Home Equity Loan vs. Car Loan: Unlocking the Best Way to Finance Your Next Vehicle

Home Equity Loan vs. Car Loan: Unlocking the Best Way to Finance Your Next Vehicle Carloan.Guidemechanic.com

Financing a new car is a significant financial decision, often ranking just behind buying a home in terms of complexity and long-term commitment. For many, the traditional car loan is the go-to option. However, homeowners often find themselves with another intriguing possibility: leveraging their home equity.

The choice between a Home Equity Loan and a traditional Car Loan (also known as an Auto Loan) isn’t always straightforward. Each comes with its own set of advantages, disadvantages, and critical implications for your financial future. This comprehensive guide will meticulously break down both options, providing you with the in-depth insights you need to make an informed, confident decision. We’ll explore their mechanics, risks, benefits, and help you determine which path aligns best with your financial goals and personal circumstances.

Home Equity Loan vs. Car Loan: Unlocking the Best Way to Finance Your Next Vehicle

Understanding the Home Equity Loan: Leveraging Your Most Valuable Asset

A Home Equity Loan, often referred to as a "second mortgage," allows homeowners to borrow against the equity they’ve built up in their property. Equity is simply the difference between your home’s current market value and the outstanding balance on your mortgage. As you pay down your mortgage and your home potentially appreciates in value, your equity grows.

When you take out a Home Equity Loan, you receive a lump sum of cash. This cash can then be used for virtually any purpose, including buying a new car. The loan typically comes with a fixed interest rate, meaning your monthly payments will remain consistent throughout the repayment period, which can range from 5 to 30 years. Your home serves as collateral for this loan, which is a crucial point we’ll explore further.

The Allure of Lower Interest Rates

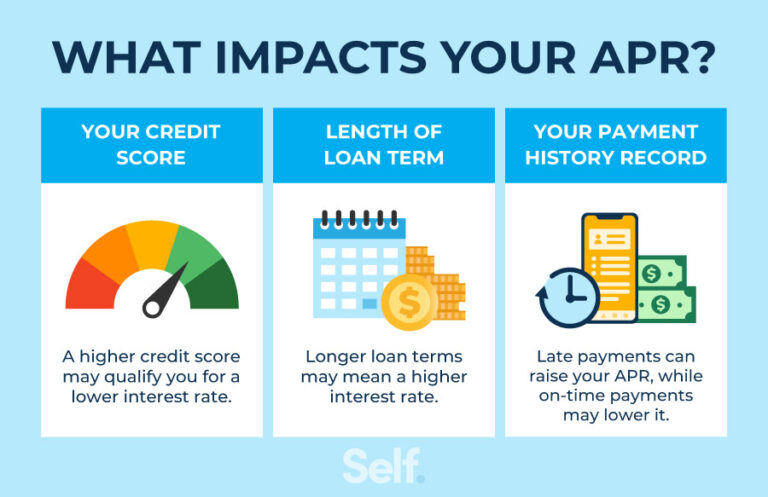

One of the most compelling reasons homeowners consider a Home Equity Loan for a car purchase is the potential for significantly lower interest rates compared to a traditional Car Loan. Why is this often the case? Because your home, a substantial and stable asset, secures the loan. Lenders view these loans as less risky, and that reduced risk translates into more favorable interest rates for the borrower.

Based on my experience, even a percentage point or two difference in interest can save you thousands of dollars over the life of a loan, especially when financing a larger sum like a car. This lower interest means more of your monthly payment goes towards the principal balance, accelerating your path to debt freedom.

Longer Repayment Terms and Predictable Payments

Home Equity Loans typically offer much longer repayment terms than Car Loans. While a car loan might be stretched to 60 or 72 months (5 or 6 years), a Home Equity Loan can extend to 15, 20, or even 30 years. This longer term results in lower monthly payments, which can free up cash flow in your budget.

For some, this predictability of fixed interest rates and consistent monthly payments offers immense peace of mind. You know exactly what you owe each month, making budgeting simpler and less stressful. However, it’s vital to remember that a longer term also means you’ll be paying interest for a longer period, potentially increasing the total cost of borrowing if not managed wisely.

Potential Tax Deductibility

Historically, the interest paid on Home Equity Loans was often tax-deductible if the funds were used for home improvements. While the Tax Cuts and Jobs Act of 2017 significantly altered this, interest can still be deductible under specific circumstances if the loan is used to "buy, build, or substantially improve" the home that secures the loan.

It’s crucial to consult with a qualified tax advisor to understand the current rules and how they apply to your specific situation. While using the loan for a car purchase typically doesn’t qualify for tax deductibility, understanding the broader tax implications of home equity products is part of making an informed decision.

The Significant Risk: Your Home as Collateral

This is perhaps the most critical consideration for any Home Equity Loan. Your home serves as the collateral. This means if you default on the loan – if you fail to make your payments as agreed – the lender has the legal right to foreclose on your home. This is a far more severe consequence than a car repossession.

Common mistakes to avoid are underestimating the long-term commitment and the potential for life changes to impact your ability to make payments. Losing your primary residence is a devastating outcome, highlighting the importance of careful financial planning and a stable income before taking on such a significant obligation.

Other Considerations: Closing Costs and Borrowing Limits

Like your primary mortgage, a Home Equity Loan comes with closing costs. These can include appraisal fees, origination fees, title search fees, and other charges, often totaling 2% to 5% of the loan amount. While these costs can sometimes be rolled into the loan, they add to the overall cost of borrowing.

Lenders typically allow you to borrow up to 80% or 90% of your home’s equity, minus your outstanding mortgage balance. For example, if your home is worth $400,000 and you owe $200,000 on your mortgage, you have $200,000 in equity. A lender might allow you to borrow up to 80% of your home’s value, which is $320,000. Subtracting your $200,000 mortgage leaves you with $120,000 in available equity for a loan.

Delving into the Home Equity Line of Credit (HELOC): A Flexible Alternative

While closely related to a Home Equity Loan, a Home Equity Line of Credit (HELOC) operates differently and offers distinct advantages and disadvantages. Instead of a lump sum, a HELOC provides a revolving line of credit, similar to a credit card, but secured by your home.

You can draw funds as needed, up to a pre-approved limit, during a "draw period" (often 10 years). You only pay interest on the amount you actually borrow, not the entire approved line. After the draw period ends, the loan converts to a repayment period, during which you pay back both principal and interest.

Flexibility with a Catch: Variable Interest Rates

The primary appeal of a HELOC is its flexibility. You can access funds when you need them, making it suitable for ongoing projects or unexpected expenses. However, this flexibility often comes with a variable interest rate, meaning your monthly payments can fluctuate.

This variable rate introduces an element of unpredictability. If market interest rates rise, your monthly payments will increase, potentially straining your budget. Pro tips from us include carefully monitoring interest rate trends and building a financial buffer to absorb potential payment increases.

Temptation to Overspend

Because a HELOC is a revolving line of credit, there can be a temptation to use it for non-essential purchases or to overextend yourself financially. Unlike a fixed-purpose loan, the funds are readily available, which requires significant financial discipline.

While a HELOC can be a powerful financial tool, using it to finance a depreciating asset like a car, especially if you’re not diligent about repayment, can lead to long-term financial woes. It’s essential to approach a HELOC with a clear plan and a strong commitment to responsible borrowing.

Demystifying the Car Loan (Auto Loan): The Traditional Path

A traditional Car Loan, or Auto Loan, is specifically designed for the purchase of a vehicle. It’s a secured loan, with the car itself serving as collateral. If you fail to make payments, the lender can repossess the vehicle. These loans are widely available through banks, credit unions, and dealership financing.

Car Loans typically come with fixed interest rates and shorter repayment terms, usually ranging from 36 to 72 months, though some lenders offer longer terms up to 84 months. The application process is generally quicker and less involved than for a Home Equity Loan.

Straightforward and Purpose-Specific

One of the main advantages of a Car Loan is its simplicity. It’s a straightforward transaction: you borrow money to buy a car, and you pay it back over a set period. There are no questions about how the funds will be used, and the loan amount is directly tied to the vehicle’s purchase price.

This clear purpose can make budgeting easier, as the loan is entirely separate from your home finances. You’re not commingling assets or putting your most valuable possession at risk.

Car as Collateral, Not Your Home

With a Car Loan, only the car is at risk if you default. While losing your vehicle can be a significant inconvenience and financial setback, it doesn’t carry the same devastating consequences as losing your home. This distinction is a major comfort for many borrowers who prefer to keep their home equity untouched and separate from their vehicle financing.

Shorter Repayment Terms and Quick Approval

Car Loans typically have shorter repayment terms, meaning you’ll be debt-free sooner. While the monthly payments might be higher than a Home Equity Loan for the same amount, the overall interest paid can be less if the interest rate is comparable and the term is significantly shorter.

The approval process for a Car Loan is generally much faster. You can often get pre-approved within minutes or hours, allowing you to shop for a car with confidence in your budget. This speed and convenience are appealing for those who need a vehicle quickly.

Higher Interest Rates and a Depreciating Asset

Generally, interest rates on Car Loans are higher than those on Home Equity Loans. This is partly because cars are depreciating assets – they lose value over time – making them riskier collateral for lenders. The value of your car will likely be less at the end of the loan term than when you bought it.

This leads to a common problem: negative equity, also known as being "upside down" on your loan. This occurs when you owe more on the car than it’s currently worth. Common mistakes to avoid are extending the loan term too long, making a small down payment, or rolling over negative equity from a previous car. If your car is totaled or stolen and you have negative equity, you could still owe money on a vehicle you no longer possess.

Limitations and Fees

Car Loans are specific to the vehicle you’re purchasing. Lenders may have restrictions on the age or mileage of the car they will finance, particularly for used vehicles. Additionally, while not as extensive as closing costs for a mortgage, Car Loans can come with various fees, such as origination fees, documentation fees, and late payment charges.

For more on managing debt effectively and understanding different loan types, check out our guide to Smart Debt Management Strategies.

Home Equity Loan vs. Car Loan: A Head-to-Head Comparison

To help clarify the differences, let’s put these two financing options side-by-side:

| Feature | Home Equity Loan (or HELOC) | Traditional Car Loan (Auto Loan) |

|---|---|---|

| Collateral | Your home | The vehicle being purchased |

| Interest Rates | Generally lower due to less risk (secured by home) | Generally higher (car is a depreciating asset) |

| Loan Term | Longer (typically 5-30 years) | Shorter (typically 3-7 years) |

| Monthly Payment | Potentially lower due to longer term | Potentially higher due to shorter term and higher rates |

| Application Process | More complex, involves home appraisal, closing costs | Simpler, quicker, often approved within hours |

| Use of Funds | Flexible – can be used for anything, including a car | Specific – solely for the purchase of the vehicle |

| Risk | Risk of losing your home if you default | Risk of car repossession if you default |

| Tax Implications | Interest potentially tax-deductible under specific circumstances (consult tax advisor) | Interest is generally not tax-deductible |

| Fees | Closing costs (appraisal, origination, title, etc.) | Origination fees, documentation fees, late fees |

| Asset Value | Secured by an appreciating (or stable) asset | Secured by a rapidly depreciating asset |

When to Consider a Home Equity Loan for Your Car

While the risks are significant, there are specific scenarios where using a Home Equity Loan for a car purchase might make financial sense:

- You Have Substantial Home Equity: This is the foundational requirement. You need enough equity to borrow against without overextending yourself.

- Excellent Credit Score: A strong credit history will help you qualify for the lowest possible interest rates on a Home Equity Loan, maximizing the benefit of this financing option.

- You Need a Large Sum for an Expensive Vehicle: If you’re buying a luxury car or a high-end electric vehicle, the lower interest rates and longer terms of a Home Equity Loan can make the large monthly payments more manageable.

- You Prioritize Lower Monthly Payments Over Shorter Term: If cash flow is a primary concern, the extended repayment period of a Home Equity Loan can significantly reduce your monthly obligations.

- You Are Financially Disciplined and Understand the Risks: Pro tips from us: Only consider this option if you have a stable income, an emergency fund, and a rock-solid commitment to making every payment on time. You must fully grasp that your home is on the line.

- You Plan to Pay it Off Early: Even with a long term, if you intend to pay down the car portion of the loan aggressively, you can benefit from the lower interest rate while mitigating the extended repayment period.

When a Traditional Car Loan is the Better Choice

For most people, a traditional Car Loan remains the safer and more practical choice for vehicle financing:

- Limited Home Equity: If you haven’t built up substantial equity in your home, a Home Equity Loan simply isn’t an option.

- You Don’t Want to Risk Your Home: This is a non-negotiable factor for many. The peace of mind that comes from knowing your home is not collateral for your car loan is invaluable.

- You Prefer a Shorter Repayment Period: Getting out of debt faster is a significant financial goal for many. Car Loans, with their shorter terms, help you achieve this.

- Buying a Moderately Priced Car: For standard vehicle purchases, the interest rate difference might not be significant enough to warrant the added risk and complexity of a Home Equity Loan.

- You Want a Simpler, Quicker Process: If convenience and speed are priorities, a Car Loan’s streamlined application and approval process are highly advantageous.

- You Qualify for Low APR Car Loans: Dealerships and banks often offer promotional low APR (Annual Percentage Rate) financing for new cars, especially for buyers with excellent credit. In such cases, a Car Loan might even have a lower rate than a Home Equity Loan.

Key Factors to Consider Before Deciding

Before you commit to either a Home Equity Loan or a Car Loan, take a moment to reflect on these critical factors:

- Your Current Home Equity: How much equity do you truly have? Do you feel comfortable using it as collateral?

- Your Credit Score and History: A higher credit score will unlock better interest rates for both loan types, but especially for Home Equity Loans.

- Current Interest Rate Environment: Are interest rates rising or falling? This can impact the attractiveness of a fixed-rate Home Equity Loan versus a variable-rate HELOC, or even influence car loan rates.

- Your Financial Stability and Risk Tolerance: Do you have a stable job, an emergency fund, and a comfortable debt-to-income ratio? How comfortable are you with the idea of putting your home at risk?

- The Total Cost of Borrowing: Always look beyond the monthly payment. Calculate the total interest paid over the life of the loan, including any fees, to determine the true cost.

- The Value and Age of the Car You’re Buying: Remember, a car is a depreciating asset. Borrowing against an appreciating asset (your home) to buy a depreciating one requires careful thought.

- Alternative Financing Options: Have you considered saving up for a larger down payment, or exploring other lending options like personal loans (though these typically have higher rates)?

For an independent perspective on consumer finance and lending, it’s always wise to consult trusted external resources like the Consumer Financial Protection Bureau (CFPB) website for general guidance and current financial advice: www.consumerfinance.gov.

Conclusion: Making the Right Financial Move for Your Future

The decision between a Home Equity Loan and a traditional Car Loan is a deeply personal one, with no universal "best" answer. It hinges on your unique financial situation, risk tolerance, and long-term goals.

A Home Equity Loan offers the allure of lower interest rates and longer repayment terms, potentially freeing up monthly cash flow. However, this comes with the significant risk of using your home as collateral and the added complexity of closing costs. A traditional Car Loan, while often having higher interest rates, offers simplicity, a quicker process, and keeps your home equity safe from vehicle-specific debt.

Ultimately, making an informed choice requires careful consideration of all factors, a thorough understanding of the risks involved, and a clear vision of your financial future. We highly recommend consulting with a qualified financial advisor. They can provide personalized guidance, help you assess your specific circumstances, and ensure you make a decision that best serves your financial well-being, paving the way for a secure and prosperous journey ahead.