Getting A Car Loan With A 600 Credit Score: Your Comprehensive Guide to Driving Away Confidently

Getting A Car Loan With A 600 Credit Score: Your Comprehensive Guide to Driving Away Confidently Carloan.Guidemechanic.com

Securing a car loan can feel like a daunting task, especially when your credit score hovers around the 600 mark. Many believe that a less-than-perfect credit score slams the door shut on their dreams of car ownership. However, based on my extensive experience in the auto finance industry, I can confidently tell you this isn’t true. While a 600 credit score presents unique challenges, getting approved for an auto loan is absolutely within reach with the right strategy and knowledge.

This comprehensive guide is designed to empower you with the insights and actionable steps needed to navigate the world of car financing with a 600 credit score. We’ll explore everything from understanding your credit standing to finding the right lenders, preparing your application, and ultimately, driving away in your new (or new-to-you) vehicle. Our goal is to provide you with pillar content that not only educates but also equips you for success.

Getting A Car Loan With A 600 Credit Score: Your Comprehensive Guide to Driving Away Confidently

Understanding Your 600 Credit Score: The Subprime Reality

Before we dive into strategies, let’s first clarify what a 600 credit score signifies in the eyes of lenders. Credit scores typically range from 300 to 850. A score of 600 generally falls into the "fair" or "subprime" category. This means lenders perceive you as a moderate to high-risk borrower.

You might have a 600 credit score for various reasons. Perhaps you’ve had some late payments in the past, have a high credit utilization ratio, or a relatively short credit history. Whatever the cause, it signals to lenders that there’s a slightly higher chance of default compared to someone with excellent credit.

What Does "Subprime" Mean for Auto Loans?

When applying for an auto loan with a 600 credit score, you’re entering what’s known as the "subprime" lending market. This market caters specifically to individuals with lower credit scores. While it opens doors that might otherwise be closed, it also comes with certain realities.

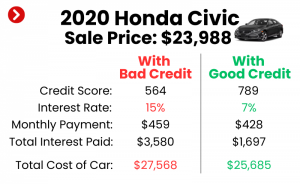

The most significant reality is often higher interest rates. Lenders mitigate the increased risk associated with subprime borrowers by charging more for the loan. This means your monthly payments and the total cost of the car will likely be higher than what someone with a prime credit score would pay. Don’t let this discourage you; understanding this upfront helps you manage expectations and prepare effectively.

Strategies to Boost Your Chances (Before You Apply)

Getting a car loan with a 600 credit score is entirely possible, but taking proactive steps before you even start applying can dramatically improve your terms and increase your approval odds. These strategies are all about reducing perceived risk for lenders.

1. Improve Your Credit Score (Even Slightly)

Even a small bump in your credit score can make a significant difference in the interest rate you’re offered. Every point counts when you’re in the fair credit range. Based on my experience, dedication to these simple steps can yield results faster than you might think.

- Pay All Bills On Time: This is the single most important factor influencing your credit score. Start by ensuring all your current bills – credit cards, utilities, rent, student loans – are paid promptly and in full. Even one missed payment can set you back.

- Reduce Existing Debt: High credit card balances, in particular, can drag down your score. Lenders look at your credit utilization ratio (how much credit you’re using versus how much you have available). Aim to keep this ratio below 30%, ideally even lower. Paying down credit card debt not only helps your score but also frees up more of your income for car payments.

- Check Your Credit Report for Errors: Pro tip from us: Approximately 1 in 5 credit reports contain errors that could be negatively impacting your score. Obtain a free copy of your credit report from each of the three major bureaus (Experian, Equifax, TransUnion) via AnnualCreditReport.com. Dispute any inaccuracies immediately. Correcting an error could give your score an instant boost. For more detailed steps on improving your credit, consider reading our article on Quick Ways to Boost Your Credit Score (placeholder for internal link).

2. Save for a Substantial Down Payment

This is arguably the most impactful strategy for a borrower with a 600 credit score. A significant down payment signals to lenders that you are serious, financially responsible, and have "skin in the game." It directly reduces the amount you need to borrow, which in turn lowers the lender’s risk.

A larger down payment also has several other benefits. It can lead to lower monthly payments, reduce the total interest paid over the life of the loan, and help you avoid being "upside down" on your loan (owing more than the car is worth). Common advice suggests 10-20% for prime borrowers, but with a 600 credit score, aiming for 20% or even 25% can dramatically improve your approval chances and secure better terms.

3. Consider a Co-signer

If you have a trusted friend or family member with excellent credit, asking them to co-sign your loan can be a game-changer. A co-signer essentially adds their good credit history and financial strength to your application. This reassures the lender that if you default, they have another reliable party to collect from.

- Who Makes a Good Co-signer? Look for someone with a high credit score, stable income, and low debt-to-income ratio.

- Benefits and Risks: A co-signer can help you get approved and secure a lower interest rate. However, it’s a significant responsibility for them. If you miss payments, their credit score will also be negatively affected, and they will be legally responsible for the debt. Pro tip: Ensure you have a frank discussion with your potential co-signer about their responsibilities and your commitment to making payments on time. This is a business agreement that impacts a personal relationship.

4. Opt for a Less Expensive Vehicle

While it might be tempting to eye that brand-new, fully-loaded SUV, financial prudence dictates otherwise when you have a 600 credit score. Choosing a more affordable, reliable used car significantly reduces the amount you need to borrow. A lower loan amount means less risk for the lender and more manageable monthly payments for you.

Focus on your needs rather than your wants. A reliable, fuel-efficient vehicle that gets you from point A to point B is a far better choice when you’re rebuilding your credit. As your credit score improves with responsible payments, you can always consider upgrading in the future.

Where to Look for a Car Loan with a 600 Credit Score (Lender Types)

Not all lenders are created equal, especially when it comes to borrowers with less-than-perfect credit. Knowing where to focus your search can save you time and frustration.

1. Subprime Lenders and Special Finance Dealerships

These lenders and dealerships specialize in working with individuals who have credit scores similar to yours. They are more accustomed to the risks involved and have loan programs specifically designed for subprime borrowers.

- How They Operate: These lenders often look beyond just your credit score. They’ll consider your income stability, employment history, down payment amount, and debt-to-income ratio more closely.

- What to Expect: Expect higher interest rates compared to prime loans. They might also offer slightly longer loan terms to make monthly payments more affordable, but be cautious of extending terms too much as it increases total interest paid.

- Common Mistakes: A common mistake is going with the first offer without comparing. Even among subprime lenders, rates and terms can vary significantly. Shop around!

2. Credit Unions

Credit unions are member-owned financial institutions that often have more flexible lending criteria than traditional banks. They are known for their customer-centric approach and competitive rates, even for borrowers with fair credit.

- Membership Benefits: To get a loan from a credit union, you usually need to be a member. Membership requirements are often quite broad, such as living in a certain area, working for a specific employer, or belonging to an association.

- Flexible Terms: Because they are not-for-profit, credit unions can sometimes offer lower interest rates and more personalized loan terms than larger banks, making them an excellent option for those with a 600 credit score.

3. Online Lenders

The digital landscape has brought forth a plethora of online lenders who specialize in various credit profiles, including subprime. They offer convenience, quick pre-approvals, and often a streamlined application process.

- Convenience and Speed: You can apply from the comfort of your home, and many online platforms provide instant pre-approval decisions.

- Variety of Options: Online lenders often have partnerships with multiple financial institutions, allowing you to compare several offers with a single application. Pro tip: Always read reviews and verify the legitimacy of online lenders before sharing your personal information. Look for lenders with transparent terms and good customer service ratings.

4. "Buy Here, Pay Here" Dealerships

These dealerships offer in-house financing, meaning they are both the seller of the car and the lender. They often cater specifically to individuals with poor credit or no credit history.

- Pros and Cons: The main advantage is that approval is almost guaranteed, as they prioritize your income stability over your credit score. However, this convenience often comes at a steep price. Interest rates are typically much higher, and the vehicle selection might be limited to older, higher-mileage cars.

- Common Mistakes: A significant pitfall is not understanding the full terms. Many "Buy Here, Pay Here" dealerships do not report payments to credit bureaus, which means even if you make all your payments on time, it might not help improve your credit score. This should be considered a last resort if other options are exhausted.

The Application Process and What to Expect

Once you’ve done your homework and chosen potential lenders, it’s time to apply. Being prepared and understanding the process will make it much smoother.

1. Gather Your Documents

Lenders will need to verify your identity, income, and residency. Having all your documents ready before you apply can expedite the process.

- Proof of Identity: Driver’s license or state ID.

- Proof of Income: Recent pay stubs (usually 2-3 months), W-2s, tax returns (especially if self-employed).

- Proof of Residency: Utility bill, lease agreement, or mortgage statement.

- Proof of Insurance: You’ll need full coverage insurance before driving off the lot.

- Trade-in Information (if applicable): Title, registration, and any loan payoff information.

2. Get Pre-Approved

Getting pre-approved for a loan is a powerful strategy. It means a lender has reviewed your financial information and determined how much they are willing to lend you and at what interest rate, before you even step foot on a dealership lot.

- Benefits of Pre-Approval: It gives you solid shopping power. You know your budget upfront, allowing you to negotiate the car price as a cash buyer, rather than being swayed by monthly payment figures. It also helps you compare rates from different lenders.

- Soft vs. Hard Inquiries: Most pre-approvals involve a "soft inquiry" on your credit, which doesn’t affect your score. Once you formally apply, it becomes a "hard inquiry." Pro tip: Apply to multiple lenders within a short window (typically 14-45 days, depending on the credit scoring model). These multiple hard inquiries will often be treated as a single inquiry, minimizing the impact on your credit score.

3. Understand the Loan Terms

When reviewing loan offers, don’t just focus on the monthly payment. It’s crucial to understand the entire financial picture. Based on my experience, many borrowers overlook critical details here.

- Interest Rate (APR): This is the cost of borrowing money, expressed as an annual percentage rate. Even a small difference in APR can save you hundreds or thousands over the life of the loan. For more on this, check out our guide on Demystifying Car Loan Interest Rates (placeholder for internal link).

- Loan Term (Duration): This is how long you have to pay back the loan (e.g., 36, 48, 60, 72 months). Longer terms mean lower monthly payments but significantly more interest paid over time. Common mistakes to avoid are extending the loan term too much just to lower the monthly payment, as it dramatically increases the total cost of the car.

- Fees: Be aware of any origination fees, documentation fees, or other charges that might be added to the loan amount.

- Total Cost of the Loan: Always calculate the total amount you’ll pay back (principal + interest + fees). This figure often provides a clearer picture of the true cost of borrowing.

4. Negotiating Your Car Purchase

Once you have your pre-approval in hand, you are in a stronger position to negotiate. Separate the negotiation for the car price from the discussion about financing.

- Focus on the Car Price First: Treat your pre-approval like cash. Negotiate the best possible price for the vehicle before discussing how you’ll pay.

- Avoid Unnecessary Add-ons: Dealerships often try to sell you extended warranties, paint protection, or other accessories. While some might be useful, many are overpriced and can significantly inflate your loan amount. Carefully consider what you truly need.

Post-Loan Management & Credit Improvement

Getting approved for a car loan with a 600 credit score is a victory, but the journey doesn’t end there. This is a prime opportunity to rebuild and improve your credit for future financial endeavors.

1. Make Payments On Time, Every Time

This is non-negotiable. Consistent, on-time payments are the most effective way to improve your credit score. Each payment reported to the credit bureaus as "on-time" builds a positive payment history, which is the biggest factor in your FICO score.

Pro tip: Set up automatic payments from your bank account to avoid missing deadlines. Even better, consider making bi-weekly payments. This can slightly reduce the total interest paid and helps you pay off the loan a bit faster.

2. Avoid Refinancing Too Soon (Unless Rates Drop Significantly)

After making 6-12 months of on-time payments, your credit score is likely to improve. At this point, you might be tempted to refinance for a lower interest rate.

- When It Makes Sense: Refinancing is a smart move if your credit score has significantly improved, and you can secure a substantially lower interest rate. This will reduce your monthly payment and/or the total interest paid over the life of the loan.

- Be Patient: Don’t jump at the first opportunity. Give your credit score time to reflect your positive payment history. Your goal should be to move from the subprime category into the prime lending tier.

Common Pitfalls and How to Avoid Them

Even with all the right strategies, it’s easy to fall into common traps when securing a car loan with fair credit. Awareness is your best defense.

- Falling for Predatory Loans: Be wary of lenders promising guaranteed approval with no credit check, especially if their interest rates seem excessively high. Always read the fine print.

- Not Understanding the Fine Print: Never sign a loan agreement you don’t fully comprehend. Ask questions until every clause, fee, and term is clear.

- Buying More Car Than You Can Afford: This is a slippery slope. Even if you get approved for a larger amount, stick to a budget that comfortably allows for your monthly payment, insurance, maintenance, and fuel without straining your finances. Common mistakes often stem from focusing solely on the monthly payment without considering the overall budget.

- Ignoring the Total Cost of the Loan: As discussed, a lower monthly payment achieved by extending the loan term can lead to paying much more in interest over time. Always compare the total cost.

Conclusion: Drive Towards a Brighter Financial Future

Getting a car loan with a 600 credit score is a journey that requires diligence, patience, and smart decision-making. It might mean higher interest rates initially, but it’s also a powerful opportunity to demonstrate financial responsibility and rebuild your credit. By understanding your credit situation, preparing strategically, exploring the right lender options, and managing your loan responsibly, you can not only secure the transportation you need but also pave the way for a stronger financial future.

Remember, every on-time payment you make is an investment in your credit score. Embrace this opportunity, stay informed, and drive away confidently, knowing you’ve taken control of your financial path. We encourage you to share your experiences and insights in the comments below – your journey could inspire others!

External Link Reference: For accurate and personalized credit score information, we recommend checking your FICO score directly through services provided by myFICO.com or your credit card issuer.