How Long Are Car Loans For Used Cars? Navigating Terms, Costs, and Your Financial Future

How Long Are Car Loans For Used Cars? Navigating Terms, Costs, and Your Financial Future Carloan.Guidemechanic.com

Buying a used car is a fantastic way to get reliable transportation without the hefty price tag of a new vehicle. However, for most people, financing is a necessary step. The question that often looms largest is: "How long are car loans for used cars?" This isn’t just a simple query; it’s a gateway to understanding your financial commitment, the total cost of your vehicle, and ultimately, your peace of mind.

As an expert blogger and professional SEO content writer, my goal is to peel back the layers of used car financing. We’ll dive deep into loan terms, interest rates, and the critical factors that should influence your decision. By the end of this comprehensive guide, you’ll be equipped with the knowledge to choose a used car loan that aligns perfectly with your budget and financial goals.

How Long Are Car Loans For Used Cars? Navigating Terms, Costs, and Your Financial Future

The Core Question: What Are Typical Used Car Loan Terms?

When you’re considering how long are car loans for used cars, you’ll find that the landscape is quite varied. Generally speaking, used car loan terms can range anywhere from 24 months to 72 months (two to six years). In some cases, especially for newer used vehicles or those with high resale value, lenders might even offer terms up to 84 months (seven years).

However, just because a term is offered doesn’t mean it’s the right choice for you. The "typical" range often hovers around 48 to 60 months. This duration tends to strike a balance between manageable monthly payments and a reasonable total interest paid. Understanding these common terms is the first step, but the real wisdom comes from knowing what drives these options and which one serves your best interest.

Factors Influencing Your Used Car Loan Term Choice

Choosing the right loan term for your used car isn’t a one-size-fits-all decision. Several crucial factors come into play, each impacting your monthly payments, the total cost of the loan, and your overall financial health. Based on my experience in the automotive and finance sectors, overlooking any of these can lead to significant financial strain down the road.

1. Monthly Payment Affordability

This is often the primary driver for many car buyers. A longer loan term, such as 72 or 84 months, will undoubtedly result in lower monthly payments. This can make a more expensive car seem attainable within your budget.

While lower payments offer immediate relief to your monthly cash flow, it’s essential not to let this be your sole focus. The allure of a smaller payment can mask the true cost of the loan over its entire duration. Always look beyond the monthly figure to understand the bigger picture.

2. Total Cost of the Loan (Interest Paid)

Here’s where the illusion of lower monthly payments can be deceptive. The longer your loan term, the more interest you will pay over the life of the loan. This is a fundamental principle of compound interest.

Even a slightly lower interest rate on a much longer term can lead to paying thousands more in total interest. This significantly inflates the actual price you pay for your used car. Always ask lenders for the total amount you will pay, including all interest, before signing.

3. Vehicle Depreciation

Cars, especially used ones, depreciate in value over time. This is an unavoidable reality. A critical concern with longer loan terms is the risk of "negative equity," also known as being "upside down" on your loan.

Negative equity occurs when you owe more on your car than it’s worth. With a long loan term, particularly for a used car that depreciates faster, you could find yourself in this situation for many years. This makes selling or trading in the car difficult without rolling the negative equity into a new loan, which creates a debt spiral.

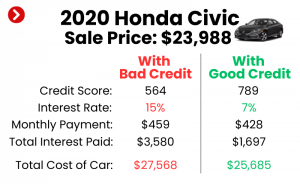

4. Your Credit Score

Your credit score is a major determinant of the interest rate you’ll be offered. A higher credit score typically translates to lower interest rates, making both short and long terms more affordable in terms of total interest.

Conversely, a lower credit score often means higher interest rates. If you have fair or poor credit, a longer term might be necessary to achieve a manageable monthly payment, but it will come at a significantly higher total cost due to the elevated interest rate. – this article provides actionable steps to boost your score before applying.

5. Age and Condition of the Used Car

Lenders consider the age and condition of the used car when approving a loan and determining terms. Older vehicles with higher mileage might be subject to shorter maximum loan terms. This is because lenders want to ensure the car outlasts the loan, reducing their risk.

It’s less likely you’ll find an 84-month loan for a 10-year-old car, for example. The car’s expected lifespan and reliability play a role in the lender’s risk assessment. Always ensure the loan term doesn’t outlive the car’s projected useful life.

6. Down Payment Amount

A substantial down payment can significantly impact your loan term options and overall cost. By putting more money down upfront, you reduce the principal amount you need to borrow.

This not only lowers your monthly payments but can also open up opportunities for shorter loan terms with still-manageable payments. A larger down payment also reduces your risk of negative equity, giving you more financial flexibility.

Pros and Cons of Shorter Loan Terms (e.g., 36-48 months)

Opting for a shorter loan term for your used car comes with a distinct set of advantages and disadvantages. It’s a choice that often appeals to those who prioritize long-term savings and financial freedom over immediate affordability.

The Upsides of a Shorter Term

- Significant Interest Savings: This is the most compelling benefit. By paying off your loan faster, you spend less time accumulating interest charges, leading to substantial savings over the life of the loan. Your total cost for the car will be considerably lower.

- Faster Path to Debt-Free Living: Getting out of car debt quickly provides immense financial freedom. You’ll free up a significant portion of your monthly budget much sooner, allowing you to allocate those funds to other financial goals like saving for a home, investing, or retirement.

- Reduced Risk of Negative Equity: With a shorter loan term, you pay down the principal balance at a much faster rate. This significantly reduces the likelihood of owing more than the car is worth, protecting you from the financial trap of negative equity.

- Less Financial Strain on the Vehicle’s Lifespan: A shorter loan term means you’re less likely to be making payments on a car that’s well past its prime or incurring major repair costs. The loan generally aligns better with the car’s most reliable years.

The Downsides of a Shorter Term

- Higher Monthly Payments: The primary drawback is that shorter terms translate directly to higher monthly payments. This requires a more substantial portion of your monthly income to be dedicated to the car payment.

- Requires a Stronger Budget: To comfortably afford higher monthly payments, you need a robust and well-managed budget. If your income is tight, a shorter term might not be feasible without sacrificing other essential expenses.

Pros and Cons of Longer Loan Terms (e.g., 60-72+ months)

Conversely, longer loan terms are a popular choice for many used car buyers, primarily due to the immediate relief they offer to monthly budgets. However, this convenience often comes at a higher long-term cost.

The Upsides of a Longer Term

- Lower Monthly Payments: This is the undeniable draw of extended loan terms. Spreading the cost over a longer period makes the monthly payment more affordable, potentially allowing you to purchase a more desirable vehicle within your budget.

- Greater Financial Flexibility (in the short term): Lower payments can free up cash flow for other monthly expenses, savings, or investments. This immediate flexibility can be appealing, especially for those with tighter budgets.

The Downsides of a Longer Term

- Significantly More Interest Paid: This is the biggest financial pitfall. As mentioned, the longer your loan term, the more interest accrues. Over 72 or 84 months, you could end up paying thousands more in interest compared to a 48-month loan, making the car much more expensive overall.

- Higher Risk of Negative Equity: Based on my experience, this is one of the most common mistakes people make. With slow principal reduction and ongoing depreciation, you’re highly susceptible to being upside down on your loan for a significant portion of its duration. This creates a challenging situation if you need to sell or trade the car early.

- Extended Debt Period: You’ll be making car payments for a much longer time. This can feel like a financial burden that drags on, limiting your ability to take on new financial commitments or save for future goals.

- Increased Chance of Major Repairs While Still Paying: For a used car, a 7-year loan term means you could be paying for a vehicle that’s 10-12 years old by the time it’s paid off. The likelihood of needing major repairs increases significantly as a car ages, potentially leaving you with both a car payment and hefty repair bills.

Finding the Sweet Spot: How to Determine Your Ideal Loan Length

So, how long are car loans for used cars for you? The key is to find a balance between affordability and financial prudence. It’s about more than just the lowest monthly payment; it’s about the smartest financial decision.

1. Budgeting: What Can You Truly Afford?

Before you even look at cars, sit down and create a realistic budget. Factor in all your income and expenses. Determine how much you can comfortably allocate to a car payment each month without straining other essential areas of your life. This isn’t about what a lender says you can afford, but what your personal finances dictate.

Pro tips from us: Aim for your total car expenses (payment, insurance, fuel, maintenance) to be no more than 10-15% of your take-home pay. This provides a healthy buffer.

2. Understanding the Total Cost: Don’t Just Look at Monthly Payments

Always ask the lender for the total cost of the loan, which includes the principal plus all interest charges. Use online loan calculators to compare different loan terms (e.g., 48, 60, 72 months) for the same car and interest rate. You’ll quickly see how total interest paid escalates with longer terms.

Make an informed decision based on the comprehensive financial picture, not just the monthly installment.

3. Considering the Vehicle’s Lifespan: Matching Loan Term to Expected Ownership

Think about how long you realistically plan to keep the car. If you typically upgrade every 3-5 years, a 72-month loan might not make sense. You could end up trying to sell a car you still owe money on, potentially facing negative equity.

Ideally, your loan term should be shorter than your anticipated ownership period. This ensures you build equity and have options when it’s time to move on.

4. Balancing Payments and Total Cost

The sweet spot often lies where the monthly payment is manageable, but the total interest paid isn’t exorbitant. For many used car buyers, a 48- to 60-month loan term hits this mark. It keeps payments reasonable while avoiding the excessively high interest costs and prolonged debt of much longer terms.

Consider if you can stretch your budget slightly for a shorter term. The extra you pay per month could save you thousands in the long run.

Common Mistakes to Avoid When Financing a Used Car

Based on my experience, many people fall into predictable traps when financing a used car. Being aware of these common mistakes can save you a significant amount of money and stress.

- Focusing Only on Monthly Payments: This is arguably the biggest pitfall. As we’ve discussed, a low monthly payment can be incredibly appealing, but it often disguises a much higher total cost due to extended interest accumulation. Always consider the total amount you’ll pay.

- Not Getting Pre-Approved: Walking into a dealership without a pre-approved loan is like walking in blindfolded. Dealerships often offer financing, but it might not be the best rate you qualify for. Getting pre-approved from banks or credit unions gives you leverage and a benchmark.

- Ignoring the Car’s Age/Mileage: Lenders might offer a long term, but consider if the car is likely to last that long without major, expensive repairs. A 7-year loan on an 8-year-old car means you could be paying for a 15-year-old vehicle that’s constantly breaking down.

- Skipping a Thorough Inspection: Before committing to a loan, have a trusted independent mechanic inspect the used car. An inspection can uncover hidden issues that could lead to costly repairs, making your car loan an even heavier burden.

- Not Understanding All Loan Terms and Fees: Don’t just look at the interest rate. Read the fine print. Are there origination fees, prepayment penalties, or other hidden costs? Ask for a detailed breakdown of all charges.

- Rolling Over Negative Equity: Common mistakes to avoid are rolling over negative equity from a previous car into a new used car loan. This immediately puts you further underwater and creates a vicious cycle of debt. It’s almost always better to address the negative equity directly before buying another vehicle.

The Role of Your Credit Score in Used Car Loans

Your credit score is like your financial report card, and lenders pay close attention to it. A higher credit score signals to lenders that you are a reliable borrower, which translates into more favorable loan terms. This includes lower interest rates and sometimes more flexibility in loan duration.

If your credit score is excellent, you’ll likely qualify for the most competitive rates, making both shorter and longer terms more affordable in terms of total interest. Conversely, a lower credit score will result in higher interest rates, significantly increasing the total cost of your loan regardless of the term. This is why improving your credit score before applying for a loan is one of the most impactful steps you can take.

What if You Need a Longer Term? Strategies to Mitigate Risk

Sometimes, a longer loan term is unavoidable to make a used car payment fit your budget. If you find yourself in this situation, there are strategies you can employ to mitigate some of the associated risks.

- Make a Larger Down Payment: This is the most effective way to reduce the amount you borrow, thereby lowering your monthly payments and interest accrual, even with a longer term. A substantial down payment also reduces your risk of negative equity.

- Consider a Slightly Less Expensive Car: If your budget is stretched, opting for a car that is a few thousand dollars less expensive can make a significant difference in your monthly payment and total interest, allowing for a more comfortable longer term.

- Gap Insurance: If you’re opting for a longer term, especially on a newer used car, consider gap insurance. This covers the "gap" between what you owe on the loan and the car’s actual cash value if it’s totaled or stolen, protecting you from negative equity in catastrophic circumstances.

- Accelerate Payments When Possible: Even if you have a long loan term, you can always pay more than your minimum monthly payment. Even an extra $50 or $100 a month can significantly reduce the principal faster and cut down on total interest paid.

Refinancing Your Used Car Loan

Even after you’ve secured a loan for your used car, your financial journey isn’t necessarily set in stone. Refinancing offers an opportunity to adjust your loan terms, potentially saving you money or making your payments more manageable.

You might consider refinancing if:

- Your Credit Score Has Improved: If you’ve diligently worked on improving your credit since you first got the loan, you might qualify for a lower interest rate.

- Interest Rates Have Dropped: Market interest rates fluctuate. If they’ve decreased since you took out your original loan, refinancing could secure you a better deal.

- You Want to Change Your Loan Term: You could refinance to a shorter term to save on interest or to a longer term to lower your monthly payments if your financial situation has changed.

Always compare the new loan’s interest rate, fees, and total cost against your current loan to ensure refinancing is truly beneficial. for a deeper dive into this valuable option.

For additional unbiased information on managing car loans and consumer debt, I recommend checking resources from the Consumer Financial Protection Bureau (CFPB). They offer excellent guides and tools for making informed financial decisions.

Conclusion: Making an Informed Decision for Your Used Car Loan

Deciding how long your car loan should be for a used car is a pivotal financial choice. It’s not merely about securing the lowest monthly payment, but about understanding the intricate balance between immediate affordability and the long-term cost of borrowing. A shorter loan term offers significant savings on interest and a quicker path to debt freedom, while a longer term provides lower monthly payments at the expense of higher overall costs and extended debt.

By thoroughly evaluating your budget, considering the total cost of the loan, understanding the impact of depreciation, and leveraging your credit score, you can find the "sweet spot" that best serves your financial health. Avoid common pitfalls, like focusing solely on monthly payments, and always prioritize transparency and comprehensive understanding of your loan terms.

Armed with this knowledge, you are now well-equipped to make a smart, informed decision that aligns with your financial goals and ensures your used car ownership experience is as rewarding as possible. Start budgeting today, compare offers diligently, and drive away with confidence!