare offers. Credit unions often have some of the most competitive rates.

Considerations and Potential Pitfalls

While refinancing can be a lifesaver, it’s not always a perfect solution. If you have significant negative equity (you owe far more than the car is worth), some lenders might be hesitant to refinance without a substantial down payment. Additionally, extending your loan term through refinancing to lower your monthly payment might seem appealing, but it can lead to paying more interest overall. Carefully weigh the pros and cons to ensure you’re truly improving your financial situation.

2. Accelerating Your Payments

Sometimes, the simplest solution is the most powerful: paying more than the minimum monthly amount. This strategy might not feel like "getting out" of the loan, but it dramatically shortens the loan term and reduces the total interest paid, effectively transforming a "bad" loan into a manageable one.

The Power of Extra Payments

When you make extra payments, ensure they are applied directly to the principal balance of your loan. By reducing the principal, you reduce the amount of money on which interest accrues. Even small, consistent extra payments can shave months or even years off your loan term and save you hundreds or thousands in interest. For example, if your payment is $300, consistently paying $350 can make a significant difference.

Strategic Ways to Pay More

One popular method is making bi-weekly payments. Instead of one monthly payment, you make half of your payment every two weeks. Since there are 26 bi-weekly periods in a year, you’ll end up making the equivalent of 13 full monthly payments instead of 12. This subtle increase can significantly accelerate your payoff. Another approach is to round up your payment or apply any unexpected windfalls, like tax refunds or bonuses, directly to the principal.

Staying Disciplined

The key to this strategy is discipline. Set up automatic extra payments if possible, so you don’t have to think about it. Regularly check your loan balance to see the impact of your efforts, which can be highly motivating. This method is particularly effective if refinancing isn’t an option due to poor credit or significant negative equity, as it gives you direct control over your debt.

3. Selling Your Vehicle

Selling your car can be a direct way to get out of a bad loan, especially if you have positive equity or can cover a small negative equity gap. This allows you to eliminate the loan entirely and gives you a fresh start.

Private Sale vs. Dealership Trade-In

You generally have two options: selling privately or trading it in at a dealership. A private sale usually fetches a higher price for your car, maximizing your chances of covering the loan balance. However, it requires more effort – advertising, showing the car, and handling paperwork. A dealership trade-in is more convenient but typically yields a lower offer, making it harder to cover an outstanding loan.

Dealing with Negative Equity When Selling

If you’re upside down on your loan, selling your car means you’ll need to pay the difference between the sale price and your loan balance out of pocket. For example, if you sell your car for $15,000 but owe $17,000, you’ll need to pay $2,000 to the lender to close the loan. This can be challenging but might be worthwhile if the new car loan or no car loan at all is a better financial move.

Pro tip: If you have significant negative equity and cannot cover the gap, you might explore a small personal loan to cover the difference, but only if the interest rate is significantly lower than your car loan and you have a clear plan for repayment. This must be approached with extreme caution to avoid simply swapping one bad debt for another.

4. Trading In Your Car (Carefully)

Trading in your car, especially if you’re upside down, requires extreme caution. While it seems like a convenient way to transition to a new vehicle, it can easily perpetuate or worsen your bad car loan situation if not handled correctly.

The Dangers of "Rolling Over" Negative Equity

The most common mistake when trading in an upside-down car is "rolling over" the negative equity into a new loan. This means the difference between what your car is worth and what you owe is added to the principal of your new car loan. For example, if you owe $20,000 but your trade-in is only worth $15,000, that $5,000 deficit gets tacked onto your new vehicle’s price.

This practice immediately puts you upside down on your new loan, often with a higher principal and potentially a longer term. You end up paying interest on a vehicle you no longer own, compounding your financial problems. As an expert, I always advise clients to avoid rolling over negative equity whenever possible.

When a Trade-In Might Work

A trade-in can be a viable option if you have little to no negative equity, or if you’re able to make a substantial down payment on the new vehicle to cover any existing gap. It can also work if the new car offers significantly better fuel efficiency, lower maintenance costs, or a much lower interest rate, leading to overall savings that outweigh the trade-in disadvantage. Always negotiate the trade-in value separately from the new car’s price. For general advice on car purchasing, you might find our article on Smart Strategies for Buying a Used Car helpful.

5. Debt Consolidation or Personal Loan

In some specific scenarios, using a personal loan or a debt consolidation loan might be a way to pay off a high-interest car loan. This strategy can be beneficial if you qualify for a personal loan with a significantly lower interest rate than your current auto loan.

How It Works

You would apply for an unsecured personal loan from a bank, credit union, or online lender. If approved, you use the funds from this personal loan to pay off your existing car loan in full. You then make payments on the personal loan. The key advantage here is securing a lower interest rate, which can reduce your monthly payments and the total amount of interest paid over time.

Considerations and Risks

This approach works best if your credit score has improved significantly, allowing you to qualify for excellent personal loan terms. However, personal loans are typically unsecured, meaning they don’t have collateral (like your car). Because of this, their interest rates can sometimes be higher than secured auto loans, especially if your credit isn’t stellar. Always compare the APRs carefully.

Furthermore, consider the loan term. A longer personal loan term might reduce your monthly payment but could lead to paying more interest overall. A common mistake is consolidating debt without addressing the underlying spending habits that led to the initial bad loan, potentially leading to new debt.

6. Negotiating Directly with Your Lender

If you’re facing genuine financial hardship that makes it impossible to make your car loan payments, don’t just stop paying. Contact your lender immediately to discuss your situation. Many lenders are willing to work with borrowers who are proactive and transparent.

Options to Discuss

Your lender might offer several options:

- Loan Modification: They might be willing to adjust your interest rate, extend your loan term, or reduce your monthly payment temporarily.

- Deferment or Forbearance: This allows you to temporarily pause or reduce payments for a set period, giving you time to get back on your feet. However, interest usually continues to accrue during this time, and the deferred payments will still need to be made later.

- Settlement: In severe cases, especially if you’re significantly behind, a lender might consider settling for a lower payoff amount than what you owe. This is rare and typically has a very negative impact on your credit score, similar to a repossession.

Be Prepared and Proactive

When contacting your lender, be prepared to explain your situation clearly and provide any necessary documentation of your hardship (e.g., job loss letter, medical bills). Being proactive and communicating openly is crucial. Ignoring the problem will only lead to more severe consequences, such as late fees, damage to your credit, and ultimately, repossession.

7. The Last Resort: Voluntary Repossession

While technically a way to "get out" of the car loan, voluntary repossession should almost always be considered a last, last resort. As an expert, I always advise clients to exhaust all other options before considering this path due to its severe and long-lasting negative consequences.

What Happens During Voluntary Repossession

If you can no longer afford your car payments, you can inform your lender that you are voluntarily surrendering the vehicle. The lender will then take possession of the car and typically sell it at auction. The proceeds from the sale are applied to your outstanding loan balance.

The Severe Consequences

The critical issue is that the sale price at auction is usually much lower than the car’s market value. This often leaves a "deficiency balance" – the difference between what you owed and what the car sold for, plus repossession and auction fees. You will still be legally obligated to pay this deficiency balance. The lender can pursue you for this amount, potentially leading to collections, lawsuits, and wage garnishment.

Moreover, a voluntary repossession will severely damage your credit score, remaining on your credit report for up to seven years. This makes it incredibly difficult to obtain future loans, mortgages, or even rent an apartment. Always explore every other possible avenue, including selling the car yourself (even at a loss you cover with a personal loan), before considering voluntary repossession.

Prevention is Key: Avoiding Future Bad Car Loans

Getting out of a bad car loan is a huge accomplishment, but the ultimate goal is to never get into one again. Learning from past experiences is invaluable. Here are proactive steps to ensure your next automotive financing experience is positive.

1. Research and Understand Before You Buy

Never walk into a dealership unprepared. Research the market value of the car you’re interested in, both new and used. Understand typical interest rates for someone with your credit score. Knowledge is power, and it gives you leverage in negotiations.

2. Shop for Financing First

One of the most powerful strategies is to secure pre-approval for a car loan before you even set foot on a dealership lot. This means you know your interest rate and loan terms ahead of time. It puts you in the position of a cash buyer, giving you immense negotiation power and preventing the dealer from playing games with financing.

3. Improve Your Credit Score

A strong credit score is your best friend when it comes to securing favorable loan terms. Work on paying bills on time, reducing existing debt, and monitoring your credit report for errors. A few points increase can translate into significant savings on interest over the life of a loan.

4. Make a Substantial Down Payment

Putting more money down upfront reduces the amount you need to borrow, which means less interest paid overall. It also helps to prevent you from being upside down on your loan early on, providing a buffer against depreciation. Aim for at least 10-20% of the car’s value.

5. Choose a Shorter Loan Term

While longer loan terms offer lower monthly payments, they dramatically increase the total interest you pay and keep you in debt longer. Opt for the shortest loan term you can comfortably afford, ideally 36 or 48 months, but no more than 60 months.

6. Scrutinize Add-Ons and Hidden Fees

Be wary of dealership add-ons like extended warranties, rustproofing, or fabric protection unless you genuinely need them and they offer real value. These often come with high markups and inflate your loan principal unnecessarily. Read every line of the contract before signing, and don’t hesitate to ask questions.

7. Focus on the Total Cost, Not Just the Monthly Payment

Dealerships often try to steer conversations toward the "affordable" monthly payment. While monthly payments are important for budgeting, always keep your eye on the total cost of the car, including interest. A lower monthly payment over a longer term can hide a much higher overall cost.

Conclusion: Take Control of Your Financial Journey

Escaping a bad car loan might seem like a daunting challenge, but with the right information and a proactive approach, it is absolutely achievable. We’ve explored a range of powerful strategies, from refinancing and accelerating payments to carefully considering selling or trading in your vehicle. Each option offers a unique path to financial freedom, and the best choice for you will depend on your personal circumstances and financial goals.

Remember, the journey out of a bad car loan begins with understanding your situation, exploring all available solutions, and making informed decisions. Don’t be afraid to seek professional advice or negotiate with lenders. By taking control, you’re not just getting rid of a loan; you’re taking a significant step towards greater financial stability and peace of mind. Drive forward with confidence, armed with the knowledge to make smart choices for your automotive future.