How Big Of A Car Loan Can I Afford? Your Ultimate Guide to Smart Car Financing

How Big Of A Car Loan Can I Afford? Your Ultimate Guide to Smart Car Financing Carloan.Guidemechanic.com

Buying a car is an exciting milestone, offering freedom, convenience, and often, a significant upgrade to your daily life. However, for many, the dream can quickly turn into a financial nightmare if not approached with careful planning. The most common question that surfaces during this process is, "How big of a car loan can I afford?"

This isn’t just a simple math problem; it’s a critical financial decision that impacts your monthly budget, your future financial goals, and your overall peace of mind. As an expert blogger and professional SEO content writer, I’ve seen countless individuals make mistakes by focusing solely on the monthly payment without understanding the bigger picture. This comprehensive guide is designed to empower you with the knowledge and tools to confidently determine a car loan amount that aligns with your true financial capacity. We’ll dive deep into every factor, ensuring you make an informed decision that drives you towards financial stability, not away from it.

How Big Of A Car Loan Can I Afford? Your Ultimate Guide to Smart Car Financing

Why Car Loan Affordability Matters More Than You Think

Understanding your car loan affordability goes far beyond just being able to make the monthly payment. It’s about safeguarding your financial health, preventing unnecessary stress, and ensuring your car purchase doesn’t derail other important life goals like saving for a home, retirement, or your children’s education.

Many people fall into the trap of only looking at the advertised monthly payment. While it’s a crucial component, it’s merely one piece of a much larger puzzle. A low monthly payment might seem attractive, but it could hide a longer loan term, higher interest rates, or a car that’s ultimately too expensive for your budget. Based on my experience, failing to consider the total cost of ownership and your comprehensive financial situation is a common mistake that leads to buyer’s remorse and financial strain.

The Core Pillars: Key Factors Determining Your Car Loan Affordability

To truly understand how big of a car loan you can afford, we need to examine several interconnected financial pillars. Each plays a vital role in painting a complete picture of your borrowing capacity.

Your Income and Employment Stability

Your income is the foundation of your borrowing power. Lenders primarily assess your gross monthly income – the amount you earn before taxes and deductions. However, it’s your net income, what you actually take home, that dictates how much discretionary income you have available for car payments and other expenses.

Beyond the number, lenders also scrutinize your employment stability. A consistent work history, typically two years or more with the same employer or within the same industry, signals reliability. This stability reassures lenders that you have a steady stream of income to repay the loan. Pro tips from us: Lenders prefer borrowers who demonstrate long-term financial consistency, as it significantly reduces their risk.

Your Current Debts and Debt-to-Income (DTI) Ratio

This is arguably one of the most critical factors. Your Debt-to-Income (DTI) ratio is a percentage that compares your total monthly debt payments to your gross monthly income. It’s a powerful indicator of how much of your income is already committed to existing obligations.

To calculate your DTI, sum up all your recurring monthly debt payments – this includes mortgage or rent, credit card minimums, student loans, personal loans, and any other car loans. Divide this total by your gross monthly income and multiply by 100 to get a percentage. For example, if your total monthly debt payments are $1,500 and your gross monthly income is $5,000, your DTI is 30% ($1,500 / $5,000 = 0.30, or 30%). Lenders generally prefer a DTI ratio of 36% or lower, though some might go up to 43% for certain loans. A lower DTI indicates you have more disposable income to comfortably manage new debt, making you a more attractive borrower.

Your Credit Score

Your credit score is a numerical representation of your creditworthiness. It’s a three-digit number that summarizes your payment history, amounts owed, length of credit history, new credit, and credit mix. A higher credit score signals to lenders that you are a responsible borrower who pays bills on time, thus posing less risk.

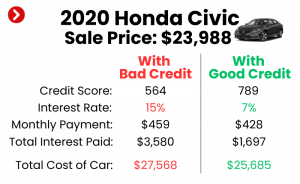

The impact of your credit score on a car loan is profound. It directly influences the interest rate you’ll be offered. Borrowers with excellent credit (typically 780+) can qualify for the lowest interest rates, saving thousands of dollars over the life of the loan. Those with lower scores (below 600) will face significantly higher rates, increasing their total cost of borrowing. Common mistakes to avoid are applying for a loan without checking your credit score first, as this can lead to disappointment and potentially accepting an unfavorable rate.

The Down Payment You Can Make

A down payment is the initial amount of money you pay upfront for the car, reducing the total amount you need to borrow. This is a powerful tool for improving your loan affordability. A larger down payment has several significant benefits.

Firstly, it lowers your monthly loan payments because you’re financing a smaller principal amount. Secondly, it reduces the total interest you’ll pay over the loan term. Thirdly, a substantial down payment helps you avoid negative equity, which occurs when you owe more on the car than it’s worth. Many financial experts recommend a down payment of at least 20% for a new car and 10% for a used car. While not always feasible, aiming for these percentages can put you in a much stronger financial position.

The Loan Term (Length of the Loan)

The loan term, or the length of time you have to repay the loan, directly impacts your monthly payment and the total interest paid. Longer loan terms (e.g., 72 or 84 months) result in lower monthly payments, which can make a more expensive car seem "affordable" on a month-to-month basis.

However, stretching out the loan term also means you’ll pay significantly more in total interest over the life of the loan. You also run a higher risk of negative equity, especially with a new car, as its value depreciates rapidly in the initial years. Shorter loan terms (e.g., 36 or 48 months) mean higher monthly payments, but you pay less interest overall and own the car outright much sooner. Pro tips from us: Always balance the desire for a lower monthly payment with the total cost of interest and the speed at which you want to be debt-free.

Interest Rates

The interest rate is the cost of borrowing money, expressed as a percentage of the loan amount. This rate is heavily influenced by your credit score, the current market conditions, and the loan term. A difference of just a few percentage points can amount to hundreds or even thousands of dollars over the life of your car loan.

For example, on a $25,000 loan over 60 months, a 5% interest rate results in total interest of approximately $3,300. At 9%, that jumps to over $6,100. Shopping around for the best interest rate, getting pre-approved by multiple lenders, and maintaining a strong credit score are crucial steps to minimize this cost.

Your Budget for Car Ownership (Beyond the Loan Payment)

This is where many people underestimate the true cost of owning a car. The loan payment is just one piece of the puzzle. A truly affordable car loan means you can comfortably cover all associated expenses without straining your budget. These "hidden" costs can quickly add up:

- Car Insurance: Premiums vary widely based on your age, driving record, location, vehicle type, and coverage limits. Get quotes before you buy.

- Fuel Costs: Consider your daily commute, vehicle’s fuel efficiency, and fluctuating gas prices.

- Maintenance & Repairs: All cars need regular oil changes, tire rotations, and eventual repairs. Newer cars might have lower immediate maintenance, but parts can be expensive. Older cars might have higher repair frequency.

- Registration & Taxes: Annual registration fees, property taxes (in some states), and sales tax on the purchase are unavoidable.

- Parking Fees & Tolls: If applicable to your lifestyle.

Many people overlook these critical ownership costs, leading to a feeling that their car is more expensive than they anticipated. Based on years of advising on personal finance, it’s these overlooked expenses that often lead to financial stress, even if the loan payment itself seems manageable.

Practical Steps to Calculate How Much Car Loan You Can Afford

Now that we understand the influencing factors, let’s put it into action with a step-by-step approach.

Step 1: Assess Your Monthly Income and Expenses

Start by creating a detailed budget. List all your sources of monthly income and track every single expense for at least a month, ideally two or three. Categorize them into fixed expenses (rent/mortgage, existing loan payments, insurance premiums) and variable expenses (groceries, entertainment, dining out, utilities).

This exercise reveals your true disposable income – the money left over after all necessary expenses are paid. This amount will help you determine how much you can realistically allocate to a car payment without sacrificing other financial goals or necessities.

Step 2: Calculate Your Debt-to-Income (DTI) Ratio

As discussed, this is a vital health check for your finances.

- Total Monthly Debt Payments: Sum up all your minimum monthly payments for credit cards, student loans, personal loans, and any existing car loans. (Do NOT include rent/mortgage in this calculation for now, as lenders often use a separate housing-related DTI).

- Gross Monthly Income: Your income before taxes and deductions.

- DTI Formula: (Total Monthly Debt Payments / Gross Monthly Income) x 100

Aim for your new DTI (including the projected car payment) to be below 36%. This leaves you with ample financial flexibility.

Step 3: Determine Your Affordable Monthly Car Payment

A common guideline is the 20/4/10 Rule:

- 20% Down Payment: Aim for at least 20% of the car’s purchase price.

- 4-Year Loan Term: Keep your loan term to no more than four years (48 months) to minimize interest paid and avoid negative equity.

- 10% of Gross Income: Your total monthly car expenses (loan payment, insurance, fuel, maintenance) should not exceed 10% of your gross monthly income.

While the 20/4/10 rule is a great benchmark, your personal budget from Step 1 is paramount. If you have high living costs or ambitious savings goals, you might need to aim for an even lower percentage.

Step 4: Get Pre-Approved for a Loan

Before you even step foot in a dealership, get pre-approved for a car loan from banks, credit unions, or online lenders. Pre-approval gives you:

- A concrete interest rate: You’ll know exactly what rate you qualify for.

- A maximum loan amount: This sets a clear budget for the car itself.

- Negotiating power: You become a cash buyer, allowing you to focus on negotiating the car’s price, not the monthly payment.

Getting pre-approved from multiple lenders within a short window (typically 14-45 days, depending on the credit scoring model) will usually only count as a single hard inquiry on your credit report, allowing you to shop for the best rate without harming your score.

Step 5: Factor in Down Payment and Trade-in Value

If you have a vehicle to trade in, get its estimated value from reputable sources like Kelley Blue Book or Edmunds. This value, combined with your cash down payment, reduces the amount you need to finance. The higher your combined down payment and trade-in, the smaller the loan amount and subsequently, the lower your monthly payments and total interest.

Step 6: Don’t Forget the "Hidden" Costs

Revisit the costs we discussed earlier: insurance, fuel, maintenance, registration, and taxes. Use online calculators or get actual quotes for insurance to add these into your total monthly car ownership budget. This ensures your chosen car loan amount still leaves room for these essential expenses. Remember, the 10% rule mentioned in Step 3 applies to all car-related expenses, not just the loan payment.

Common Mistakes to Avoid When Figuring Out Car Loan Affordability

Navigating the car buying process can be tricky, and it’s easy to make missteps that can cost you dearly in the long run. Based on years of advising on personal finance, here are some common pitfalls:

- Focusing Only on the Monthly Payment: This is the biggest trap. A low monthly payment might mean an extended loan term and significantly more interest paid over time, or even negative equity. Always consider the total cost of the loan.

- Ignoring the Total Cost of Ownership: As discussed, insurance, fuel, maintenance, and registration add up. Neglecting these can make an otherwise affordable loan payment feel unbearable.

- Not Getting Pre-Approved: Walking into a dealership without a pre-approval puts you at a disadvantage. The dealership’s finance department might offer you a less favorable rate, knowing you haven’t shopped around.

- Stretching the Loan Term Too Long: While an 84-month loan lowers your monthly payment, it dramatically increases the total interest you pay and leaves you vulnerable to being "upside down" on your loan.

- Underestimating Future Expenses: Life happens. Don’t assume your income will always increase or that you won’t face unexpected expenses. Build a buffer into your budget.

- Not Checking Your Credit Report: Errors on your credit report can negatively impact your score, leading to higher interest rates. Always review your report for accuracy before applying for a loan. You can get a free copy annually from AnnualCreditReport.com.

Pro Tips for Securing the Best Car Loan

You’ve done the hard work of assessing your affordability. Now, here are some pro tips from us to help you secure the most favorable loan terms possible:

- Improve Your Credit Score: If your credit score isn’t in the excellent range, take steps to improve it before applying. Pay down existing debts, make all payments on time, and avoid opening new lines of credit. Even a small increase can lead to a lower interest rate. For more detailed guidance, consider reading our article on .

- Save for a Larger Down Payment: The more you put down, the less you borrow, which means lower monthly payments and less interest paid overall. A larger down payment also reduces your risk of negative equity.

- Shop Around for Lenders: Don’t just accept the first offer you receive, especially from the dealership. Get quotes from at least three different lenders (banks, credit unions, online lenders) to compare interest rates and terms. Credit unions, in particular, often offer very competitive rates.

- Negotiate the Car Price, Not Just the Payment: Always treat your car purchase as two separate transactions: negotiating the car’s price and negotiating the loan terms. Focus on getting the lowest possible purchase price first. Then, apply your pre-approved loan or compare it to the dealer’s financing offer.

- Consider Refinancing Later: If you have less-than-stellar credit now but plan to improve it, you might consider refinancing your car loan down the road. Once your credit score improves, you could qualify for a lower interest rate, reducing your monthly payment or the total interest paid.

- Understand All Fees: Beyond the interest rate, be aware of any origination fees, documentation fees, or other charges associated with the loan. Read the fine print carefully.

- Know Your Trade-In Value Separately: If you’re trading in a car, research its value beforehand. Don’t let the dealer bundle the trade-in value into the new car’s price negotiation; negotiate it as a separate transaction to ensure you’re getting a fair deal.

Conclusion: Drive Smart, Not Just Fast

Determining "how big of a car loan can I afford" is a multi-faceted process that demands a holistic view of your financial health. It’s not just about the shiny new car; it’s about smart financial planning that allows you to enjoy your vehicle without sacrificing your long-term economic well-being. By diligently assessing your income, managing your debts, understanding your credit score, making a strategic down payment, and considering all associated ownership costs, you empower yourself to make a truly informed decision.

Remember, the goal is not to get approved for the maximum amount a lender might offer, but to secure a loan that comfortably fits within your budget and helps you achieve your broader financial objectives. Take control of your car buying journey, be patient, do your homework, and prioritize your financial future. Start by creating that detailed budget today, and drive away with confidence! For further insights into budgeting and managing your finances effectively, explore our guide on . For an external perspective on car loan considerations, you might find valuable information from the Consumer Financial Protection Bureau’s advice on auto loans: .