First Citizens Bank Car Loan: Your Ultimate Guide to Driving Away with Confidence

First Citizens Bank Car Loan: Your Ultimate Guide to Driving Away with Confidence Carloan.Guidemechanic.com

Buying a car is a significant life event, often marking a new chapter, enhanced mobility, or simply fulfilling a long-held dream. For many, this dream relies on securing the right financing. Navigating the world of auto loans can feel overwhelming, with countless options and terms to understand. That’s where a trusted financial partner like First Citizens Bank comes into play.

As an expert in auto financing, I’ve seen firsthand how crucial it is to choose a lender that not only offers competitive rates but also provides clear guidance and exceptional service. This comprehensive guide will walk you through everything you need to know about securing a First Citizens Bank Car Loan, from understanding your options to navigating the application process and managing your loan effectively. Our goal is to empower you with the knowledge to make an informed decision and drive away with confidence.

First Citizens Bank Car Loan: Your Ultimate Guide to Driving Away with Confidence

Why Choose First Citizens Bank for Your Car Loan?

When it comes to financing a vehicle, selecting the right institution is paramount. First Citizens Bank has established itself as a reliable choice for countless individuals seeking auto loans. Their approach combines modern banking solutions with a commitment to personalized customer service.

A Legacy of Trust and Reliability

First Citizens Bank boasts a long and reputable history in the financial sector. This extensive experience translates into a deep understanding of customer needs and a commitment to stability. Their longevity offers a sense of security, which is invaluable when entrusting a bank with a major purchase like a car.

Based on my experience, working with a bank that has a solid foundation often means more consistent policies and a less volatile lending environment. This stability can be a significant advantage for borrowers looking for predictable terms.

Diverse Loan Options to Fit Your Needs

One of the standout features of First Citizens Bank is its flexibility in offering various auto loan products. Whether you’re eyeing a brand-new model, a reliable used vehicle, or looking to refinance an existing loan, they likely have a solution tailored for you. This comprehensive approach ensures that a wide range of financial situations and vehicle preferences can be accommodated.

They understand that not all car buying journeys are the same, and their product suite reflects this understanding. This versatility allows you to explore options that genuinely match your specific circumstances.

Competitive Rates and Transparent Terms

First Citizens Bank aims to provide competitive interest rates and transparent loan terms, which are critical components of any favorable auto loan. They strive to offer rates that stand up against other lenders, helping you keep your overall borrowing costs down. Moreover, clarity in their terms means you’ll understand exactly what you’re signing up for without hidden surprises.

Pro tips from us: Always compare the Annual Percentage Rate (APR), not just the interest rate, as APR includes all fees and charges, giving you a truer picture of the loan’s cost. First Citizens Bank is generally upfront with this information.

Personalized Customer Service

In an increasingly digital world, the human touch remains invaluable, especially for significant financial decisions. First Citizens Bank prides itself on offering personalized customer service, whether you prefer to apply online or speak with a loan officer in person. Their local branch network provides opportunities for face-to-face consultations, allowing you to ask questions and receive tailored advice.

This personal connection can make a significant difference, particularly if you have unique financial circumstances or simply prefer a more guided approach to your auto loan application.

Understanding First Citizens Bank Car Loan Options

First Citizens Bank offers a range of auto loan products designed to cater to different vehicle acquisition needs. Understanding these options is the first step toward finding the perfect financial fit for your next car. Each type of loan has specific considerations and benefits.

New Car Loans

If you’re dreaming of that pristine, factory-fresh vehicle, a new car loan from First Citizens Bank can help make it a reality. These loans are typically for vehicles that have never been owned and have very low mileage, often directly from a dealership. New car loans often come with the most attractive interest rates due to the vehicle’s higher resale value and lower depreciation risk for the lender.

The terms for new car loans can vary, but they generally offer flexible repayment schedules, allowing you to choose a term that aligns with your budget. While longer terms can mean lower monthly payments, remember they often result in paying more interest over the life of the loan.

Used Car Loans

Opting for a used car can be a smart financial move, offering excellent value and reducing the immediate depreciation hit. First Citizens Bank provides robust used car loan options, whether you’re buying from a dealership or a private seller. The key difference here often lies in the vehicle’s age and mileage, which can influence both the loan amount and the interest rate.

Lenders typically have limits on the age or mileage of a used car they will finance. Based on my experience, older vehicles or those with very high mileage might face slightly higher interest rates or shorter loan terms due to increased risk. However, First Citizens Bank aims to provide competitive rates even for pre-owned vehicles, making them accessible.

Auto Loan Refinancing

Perhaps you already have a car loan but are looking for a better deal. Auto loan refinancing through First Citizens Bank could be your solution. Refinancing involves taking out a new loan to pay off your existing car loan, ideally at a lower interest rate or with more favorable terms. This can lead to lower monthly payments, significant savings on interest over time, or a shorter repayment period.

Pro tips from us: Refinancing is particularly beneficial if your credit score has improved since you first took out your loan, or if interest rates have dropped. It’s also a good strategy if you want to adjust your monthly payment to better fit your current budget.

Lease Buyout Loans

For those currently leasing a vehicle, a lease buyout loan from First Citizens Bank offers an avenue to purchase your car at the end of your lease term. When your lease concludes, you typically have the option to return the car or buy it outright for a predetermined residual value. A lease buyout loan provides the financing to cover this purchase price.

This option can be appealing if you love your leased car, have maintained it well, and the buyout price is favorable compared to its market value. It allows you to continue driving a vehicle you’re already familiar with, avoiding the hassle of finding a new car.

Navigating the First Citizens Bank Car Loan Application Process

Applying for a car loan can seem daunting, but First Citizens Bank streamlines the process to make it as straightforward as possible. Understanding each step can significantly reduce stress and improve your chances of approval.

Step 1: Research and Preparation

Before you even think about applying, thorough preparation is crucial. This involves understanding your financial standing and the type of vehicle you intend to purchase. Begin by checking your credit score and report. Your creditworthiness is a primary factor lenders consider.

Common mistakes to avoid are applying without knowing your credit score or trying to finance a car that’s beyond your budget. Pro tips from us: Get a free copy of your credit report from AnnualCreditReport.com to identify any errors and understand your financial health. Also, determine a realistic budget for your monthly payment and overall loan amount.

Step 2: Pre-Approval – Your Strategic Advantage

Seeking pre-approval from First Citizens Bank is a highly recommended step. Pre-approval means the bank has conditionally agreed to lend you a certain amount, based on a preliminary review of your credit and financial information. This gives you a clear budget before you even step onto a dealership lot.

The benefits of pre-approval are substantial. It gives you significant bargaining power with dealerships, as you’re essentially a cash buyer. You can focus on negotiating the car price, not the financing. It also provides peace of mind, knowing your financing is largely secured.

Step 3: Gathering Required Documents

Once you’re ready to apply, either for pre-approval or a full loan, you’ll need a set of documents. Having these ready in advance can expedite the entire process. While specific requirements can vary, typical documents include:

- Proof of Identity: Valid government-issued ID (driver’s license, passport).

- Proof of Income: Recent pay stubs, W-2 forms, tax returns, or bank statements if self-employed.

- Proof of Residence: Utility bill, lease agreement, or mortgage statement.

- Vehicle Information (if applicable): VIN, make, model, year, and mileage for the car you intend to purchase.

- Social Security Number: For credit checks.

Common mistakes to avoid are presenting outdated documents or incomplete information, which can cause delays.

Step 4: Submitting Your Application

First Citizens Bank offers multiple convenient ways to submit your car loan application. You can apply online through their secure portal, visit a local branch to speak with a loan officer, or even apply over the phone. Each method is designed to be user-friendly, allowing you to choose what works best for you.

When applying, be sure to provide accurate and complete information. Any discrepancies could lead to questions or delays in processing your application.

Step 5: Understanding the Decision

After submitting your application, First Citizens Bank will review your information, including your credit history and financial stability. This typically involves a hard inquiry on your credit report. You will then receive a decision: approval, conditional approval (requiring more information), or denial.

If approved, you’ll receive the terms of your loan, including the interest rate, loan amount, and repayment schedule. If denied, the bank is legally required to provide you with the reasons for the denial, allowing you to address any issues for future applications.

Key Factors Influencing Your First Citizens Bank Car Loan Approval & Rates

Several critical factors play a pivotal role in determining whether your First Citizens Bank car loan application is approved and what interest rate you’ll receive. Understanding these elements can help you prepare and potentially improve your loan terms.

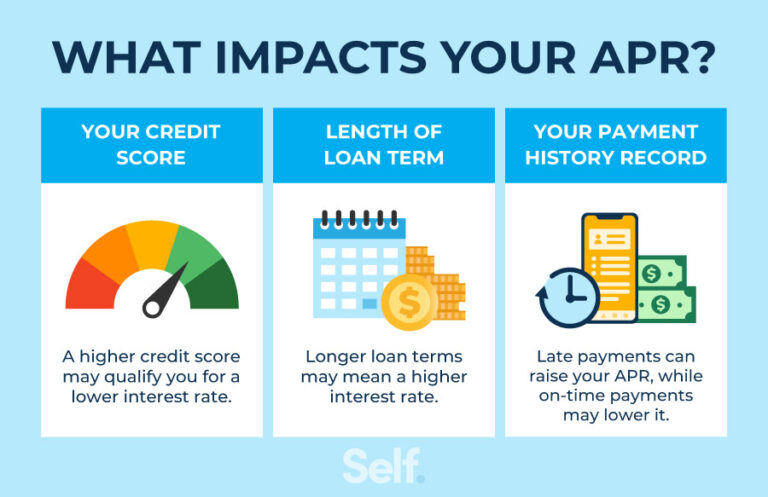

Credit Score: The Cornerstone of Loan Approval

Your credit score is arguably the most influential factor in securing an auto loan and determining your interest rate. It’s a numerical representation of your creditworthiness, reflecting your history of borrowing and repaying debt. Lenders use this score to assess the risk of lending to you. A higher credit score signals a lower risk, often leading to better rates and more favorable terms.

Based on my experience, a strong credit score (generally 700+) can save you thousands of dollars over the life of a car loan. First Citizens Bank, like other lenders, typically reserves its lowest rates for borrowers with excellent credit histories.

Debt-to-Income Ratio (DTI)

Beyond your credit score, lenders assess your ability to manage additional debt. Your debt-to-income (DTI) ratio compares your total monthly debt payments to your gross monthly income. A lower DTI ratio indicates that you have more disposable income to cover new loan payments, making you a less risky borrower.

First Citizens Bank will look for a DTI ratio that suggests you can comfortably afford the monthly car loan payment without overextending your finances. Common mistakes to avoid are taking on too much new debt just before applying for a car loan, as this can negatively impact your DTI.

Loan Amount and Term

The total amount you wish to borrow and the repayment period (loan term) significantly impact your monthly payments and the total interest you’ll pay. A larger loan amount or a longer loan term will naturally result in higher total interest paid, even if the monthly payments are lower.

While First Citizens Bank offers flexible terms, it’s wise to consider the trade-off between a lower monthly payment and the overall cost of the loan. Pro tips from us: Aim for the shortest loan term you can comfortably afford, as this minimizes the total interest paid.

Down Payment

Making a substantial down payment on your vehicle can greatly improve your loan application. A larger down payment reduces the amount you need to borrow, which can lower your monthly payments and decrease the total interest paid. It also signals to the lender that you are financially committed to the purchase, reducing their risk.

A significant down payment can also help you avoid being "upside down" on your loan, where you owe more than the car is worth, especially given a new car’s initial depreciation.

Vehicle Specifics

The characteristics of the car you intend to finance also play a role. For used cars, factors like the vehicle’s age, mileage, make, and model can influence the loan amount and interest rate. Lenders consider the car’s resale value and its likelihood of maintaining value over the loan term.

First Citizens Bank will typically have guidelines regarding the types of vehicles they finance, particularly for older or very high-mileage used cars. This is to ensure the collateral (the car itself) adequately secures the loan.

Tips for Securing the Best First Citizens Bank Car Loan Deal

Getting an auto loan isn’t just about approval; it’s about securing the most favorable terms possible. With some strategic planning, you can significantly improve your chances of getting an excellent deal on your First Citizens Bank car loan.

Boost Your Credit Score

As discussed, your credit score is king. Before applying, take steps to improve it. Pay down existing debts, especially credit card balances, and ensure all your payments are made on time. Dispute any errors on your credit report. Even a few points increase can translate into a lower interest rate.

This proactive approach demonstrates financial responsibility, making you a more attractive borrower to First Citizens Bank.

Save for a Down Payment

Aim to save at least 10-20% of the vehicle’s purchase price for a down payment. A larger down payment reduces the loan amount, lowers your monthly payments, and shows the bank your commitment. It also helps mitigate the risk of being upside down on your loan.

Pro tips from us: Even a 5% down payment is better than none, but pushing for more will always benefit you in the long run with lower interest costs.

Shop Around (Even with FCB)

While First Citizens Bank offers competitive rates, it’s always wise to compare their offer with those from other lenders. This doesn’t mean you shouldn’t go with FCB, but rather that being informed about the market rates gives you leverage. Knowing what other banks or credit unions are offering can help you confidently accept First Citizens Bank’s best offer or, if needed, negotiate.

You can visit sites like Bankrate.com or Nerdwallet.com for general market rates. (External Link: Check current auto loan rates on Bankrate.com)

Consider a Co-Signer (If Necessary)

If your credit history is limited or your score isn’t as strong as you’d like, a co-signer with excellent credit can significantly improve your chances of approval and help you secure a lower interest rate. A co-signer agrees to be equally responsible for the loan, providing an additional layer of security for First Citizens Bank.

However, ensure both parties understand the full implications. If you default, the co-signer’s credit will be negatively impacted.

Negotiate Wisely

Even after securing pre-approval from First Citizens Bank, there’s still room for smart negotiation. Focus on negotiating the vehicle’s purchase price first, separate from the financing. Once you have a firm price, then discuss the financing terms. Do not let the dealership try to combine these two aspects, as it can confuse the real cost.

Your pre-approval acts as your "outside financing" option, giving you the power to walk away if the dealer’s financing isn’t as good.

Post-Approval: Managing Your First Citizens Bank Car Loan

Once your First Citizens Bank car loan is approved and you’ve driven off the lot, the journey isn’t over. Effective loan management is crucial to ensure a smooth repayment process and to maximize your financial well-being.

Understanding Your Loan Agreement

Before you sign on the dotted line, meticulously read and understand every clause in your First Citizens Bank loan agreement. Pay close attention to the interest rate (APR), the total loan amount, the repayment schedule, any fees (late payment, early payoff penalties), and what happens in case of default.

Common mistakes to avoid are rushing through the paperwork. If anything is unclear, ask your First Citizens Bank loan officer for clarification. It’s your right to understand every detail of your financial commitment.

Convenient Payment Options

First Citizens Bank typically offers several convenient ways to make your monthly car loan payments. These often include:

- Online Banking: Set up recurring payments directly from your checking or savings account.

- Automatic Payments (Auto-Pay): Enroll in auto-pay to ensure your payments are always on time, potentially avoiding late fees and improving your credit history.

- Mobile App: Manage your loan and make payments on the go.

- In-Branch Payments: Visit any First Citizens Bank branch to make a payment in person.

- Mail: Send a check or money order.

Pro tips from us: Setting up automatic payments is highly recommended to avoid missed payments, which can negatively impact your credit score.

Early Payoff Strategies

If your financial situation improves, you might consider paying off your First Citizens Bank car loan early. This can save you a significant amount in interest over the life of the loan. Before making extra payments, confirm with the bank that there are no prepayment penalties.

Strategies for early payoff include:

- Making extra principal payments: Clearly designate additional payments towards the principal balance.

- Bi-weekly payments: Instead of one monthly payment, make half-payments every two weeks. This results in one extra full payment per year, significantly shortening your loan term.

- Round up your payments: If your payment is $325, pay $350. The extra $25 will chip away at the principal.

For more insights on managing debt and making smart financial choices, consider reading our article on Effective Strategies for Debt Management and Savings (Internal Link example).

What If You Face Payment Difficulties?

Life can be unpredictable, and sometimes financial challenges arise. If you anticipate or are experiencing difficulty making your First Citizens Bank car loan payments, the most important step is to communicate with the bank immediately. Do not wait until you miss a payment.

First Citizens Bank may be able to work with you to explore options like temporary payment deferrals, loan modifications, or other solutions that can help you get back on track without severely damaging your credit or risking vehicle repossession. Open communication is key to finding a resolution.

Common Mistakes to Avoid When Getting a Car Loan

Even with all the right information, it’s easy to stumble into common pitfalls during the car loan process. Being aware of these mistakes can help you navigate your First Citizens Bank car loan application more smoothly and save you money.

Ignoring Your Credit Score

Many individuals apply for a car loan without first checking their credit score. This can lead to unpleasant surprises, higher interest rates, or even denial. Your credit score is the single most important factor for lenders.

Pro tips from us: Always review your credit report for errors and take steps to improve your score before applying. For a deeper dive, check out our guide on Understanding Your Credit Score: A Beginner’s Guide (Internal Link example).

Skipping Pre-Approval

As highlighted earlier, skipping the pre-approval step puts you at a disadvantage. Without it, you lack a clear budget and negotiating power at the dealership. You might end up focusing solely on monthly payments, potentially accepting unfavorable loan terms bundled into the car price.

Always get pre-approved by First Citizens Bank or another lender before you start serious car shopping.

Focusing Only on Monthly Payments

Dealers often highlight only the monthly payment, trying to make a car seem more affordable. However, a low monthly payment might be achieved through a very long loan term, leading to significantly more interest paid over time.

Always look at the total cost of the loan, including the interest rate, loan amount, and the overall amount you’ll pay back.

Not Reading the Fine Print

Loan agreements can be complex documents. Failing to read the fine print means you could miss important details about fees, penalties, or specific terms that could affect your financial future.

Take your time to understand every aspect of your First Citizens Bank loan agreement before signing. Don’t hesitate to ask questions.

Buying More Car Than You Can Afford

It’s easy to get carried away by the excitement of a new vehicle. However, buying a car that stretches your budget too thin can lead to financial strain down the road. This includes not just the loan payment, but also insurance, maintenance, and fuel costs.

Be realistic about what you can afford comfortably. Remember, a car is a depreciating asset.

Falling for Dealer Financing Tricks Without Comparing

Dealerships often have their own financing options and may try to steer you towards them. While some dealer financing can be competitive, it’s not always the best deal. They might offer incentives that seem attractive but come with hidden costs or higher interest rates.

Always compare the dealer’s offer with your First Citizens Bank pre-approval. Your pre-approval acts as your benchmark and gives you leverage.

Conclusion: Drive Away with Confidence with First Citizens Bank

Securing a car loan is a significant financial decision, and choosing the right partner can make all the difference. First Citizens Bank offers a robust suite of car loan options, competitive rates, and a commitment to customer service that can help you navigate this process with ease and confidence.

By understanding your options, diligently preparing for your application, and making informed decisions throughout the process, you empower yourself to get the best possible deal. Remember the importance of your credit score, the value of a down payment, and the strategic advantage of pre-approval.

Whether you’re purchasing a new or used vehicle, refinancing an existing loan, or exploring a lease buyout, First Citizens Bank stands as a reliable institution ready to assist you. With the insights from this ultimate guide, you are well-equipped to embark on your car buying journey, securing a First Citizens Bank car loan that aligns with your financial goals and gets you on the road with peace of mind. Drive away confidently, knowing you’ve made a smart and informed choice.