How Do I Get Approved For A Car Loan: Your Ultimate Guide to Driving Away with Confidence

How Do I Get Approved For A Car Loan: Your Ultimate Guide to Driving Away with Confidence Carloan.Guidemechanic.com

Dreaming of a new set of wheels? Whether it’s for daily commutes, family adventures, or simply the freedom of the open road, owning a car is a significant milestone for many. However, the path to car ownership often involves navigating the world of car loans, which can seem daunting at first glance. The burning question on many minds is, "How do I get approved for a car loan?"

Securing a car loan doesn’t have to be a mystery. It’s a structured process where lenders evaluate your financial health to determine your eligibility and the terms they can offer. As an expert blogger and professional SEO content writer, I’ve seen firsthand the common pitfalls and successful strategies people employ. This comprehensive guide will demystify the entire process, providing you with the knowledge and actionable steps to significantly boost your chances of getting approved for a car loan with favorable terms. We’re going to dive deep, covering everything from understanding what lenders look for to mastering the application process, ensuring you’re well-equipped to make informed decisions.

How Do I Get Approved For A Car Loan: Your Ultimate Guide to Driving Away with Confidence

Understanding the Car Loan Landscape: What Lenders Really Look For

Before you even start browsing vehicles, it’s crucial to understand the foundation of car loan approval. Lenders aren’t just looking at your enthusiasm for a new car; they’re assessing your ability and willingness to repay the loan. This assessment is multifaceted, taking into account several key financial indicators that paint a picture of your creditworthiness.

Based on my experience in the financial education space, most lenders, whether banks, credit unions, or auto finance companies, operate on a similar set of criteria. They want to minimize their risk, and your financial profile helps them do just that. Getting a car loan is less about luck and more about preparation and understanding these fundamental requirements.

Key Factors Lenders Consider for Car Loan Approval

To truly answer "How do I get approved for a car loan?", we need to break down the critical elements that form the basis of a lender’s decision. Each of these factors plays a significant role in not only your approval but also the interest rate and loan terms you’ll receive.

1. Your Credit Score and Credit History

This is arguably the most influential factor in your car loan application. Your credit score, typically a FICO Score or VantageScore, is a three-digit number that summarizes your credit risk based on your credit report. It tells lenders how responsibly you’ve managed credit in the past.

A higher credit score signals lower risk to lenders, making you a more attractive borrower. Generally, scores above 700 are considered good, while those in the 600s might still get approved but often with higher interest rates. Scores below 600 often present challenges, though approval is not impossible. Your credit history, which details your past borrowing and repayment behavior, is equally important. Lenders examine things like payment history, the length of your credit history, types of credit used, and any outstanding debts.

Pro tips from us: Regularly checking your credit score and report is not just a good habit; it’s a necessity before applying for any significant loan. You want to ensure there are no errors that could negatively impact your standing. Even minor discrepancies can make a difference in your car loan approval chances.

2. Your Income and Employment Stability

Lenders need assurance that you have a consistent and sufficient income to cover your monthly car loan payments. This isn’t just about the dollar amount; it’s also about the stability of your employment. Someone with a long-term, stable job in a consistent industry will generally be viewed more favorably than someone with a sporadic work history or frequent job changes.

You’ll typically need to provide proof of income, such as recent pay stubs, W-2 forms, or tax returns if you’re self-employed. Lenders use this information to calculate your debt-to-income ratio, which we’ll discuss shortly. The goal here is to demonstrate that your income is reliable and robust enough to handle the additional financial commitment of a car loan.

3. Your Down Payment Amount

Making a down payment on a car loan is a powerful signal to lenders. It shows your commitment to the purchase and immediately reduces the amount you need to borrow, thereby lowering the lender’s risk. A larger down payment also translates to a lower loan amount, which means smaller monthly payments and less interest paid over the life of the loan.

Common mistakes to avoid are thinking you don’t need a down payment at all, especially if your credit isn’t stellar. While 0% down loans exist, they are often reserved for buyers with excellent credit or come with higher interest rates. Aim for at least 10-20% of the car’s purchase price as a down payment if possible. This significantly improves your car loan approval prospects and can save you a substantial amount of money in the long run.

4. Your Debt-to-Income (DTI) Ratio

Your Debt-to-Income (DTI) ratio is a crucial metric lenders use to assess your ability to manage monthly payments. It’s calculated by dividing your total monthly debt payments (including rent/mortgage, credit card payments, student loans, etc.) by your gross monthly income. For instance, if your total monthly debt is $1,500 and your gross monthly income is $4,000, your DTI is 37.5%.

Lenders prefer a lower DTI, typically under 43%, though some prefer it even lower, around 36% for auto loans. A high DTI suggests that too much of your income is already allocated to existing debts, making it difficult to take on a new car payment. To improve your DTI, you can either increase your income or reduce your existing debt.

5. Loan-to-Value (LTV) Ratio

The Loan-to-Value (LTV) ratio compares the amount you want to borrow for the car to the car’s actual market value. If you’re borrowing $25,000 for a car valued at $20,000, your LTV is 125%. Lenders are generally more comfortable with an LTV of 100% or less, meaning you’re borrowing no more than the car is worth, or even less, thanks to a down payment or trade-in.

A high LTV indicates that you’re "upside down" or "underwater" on the loan from day one, meaning you owe more than the car is worth. This increases the risk for the lender, as they might not recover their money if you default and they have to repossess the vehicle. A good down payment or a valuable trade-in can significantly reduce your LTV and make your car loan application much stronger.

6. The Presence of a Co-Signer (If Applicable)

If your credit history is limited, your credit score is low, or your income isn’t quite sufficient, a co-signer can be a game-changer for car loan approval. A co-signer is someone, usually a trusted family member or friend with excellent credit, who agrees to be equally responsible for the loan if you fail to make payments.

While a co-signer can open doors, it’s crucial to understand the implications. The co-signer’s credit is on the line, and any missed payments will negatively impact both your credit reports. Based on my observations, it’s a serious commitment for the co-signer and should only be considered with a clear understanding of the responsibilities involved.

The Step-by-Step Process to Boost Your Car Loan Approval Chances

Now that you understand the key factors, let’s walk through the practical steps you can take to prepare yourself and navigate the application process successfully. This proactive approach is key to getting approved for a car loan.

Step 1: Check Your Credit Report and Score Thoroughly

This is your starting line. Obtain your credit reports from all three major credit bureaus (Experian, Equifax, and TransUnion) via AnnualCreditReport.com – this is the only federally authorized source for free annual credit reports. Review them meticulously for any inaccuracies, old debts that should be removed, or fraudulent activity.

Dispute any errors immediately. Correcting mistakes can often boost your credit score significantly, sometimes by dozens of points. Knowing your score also gives you a realistic expectation of the interest rates you might qualify for and helps you identify areas for improvement.

Step 2: Understand Your Budget and True Affordability

Before you fall in love with a specific car, establish a realistic budget. This isn’t just about the monthly car payment; it includes insurance, fuel, maintenance, and potential repair costs. Use an online car loan calculator to estimate monthly payments based on different loan amounts, interest rates, and terms.

Pro tips from us: Don’t just focus on the lowest possible monthly payment. A longer loan term might reduce your payment, but it also means you’ll pay significantly more in interest over time. Aim for a loan term that balances affordability with the total cost of the loan.

Step 3: Save for a Substantial Down Payment

As discussed, a larger down payment improves your LTV ratio and reduces the overall loan amount. Saving up even a modest sum, say 10% of the car’s price, can make a significant difference in your car loan approval odds and the interest rate offered.

Consider setting up an automatic savings plan specifically for your car down payment. Every dollar you put down is a dollar you don’t have to borrow, saving you interest and making your application more appealing.

Step 4: Get Pre-Approved for a Car Loan First

One of the most powerful strategies is to get pre-approved for a car loan before you even set foot in a dealership. Pre-approval involves a lender reviewing your financial information and giving you a conditional offer for a specific loan amount and interest rate.

This gives you significant leverage at the dealership because you’ll know exactly what you can afford and what interest rate you qualify for. It also separates the financing negotiation from the car price negotiation, allowing you to focus on getting the best deal on the vehicle itself. A pre-approval typically involves a soft credit inquiry, which doesn’t harm your score, until you finalize the loan.

Step 5: Gather All Necessary Documents

Being prepared with your paperwork streamlines the application process. While requirements vary slightly by lender, you’ll generally need:

- Government-issued photo ID (driver’s license, passport)

- Proof of income (recent pay stubs, W-2s, tax returns for self-employed)

- Proof of residence (utility bill, lease agreement)

- Bank statements

- Social Security Number

- Trade-in title/information (if applicable)

Having these ready demonstrates your seriousness and efficiency, speeding up the car loan approval process.

Step 6: Choose the Right Lender for Your Needs

Don’t limit yourself to just dealership financing. Explore various types of lenders:

- Banks: Often offer competitive rates for well-qualified borrowers.

- Credit Unions: Known for member-friendly rates and personalized service, especially if you have an existing relationship.

- Online Lenders: Provide quick applications and competitive offers, often catering to a wider range of credit scores.

- Dealership Financing: Convenient, but compare their offers with your pre-approval to ensure you’re getting the best deal.

Pro tip: Compare at least three to four loan offers. Shopping around within a 14-45 day window for auto loans counts as a single inquiry on your credit report, minimizing the impact on your score. This allows you to find the best possible interest rate and terms for your car loan.

Step 7: Select the Right Vehicle for Your Financial Situation

The type of car you choose significantly impacts your car loan approval. More expensive cars naturally require larger loans, which can be harder to get approved for, especially if your income or credit isn’t top-tier. Consider a reliable, more affordable used car if you’re concerned about approval or want to keep payments low.

New cars generally have higher prices and depreciate quickly, potentially leading to a higher LTV. Used cars, while potentially having higher interest rates depending on age, can offer a more manageable purchase price and therefore a smaller loan amount, improving your chances of getting approved for a car loan.

Common Mistakes to Avoid When Applying for a Car Loan

Based on my observations of countless applicants, certain missteps can severely hinder your car loan approval chances or lead to unfavorable terms. Steering clear of these common pitfalls will put you on a smoother path.

- Applying for Too Many Loans at Once: While shopping for rates within a short window is fine, indiscriminately applying to numerous lenders outside that window can result in multiple hard inquiries on your credit report, which can temporarily lower your score.

- Not Checking Your Credit Beforehand: Going into the application process blind means you might be surprised by your score or discover errors too late, delaying or even derailing your car loan approval.

- Underestimating Total Ownership Costs: Focusing solely on the car’s price or monthly payment without considering insurance, fuel, and maintenance can lead to financial strain down the road, making lenders hesitant.

- Going to the Dealership Without Pre-Approval: This puts you at a disadvantage. Without a pre-approval in hand, you lose valuable negotiation power and might settle for less favorable financing offered by the dealership.

- Stretching the Loan Term Too Long: While a 72- or 84-month loan might offer lower monthly payments, you’ll pay significantly more in interest over time, and you risk being "upside down" on your loan for a longer period.

Special Situations: Getting Approved with Less-Than-Perfect Credit

Even if your credit score isn’t ideal, getting approved for a car loan is still possible, though it might require a slightly different approach. Don’t despair if you’re in this boat; many lenders specialize in helping individuals rebuild their credit.

- Secured Loans: Some lenders offer secured auto loans, where the car itself acts as collateral. This reduces the lender’s risk, making them more willing to approve applicants with lower credit scores.

- Co-Signers: As mentioned earlier, a co-signer with good credit can significantly improve your chances. They act as a guarantee for the lender.

- Higher Down Payment or Trade-In: A substantial down payment or a valuable trade-in reduces the amount you need to borrow, offsetting the risk associated with a lower credit score.

- Bad Credit Car Loans: Be aware that "bad credit" or "subprime" auto loans often come with higher interest rates and sometimes less favorable terms. However, they can be a stepping stone to rebuilding your credit if managed responsibly.

- Focus on Rebuilding Credit: If time permits, dedicate a few months to improving your credit score before applying. Pay down existing debts, make all payments on time, and dispute any errors. For more detailed strategies on improving your credit, check out our guide on . This proactive step can save you thousands in interest over the life of your car loan.

The Final Steps: What Happens After Approval?

Congratulations! Once you’ve been approved for a car loan and have chosen your vehicle, there are a few final but crucial steps to ensure a smooth closing.

Carefully review the entire loan agreement before signing. Pay close attention to:

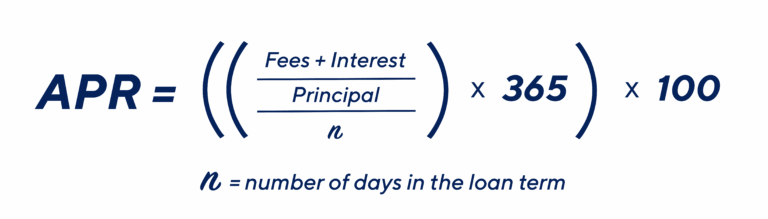

- Interest Rate and APR: Understand the difference. APR (Annual Percentage Rate) includes the interest rate plus any additional fees, giving you the true cost of borrowing.

- Loan Term: Confirm the length of your loan.

- Monthly Payment: Ensure it matches your budget.

- Any Fees: Look for origination fees, documentation fees, or prepayment penalties.

- Payment Schedule: Know exactly when your payments are due.

- Insurance Requirements: Lenders typically require full coverage (collision and comprehensive) insurance until the loan is paid off.

Understanding every clause protects you and ensures there are no surprises down the road. Don’t hesitate to ask questions if anything is unclear.

Drive Away with Confidence

Getting approved for a car loan is a significant financial step, but it doesn’t have to be an intimidating one. By understanding the factors lenders consider, preparing your finances, and following a strategic application process, you can significantly increase your chances of securing a car loan with favorable terms.

Remember, preparation is your most powerful tool. Check your credit, budget wisely, save for a down payment, and get pre-approved. With this comprehensive guide, you now have the knowledge to navigate the auto loan landscape like a seasoned pro. Take these steps, and you’ll be well on your way to answering "How do I get approved for a car loan?" with a resounding "I did it!" and driving off in your new vehicle with confidence.