How Long Are Car Loans Typically? Your Definitive Guide to Smart Financing

How Long Are Car Loans Typically? Your Definitive Guide to Smart Financing Carloan.Guidemechanic.com

Embarking on the journey to buy a new or used car is exciting. The smell of new leather, the promise of open roads – it’s a dream for many. But beneath the shiny exterior and the test drive thrill lies a crucial financial decision: how long are car loans typically, and more importantly, what’s the right loan length for you?

This isn’t just about monthly payments; it’s about the total cost of ownership, your financial flexibility, and even your peace of mind. As an expert in automotive financing, I’ve seen countless individuals navigate this landscape, and understanding loan terms is perhaps the most critical first step. In this comprehensive guide, we’ll dive deep into everything you need to know to make an informed decision, ensuring your car ownership experience is a smooth ride from start to finish.

How Long Are Car Loans Typically? Your Definitive Guide to Smart Financing

Understanding Car Loan Terms: The Basics You Need to Know

Before we explore specific durations, let’s clarify what a "car loan term" actually means. Simply put, the loan term is the duration, usually expressed in months, over which you agree to repay the money you’ve borrowed to purchase a vehicle. This period dictates the number of payments you’ll make and significantly influences both the size of your monthly payment and the total amount of interest you’ll pay over the life of the loan.

Common loan lengths typically range from 36 months (3 years) to 84 months (7 years), though you might occasionally find shorter or longer options. Historically, 48-month and 60-month loans were considered standard. However, the automotive landscape has evolved, and with it, the average car loan term has shifted considerably.

The Shifting Sands of Average Car Loan Terms

Based on my experience and industry trends, the average car loan term has been steadily increasing over the past decade. What was once considered a long loan, like 72 months, has become increasingly common, with 84-month loans also gaining traction. This shift is primarily driven by rising vehicle prices. As cars become more expensive, consumers seek ways to keep their monthly payments manageable. Stretching out the loan term achieves this by spreading the total cost over a longer period, resulting in lower individual payments.

For instance, recent data often shows the average new car loan term hovering around 69-72 months, with used car loans not far behind. This lengthening trend has significant implications for car buyers, which we’ll explore in detail.

The Evolution of Car Loan Lengths: Why Are They Getting Longer?

The question of how long are car loans typically isn’t static; it’s a dynamic reflection of economic realities and consumer behavior. The consistent increase in average car loan terms isn’t a coincidence; it’s a response to several powerful market forces.

Firstly, the price of new vehicles has surged dramatically. Advanced technology, safety features, and consumer demand for larger, more equipped cars have driven up sticker prices. Faced with these higher price tags, many buyers find that a traditional 36 or 48-month loan results in an uncomfortably high monthly payment that strains their budget.

Secondly, lenders have become more flexible in offering extended terms. While this might seem beneficial on the surface, it also means they collect more interest over a longer period, which is profitable for them. This combination of higher car prices and readily available longer terms has fundamentally reshaped what is considered "typical" in the auto loan market.

Pros and Cons of Different Car Loan Lengths

Choosing your car loan length is a balancing act between your monthly budget and the total cost of ownership. Each option comes with its own set of advantages and disadvantages. Let’s break them down.

Short-Term Loans (e.g., 36-48 Months)

These loans are the fastest way to pay off your vehicle. They typically involve a higher monthly payment but significantly reduce the total interest paid.

Pros:

- Lower Total Interest Paid: This is the most significant advantage. Because you’re borrowing money for a shorter duration, the interest accrues for less time, saving you hundreds or even thousands of dollars over the life of the loan.

- Faster Equity Build-Up: You gain ownership of your car more quickly. This means you’ll reach a point where you owe less than the car is worth much sooner, avoiding negative equity.

- Quicker Debt Freedom: You’ll be free from car payments sooner, opening up your budget for other financial goals like saving, investing, or paying off other debts.

- Lower Risk of Negative Equity: With a faster payment schedule, your principal balance drops more rapidly than the car depreciates, greatly reducing your chances of being "upside down" on your loan.

Cons:

- Higher Monthly Payments: This is the primary hurdle for many. The larger monthly obligation can strain budgets, especially for more expensive vehicles.

- Potentially Harder to Qualify: Lenders might require a stronger credit score or a larger down payment to approve a shorter-term loan with higher payments, as it represents a higher risk if the borrower defaults.

Who it’s for: Short-term loans are ideal for buyers with stable incomes, strong credit, and enough financial breathing room to comfortably handle higher monthly payments. They prioritize saving on interest and achieving debt freedom quickly.

Medium-Term Loans (e.g., 60-72 Months)

These represent the most common loan lengths in today’s market. They offer a compromise between monthly affordability and total interest paid.

Pros:

- Balanced Monthly Payments: Compared to short-term loans, the monthly payments are more manageable, making them accessible to a broader range of buyers.

- Still Manageable Interest: While you’ll pay more interest than with a 36 or 48-month loan, it’s generally not as drastic as with very long-term options.

- Wider Availability: Most lenders readily offer these terms, and they align with what many consumers are looking for in terms of affordability.

Cons:

- More Interest Than Short-Term: You’ll still end up paying significantly more in interest compared to shorter terms.

- Slower Equity Build-Up: It takes longer to build equity, increasing the risk of being upside down in the early years of the loan, especially with rapid depreciation.

- Potential for Overlap with Maintenance: As your car ages, it might start requiring more maintenance or repairs while you’re still making payments.

Who it’s for: Medium-term loans suit buyers who need a balance between affordable monthly payments and a reasonable total cost. They are a popular choice for those looking for a new car without breaking the bank on monthly outgoings, but who are still conscious of the overall financial impact.

Long-Term Loans (e.g., 72-84+ Months)

These extended loan terms have become increasingly prevalent, particularly for new and higher-priced vehicles. They offer the lowest monthly payments but come with significant financial drawbacks.

Pros:

- Lowest Monthly Payments: This is their main appeal. By stretching payments over many years, long-term loans make even expensive vehicles seem affordable on a monthly basis.

- Greater Affordability for Expensive Cars: They open up the market for premium vehicles to buyers who might not otherwise be able to afford the monthly payments on shorter terms.

Cons:

- Significantly Higher Total Interest: This is the biggest drawback. Over 7 or 8 years, the interest accumulates substantially, making the car much more expensive in the long run. Common mistakes to avoid are focusing solely on the monthly payment without considering the total amount you’ll pay back.

- Prolonged Debt: You’ll be in debt for a much longer period, potentially tying up your financial resources for nearly a decade. This can impact your ability to save for other goals or take on new debt.

- High Risk of Negative Equity (Upside Down): With a long loan, your car often depreciates faster than you pay off the principal. This means you could owe more on the car than it’s worth for a significant portion of the loan term, making it difficult to sell or trade in without losing money.

- Higher Insurance Costs Over Time: If you’re upside down, you’ll likely need gap insurance, and your full coverage insurance will be necessary for longer, potentially increasing your overall ownership costs.

- Car Outlives Warranty: The car’s factory warranty often expires long before your loan term ends, leaving you responsible for costly repairs while still making payments.

Who it’s for: Long-term loans are generally suitable only for buyers who absolutely need the lowest possible monthly payment to afford a necessary vehicle, and who are willing to accept the increased total cost and risks. Pro tips from us: If you must take a long-term loan, aim for a significant down payment to mitigate negative equity risk, and consider paying extra on the principal whenever possible.

Key Factors Influencing Your Ideal Car Loan Length

Choosing the right car loan length isn’t a one-size-fits-all decision. Several personal and financial factors should guide your choice.

1. Monthly Budget: How Much Can You Truly Afford?

This is the most immediate concern for many. Be honest about your financial limits. Don’t just consider the car payment, but factor in insurance, fuel, maintenance, and potential repairs. A car payment should ideally not exceed 10-15% of your take-home pay. Overstretching your budget for a lower monthly payment on a long-term loan can lead to financial stress down the road.

2. Interest Rate: How Does it Change with Loan Length?

Interest rates often vary with the loan term. Shorter loans typically come with lower interest rates because the lender’s risk is reduced. Longer loans, conversely, often carry higher interest rates to compensate the lender for the extended period of risk. A seemingly small difference in interest rate can add up to hundreds or thousands of dollars over several years.

3. Total Cost of Ownership: Don’t Just Look at Monthly Payment

This is perhaps the most crucial point. Always calculate the total amount you’ll pay over the life of the loan, including all interest. A lower monthly payment might feel good, but if it means paying significantly more overall, it might not be the smartest financial move. Use online calculators to compare different scenarios.

4. Down Payment: Impact on Loan Amount and Term

A larger down payment reduces the principal amount you need to borrow. This can enable you to choose a shorter loan term with manageable monthly payments, or keep payments low on a medium-term loan while significantly reducing interest paid. Based on my experience, a substantial down payment is one of the best ways to protect yourself from negative equity, regardless of loan length.

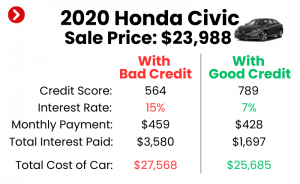

5. Credit Score: Better Scores Unlock Better Terms

Your credit score plays a huge role in the interest rate you’ll qualify for. Borrowers with excellent credit (typically 720+) will get the best rates, making shorter loans even more attractive. If your credit score is lower, you might be offered higher rates, which makes any loan, especially a long one, much more expensive. Focus on improving your credit before applying for a loan if possible.

6. Vehicle Depreciation: Crucial for Avoiding Negative Equity

Cars lose value rapidly, especially in the first few years. Understanding depreciation is key to avoiding negative equity. If your loan term is too long and your payments are too low, your car’s value can drop faster than you pay off the loan, leaving you owing more than it’s worth. This is particularly relevant for new cars, which can lose 20-30% of their value in the first year alone.

7. Your Financial Goals: Quicker Debt-Free vs. Lower Monthly Burden

Consider your broader financial aspirations. Do you want to be debt-free quickly so you can save for a down payment on a house, invest, or start a business? Or is minimizing monthly expenses your top priority right now, even if it means carrying debt longer? Your personal financial philosophy should heavily influence your choice.

The Hidden Dangers of Long Car Loans: A Deep Dive

While extended car loan terms offer the allure of lower monthly payments, they come with significant financial perils that many buyers overlook. How long are car loans typically should also prompt the question: "At what cost?"

1. Negative Equity (Being Upside Down)

This is arguably the most significant danger. Negative equity, often called being "upside down" or "underwater," means you owe more on your car than it’s currently worth. This is common with long-term loans because the car depreciates quickly, especially in the early years, while your principal balance decreases slowly due to smaller monthly payments and more interest being paid upfront.

If your car is totaled or stolen while you’re upside down, your insurance payout might not cover the full amount you owe, leaving you to pay the difference out of pocket. Similarly, if you need to sell or trade in your car before the loan is paid off, you’ll have to come up with the cash to cover the negative equity or roll it into your next loan – a cycle that can be financially crippling.

2. Increased Total Interest Paid

This is a straightforward, yet often underestimated, consequence. The longer you borrow money, the more interest the lender charges. Even a seemingly small increase in the loan term can result in thousands of extra dollars paid over time. For example, a $30,000 loan at 5% interest over 60 months might cost you around $3,900 in interest. Stretch that to 84 months, and your total interest could jump to over $5,500 – an extra $1,600 for the same car.

3. Prolonged Debt and Financial Restriction

A long car loan means you’re tied to that debt for many years. This can restrict your financial flexibility, limiting your ability to save for retirement, make a down payment on a home, or respond to unexpected financial emergencies. It also impacts your debt-to-income ratio, potentially affecting your ability to qualify for other loans (like a mortgage) in the future.

4. Car Outlives Its Warranty While Still Being Paid Off

Many new car warranties last for 3-5 years. If you have a 7-year loan, your car could be out of warranty for several years while you’re still making payments. This means you’ll be responsible for any major repairs, which can be expensive, on a vehicle you don’t fully own yet. This scenario is a classic example of when car ownership becomes a financial burden rather than a convenience.

Pro tips from us to mitigate these risks:

- Make a substantial down payment: This immediately reduces the principal and helps you build equity faster.

- Consider gap insurance: If you take a long-term loan, gap insurance can protect you in case of a total loss by covering the difference between what you owe and what the car is worth.

- Pay extra whenever possible: Even small additional payments towards the principal can significantly reduce the total interest paid and shorten the loan term.

How to Choose the Right Car Loan Length for YOU

Making an informed decision about your car loan length requires careful consideration of your personal finances and priorities. Here’s a step-by-step approach:

- Assess Your True Monthly Budget: Don’t just think about what you can pay, but what you should pay without feeling financially strained. Create a detailed budget that includes all your income and expenses.

- Calculate the Total Cost, Not Just Monthly Payments: Use online loan calculators to compare different loan terms (e.g., 48, 60, 72 months) for the same vehicle price and interest rate. Focus on the "total amount paid" column.

- Consider the Car’s Reliability and Your Ownership Plans: If you’re buying a highly reliable car that you plan to keep for 10+ years, a longer loan might be slightly less risky than if you’re buying a less dependable model or planning to trade it in after 3-5 years.

- Get Pre-Approved: Before you even step into a dealership, get pre-approved for a loan from your bank or credit union. This gives you a benchmark rate and terms, empowering you to negotiate more effectively.

- Don’t Be Afraid to Walk Away: If the numbers don’t work for you, or if a particular loan term feels too risky, be prepared to walk away. There will always be another car or another deal.

Pro tips from us: Never tell a salesperson what monthly payment you want. Instead, negotiate the total vehicle price first, then discuss the financing options. This prevents them from "packing" the loan with extras or stretching the term unnecessarily to meet your desired payment.

Beyond the Standard: Refinancing and Early Payoff

Your car loan journey doesn’t necessarily end the day you sign the papers. Life changes, and so can your financial situation, opening up opportunities to adjust your loan.

When Refinancing Makes Sense

Refinancing means taking out a new loan to pay off your existing car loan. It can be a smart move in several situations:

- Lower Interest Rates: If interest rates have dropped since you took out your original loan, or if your credit score has significantly improved, you might qualify for a lower rate, saving you money.

- Change in Financial Situation: If you’ve received a raise or your budget has more room, you might refinance to a shorter term to pay off the car faster and save on interest. Conversely, if you’re facing financial hardship, you might extend the loan term to lower monthly payments, though this will cost you more in the long run.

- Remove a Co-signer: If you initially needed a co-signer but now have a strong credit history, refinancing can allow you to remove them from the loan.

Benefits of Paying Off Early

If you have extra cash, paying off your car loan early can be incredibly beneficial:

- Save on Interest: Every extra dollar you pay towards the principal reduces the amount of interest you’ll owe.

- Achieve Debt Freedom Sooner: Being free from car payments frees up your budget and reduces financial stress.

- Full Ownership: You own the car outright, giving you complete control and the ability to sell or trade it without any loan complications.

Consider prepayment penalties: Before making extra payments or refinancing, check your original loan agreement for any prepayment penalties. While less common with auto loans than mortgages, some lenders might charge a fee for paying off the loan ahead of schedule.

Expert Advice & Common Mistakes to Avoid

Navigating the world of car loans can be tricky, but with the right knowledge, you can make choices that benefit your financial health. Here’s some final expert advice and a recap of pitfalls to sidestep.

Based on my experience coaching countless buyers, the biggest mistake people make is falling in love with a car before securing their financing. This emotional attachment can lead to poor financial decisions. Always research, get pre-approved, and understand your budget before you step onto the dealership lot.

Common Mistakes to Avoid Are:

- Focusing Only on the Monthly Payment: This is the golden rule of car buying. A low monthly payment can hide a very expensive loan stretched over an excessive term. Always look at the total cost of the vehicle.

- Not Getting Pre-Approved: Walking into a dealership without pre-approval is like walking into a negotiation blindfolded. You lose your leverage and may accept whatever financing the dealer offers, which might not be the best rate.

- Ignoring Your Credit Score: Your credit score is your financial passport. A low score means higher interest rates. Take steps to improve it before applying for a loan.

- Forgetting About Additional Costs: Beyond the loan payment, factor in insurance, registration, taxes, fuel, and maintenance. These can significantly impact your overall budget.

- Rolling Negative Equity into a New Loan: If you’re upside down on your current car, rolling that negative balance into a new loan is a dangerous cycle that deepens your debt and makes it harder to get ahead. Try to pay off the negative equity separately if possible.

- Not Reading the Fine Print: Always read your loan agreement thoroughly. Understand the interest rate, term, any fees, and prepayment penalties. Don’t be afraid to ask questions.

For more in-depth information on managing your auto loan, consider exploring resources from trusted financial institutions or consumer protection agencies. . You might also find our articles on and helpful for making an even more informed decision.

Conclusion

The question of how long are car loans typically is not just about a number; it’s about making a financially sound decision that aligns with your personal goals and budget. While average loan terms have stretched longer due to rising vehicle prices, it’s crucial to understand the implications of these extended durations. Short-term loans save you money on interest and get you to debt freedom faster, albeit with higher monthly payments. Long-term loans offer lower monthly payments but come with the significant risks of increased total interest, prolonged debt, and negative equity.

By understanding the pros and cons, evaluating your own financial situation, and avoiding common pitfalls, you can choose a car loan length that truly benefits you. Remember, a car is a tool for transportation, not a financial burden. Make smart choices today for a smoother financial journey tomorrow.