How Do You Get a Car Loan: Your Ultimate Step-by-Step Guide to Approval & Great Rates

How Do You Get a Car Loan: Your Ultimate Step-by-Step Guide to Approval & Great Rates Carloan.Guidemechanic.com

Navigating the world of car loans can feel like deciphering a complex financial puzzle. For many, the dream of a new set of wheels can quickly turn into a stressful endeavor when faced with interest rates, credit checks, and confusing terminology. But what if there was a clear, actionable roadmap to securing not just a car loan, but the best car loan for your situation?

Based on my experience as a financial content writer and observing countless individuals successfully secure their vehicle financing, the secret lies in preparation and understanding. This comprehensive guide is designed to empower you, breaking down every step of how you get a car loan, from initial credit checks to driving off the lot with confidence. We’ll demystify the process, offer expert insights, and arm you with the knowledge to secure favorable terms, even if your credit isn’t perfect.

How Do You Get a Car Loan: Your Ultimate Step-by-Step Guide to Approval & Great Rates

Understanding the Car Loan Landscape: Your Foundation for Success

Before diving into applications and negotiations, it’s crucial to understand the basics of what a car loan entails. A car loan is essentially an installment loan, where a lender provides you with funds to purchase a vehicle, and you agree to repay that amount, plus interest, over a predetermined period. This period, known as the loan term, can range from a few months to several years.

Common mistakes to avoid are rushing into a loan without grasping these fundamental concepts. Many people focus solely on the monthly payment, overlooking the total cost of the loan over its entire term. A lower monthly payment often means a longer loan term and, consequently, more interest paid over time.

Key Terms You Must Know

To truly navigate the car loan process effectively, you need to speak the language. Understanding these key terms will allow you to make informed decisions and compare offers with clarity. Don’t let financial jargon intimidate you; these are the building blocks of your loan agreement.

- Annual Percentage Rate (APR): This is perhaps the most critical term. APR represents the total cost of borrowing money over a year, expressed as a percentage. It includes not only the interest rate but also any additional fees associated with the loan. A lower APR means a cheaper loan.

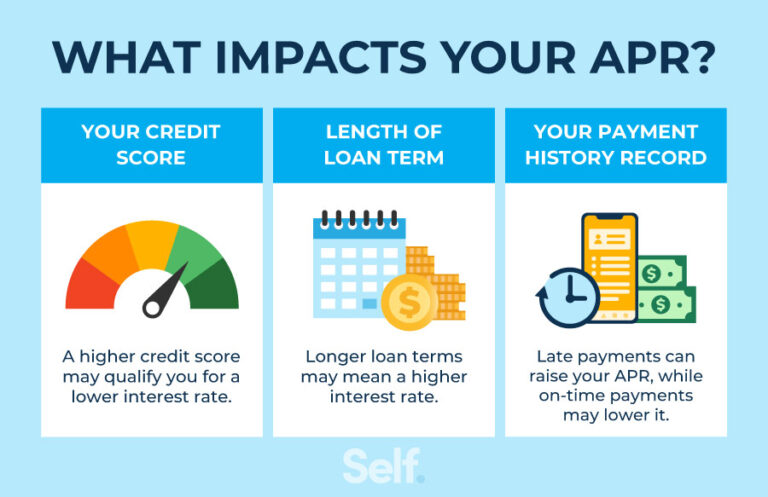

- Loan Term: This refers to the length of time you have to repay the loan, typically expressed in months (e.g., 36, 48, 60, 72, or 84 months). While a longer term can result in lower monthly payments, it almost always means you’ll pay more in total interest over the life of the loan.

- Principal: This is the initial amount of money you borrow to purchase the car. It does not include any interest or fees. As you make payments, a portion goes towards reducing the principal, and another portion covers the interest.

- Interest: This is the cost of borrowing the principal amount, charged by the lender. It’s usually calculated as a percentage of the outstanding principal balance. The interest rate is a component of the APR.

- Down Payment: This is the upfront cash payment you make towards the purchase of the vehicle. A larger down payment reduces the amount you need to borrow, which can lead to lower monthly payments and less interest paid over the loan’s life. It also helps build equity in your car faster.

Pro tips from us: Always focus on the APR when comparing loan offers, as it gives you the most accurate picture of the total cost of borrowing. Understanding these terms will empower you to ask the right questions and spot potentially unfavorable terms.

Phase 1: Pre-Application Preparation – Setting Yourself Up for Success

The most successful car loan applicants are those who do their homework before approaching lenders or dealerships. This preparatory phase is where you build your financial profile, understand your borrowing power, and set realistic expectations. Skipping these steps can lead to higher interest rates, unfavorable terms, or even loan rejection.

Based on my experience, adequate preparation is the single biggest factor in securing a competitive car loan. It gives you leverage and confidence in negotiations.

Check Your Credit Score & Report: Your Financial Report Card

Your credit score is the single most influential factor in determining the interest rate you’ll be offered on a car loan. Lenders use it to assess your creditworthiness – essentially, how likely you are to repay the borrowed money. A higher credit score signals lower risk to lenders, often translating into significantly better interest rates and terms.

Conversely, a lower score indicates higher risk, which means lenders might offer higher rates or stricter conditions. It’s not uncommon for someone with excellent credit to pay thousands less in interest over the life of a loan compared to someone with poor credit, even for the same car.

How to Check Your Credit & What to Look For

You are legally entitled to a free copy of your credit report from each of the three major credit bureaus (Equifax, Experian, and TransUnion) once every 12 months. You can access these reports through AnnualCreditReport.com. Checking your report won’t negatively impact your score.

When you receive your reports, scrutinize them carefully for any inaccuracies or errors. Common mistakes include incorrect addresses, misspelled names, accounts that aren’t yours, or outdated derogatory information. Even small errors can drag down your score. If you find discrepancies, dispute them immediately with the credit bureau and the information provider.

Tips for Improving Your Credit Score

If your credit score isn’t where you’d like it to be, there are steps you can take to improve it, even in the short term. The most impactful actions include paying all your bills on time, every time. Payment history is the largest component of your credit score.

Reducing your credit card balances to lower your credit utilization ratio (the amount of credit you’re using compared to your total available credit) can also provide a boost. Aim to keep this ratio below 30%. Avoid opening new credit accounts right before applying for a car loan, as new inquiries can temporarily lower your score.

Determine Your Budget: Beyond the Monthly Payment

Many prospective car buyers make the mistake of focusing solely on the monthly car payment. However, the true cost of car ownership extends far beyond that single figure. A comprehensive budget will help you understand what you can truly afford, preventing financial strain down the road.

Common mistakes to avoid are underestimating the full cost of car ownership. Remember, the car itself is just one part of the equation.

The True Cost of Car Ownership

When budgeting for a car, you must consider several ongoing expenses. These include auto insurance premiums, which can vary significantly based on the car’s make and model, your driving history, and your location. Fuel costs are another major factor, especially with fluctuating gas prices and varying vehicle fuel efficiencies.

Maintenance and repair costs, registration fees, and potential parking fees should also be factored in. For example, a luxury car might have a manageable monthly payment, but its insurance, premium fuel, and specialized maintenance can quickly become prohibitive. Pro tips from us: Use online calculators to estimate insurance costs for specific vehicles before you commit.

Calculate Your Debt-to-Income (DTI) Ratio

Lenders don’t just look at your credit score; they also assess your ability to repay new debt based on your existing financial obligations. Your debt-to-income (DTI) ratio is a crucial metric here. It’s calculated by dividing your total monthly debt payments (including rent/mortgage, credit card minimums, student loans, etc.) by your gross monthly income.

Most lenders prefer a DTI ratio below 43%, though a lower ratio is always better. A high DTI suggests you might be overextended financially, making you a higher risk. Understanding your DTI helps you gauge how much additional debt you can realistically take on without jeopardizing your financial health.

Save for a Down Payment: The Power of Upfront Cash

Making a significant down payment is one of the smartest financial moves you can make when buying a car. It immediately reduces the amount you need to borrow, which directly translates to lower monthly payments and less interest paid over the life of the loan. A larger down payment also puts you in a stronger equity position from day one.

This means you’re less likely to be "upside down" on your loan (owing more than the car is worth), which can happen quickly due to depreciation. While there’s no magic number, aiming for at least 10-20% of the car’s purchase price is generally recommended. For used cars, a higher percentage might be wise due to faster depreciation.

Phase 2: Exploring Your Financing Options – Where to Get a Loan

Once you’ve prepared your financial profile, the next step in how you get a car loan is to explore where you can actually obtain one. You have several avenues, each with its own advantages and disadvantages. It’s wise to explore multiple options to find the most competitive rates and terms.

Based on my experience, comparing offers from different types of lenders can save you thousands over the life of your loan. Don’t settle for the first offer you receive.

Banks and Credit Unions (Direct Lenders)

Traditional banks and local credit unions are often excellent sources for car loans. These are considered "direct lenders" because you apply for the loan directly with them before you even step foot in a dealership. This approach provides a pre-approval, giving you a clear budget and strong negotiating power at the dealership.

Pros and Cons

Banks typically offer a wide range of loan products and may have competitive rates for well-qualified borrowers. Credit unions, being non-profit organizations, are often known for offering some of the most competitive interest rates and more flexible terms, especially to their members. However, you usually need to be a member to qualify, which might involve opening an account.

The main advantage of direct lenders is transparency; you know exactly what rate you’re getting before you choose a car. The potential downside is that their approval process can sometimes be a bit slower than a dealership’s, and they might have stricter lending criteria compared to some dealership financing options.

Dealership Financing: Convenience at a Cost?

Most car dealerships offer financing options directly on-site. They act as intermediaries, working with a network of banks, credit unions, and captive finance companies (lenders owned by the car manufacturer, like Toyota Financial Services or Ford Credit). This is often presented as a convenient "one-stop shop" solution.

Pros and Cons

The primary advantage of dealership financing is convenience. You can complete the entire car buying and financing process in one location. Dealerships also often have access to special manufacturer incentives, low APR offers, or lease deals that aren’t available through direct lenders. They can be a good option for buyers with excellent credit looking to take advantage of these promotional rates.

However, a common mistake to avoid is letting the dealership dictate your financing. While convenient, dealerships can sometimes mark up the interest rate they offer you from what the lender originally quoted them, adding to their profit. Pro tips from us: Always secure a pre-approval from an outside lender before visiting the dealership. This benchmark empowers you to compare their offer and negotiate effectively.

Online Lenders: Speed and Comparison

The digital age has brought forth a plethora of online lenders specializing in auto loans. These platforms allow you to apply for and often secure a car loan entirely online, from the comfort of your home. Many also offer tools to compare multiple loan offers from different lenders simultaneously.

Pros and Cons

Online lenders are celebrated for their speed and convenience. You can often get pre-approved in minutes, and some platforms allow you to complete the entire loan process digitally. They also make comparison shopping incredibly easy, as many aggregate offers from various lenders, allowing you to quickly find the best rates without multiple applications.

The main drawback might be the lack of personal interaction; if you prefer face-to-face discussions or have complex questions, an online-only process might feel impersonal. However, for tech-savvy borrowers looking for efficiency and competitive rates, online lenders are a strong contender.

Phase 3: The Application Process – What Lenders Look For

Once you’ve decided on your preferred lending avenue, it’s time to understand the application process itself. Knowing what lenders scrutinize will help you present the strongest possible case for approval and favorable terms. This phase is critical to how you get a car loan successfully.

Based on my experience, transparency and accuracy in your application are paramount. Any inconsistencies can raise red flags and delay your approval.

Pre-Approval vs. Full Application: A Crucial Distinction

It’s important to differentiate between pre-approval and a full loan application, as they serve different purposes.

- Pre-Approval: This is typically a soft credit inquiry, meaning it won’t impact your credit score. Lenders use the information you provide (income, existing debts, estimated credit score) to give you an estimate of how much you can borrow and at what interest rate. A pre-approval gives you a solid budget before you shop for a car and significant leverage in negotiations. It’s non-binding and doesn’t obligate you to take the loan.

- Full Application: Once you’ve chosen a specific vehicle, you’ll submit a full application. This involves a hard credit inquiry, which will temporarily ding your credit score by a few points. The lender will review all your detailed financial documents and the specifics of the car you intend to buy (make, model, VIN, purchase price) to finalize the loan offer.

Pro tips from us: Aim to get pre-approved by at least two to three lenders. This allows you to compare actual offers and walk into the dealership with confidence, knowing your financing options.

Key Information Required by Lenders

When you apply for a car loan, lenders will ask for a range of personal and financial information to assess your risk and ability to repay. Having these documents ready beforehand will streamline the process.

- Personal Details: This includes government-issued identification (driver’s license), Social Security number, current and previous addresses, and contact information.

- Employment History and Income Verification: Lenders need to confirm your ability to make payments. Be prepared to provide recent pay stubs (typically for the last 1-3 months), W-2 forms, and potentially tax returns if you are self-employed or have variable income. They will look for stable employment.

- Financial History: This involves providing information about your existing debts (mortgage, student loans, credit cards), bank account statements, and potentially investment account statements. This helps them verify your assets and calculate your debt-to-income ratio.

- Vehicle Information (for full application): Once you’ve picked a car, you’ll need its make, model, year, Vehicle Identification Number (VIN), and the agreed-upon purchase price.

Understanding Lender Criteria: The Factors Behind Approval

Beyond your credit score, lenders evaluate several other factors to determine whether to approve your loan and what terms to offer.

- Debt-to-Income (DTI) Ratio: As discussed, this ratio indicates how much of your gross monthly income goes towards debt payments. Lenders want to ensure you have enough disposable income to comfortably afford the new car payment.

- Payment-to-Income (PTI) Ratio: Similar to DTI, this specifically looks at your projected car loan payment in relation to your gross monthly income. Lenders typically prefer this ratio to be below 10-15%.

- Loan-to-Value (LTV) Ratio: This compares the loan amount to the car’s market value. If you’re borrowing more than the car is worth (e.g., rolling negative equity from a trade-in), it’s a higher risk for the lender. A lower LTV (meaning a larger down payment) is always more attractive.

- Stability: Lenders assess your overall stability through factors like your job history (consistent employment is a plus) and residency history (how long you’ve lived at your current address). Stability suggests reliability.

Phase 4: Securing Your Loan – Navigating Offers and Finalizing

Once you’ve submitted your applications, you’ll start receiving loan offers. This is a critical juncture where smart decision-making can save you thousands. Don’t rush; take the time to compare offers thoroughly. This final stage is crucial to how you get a car loan that truly benefits you.

Common mistakes to avoid are focusing solely on the monthly payment or blindly accepting the first offer presented.

Comparing Loan Offers: Beyond the Monthly Payment

When reviewing loan offers, it’s easy to get swayed by the lowest monthly payment. However, this is often a deceptive metric. A low monthly payment might come with a significantly longer loan term and a higher overall interest cost.

Pro tips from us: Always compare the Annual Percentage Rate (APR), the loan term, and the total cost of the loan (principal + total interest paid). A lower APR and shorter term, even with a slightly higher monthly payment, usually result in substantial savings over the loan’s life. Use a loan calculator to see how different APRs and terms affect the total interest paid.

Negotiating Terms: Your Right as a Borrower

While you might not be able to negotiate your credit score, you can negotiate certain loan terms. If you have multiple pre-approvals, use them as leverage. For example, if Lender A offers you 5.5% APR and Lender B offers 5.7% APR, you can ask Lender B if they can beat Lender A’s offer.

Be wary of dealership add-ons during the financing process. Salespeople may try to include extended warranties, GAP insurance, or other products in your loan. While some of these might be valuable, research them independently and decide if you truly need them. Often, you can purchase them separately for a lower cost, or they might already be covered by your existing insurance.

Reading the Fine Print: No Surprises

Before signing any loan documents, read every single page carefully. Do not feel rushed by the loan officer. Ensure all the terms you agreed upon – the APR, loan term, monthly payment, and total loan amount – are accurately reflected in the contract.

Look for any hidden fees, prepayment penalties (though rare for car loans, it’s worth checking), or late payment clauses. Understanding your obligations and the lender’s policies is crucial to avoid unpleasant surprises later. If anything is unclear, ask for clarification until you fully understand it.

Finalizing the Loan: Drive Away with Confidence

Once you’re satisfied with all the terms and have read the fine print, it’s time to sign. Congratulations! You’ve successfully navigated the car loan process. Make sure you receive copies of all signed documents for your records.

With your financing secured, you can now complete the purchase of your vehicle with peace of mind, knowing you’ve made an informed decision. Remember to keep up with your monthly payments to maintain a good credit history and avoid any late fees or negative marks on your credit report.

What if You Have Bad Credit? (Addressing a Common Concern)

Having less-than-perfect credit doesn’t mean you can’t get a car loan, but it does mean the process might be more challenging and the terms less favorable. Lenders view bad credit as a higher risk, which typically translates to higher interest rates.

Based on my experience, even with bad credit, patience and preparation can significantly improve your chances and the terms you receive. Don’t despair; there are strategies to help.

Expect Higher Interest Rates

The most immediate impact of bad credit is a higher Annual Percentage Rate (APR). Lenders compensate for the increased risk by charging more interest. While someone with excellent credit might get an APR of 3-5%, someone with poor credit could face rates of 10-20% or even higher. This significantly increases the total cost of the loan.

Strategies for Bad Credit Car Loans

- Larger Down Payment: A substantial down payment reduces the amount you need to borrow and lowers the lender’s risk. This can sometimes help you qualify for a better rate or get approved when you otherwise wouldn’t.

- Co-signer: If you have a trusted friend or family member with good credit who is willing to co-sign the loan, it can significantly improve your chances of approval and secure a lower interest rate. A co-signer shares equal responsibility for the loan, so choose wisely.

- Secured Car Loan: Some lenders offer secured car loans where the car itself acts as collateral. While most traditional car loans are secured by the vehicle, some specific "bad credit" lenders might emphasize this aspect or require additional collateral.

- Improve Your Credit First: If possible, taking a few months to focus on improving your credit score before applying can yield substantial long-term savings. Pay down existing debts, pay all bills on time, and dispute any errors on your credit report.

- Be Wary of Predatory Lenders: Unfortunately, some lenders prey on individuals with bad credit, offering extremely high-interest rates or unfavorable terms. Research any lender thoroughly, read reviews, and compare offers before committing. If an offer seems too good to be true, or too bad to be fair, proceed with extreme caution.

Pro tips from us: Even with bad credit, shop around. Don’t just take the first offer you receive. Apply with multiple lenders (within a short window to minimize credit score impact) and compare their rates and terms carefully.

Conclusion: Your Road to Car Loan Success

Getting a car loan doesn’t have to be an intimidating ordeal. By approaching the process with preparation, knowledge, and a strategic mindset, you can navigate the complexities with confidence and secure financing that aligns with your financial goals. From understanding your credit score to meticulously comparing offers, every step contributes to a successful outcome.

Remember, the ultimate goal isn’t just to get a car loan, but to get the right car loan for you – one with favorable terms that won’t strain your budget. By following this comprehensive guide on how do you get a car loan, you’re not just applying for financing; you’re empowering yourself to make smart financial decisions that will benefit you for years to come. Start your journey today, and drive off with the peace of mind you deserve.