How Does Applying For a Car Loan Affect Your Credit Score? Unveiling the True Impact

How Does Applying For a Car Loan Affect Your Credit Score? Unveiling the True Impact Carloan.Guidemechanic.com

Navigating the world of car financing can feel like a complex journey, especially when you consider its ripple effect on your financial health. One of the most common questions prospective car buyers ask is: "How does applying for a car loan affect credit?" It’s a valid concern, as your credit score is a powerful indicator of your financial responsibility and directly impacts the interest rates you qualify for.

Understanding this relationship isn’t just about avoiding a temporary dip; it’s about strategizing for long-term financial growth. This comprehensive guide will peel back the layers, revealing precisely what happens to your credit when you apply for an auto loan, both immediately and over time. We’ll demystify the process, offer expert insights, and equip you with the knowledge to make informed decisions that benefit your credit score.

How Does Applying For a Car Loan Affect Your Credit Score? Unveiling the True Impact

The Initial Credit Check: Hard vs. Soft Inquiries Explained

When you decide to finance a car, the first step an auto lender takes is to check your creditworthiness. This crucial action involves accessing your credit report and score, and it’s where the distinction between "hard" and "soft" inquiries becomes incredibly important. Understanding this difference is fundamental to grasping the immediate impact on your credit.

What is a Credit Inquiry?

A credit inquiry is essentially a request by a lender to view your credit report. This report contains detailed information about your borrowing history, payment patterns, and existing debts. Lenders use this information to assess your risk as a borrower and determine the terms of the loan they might offer you.

Soft Inquiries: No Impact on Your Score

A soft inquiry, sometimes called a "soft pull," occurs when you check your own credit score or when a lender pre-approves you for an offer without you formally applying. These inquiries are often used for promotional purposes or by employers for background checks. The good news is that soft inquiries are only visible to you and do not affect your credit score in any way. They serve as a useful tool for personal monitoring or initial checks.

Based on my experience, many people get nervous when they see a credit check, not realizing that a soft inquiry is harmless. Checking your own score regularly is actually a smart financial habit, and it won’t ever ding your credit.

Hard Inquiries: The Application Trigger

Conversely, a hard inquiry, or "hard pull," happens when you formally apply for a new line of credit, such as a mortgage, a credit card, or, indeed, a car loan. This type of inquiry signifies to credit bureaus that you are actively seeking new credit, which carries a slightly higher risk for lenders. Because of this, hard inquiries are recorded on your credit report and can slightly impact your credit score.

When you sit down at the dealership or apply online for that car loan, you are consenting to a hard inquiry. This is a necessary step for the lender to evaluate your full financial profile and make a lending decision.

Understanding the "Hit": How Hard Inquiries Affect Your Score

The immediate impact of a hard inquiry on your credit score is often a point of anxiety for many applicants. While it’s true that a hard inquiry can cause a temporary dip, the extent of this drop is usually minor and short-lived. It’s crucial to understand how credit scoring models factor this into their calculations.

The "New Credit" Factor

Credit scoring models, like FICO and VantageScore, consider several categories when calculating your score. One of these categories is "New Credit," which typically accounts for about 10% of your FICO score. This factor looks at how many new credit accounts you’ve recently opened and how many inquiries have been made on your report. The logic here is that opening multiple new accounts in a short period can sometimes indicate a higher risk of financial distress.

Each hard inquiry can cause your credit score to drop by a few points, usually between 2 and 5 points. This might seem concerning, but for individuals with a strong credit history, the impact is often negligible and quickly recovers. The inquiry itself typically remains on your credit report for two years, but its influence on your score diminishes significantly after just a few months.

The Rate Shopping Window: A Smart Strategy

Here’s where a common misconception arises and where smart strategy comes into play. Many people worry that applying to multiple lenders for the best car loan rate will lead to numerous hard inquiries, severely damaging their score. Fortunately, credit scoring models are designed to recognize "rate shopping" for the same type of loan.

Pro tips from us: If you apply for several car loans within a concentrated period – typically 14 to 45 days, depending on the scoring model – these inquiries will usually be treated as a single hard inquiry for scoring purposes. This "rate shopping window" allows you to compare offers from various lenders without unfairly penalizing your credit score. It’s a feature specifically designed to encourage consumers to find the best terms for their large purchases.

Therefore, don’t be afraid to shop around for the best interest rate on your car loan. Just ensure you do all your applications within a short timeframe to benefit from this credit scoring allowance. This approach can save you a significant amount of money over the life of the loan.

The Impact of Approval: What Happens After You Get the Loan?

Getting approved for a car loan is a big step, but the credit impact doesn’t end with the inquiry. Once the loan is established, it begins to influence various aspects of your credit profile. This long-term interaction is where the true power of a car loan to build or detract from your credit score lies.

Opening a New Account: Initial Adjustments

When you open a new car loan, it’s reported to the credit bureaus as a new installment account. Initially, this can have a couple of effects:

- Length of Credit History: Your credit score considers the average age of all your credit accounts. Adding a brand new account can slightly decrease this average, especially if you have a long-standing credit history. However, this is usually a minor and temporary effect.

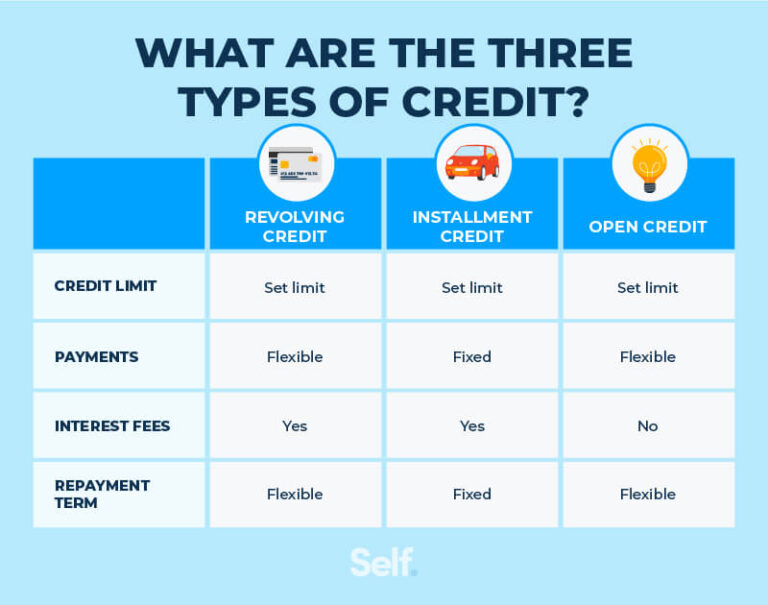

- Credit Mix: Having a diverse mix of credit, including both revolving credit (like credit cards) and installment credit (like car loans or mortgages), is generally seen as positive. A car loan can improve your "credit mix," which accounts for about 10% of your FICO score, demonstrating your ability to manage different types of debt responsibly.

Increased Debt: Amounts Owed

Taking on a car loan means you’re adding a new debt obligation. Your credit score considers the "Amounts Owed" category, which makes up about 30% of your FICO score. While this category often focuses on credit card utilization, an installment loan also adds to your overall debt burden.

It’s important to differentiate between revolving credit utilization (how much of your available credit card limit you’re using) and installment loan debt. Installment loans have a fixed payment schedule and a defined end date, which is viewed differently than high credit card balances. As you pay down your car loan, your outstanding balance decreases, which can positively impact this factor over time.

Debt-to-Income (DTI) Ratio

While not directly a component of your credit score, your debt-to-income (DTI) ratio is crucial for lenders. It compares your total monthly debt payments to your gross monthly income. A new car loan will increase your monthly debt payments, thus impacting your DTI. Lenders often look for a DTI below 36%, though it can vary. A high DTI might make it harder to qualify for future loans, even with a good credit score.

The Long-Term Game: Payment History is King

While the initial effects of a hard inquiry and opening a new account are important, the most significant and lasting impact of a car loan on your credit score comes down to one factor: your payment history. This component is the bedrock of your credit health.

Payment History: 35% of Your FICO Score

"Payment History" is the single most influential factor in your FICO credit score, accounting for a massive 35%. This category tracks whether you pay your bills on time, every time. Consistent, timely payments on your car loan are a powerful way to build and strengthen your credit score. Each on-time payment demonstrates reliability and financial responsibility to lenders.

Think of each monthly payment as a positive report card entry. Over months and years, these consistent on-time payments create a robust track record that significantly boosts your creditworthiness. A well-managed car loan can serve as an excellent credit-building tool, especially for those with a limited credit history.

The Severe Negative Impact of Missed or Late Payments

Conversely, missing payments or making them late can severely damage your credit score. A payment that is 30 days or more past due will be reported to the credit bureaus and can cause a significant drop in your score. The longer the payment is delayed, and the more frequently it happens, the more detrimental the impact.

Common mistakes to avoid are underestimating the severity of late payments. Even one late payment can stay on your credit report for seven years and impact your ability to get favorable rates on future loans, mortgages, or even apartment rentals. Setting up automatic payments or payment reminders is a simple yet effective strategy to ensure you never miss a due date.

Key Factors Your Credit Score Considers (A Deeper Dive)

To truly understand how a car loan application affects your credit, it’s essential to grasp the five main components that credit scoring models use. A car loan touches upon almost all of them.

- Payment History (35%): As discussed, this is paramount. On-time payments on your car loan will significantly bolster this category. Late payments will be detrimental.

- Amounts Owed / Credit Utilization (30%): This looks at how much debt you currently have compared to your available credit. For revolving credit (like credit cards), keeping utilization below 30% is ideal. For installment loans like car loans, the focus is more on the total outstanding balance and whether you are making consistent progress in paying it down. A new car loan increases your overall debt, but as you pay it off, the balance decreases, which is viewed favorably.

- Length of Credit History (15%): This factor considers the age of your oldest account, the age of your newest account, and the average age of all your accounts. Opening a new car loan can slightly lower your average age of accounts initially, but over time, it will contribute positively as it matures.

- New Credit (10%): This category specifically accounts for recent hard inquiries and newly opened accounts. This is where the initial "hit" from applying for a car loan comes into play. However, as noted, the impact is usually minor and fades quickly.

- Credit Mix (10%): Lenders like to see that you can responsibly manage different types of credit. A car loan adds an installment loan to your credit portfolio, which can diversify your credit mix if you previously only had revolving credit (e.g., credit cards). This diversification is often viewed positively.

For more detailed information on how these factors are weighed, you can refer to trusted sources like FICO’s official website: External Link: Understanding Your FICO Score.

Strategic Loan Application: Minimizing Negative Impact and Maximizing Benefits

Applying for a car loan doesn’t have to be a shot in the dark. With a strategic approach, you can minimize any potential negative impact on your credit score while maximizing the benefits of a well-managed loan.

Get Pre-Approved First

One of the smartest moves you can make is to get pre-approved for a car loan before you even set foot in a dealership. Pre-approval involves a soft inquiry, which doesn’t affect your credit score. It gives you a clear idea of how much you can borrow, at what interest rate, and helps you set a realistic budget.

Knowing your pre-approved terms empowers you to negotiate confidently with dealerships. You’ll understand a good offer when you see one, and you won’t be swayed by unfavorable financing options presented at the last minute.

Utilize the Rate Shopping Window Effectively

As discussed, credit scoring models allow for a rate shopping window. Make sure all your formal car loan applications are submitted within a 14-to-45-day period. This ensures that multiple hard inquiries for the same type of loan are grouped and treated as a single inquiry, mitigating the credit score impact.

Don’t rush the decision, but be efficient in gathering your offers. This strategy is key to securing the best possible interest rate without unnecessary credit score damage.

Review Your Credit Report Before Applying

Before you even think about applying for a car loan, pull your own credit report. You’re entitled to a free report from each of the three major credit bureaus (Experian, Equifax, and TransUnion) once a year. Check for any errors, inaccuracies, or signs of identity theft.

Discovering and disputing errors before applying for a loan can prevent them from negatively impacting your eligibility or interest rate. It’s a proactive step that can save you both money and stress. For a deeper dive into this process, read our guide on .

Only Apply When You Are Truly Ready

Resist the urge to apply for a car loan "just to see" if you qualify, especially if you’re not serious about buying a car in the near future. Each hard inquiry, even if minor, has some impact. Save your applications for when you are genuinely prepared to make a purchase. This thoughtful approach preserves your credit profile for when it truly matters.

Don’t Apply for More Than You Need

While a lender might approve you for a higher loan amount than you initially sought, resist the temptation to borrow more than you comfortably need or can afford. A larger loan means higher monthly payments and a greater impact on your debt-to-income ratio. This can strain your budget and potentially make it harder to manage other financial obligations, which could indirectly harm your credit.

Common Myths and Misconceptions About Car Loan Applications and Credit

There are many circulating myths that can cause unnecessary stress or lead to poor financial decisions. Let’s debunk a few.

- Myth 1: "Applying for one car loan will destroy my credit score." As we’ve seen, a single hard inquiry typically results in a minor, temporary dip of a few points, usually recovering within a few months. It’s far from "destroying" your score, especially if your overall credit health is good.

- Myth 2: "Multiple inquiries for different car loans, even within a week, are all separate hits." This is false due to the rate shopping window. Credit scoring models are designed to recognize that consumers shop around for the best rates for the same type of loan. As long as these inquiries occur within the designated timeframe, they are typically grouped and counted as one for scoring purposes.

- Myth 3: "Pre-approval is the same as a full loan application and impacts my credit." Pre-approval generally involves a soft inquiry, which has no effect on your credit score. It’s a preliminary step to give you an estimate, not a final loan offer. A full application is where the hard inquiry comes into play.

Pro Tips for Boosting Your Credit Score While Repaying Your Car Loan

Once you’ve secured your car loan, the journey to improving your credit score is just beginning. Here are some actionable strategies to maximize the positive impact of your new auto financing.

- Make Payments On Time, Every Time: This cannot be stressed enough. Set up automatic payments from your bank account or schedule reminders a few days before the due date. Consistent, on-time payments are the most powerful credit-building tool.

- Keep Other Credit Accounts in Good Standing: Don’t neglect your other credit obligations. Continue to pay your credit card bills, student loans, and any other debts on time. Your overall payment history across all accounts contributes to your score.

- Maintain Low Credit Card Utilization: While your car loan is an installment debt, your credit card utilization (the amount of credit you’re using versus your total available credit) still heavily influences your score. Aim to keep your credit card balances below 30% of your limit, ideally even lower.

- Avoid Opening Too Many New Credit Accounts: Resist the urge to apply for multiple new credit cards or other loans shortly after getting your car loan. Too many new accounts in a short period can signal risk to lenders and may negatively impact your "New Credit" factor.

- Monitor Your Credit Regularly: Keep an eye on your credit report and score. Many credit card companies and banks now offer free access to your credit score. Regularly checking your report for inaccuracies and monitoring your score helps you stay on top of your financial health. Consider using a service that alerts you to significant changes. You can also explore our article on for more advanced tips.

Conclusion: A Strategic Approach to Car Financing and Your Credit

Applying for a car loan is a significant financial decision that undoubtedly impacts your credit, but not always in the ways you might assume. While there’s a temporary, minor dip from the initial hard inquiry, the long-term effects are largely within your control. A car loan, when managed responsibly, can be a powerful tool for building a strong and diverse credit history.

Remember, the key is to be informed and strategic. Understand the difference between hard and soft inquiries, leverage the rate shopping window, and prioritize on-time payments above all else. By approaching the process thoughtfully, you can secure the vehicle you need while simultaneously enhancing your financial standing. The impact of applying for a car loan on credit doesn’t have to be a mystery; with the right knowledge, it can be a stepping stone to greater financial freedom.