From Bank of the West to BMO Harris: Navigating Your Auto Loan Journey with Confidence

From Bank of the West to BMO Harris: Navigating Your Auto Loan Journey with Confidence Carloan.Guidemechanic.com

The open road beckons, and the dream of a new or pre-owned vehicle often begins with securing the right auto loan. For years, many in the western United States turned to Bank of the West for their financing needs. However, the financial landscape is constantly evolving, and understanding these changes is crucial for anyone looking to finance a car today.

This comprehensive guide will demystify the process of obtaining an auto loan, specifically addressing the transition from Bank of the West to BMO Harris. We’ll explore what this means for prospective car buyers, delve into the specifics of BMO Harris auto financing, and equip you with the knowledge to secure the best possible terms for your next vehicle. Our ultimate goal is to empower you with expert insights, ensuring a smooth and confident journey toward vehicle ownership.

From Bank of the West to BMO Harris: Navigating Your Auto Loan Journey with Confidence

The Evolution of Bank of the West Car Loans: A BMO Harris Perspective

The name "Bank of the West" still resonates with many, but the institution itself has undergone a significant transformation. In February 2023, BMO Harris Bank completed its acquisition of Bank of the West. This monumental merger means that all banking services, including auto loans, previously offered by Bank of the West are now provided under the BMO Harris umbrella.

For former Bank of the West customers, this transition aimed to be as seamless as possible. Accounts were transitioned, and new services became available through BMO Harris. What this fundamentally means for you, the car buyer, is that if you were looking for a "Bank of the West car loan," you are now effectively looking for a BMO Harris auto loan.

Based on my understanding of the financial landscape and major bank mergers, such acquisitions often bring both continuity and new opportunities. BMO Harris, as a larger national bank, brings its own robust set of financial products and services, including a comprehensive auto financing division. This integration allows them to leverage a broader network and potentially offer competitive rates and terms to a wider audience.

Understanding BMO Harris Auto Loans: Your Path to Vehicle Ownership

BMO Harris Bank offers a diverse range of auto financing solutions designed to help individuals purchase new or used vehicles, or even refinance existing loans. Their commitment to customer service and competitive offerings makes them a strong contender in the auto loan market. Understanding their product suite is the first step toward finding the right fit for your needs.

Types of Auto Loans Offered by BMO Harris:

BMO Harris provides flexibility to cater to different purchasing scenarios. Whether you’re eyeing a brand-new model or a reliable pre-owned vehicle, they likely have a solution.

- New Car Loans: Designed for brand-new vehicles purchased from a dealership. These typically come with lower interest rates due to the vehicle’s higher value and slower depreciation in its initial stages.

- Used Car Loans: Ideal for pre-owned vehicles, whether from a dealership or a private seller. While rates might be slightly higher than new car loans, BMO Harris aims to keep them competitive.

- Auto Loan Refinancing: If you already have an existing car loan, refinancing with BMO Harris could potentially lower your interest rate, reduce your monthly payments, or shorten your loan term. This is a smart move if your credit score has improved or if market rates have dropped since you initially financed your vehicle.

Key Features and Benefits:

When considering BMO Harris for your auto loan, several features stand out. These benefits are designed to provide convenience, transparency, and value to the borrower.

- Competitive Interest Rates: BMO Harris strives to offer rates that are attractive, especially for borrowers with strong credit histories.

- Flexible Loan Terms: They provide a range of repayment periods, allowing you to choose a term that aligns with your budget and financial goals. Common terms range from 36 to 72 months, and sometimes even longer.

- Pre-Approval Options: This crucial feature allows you to know how much you can borrow before you even step onto a dealership lot. It gives you significant leverage in price negotiations.

- Online Application: The convenience of applying for an auto loan from the comfort of your home or office is a major advantage. Their online portal typically streamlines the process.

Pro Tip from Us: Always pursue pre-approval before you start serious car shopping. Having a pre-approval in hand from BMO Harris or any lender turns you into a cash buyer in the eyes of the dealership. This empowers you to negotiate the car’s price separately from the financing, often leading to a better overall deal. It also sets a clear budget, preventing you from falling in love with a car outside your financial comfort zone.

Navigating the Application Process: A Step-by-Step Guide

Applying for an auto loan can seem daunting, but breaking it down into manageable steps makes the journey much clearer. BMO Harris, like most reputable lenders, has a structured process to assess your eligibility and provide you with financing options. Understanding each stage will help you prepare and move through the application with ease.

Step 1: Pre-Qualification vs. Pre-Approval – Know the Difference

Before you submit a full application, it’s important to understand two similar-sounding but distinct concepts.

- Pre-qualification: This is a preliminary check that gives you an idea of what you might qualify for. It typically involves a "soft credit pull," which doesn’t impact your credit score. It’s a good starting point for budgeting.

- Pre-approval: This is a more formal process where the lender thoroughly reviews your creditworthiness and provides you with a conditional offer for a specific loan amount and interest rate. This involves a "hard credit pull," which will temporarily affect your credit score. However, multiple hard pulls within a short shopping window (typically 14-45 days, depending on the credit model) for the same type of loan are often treated as a single inquiry, so don’t be afraid to shop around for the best rates after pre-approval.

Step 2: Gathering Your Required Documentation

To ensure a smooth application process, have all your necessary documents ready. Lenders need this information to verify your identity, income, and financial stability.

Here’s a list of common documents BMO Harris, or any lender, might request:

- Proof of Identity: Valid government-issued ID (driver’s license, state ID).

- Proof of Income: Recent pay stubs (usually 2-3 months), W-2 forms, tax returns (for self-employed individuals), or bank statements.

- Proof of Residence: Utility bill, lease agreement, or mortgage statement with your current address.

- Employment Information: Name and contact information of your employer.

- Financial Information: Bank account numbers, existing loan details, and any assets you wish to declare.

- Vehicle Information (if applicable): If you’ve already found a car, you’ll need details like the make, model, year, VIN, and purchase price.

Step 3: The Online Application Process

BMO Harris offers a convenient online application portal. This typically involves:

- Creating an Account or Logging In: If you’re an existing customer, you might log into your online banking portal. New customers will likely create an account.

- Filling Out the Application Form: This will ask for personal details, employment history, income, and information about the loan you’re seeking (e.g., new car, used car, refinance).

- Uploading Documents: You’ll be prompted to upload digital copies of your supporting documents.

- Review and Submit: Carefully review all information for accuracy before submitting.

Common Mistakes to Avoid:

Based on my experience helping individuals secure financing, several pitfalls can hinder your auto loan application.

- Applying to Too Many Lenders Simultaneously: While it’s good to shop around, excessive hard inquiries within a short period can slightly depress your credit score. Focus on a few strong contenders after initial research.

- Not Checking Your Credit Score Before Applying: Knowing your credit standing allows you to anticipate rates and address any inaccuracies. A surprise low score can lead to disappointment or rejection.

- Incomplete or Inaccurate Information: Any discrepancies in your application can cause delays or even rejection. Double-check all details before submission.

- Not Understanding Your Budget: Don’t just focus on the monthly payment. Consider the total cost of the loan, including interest, and how it fits into your overall financial picture.

For a deeper dive into improving your credit score and preparing for any loan application, check out our article on "Mastering Your Credit Score: A Guide to Financial Freedom." (Internal Link 1 Placeholder)

Key Factors Influencing Your Car Loan Approval and Rates

Securing a favorable auto loan isn’t just about finding the right lender; it’s also about understanding the factors that influence their decision. Lenders like BMO Harris assess several key elements to determine your eligibility, the interest rate you’ll receive, and the overall loan terms. Being aware of these can help you position yourself for the best possible outcome.

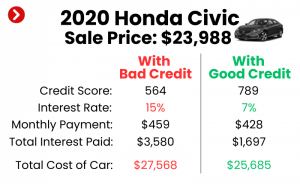

1. Your Credit Score: The Cornerstone of Your Loan

Your credit score is arguably the most critical factor in auto loan approval and interest rates. It’s a numerical representation of your creditworthiness, reflecting your history of borrowing and repaying debt.

- FICO vs. VantageScore: While both are widely used, FICO is the most common model lenders use. Scores typically range from 300 to 850.

- Credit Tiers: Lenders categorize scores into tiers:

- Excellent (780-850): Best rates, easiest approval.

- Very Good (740-779): Excellent rates, strong approval chances.

- Good (670-739): Good rates, standard approval.

- Fair (580-669): Higher rates, more scrutiny.

- Poor (300-579): Very high rates, difficult approval, often requires a co-signer.

From my experience working with countless borrowers, a higher credit score signals lower risk to the lender, translating directly into lower interest rates and more attractive loan terms. Always check your credit report for errors before applying.

2. Income and Debt-to-Income (DTI) Ratio: Can You Afford It?

Lenders need assurance that you can comfortably make your monthly loan payments. This is where your income and DTI ratio come into play.

- Income: A steady, verifiable income is essential. Lenders want to see that you have the financial capacity to meet your obligations.

- Debt-to-Income Ratio (DTI): This is the percentage of your gross monthly income that goes towards debt payments. For example, if your gross monthly income is $5,000 and your total monthly debt payments (including the proposed car loan, mortgage/rent, credit cards, student loans) are $2,000, your DTI is 40% ($2,000 / $5,000). Most lenders prefer a DTI ratio of 43% or lower, though some might be more flexible. A lower DTI indicates less financial strain and a greater ability to handle new debt.

3. Down Payment: Reducing Risk, Saving Money

A down payment is the initial amount of money you pay upfront for the vehicle. It significantly impacts your auto loan in several ways.

- Reduces Loan Amount: A larger down payment means you’re borrowing less, which reduces your monthly payments and the total interest paid over the life of the loan.

- Lower Risk for Lender: It shows your commitment to the purchase and reduces the lender’s exposure, especially since cars depreciate quickly. This can lead to better interest rates.

- Prevents Negative Equity: Putting money down helps prevent you from owing more than the car is worth (negative equity), especially in the early years of ownership.

Pro Tip: Aim for at least 10-20% down payment on a new car and 10% on a used car if your budget allows. This not only makes your loan more affordable but also gives you a buffer against depreciation.

4. Loan Term: Balancing Monthly Payments and Total Cost

The loan term is the length of time you have to repay the loan, typically expressed in months (e.g., 36, 48, 60, 72, or 84 months).

- Shorter Terms (e.g., 36-48 months):

- Pros: Lower total interest paid, quicker payoff, often lower interest rates.

- Cons: Higher monthly payments.

- Longer Terms (e.g., 60-84 months):

- Pros: Lower monthly payments, making the car more "affordable" on a monthly basis.

- Cons: Significantly more total interest paid over the life of the loan, higher risk of negative equity, often slightly higher interest rates.

Common mistakes to avoid are extending the loan term too much just to achieve a low monthly payment without considering the substantial increase in total interest paid. Carefully weigh your budget against the long-term cost.

5. Vehicle Type and Age: The Asset’s Value

The car itself plays a role in the loan decision, particularly its value and expected depreciation.

- New Cars: Generally easier to finance and often qualify for lower rates because they hold their value better initially and have fewer mechanical risks.

- Used Cars: Financing used cars can be slightly trickier. Lenders are wary of older vehicles with high mileage due to higher depreciation and potential mechanical issues. They might impose age or mileage limits, or offer higher rates. The vehicle’s resale value also impacts the maximum loan amount.

Beyond the Approval: Managing Your Auto Loan Effectively

Congratulations, you’ve secured your auto loan! But the journey doesn’t end there. Effective loan management is crucial to maintain your financial health, protect your credit score, and ultimately, save money. Here’s how to handle your BMO Harris auto loan responsibly and strategically.

Making Timely Payments: The Golden Rule

This is perhaps the most critical aspect of managing any loan. Missing payments, or making them late, can have severe consequences:

- Credit Score Damage: Late payments are reported to credit bureaus and can significantly drop your score, making future borrowing more expensive or difficult.

- Late Fees: Lenders typically charge fees for overdue payments.

- Repossession Risk: Consistent non-payment can lead to your vehicle being repossessed.

Pro Tip: Set up automatic payments directly from your bank account. This eliminates the risk of forgetting a payment and ensures consistency. BMO Harris, like most modern banks, offers convenient online payment options.

Understanding Your Loan Statement

Don’t just glance at the total due; take time to understand your monthly statement. It provides a detailed breakdown of your payment:

- Principal: The portion of your payment that goes towards reducing the actual loan amount.

- Interest: The cost of borrowing money.

- Escrow/Fees (if any): While less common for auto loans, some statements might show other charges.

- Remaining Balance: How much you still owe on the car.

Understanding these components helps you see how quickly you’re paying down the principal and the total interest accumulated.

Refinancing Options: When and Why to Consider It

Refinancing your auto loan means taking out a new loan to pay off your existing one. This can be a smart move in certain situations:

- Lower Interest Rates: If market rates have dropped or your credit score has significantly improved since you got your original loan, refinancing could secure you a lower interest rate, saving you hundreds or even thousands over the loan term.

- Lower Monthly Payments: By extending the loan term (though be wary of total interest paid), or securing a lower rate, you can reduce your monthly outflow.

- Change Loan Terms: You might want to switch from a shorter, high-payment term to a longer, more manageable one, or vice-versa if your financial situation has improved.

Before refinancing, compare the new loan’s interest rate, terms, and any associated fees with your current loan. Ensure the benefits outweigh the costs.

Early Payoff Considerations

Paying off your auto loan early can be a fantastic financial move, saving you a significant amount in interest.

- Check for Prepayment Penalties: Most auto loans do not have prepayment penalties, but it’s always wise to check your loan agreement. BMO Harris generally does not impose these, but verify your specific contract.

- Accelerated Payments: Even making one extra principal payment a year or rounding up your monthly payment can shave months off your loan term and save you interest.

- Financial Priorities: Before aggressively paying down your car loan, ensure you have an emergency fund, are contributing to retirement, and have paid off any higher-interest debt (like credit cards).

For further guidance on managing your debt and improving your financial literacy, we recommend exploring resources from the Consumer Financial Protection Bureau (CFPB) at consumerfinance.gov. (External Link Placeholder)

Common Questions About Auto Loans (FAQs)

Navigating auto financing often brings up a host of questions. Here are some of the most frequently asked, along with expert insights to help clarify your concerns.

1. What if I have bad credit? Can I still get an auto loan?

Yes, it is possible to get an auto loan with bad credit, but it will likely come with higher interest rates and potentially less favorable terms. Lenders consider borrowers with lower credit scores to be higher risk. You might need to:

- Provide a larger down payment.

- Find a co-signer with good credit.

- Be prepared for a higher Annual Percentage Rate (APR).

- Focus on affordable, reliable used cars rather than new ones.

BMO Harris, like other traditional banks, typically prefers borrowers with good to excellent credit. If your score is low, consider credit unions or specialized bad-credit lenders, but always compare terms carefully.

2. Can I get a car loan without a down payment?

While it’s generally not recommended, 100% financing (no down payment) is possible, especially for borrowers with excellent credit scores and stable incomes. However, it comes with risks:

- Higher Monthly Payments: You’re financing the entire cost of the car.

- More Total Interest: A larger principal loan means more interest paid over time.

- Immediate Negative Equity: You’ll owe more than the car is worth as soon as you drive it off the lot, making it difficult if you need to sell or if the car is totaled.

Always try to make a down payment if you can, even a small one, to mitigate these risks.

3. How long does auto loan approval take with BMO Harris?

The approval timeline can vary. For online applications, BMO Harris often provides an initial decision within minutes or a few hours for pre-qualification. For full pre-approval or a formal loan application, it might take anywhere from a few hours to a couple of business days, especially if additional documentation or review is required. Having all your documents ready and submitting a complete application can significantly speed up the process.

4. What about co-signers? How do they help?

A co-signer is someone who agrees to be equally responsible for the loan if the primary borrower defaults. Co-signers are typically used when the primary borrower has a limited or poor credit history.

- Benefits: A co-signer with good credit can help you get approved for a loan you otherwise wouldn’t qualify for, or secure a lower interest rate.

- Risks for Co-signer: If you miss payments, it negatively impacts their credit score. If you default, they are legally obligated to repay the loan. This is a significant responsibility and should only be undertaken with careful consideration and mutual trust.

Pro Tips for Securing the Best Auto Loan

Navigating the auto loan landscape requires more than just filling out an application. Strategic planning and informed decisions can lead to substantial savings and a smoother buying experience. Here are our expert tips to help you secure the most advantageous auto loan possible.

1. Shop Around for Rates (Within a Short Window)

Don’t settle for the first offer you receive, even if it’s from BMO Harris. Contact multiple lenders—banks, credit unions, and online lenders—to compare interest rates and terms. As mentioned earlier, credit bureaus understand that you’ll shop for the best rate for a car loan. They typically count multiple inquiries for the same type of loan within a 14-45 day window as a single inquiry, minimizing the impact on your credit score.

2. Negotiate the Car Price Separately from the Financing

This is a critical strategy. Always finalize the price of the vehicle before discussing financing options. When you combine these two negotiations, dealerships can often mask a less favorable loan rate by making it seem like you’re getting a great deal on the car, or vice-versa. Having a pre-approval from BMO Harris (or another lender) gives you the power to focus solely on the car’s price.

3. Read the Fine Print – Every Single Word

Before signing any loan agreement, meticulously read all the terms and conditions. Pay close attention to:

- APR (Annual Percentage Rate): This is the true cost of the loan, including interest and any fees.

- Loan Term: Ensure it aligns with your budget and long-term financial goals.

- Prepayment Penalties: Confirm there are none if you plan to pay off early.

- Late Payment Fees: Understand the penalties for missed payments.

- Any additional clauses or fees: Be aware of all costs involved.

If anything is unclear, ask for clarification. Don’t be rushed into signing.

4. Don’t Forget Insurance

Your lender will require you to carry full coverage (comprehensive and collision) insurance on your financed vehicle until the loan is paid off. Factor the cost of this insurance into your overall budget. Get insurance quotes before you buy the car, as premiums can vary significantly based on the vehicle type, your driving history, and your location.

Learn more about negotiating vehicle prices and other car-buying strategies in our comprehensive guide: "The Ultimate Car Buyer’s Playbook: Negotiation Tactics and Smart Decisions." (Internal Link 2 Placeholder)

Conclusion: Driving Forward with Confidence

Securing an auto loan, whether through the new BMO Harris platform or any other reputable lender, is a significant financial decision. The journey from considering a vehicle to driving it off the lot is filled with choices, and being well-informed is your most powerful tool. By understanding the transition from Bank of the West to BMO Harris, familiarizing yourself with the application process, and recognizing the factors that influence your loan terms, you’re already ahead of the curve.

Remember, a successful auto loan experience hinges on preparation, diligence, and asking the right questions. Utilize the pre-approval process, compare offers, and always read the fine print. With the insights provided in this guide, you are now equipped to navigate the auto financing landscape with confidence and make choices that align with your financial well-being.

Your dream car is within reach. Take the next step by exploring BMO Harris’s current auto loan offerings and embark on your journey toward vehicle ownership today!