Getting a Personal Loan for a Car: Your Ultimate Guide to Approval & Best Rates

Getting a Personal Loan for a Car: Your Ultimate Guide to Approval & Best Rates Carloan.Guidemechanic.com

Buying a car is a significant milestone, often accompanied by the excitement of new adventures and the freedom of the open road. However, for many, the path to vehicle ownership isn’t always straightforward. Traditional auto loans, while common, aren’t the only financing option available. In certain situations, a personal loan can emerge as a surprisingly flexible and powerful tool for getting a personal loan for a car.

This comprehensive guide is designed to demystify the process, offering you a deep dive into how personal loans work for car purchases. We’ll explore everything from eligibility criteria and the application journey to crucial strategies for securing the best rates and increasing your chances of approval. Our goal is to equip you with the knowledge to make an informed financial decision, ensuring your car buying experience is as smooth as possible.

Getting a Personal Loan for a Car: Your Ultimate Guide to Approval & Best Rates

Why Consider a Personal Loan for Your Car?

When thinking about car financing, most people immediately picture a traditional auto loan. While these are indeed popular, there are distinct scenarios where a personal loan for a car can be a more advantageous or even necessary option. Understanding these situations is key to making the right choice for your financial circumstances.

Based on my experience as a financial expert, personal loans offer a level of flexibility that secured auto loans often lack. This flexibility can be particularly appealing if you’re looking to purchase a vehicle from a private seller, which is a common scenario where traditional auto loans can be cumbersome or even unavailable. Private sales typically don’t involve a dealership’s financing department, making a personal loan an ideal solution.

Another compelling reason to consider a personal loan is when you’re eyeing an older, classic, or unique vehicle. Many traditional auto lenders have strict age or mileage limits for the cars they’ll finance, or they might offer less favorable terms for such vehicles. A personal loan, being unsecured in most cases, isn’t tied to the car’s value or age, giving you the freedom to buy the car of your dreams, regardless of its vintage. This flexibility extends to the type of vehicle you purchase, as the loan isn’t secured by the car itself.

Furthermore, if your credit history isn’t perfect, but you have a strong income and a good relationship with your bank, a personal loan might sometimes be more accessible than a secured auto loan. While both require good credit, some lenders might offer personal loans with slightly more lenient criteria or be willing to consider your overall financial picture more broadly. The funds from a personal loan are disbursed directly to you, providing you with cash to purchase the vehicle outright, which can sometimes give you more bargaining power with the seller.

Personal Loan vs. Traditional Auto Loan: What’s the Difference?

Before diving deeper into the specifics of getting a personal loan for a car, it’s crucial to understand how it stacks up against its more conventional counterpart: the traditional auto loan. While both serve the purpose of helping you finance a vehicle, their fundamental structures and implications for you, the borrower, are quite different. Knowing these distinctions is vital for making an informed decision.

Traditional Auto Loan: The Secured Approach

A traditional auto loan is a secured loan, meaning the vehicle you’re purchasing serves as collateral. If you fail to make your payments, the lender has the legal right to repossess the car to recover their losses. This collateral aspect is why auto loans often come with lower interest rates compared to personal loans, as the lender faces less risk.

The funds from an auto loan are typically disbursed directly to the car dealership or seller, specifically for the purchase of the vehicle. This means the loan is explicitly tied to the car itself. Lenders often have specific requirements regarding the vehicle’s age, mileage, and condition, as these factors affect its value as collateral.

Personal Loan: The Unsecured Alternative

In contrast, most personal loans are unsecured loans. This means there is no collateral tied to the loan. If you default, the lender cannot directly seize an asset like your car. This higher risk for the lender typically translates to higher interest rates compared to secured auto loans, especially if your credit score isn’t stellar.

With a personal loan, the funds are disbursed directly to you, the borrower. Once you receive the money, you can use it for virtually any purpose, including purchasing a car. This provides immense flexibility; you become a cash buyer, which can be advantageous in negotiations, particularly with private sellers. There are no restrictions on the car’s age, make, or model from the lender’s perspective, as the loan isn’t tied to the vehicle itself.

Key Differences at a Glance

| Feature | Traditional Auto Loan | Personal Loan (for a car) |

|---|---|---|

| Collateral | Yes (the car itself) | No (typically unsecured) |

| Interest Rates | Often lower (due to collateral) | Can be higher (due to higher lender risk) |

| Fund Disbursement | To dealership/seller | To borrower |

| Usage | Specifically for car purchase | Flexible; can be used for car or other needs |

| Car Restrictions | Often has age/mileage limits | No restrictions on car type/age |

| Loan Terms | Typically 3-7 years | Varies, often 1-7 years |

Pro tips from us: While auto loans often boast lower interest rates, a personal loan can offer greater flexibility, especially if you have an excellent credit score that qualifies you for competitive personal loan rates. It’s crucial to compare the Annual Percentage Rate (APR) for both types of loans to see which is truly more cost-effective for your specific situation. Don’t just look at the advertised rate; delve into all fees and charges.

Eligibility & Key Factors Lenders Look For

Securing a personal loan for a car, like any significant financial product, hinges on meeting specific eligibility criteria. Lenders meticulously assess various aspects of your financial profile to determine your creditworthiness and ability to repay the loan. Understanding these key factors is the first step toward successful loan approval.

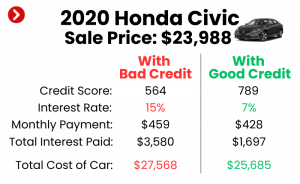

Your Credit Score: The Cornerstone of Lending

Your credit score is arguably the most critical factor lenders consider. It’s a numerical representation of your credit risk, reflecting your history of borrowing and repayment. A higher credit score signals to lenders that you are a responsible borrower, making you a more attractive candidate for a loan.

Generally, a credit score of 670 and above is considered "good," increasing your chances of approval and qualifying you for more favorable interest rates. Scores below this might still get approved, but often with higher interest rates to compensate the lender for the increased risk. Common mistakes to avoid are not checking your credit score before applying. This can lead to surprises and prevent you from addressing potential issues beforehand.

Income and Employment Stability

Lenders want assurance that you have a consistent and sufficient income stream to comfortably make your monthly loan payments. They will typically ask for proof of income, such as pay stubs, W-2s, or tax returns. Stable employment history, usually two years or more with the same employer, also demonstrates reliability.

Freelancers or self-employed individuals might need to provide more extensive documentation, such as several years of tax returns and bank statements, to prove income consistency. The steadier your income, the more confident lenders will be in your ability to repay.

Debt-to-Income Ratio (DTI): A Measure of Affordability

Your debt-to-income ratio (DTI) is another crucial metric. It’s calculated by dividing your total monthly debt payments by your gross monthly income. This ratio helps lenders understand how much of your income is already committed to existing debts.

A lower DTI indicates that you have more disposable income available to take on new debt, like a personal loan for a car. Most lenders prefer a DTI of 36% or lower, though some might go up to 43%. A high DTI can signal that you’re overextended financially, making lenders hesitant to approve additional credit.

Repayment History: A Glimpse into Your Past

Beyond your credit score, lenders will review your detailed credit report to examine your repayment history. They look for patterns of on-time payments across all your credit accounts, including credit cards, mortgages, and other loans. A history of missed or late payments, defaults, or bankruptcies will significantly reduce your chances of approval.

Demonstrating a consistent history of financial responsibility is paramount. It assures lenders that you are reliable and committed to fulfilling your financial obligations. Even a few minor late payments can negatively impact their assessment of your trustworthiness.

The Step-by-Step Process to Getting Your Personal Car Loan Approved

Navigating the world of loans can feel daunting, but breaking it down into manageable steps makes the process much clearer. Based on my experience guiding numerous individuals through this journey, a structured approach is key to successfully getting a personal loan for a car.

Step 1: Assess Your Financial Health

Before even looking at cars or lenders, take an honest look at your own finances. Start by creating a detailed budget to understand your monthly income and expenses. This will help you determine how much you can realistically afford for a monthly car payment without stretching your finances too thin.

Next, check your credit score and review your credit report for any inaccuracies or areas for improvement. You can obtain a free credit report from AnnualCreditReport.com. Calculate your current debt-to-income (DTI) ratio to get a sense of where you stand. This self-assessment is crucial; it helps you set realistic expectations and address potential issues proactively.

Step 2: Determine Your Loan Needs

Once you have a clear picture of your financial standing, decide how much you need to borrow. Consider the price of the car you intend to buy, any down payment you plan to make, and potential additional costs like taxes, registration, and insurance. Remember, a personal loan allows you to borrow a specific amount, so you need to be precise.

Also, think about your desired loan term. Shorter terms typically mean higher monthly payments but less interest paid over the life of the loan. Longer terms offer lower monthly payments but accumulate more interest. Choose a term that aligns with your budget and financial goals.

Step 3: Research & Compare Lenders

This is a critical step that many people rush, but it can save you a significant amount of money. Don’t just go with your primary bank. Research various types of lenders, including traditional banks, credit unions, and online lenders. Each type of institution has its own strengths and offerings.

- Banks: Often have established reputations and a wide range of products.

- Credit Unions: Member-owned, often offer competitive rates and personalized service.

- Online Lenders: Known for quick application processes and potentially lower rates due to lower overheads.

Compare interest rates (APR), fees (origination fees, late payment fees), repayment terms, and customer service reviews. Pro tips from us: Look beyond just the interest rate; the APR gives you a more accurate picture of the total cost of borrowing, including fees.

Step 4: Get Pre-Approval

Many lenders offer a pre-approval process, which typically involves a soft credit inquiry that doesn’t harm your credit score. Pre-approval gives you an estimate of the loan amount you qualify for and the interest rate you can expect. This step is incredibly beneficial.

With a pre-approval in hand, you know exactly how much car you can afford before you start shopping. This makes you a stronger, more confident buyer, whether you’re dealing with a private seller or a dealership. It also helps you avoid falling in love with a car that’s out of your budget.

Step 5: Gather Required Documents

Once you’ve narrowed down your lender choice and are ready to apply, compile all necessary documentation. This usually includes:

- Proof of Identity: Government-issued ID (driver’s license, passport).

- Proof of Address: Utility bill, lease agreement.

- Proof of Income: Pay stubs (last 2-3 months), W-2 forms (last 2 years), tax returns (last 2 years for self-employed).

- Bank Statements: (Last 3-6 months) to verify income and spending habits.

Having these documents ready will significantly expedite the application process.

Step 6: Submit Your Application

With all your documents prepared, complete the loan application carefully and accurately. Double-check all information before submission. A full application usually involves a hard credit inquiry, which will temporarily ding your credit score by a few points. However, if you apply to multiple lenders for the same type of loan within a short window (typically 14-45 days, depending on the scoring model), it will often be treated as a single inquiry.

Step 7: Review & Accept Loan Offer

If your application is approved, the lender will provide you with a loan offer detailing the principal amount, interest rate, monthly payment, and repayment schedule. Read every line of the loan agreement meticulously. Understand all terms and conditions, including any penalties for late payments or early repayment.

Do not hesitate to ask questions if anything is unclear. Once you are completely satisfied and understand your obligations, sign the agreement. The funds will then be disbursed to your bank account, usually within a few business days. For more insights on financial planning, you might find our article on Budgeting for Your First Car Purchase helpful.

Maximizing Your Chances of Approval & Getting Better Rates

Successfully getting a personal loan for a car isn’t just about meeting the minimum requirements; it’s about optimizing your financial profile to stand out to lenders. There are several proactive steps you can take to significantly boost your approval odds and secure more favorable interest rates. These strategies are rooted in demonstrating financial responsibility and reducing perceived risk for lenders.

Improve Your Credit Score

Your credit score is a powerful determinant of loan eligibility and interest rates. Prioritize improving it well before you apply for a loan. This involves several key actions: consistently paying all your bills on time, reducing your outstanding credit card balances, and avoiding opening new credit accounts unnecessarily.

Each on-time payment builds positive credit history, while keeping credit utilization low (ideally below 30%) shows you’re not over-reliant on credit. Even a 50-point increase in your score can unlock significantly better interest rates, saving you hundreds or even thousands of dollars over the life of the loan.

Lower Your Debt-to-Income Ratio (DTI)

As we discussed, a lower DTI signals to lenders that you have more disposable income to manage new debt. Before applying for a personal loan, focus on paying down existing debts, especially those with high interest rates, like credit card balances.

Even a small reduction in your monthly debt obligations can make a noticeable difference to your DTI. This demonstrates to lenders that you are not overextended and are capable of taking on additional financial commitments.

Consider a Co-signer

If your credit score is on the lower side or your income isn’t exceptionally high, applying with a co-signer can dramatically increase your chances of approval. A co-signer, typically a trusted friend or family member with excellent credit and stable income, agrees to be equally responsible for the loan repayment if you default.

This significantly reduces the risk for the lender, potentially leading to approval and better interest rates. However, be aware that this also places a significant responsibility on your co-signer, as their credit will be affected if you miss payments.

Make a Down Payment

While a personal loan gives you the cash to buy a car outright, making a down payment, even a small one, can still be beneficial. If you borrow less money, your monthly payments will be lower, making the loan more affordable and less risky in the eyes of the lender.

Although the personal loan isn’t secured by the car, showing that you have upfront cash to put towards the purchase demonstrates financial prudence. This can indirectly improve your loan application’s attractiveness to lenders, as it suggests stronger financial management.

Shop Around and Compare Offers

Common mistakes to avoid are accepting the first loan offer you receive. Different lenders have different criteria and risk assessments, leading to varying interest rates and terms. As mentioned earlier, use the pre-approval process with several lenders to compare offers without impacting your credit score significantly.

By actively shopping around, you empower yourself to choose the loan that best fits your financial situation, ensuring you get the most competitive rates and favorable terms available. This diligence can result in substantial savings over the loan’s duration.

Post-Approval: What to Do Next

Congratulations! You’ve successfully navigated the application process and secured your personal loan for a car. This is a significant step, but the journey doesn’t end here. There are a few crucial actions to take post-approval to ensure a smooth transition into car ownership and responsible loan management.

Once the funds are disbursed into your bank account, you are effectively a cash buyer. This empowers you to negotiate confidently with private sellers or dealerships. Take your time to find the right vehicle that fits your needs and budget, knowing you have the funds readily available.

The most important step after receiving your car loan is to set up your repayment schedule immediately. Understand your monthly payment amount and due date. Consider setting up automatic payments from your bank account to avoid missing any deadlines. This ensures consistent, on-time payments, which is vital for maintaining a good credit score and avoiding late fees.

Remember that owning a car involves more than just the purchase price. You’ll need to factor in ongoing costs such as car insurance, fuel, maintenance, and potential repairs. It’s wise to revisit your budget and allocate funds for these essential expenses. For a deeper dive into managing your finances after a big purchase, our guide on Smart Budgeting for Car Ownership Costs can provide valuable insights.

Finally, keep a close eye on your loan statements and your credit report periodically. Ensure that your payments are being accurately reported and that there are no discrepancies. Responsible management of your personal loan will not only help you successfully purchase your car but also strengthen your overall financial health for future endeavors. You can learn more about managing personal loans responsibly from trusted financial literacy resources like the Consumer Financial Protection Bureau (CFPB) at consumerfinance.gov.

Conclusion

Getting a personal loan for a car offers a flexible and powerful financing solution that many overlook. While traditional auto loans remain popular, personal loans provide distinct advantages, especially for private sales, older vehicles, or when you simply desire the freedom of being a cash buyer. By understanding the nuances between personal and auto loans, and by meticulously preparing your financial profile, you significantly enhance your chances of approval and securing favorable terms.

Our comprehensive guide has walked you through the entire journey, from assessing your financial health and navigating the application process to implementing strategies for better rates. Remember, a strong credit score, stable income, and a low debt-to-income ratio are your best allies in this process. By doing your homework, comparing lenders, and managing your loan responsibly, you can successfully finance your car purchase and hit the road with confidence.

Armed with this knowledge, you are now well-equipped to make an informed decision and embark on your car ownership journey with financial peace of mind. Happy driving!