How Long Can I Get A Used Car Loan For? Your Ultimate Guide to Smart Financing

How Long Can I Get A Used Car Loan For? Your Ultimate Guide to Smart Financing Carloan.Guidemechanic.com

Securing a used car loan is a significant financial decision, and one of the most common questions people ask is: "How long can I get a used car loan for?" This isn’t just about monthly payments; it delves into your long-term financial health, the total cost of your vehicle, and even the equity you build.

As an expert blogger and someone deeply immersed in auto financing, I’ve seen countless scenarios. Understanding the nuances of loan terms can save you thousands of dollars and prevent future headaches. This comprehensive guide will break down everything you need to know, helping you make an informed choice that truly benefits you.

How Long Can I Get A Used Car Loan For? Your Ultimate Guide to Smart Financing

The Core Question: What’s the Average Used Car Loan Term?

When you’re looking to finance a used car, the loan terms can vary widely. Unlike new cars, which often see terms stretching up to 84 months (7 years), used car loans typically have slightly shorter maximums.

Based on my experience and industry data, the most common used car loan terms range from 36 to 72 months (3 to 6 years). While 60 months (5 years) is a very popular choice, some lenders might offer terms up to 84 months for newer, low-mileage used vehicles. However, these extended terms come with their own set of considerations.

The "right" term for you isn’t universal. It depends heavily on several interconnected factors. Let’s dive into what truly influences how long you can finance that used car.

Decoding the Factors That Influence Your Loan Term

Lenders assess risk when approving a loan. The longer the loan term, the more risk they perceive. Consequently, several elements play a crucial role in determining the maximum loan length you qualify for and the interest rate you’ll receive.

Your Credit Score: The Ultimate Game Changer

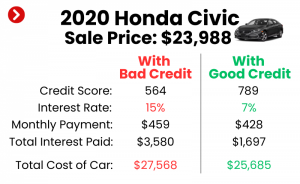

Your credit score is arguably the most significant factor in auto loan approvals. A higher credit score (generally 670 and above) signals to lenders that you are a responsible borrower.

With excellent credit, you’re more likely to qualify for longer loan terms and, crucially, lower interest rates. Lenders feel more confident that you’ll repay the loan, even over an extended period. Conversely, a lower credit score might limit you to shorter terms and higher interest rates, reflecting the increased risk.

The Car’s Age and Mileage: Lenders’ Risk Assessment

The vehicle itself is collateral for the loan, so its condition and longevity matter to lenders. Older cars with high mileage represent a higher risk. They are more prone to mechanical issues, which could lead to missed payments if you face unexpected repair costs.

Because of this, lenders typically impose shorter maximum loan terms on older or higher-mileage used cars. A car that’s five years old might have a maximum term of 60 months, while a seven-year-old car might be capped at 48 months. This protects the lender by ensuring the car’s value doesn’t depreciate faster than you pay off the loan, especially if it becomes unreliable.

Your Down Payment: Showing Commitment

Making a substantial down payment can significantly impact your loan term options and interest rates. A larger down payment reduces the amount you need to borrow, thereby lowering the lender’s risk.

When you put more money down, you demonstrate your commitment to the purchase. This can make lenders more flexible with loan terms, potentially offering you longer options or better rates. It also helps you avoid being "upside down" on your loan, where you owe more than the car is worth.

Interest Rates: The Cost of Borrowing

While not directly dictating the length of your loan, interest rates are intertwined with loan terms. Generally, longer loan terms come with slightly higher interest rates. This is because lenders are taking on more risk over an extended period.

A small difference in the interest rate can lead to a significant difference in the total amount you pay over the life of the loan. Always consider the Annual Percentage Rate (APR), which includes the interest rate plus any fees, to understand the true cost of borrowing.

Lender Type: Banks, Credit Unions, Dealerships

Different types of lenders have varying appetites for risk and different product offerings.

- Banks often have competitive rates for well-qualified borrowers but might be stricter on car age/mileage limits.

- Credit unions are known for their customer-centric approach and can sometimes offer more flexible terms or better rates, especially for members.

- Dealerships often work with multiple lenders, offering convenience, but their rates might not always be the absolute best. They sometimes push longer terms to make monthly payments seem more affordable.

Shopping around is a pro tip from us. Don’t just take the first offer; compare options from at least three different lenders.

Debt-to-Income Ratio: Your Financial Capacity

Your debt-to-income (DTI) ratio is another critical metric lenders consider. This ratio compares your total monthly debt payments to your gross monthly income. A lower DTI indicates that you have more disposable income to manage new debt.

If your DTI is high, a lender might approve you for a shorter loan term to ensure your monthly payments remain manageable. This reduces their risk of default. It’s all about demonstrating your ability to comfortably afford the loan.

The Great Debate: Short vs. Long Loan Terms

Choosing between a shorter and a longer loan term is a balancing act between immediate affordability and long-term cost. Both have distinct advantages and disadvantages.

The Allure of Shorter Terms (e.g., 36-48 Months)

Shorter loan terms, typically 3 to 4 years, are often the financially savvy choice if your budget allows for higher monthly payments.

-

Pros:

- Less Total Interest Paid: This is the biggest benefit. The quicker you pay off the loan, the less interest accrues over time. You save a significant amount of money in the long run.

- Quicker Ownership: You’ll own your car outright sooner, freeing up your budget for other financial goals.

- Build Equity Faster: You’ll build equity in your vehicle more rapidly, reducing the risk of negative equity (owing more than the car is worth).

- Less Risk of Mechanical Issues While Still Paying: You’re less likely to be making payments on a car that’s constantly in the shop because you’ll pay it off before it hits peak maintenance years.

-

Cons:

- Higher Monthly Payments: This is the trade-off. Your budget needs to comfortably accommodate the larger payment.

- Less Financial Flexibility: Higher payments can strain your monthly cash flow, leaving less room for unexpected expenses or savings.

The Appeal of Longer Terms (e.g., 60-72+ Months)

Longer loan terms, spanning 5 years or more, are popular because they make monthly payments more affordable. This can be very tempting, but it comes with significant caveats.

-

Pros:

- Lower Monthly Payments: The primary draw is the reduced monthly financial burden, making a more expensive car seem attainable.

- More Budget Flexibility: Lower payments leave more room in your budget for other expenses or savings, which can be crucial for some.

-

Cons:

- More Total Interest Paid: This is the most critical downside. Over a longer period, even with a slightly lower interest rate, you’ll pay substantially more in interest.

- Higher Risk of Negative Equity: Cars depreciate, especially used ones. With a longer loan, you’re more likely to owe more than the car is worth for a significant portion of the loan term. This is a common mistake to avoid.

- Longer Debt Period: You’ll be making car payments for a longer time, delaying financial freedom from that particular debt.

- Increased Risk of Mechanical Issues: As mentioned, the car will be older when you finish paying for it, increasing the chances you’ll be making payments and paying for major repairs simultaneously.

Pro Tip from us: While longer terms offer lower payments, the "sweet spot" for most used car loans, especially for vehicles a few years old, is often between 48 to 60 months. This range balances manageable monthly payments with a reasonable total cost of interest and reduces the risk of negative equity.

Finding Your Ideal Used Car Loan Term: A Strategic Approach

Choosing the right loan term requires careful consideration and a strategic approach. It’s not just about what you can afford, but what makes the most financial sense for your situation.

Assess Your Budget Realistically

Before you even start looking at cars, understand your true monthly budget. Factor in not just the car payment, but also insurance, fuel, and estimated maintenance costs.

Don’t stretch yourself too thin for a lower monthly payment on a longer term. A comfortable payment means you can handle it even if unexpected expenses arise.

Boost Your Credit Score

Improving your credit score before applying for a loan is one of the most impactful steps you can take. A better score unlocks lower interest rates and more flexible terms.

- Pay bills on time.

- Reduce existing debt.

- Check your credit report for errors.

We have an in-depth article on How to Improve Your Credit Score for a Car Loan that provides actionable steps if you need more guidance. (Internal Link)

Save for a Substantial Down Payment

Aim for at least a 10-20% down payment on a used car. This immediately reduces the loan amount, lowers your monthly payments, and mitigates the risk of negative equity.

A strong down payment also signals to lenders that you are a serious and responsible buyer, potentially leading to better loan offers.

Shop Around for Lenders (Don’t Settle!)

Never take the first loan offer you receive, especially from a dealership. Get pre-approved by several banks and credit unions before you even step onto a dealership lot.

Comparing pre-approvals allows you to negotiate with confidence and ensures you secure the best possible rates and terms for your financial profile. This comparison can highlight how different lenders approach loan terms.

Understand the Total Cost of the Loan

Focusing solely on the monthly payment is a common mistake. Always ask for the total cost of the loan, which includes the principal borrowed plus all interest paid over the term.

A lower monthly payment over a longer term almost always means a higher total cost. Use online loan calculators to see how different terms and interest rates impact both your monthly payment and the total interest paid.

Common Mistakes to Avoid When Choosing a Loan Term

Based on my experience, many people fall into similar traps when financing a used car. Being aware of these can save you a lot of grief.

- Focusing Only on the Monthly Payment: This is the biggest pitfall. A low monthly payment on an 84-month loan might look appealing, but it often means you’re paying significantly more in total interest. Always consider the big picture.

- Ignoring the Car’s Depreciation: Used cars continue to depreciate. If your loan term is too long, you risk being "upside down" on your loan, meaning you owe more than the car is worth. This can be a huge problem if you need to sell the car or if it gets totaled.

- Not Getting Pre-Approved: Walking into a dealership without a pre-approval from your bank or credit union puts you at a disadvantage. You won’t know if the dealer’s financing offer is truly competitive.

- Falling for Extended Warranty Bundles on Long Terms: While extended warranties can be useful, avoid bundling them into a very long loan term. You’ll end up paying interest on the warranty itself for years, often after the original warranty has expired.

Beyond the Loan Term: Other Critical Considerations

Your loan term decision doesn’t exist in a vacuum. It interacts with other crucial aspects of car ownership.

Depreciation and Negative Equity

As mentioned, cars lose value over time. This is depreciation. Negative equity occurs when the outstanding balance of your loan is greater than the current market value of your car.

Longer loan terms increase the likelihood and duration of negative equity, especially with used cars. If your car is totaled in an accident and you have negative equity, your insurance payout might not cover the full loan balance, leaving you responsible for the difference. Gap insurance can help, but avoiding negative equity in the first place is ideal.

Insurance and Maintenance Costs

Remember that car payments are just one part of the equation. Used cars, by their nature, might require more maintenance than new ones. Factor in potential repair costs, as well as the ongoing expense of car insurance.

A longer loan term might free up monthly cash, but if that cash is then eaten up by unexpected repairs or higher insurance premiums (especially for older vehicles), the "affordability" advantage diminishes quickly. For more insights on overall car costs, consider reading our article on The True Cost of Car Ownership Beyond the Monthly Payment. (Internal Link)

The Option to Refinance

Even if you initially take a longer loan term due to budget constraints, you might have the option to refinance later. If your credit score improves, or interest rates drop, refinancing can allow you to secure a shorter term or a lower interest rate, or both.

This provides a degree of flexibility. However, it’s best to aim for the ideal term from the start to minimize interest paid.

Pro Tips from an Expert: Securing Your Best Used Car Loan

Having guided many through the car buying process, here are my top recommendations for navigating used car loans:

- Prioritize Your Credit: A good credit score is your golden ticket to better terms and rates. Dedicate time to improving it before you apply.

- Save Aggressively for a Down Payment: The more you put down, the less you borrow, the less interest you pay, and the more favorable your loan terms will be.

- Get Multiple Pre-Approvals: This empowers you. It gives you a benchmark for what a fair offer looks like and strengthens your negotiating position at the dealership.

- Balance Monthly Payment with Total Cost: Don’t let a low monthly payment blind you to the total interest you’ll pay over the life of the loan. Use online calculators to compare scenarios.

- Understand the Car’s Value: Research the used car’s market value (e.g., Kelley Blue Book, Edmunds) to ensure you’re not overpaying and that the loan amount aligns with its worth.

- Read the Fine Print: Always review the loan agreement carefully. Understand all fees, the APR, and any prepayment penalties (though these are less common with simple interest auto loans).

For more detailed information on understanding auto loan terms and conditions, a trusted resource like the Consumer Financial Protection Bureau (CFPB) offers excellent, unbiased guidance: Understanding Vehicle Financing. (External Link)

Conclusion: Making an Informed Decision

"How long can I get a used car loan for?" is a question with a multi-faceted answer. While typical terms range from 36 to 72 months, the ideal length for you depends on your unique financial situation, the car’s characteristics, and your personal comfort with debt.

My ultimate advice is to approach used car financing with knowledge and strategy. Don’t rush the decision. Prioritize a loan term that minimizes total interest paid while still offering a comfortably affordable monthly payment. By focusing on your credit, making a strong down payment, and shopping around, you can secure a used car loan that serves your best interests, helping you drive away happy and financially sound.