How Long Does It Really Take to Pay Off a Car Loan? Your Ultimate Guide to Financial Freedom

How Long Does It Really Take to Pay Off a Car Loan? Your Ultimate Guide to Financial Freedom Carloan.Guidemechanic.com

The open road beckons, and a new car often feels like the key to unlocking it. But lurking beneath the shiny paint and new car smell is often a multi-year commitment: your car loan. For many, the question isn’t just "Can I afford the monthly payment?" but rather, "How long to pay off car loan and truly own my vehicle?" This isn’t just a simple math problem; it’s a journey influenced by numerous factors and offering multiple paths to financial freedom.

Understanding your car loan payoff time is crucial for sound financial planning. It impacts everything from your budget flexibility to your overall debt burden. In this comprehensive guide, we’ll dive deep into the mechanics of car loans, explore strategies for faster repayment, and equip you with the knowledge to make informed decisions about your automotive financing. Let’s navigate the road to debt-free driving together.

How Long Does It Really Take to Pay Off a Car Loan? Your Ultimate Guide to Financial Freedom

The Core Factors Influencing Your Car Loan Payoff Time

The duration of your car loan isn’t a mystery; it’s a direct result of several key variables. To truly understand how long it will take to pay off your car loan, you need to dissect these components. Each plays a significant role in shaping your repayment schedule and the total amount you’ll ultimately spend.

1. The Loan Term (Duration)

The loan term is perhaps the most obvious and direct factor. This is the agreed-upon period, in months, over which you’re expected to repay the loan. Common terms range from 36 months (3 years) to 84 months (7 years), with 60 and 72 months being very popular.

A shorter loan term, like 36 or 48 months, means you’ll pay off the car loan much faster. While your monthly payments will be higher, you’ll significantly reduce the total interest paid over the life of the loan. This accelerates your journey to full ownership.

Conversely, opting for a longer loan term, such as 72 or 84 months, stretches out your payments. This results in lower monthly installments, making the car seem more affordable upfront. However, the trade-off is a much longer period of debt and a substantially higher amount of interest paid over time.

2. The Interest Rate (APR)

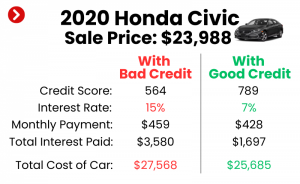

Your Annual Percentage Rate (APR) is the cost of borrowing money, expressed as a yearly percentage. It’s a critical factor that often gets underestimated. A higher interest rate means a larger portion of your monthly payment goes towards interest, especially in the early stages of the loan.

Even a difference of a few percentage points can dramatically alter your total payoff time and the overall cost of your car. A lower APR, secured through good credit or savvy negotiation, means more of your payment attacks the principal balance directly. This accelerates the payoff process without you necessarily increasing your monthly payment.

Based on my experience, many car buyers focus almost exclusively on the monthly payment without fully grasping the long-term impact of the interest rate. Always shop around for the best APR, as it’s one of your most powerful tools.

3. The Principal Amount Borrowed

This is the initial amount of money you borrowed to purchase the car, minus any down payment. Naturally, the larger the principal amount, the longer it will take to pay off, assuming all other factors remain constant. A higher principal means more money needs to be repaid, which will either require larger monthly payments or a longer loan term.

Reducing the principal amount from the outset is a powerful strategy. This can be achieved through a substantial down payment or by choosing a less expensive vehicle. Every dollar you don’t borrow is a dollar you won’t pay interest on.

4. Your Down Payment

A down payment is the initial sum of money you pay towards the car’s purchase price. This reduces the amount you need to borrow, directly impacting your principal. A larger down payment immediately shrinks the loan amount.

By lowering the principal, a significant down payment not only reduces your monthly payments but also cuts down the total interest you’ll pay. This can significantly shorten your effective car loan payoff time, as you’re starting with a smaller debt burden from day one. It’s a foundational step towards quicker financial freedom.

5. Your Monthly Payment Amount

This is the most tangible factor for most people. The size of your monthly payment directly dictates how quickly you chip away at the principal and interest. If you only pay the minimum required amount, your loan will last for the full agreed-upon term.

However, any amount you pay above the minimum accelerates your payoff schedule. Even small, consistent extra payments can shave months, or even years, off your car loan. This is where personal financial discipline truly shines.

6. Payment Frequency

While less common for car loans than mortgages, some lenders might offer bi-weekly payment options. Instead of one payment per month, you make half a payment every two weeks. This results in 26 half-payments per year, which equates to 13 full monthly payments instead of 12.

This extra payment directly reduces your principal, effectively shortening your loan term and saving you interest. It’s a subtle but effective strategy to pay off car loan faster without feeling a significant pinch in your budget each month.

The Pros and Cons of Different Loan Terms

Choosing the right car loan term is a critical decision that balances immediate affordability with long-term financial health. There’s no universally "best" option; it depends entirely on your personal financial situation and goals. Let’s explore the implications of common loan durations.

Short Loan Terms (e.g., 36-48 months)

Opting for a shorter loan term means you’re committing to a quicker path to ownership. These terms typically range from three to four years, making them ideal for those who prioritize rapid debt elimination.

Pros:

- Lower Total Interest Paid: This is the biggest advantage. Because you’re borrowing for a shorter period, the lender has less time to accrue interest on your principal. This can save you hundreds, if not thousands, of dollars over the life of the loan.

- Faster Path to Ownership: You achieve financial freedom from your car payment much sooner. This frees up cash flow for other financial goals, like saving for a down payment on a house, investing, or tackling other debts.

- Reduced Risk of Being Upside Down: With a faster payoff, you’re less likely to owe more on your car than it’s worth (negative equity), especially as cars depreciate rapidly in their early years.

- Sense of Accomplishment: There’s a significant psychological benefit to paying off a major debt quickly. It’s a clear milestone in your financial journey.

Cons:

- Higher Monthly Payments: The trade-off for a shorter term is a higher monthly payment. You’re condensing the repayment of the principal into fewer installments.

- Potential Budget Strain: These higher payments might strain your monthly budget, especially if unexpected expenses arise. It’s crucial to ensure your income comfortably supports these payments.

- Less Financial Flexibility: With a larger fixed expense each month, you might have less discretionary income. This could impact your ability to save for emergencies or other short-term goals.

Long Loan Terms (e.g., 60-84 months)

Longer loan terms, spanning five to seven years, have become increasingly common. They appeal to buyers looking for lower monthly payments, but they come with their own set of considerations.

Pros:

- Lower Monthly Payments: This is the primary draw. By spreading the loan over more months, each individual payment is reduced, making more expensive vehicles seem more affordable.

- Easier Budgeting: Lower payments can free up cash flow in your monthly budget, providing more flexibility for other expenses or savings. This can be particularly appealing if you’re managing multiple financial commitments.

Cons:

- Higher Total Interest Paid: This is the most significant disadvantage. The longer your money is borrowed, the more interest accrues. You will pay substantially more over the life of the loan compared to a shorter term for the same car.

- Longer Period of Debt: You’re tied to a car payment for a much extended period. This can feel burdensome, especially if your financial situation changes or you wish to upgrade your vehicle sooner.

- Increased Risk of Being "Upside Down": Cars depreciate quickly. With a long loan, you’re more likely to owe more on the car than it’s worth for a significant portion of the loan term. This makes selling or trading in the car challenging without rolling negative equity into a new loan.

- Potential for More Repairs: As your car ages, the likelihood of needing significant repairs increases. You could find yourself making car payments on a vehicle that’s also requiring costly maintenance.

- Based on my experience, many people get drawn to longer terms for the allure of a lower monthly payment, only to regret the extra interest paid and the extended period of debt years down the line. It’s a classic example of prioritizing short-term relief over long-term financial health.

Strategies to Pay Off Your Car Loan Faster

The good news is you’re not entirely at the mercy of your initial loan agreement. There are proactive steps you can take to significantly shorten your car loan payoff time and save a substantial amount of money on interest. Taking control of your debt is a powerful financial move.

1. Making Larger Payments Consistently

This is the most straightforward and effective method. Simply paying more than your minimum required monthly payment directly attacks your principal balance. Every extra dollar you pay reduces the amount on which interest is calculated in subsequent months.

Even an additional $20 or $50 per month can make a remarkable difference over the life of the loan. It’s like putting your foot on the accelerator for your debt payoff journey. Be sure to instruct your lender to apply the extra amount directly to the principal, not towards future interest.

2. Making Bi-Weekly Payments

As discussed earlier, this strategy involves splitting your monthly payment in half and paying that amount every two weeks. Since there are 52 weeks in a year, this results in 26 half-payments, which equates to 13 full monthly payments instead of 12.

That "extra" payment each year goes directly towards reducing your principal balance. This accelerates your payoff schedule and saves you interest without requiring a significant change to your regular budget. It’s a clever trick to pay off car loan faster.

3. Applying Extra Payments from Windfalls

Did you receive a work bonus, a tax refund, or an unexpected gift? Instead of spending it, consider dedicating a portion or all of it to your car loan. These "windfalls" are perfect opportunities to make a lump-sum payment towards your principal.

Even a single large extra payment can shave months off your loan term and significantly reduce the total interest you pay. Pro tips from us: Treat these extra funds as opportunities to advance your financial goals, rather than just immediate spending money.

4. Refinancing Your Car Loan

Refinancing involves taking out a new loan to pay off your existing car loan. This strategy is particularly effective if you can secure a lower interest rate than your current loan. A lower APR means more of each payment goes to principal, speeding up your payoff.

You might also consider refinancing to a shorter loan term if your financial situation has improved since you first took out the loan. This combination of a lower rate and a shorter term can dramatically reduce your car loan payoff time and overall cost. Always compare offers from multiple lenders to ensure you’re getting the best deal.

5. Selling Your Car

While perhaps a more drastic measure, selling your car is a viable option if your goal is to eliminate the loan entirely and you no longer need the vehicle or can downsize. If the car’s market value is more than your outstanding loan balance, you can use the proceeds to pay off the loan and even pocket the difference.

If you are "upside down" (owe more than it’s worth), you’d need to cover the difference out of pocket. This might be a last resort, but it offers the fastest possible way to get rid of your car loan debt.

6. Utilizing Debt Snowball or Avalanche Methods

If you have multiple debts, you can integrate your car loan into a broader debt payoff strategy.

- Debt Snowball: Pay minimums on all debts except the smallest one, which you attack aggressively. Once the smallest is paid off, you roll that payment amount into the next smallest, gaining momentum.

- Debt Avalanche: Similar to the snowball, but you prioritize paying off the debt with the highest interest rate first. This method saves you the most money on interest over time.

Whichever method you choose, applying extra funds from other paid-off debts to your car loan can significantly accelerate its payoff. If you’re weighing this against other debts, you might find our guide on helpful.

Common Mistakes to Avoid When Managing Your Car Loan

While the desire to pay off your car loan is commendable, certain pitfalls can hinder your progress or even put you in a worse financial position. Being aware of these common mistakes is just as important as knowing the effective strategies.

1. Only Paying the Minimum

This is the most fundamental mistake. While paying the minimum keeps you current on your loan, it ensures you’ll pay the maximum amount of interest and remain in debt for the full term. It’s a passive approach that misses out on significant savings.

To truly accelerate your car loan payoff time, you must consistently pay more than the minimum required. Even a small surplus each month adds up over time.

2. Not Understanding Your Loan Terms

Many borrowers sign loan documents without fully comprehending the fine print. This includes understanding your interest rate, whether there are any prepayment penalties, and how extra payments are applied. Some lenders might automatically apply extra payments to the next month’s payment, rather than directly to the principal.

Common mistakes to avoid are not checking for prepayment penalties. While less common on car loans than mortgages, they do exist and can negate the benefits of early payoff. Always confirm with your lender how additional payments are processed to ensure they go directly to the principal.

3. Rolling Over Negative Equity from an Old Car

This is a very dangerous trap. If you trade in a car that you owe more on than it’s worth (negative equity), and the dealer rolls that difference into your new car loan, you start your new loan "upside down." This instantly increases your principal amount.

This mistake significantly extends your new car loan payoff time and can trap you in a cycle of debt. Always aim to sell your old car for more than you owe or pay off any negative equity out of pocket before financing a new vehicle.

4. Ignoring the Impact of Interest Rates

As discussed, the interest rate (APR) is a major driver of your total loan cost. Failing to shop around for the best rate or accepting a high rate due to convenience can cost you thousands over the life of the loan. This is especially critical if you have good credit and could qualify for much better terms.

Pro tip: Get pre-approved for a car loan from your bank or credit union before stepping into a dealership. This gives you leverage and a benchmark rate to compare against dealership financing offers. You can research average APRs at reputable financial sites like .

5. Forgetting About Depreciation

Cars are depreciating assets, meaning they lose value over time. Forgetting this reality can lead to being upside down on your loan, especially with long loan terms. If your car depreciates faster than you pay down the principal, you’ll owe more than the car is worth.

This becomes a problem if you need to sell the car or if it gets totaled in an accident, as your insurance payout might not cover the full loan amount. Being mindful of depreciation encourages you to pay off your car loan faster to mitigate this risk.

Understanding Your Car’s Depreciation and Its Impact

Depreciation is a silent but powerful force that significantly influences your financial position with a car loan. It’s the inevitable decline in your car’s value over time due to wear and tear, age, and the introduction of newer models. Understanding this concept is crucial for managing your car loan effectively.

What is Depreciation?

Simply put, depreciation is the difference between what you paid for your car and what it’s currently worth. A new car can lose 10-20% of its value in the first year alone, and roughly 40-50% within the first five years. This rapid decline means your car’s market value often falls faster than you pay down your loan, especially in the early years of ownership.

Factors like mileage, condition, accident history, and even the car’s color can all influence its rate of depreciation. While you can’t stop depreciation, you can understand its pace and plan accordingly.

How Does It Affect Being "Upside Down" on Your Loan?

Being "upside down" or having "negative equity" means you owe more on your car loan than the car is currently worth. This situation is directly tied to depreciation. If your loan balance is $20,000, but the car’s market value is only $18,000, you have $2,000 in negative equity.

This is a common scenario, especially with long loan terms (60+ months) and small or no down payments. When you stretch out your payments, the principal reduces very slowly, allowing depreciation to outpace your loan payoff progress. From an expert perspective, this is one of the riskiest positions for a car owner.

Why Paying Off Faster Helps Mitigate This Risk

Paying off your car loan faster is your best defense against negative equity. By aggressively reducing your principal balance, you work to ensure your loan amount decreases at a rate that keeps pace with, or ideally, outpaces depreciation.

This means you’ll reach a point where your car is worth more than you owe much sooner. This financial buffer provides peace of mind and flexibility. If you need to sell or trade in your car, you won’t be in the uncomfortable position of having to pay extra money just to get out of the loan.

Is Paying Off Your Car Loan Early Always the Best Option?

While the idea of being debt-free from your car loan is incredibly appealing, and often financially savvy, it’s not always the absolute best move for everyone at every point in their financial journey. Your personal circumstances and broader financial goals should always guide your decision.

Considerations Beyond the Car Loan

Before aggressively paying off your car loan, take a holistic look at your entire financial landscape.

- Other High-Interest Debt: Do you have credit card debt or personal loans with significantly higher interest rates than your car loan? If your car loan has a low APR (e.g., 2-4%), but you have credit card debt at 18-25%, it almost always makes more financial sense to prioritize paying off the higher-interest debt first. The money saved on interest from those debts will be far greater.

- Emergency Fund: Do you have a fully funded emergency fund (typically 3-6 months of living expenses) readily accessible? If not, building this safety net should be a top priority. An emergency fund protects you from unexpected job loss, medical bills, or major home repairs, preventing you from going into more debt.

- Investment Opportunities: Could the extra money you’d put towards your car loan yield a higher return if invested elsewhere? If you have access to investment vehicles that historically offer returns greater than your car loan’s interest rate, it might be more financially advantageous to invest that money. This is a nuanced decision and often depends on your risk tolerance and financial knowledge.

- Future Financial Goals: Are you saving for a down payment on a house, your child’s education, or retirement? While paying off a car loan is great, it shouldn’t derail other critical long-term financial goals that could have a larger impact on your future.

Balancing Act: Financial Goals Beyond Just the Car Loan

Ultimately, deciding how long to pay off car loan or if you should pay it off early involves a balancing act. It’s about optimizing your financial resources to achieve your most important goals. For some, the psychological relief of being car-debt-free outweighs slightly higher returns elsewhere. For others, particularly those with disciplined investing habits and low car loan interest rates, redirecting funds to investments makes more sense.

Our in-depth analysis suggests that for most people, especially those with average or higher interest rates, paying off a car loan earlier provides a tangible benefit in saved interest and reduced financial stress. However, always ensure your emergency fund is robust and that you’re not neglecting higher-interest debts in the process. You might find our comprehensive guide on useful for future vehicle purchases.

Conclusion: Your Path to Car Loan Freedom

Navigating the world of car loans can feel complex, but with a clear understanding of the factors at play, you’re empowered to take control. How long to pay off car loan isn’t a fixed destiny; it’s a journey influenced by your choices, from the initial loan term you select to the proactive strategies you employ during repayment.

We’ve explored how loan terms, interest rates, principal amounts, down payments, and even payment frequency all shape your payoff timeline. We’ve also highlighted the benefits of shorter terms, the pitfalls of longer ones, and a host of actionable strategies to accelerate your debt freedom. Remember the crucial mistakes to avoid, such as only paying the minimum or neglecting depreciation’s impact.

Ultimately, your goal should be to align your car loan management with your broader financial objectives. Whether you choose to aggressively pay it down, strategically refinance, or balance it against other financial priorities, the power is in your hands. Drive towards financial freedom with confidence and make your car loan a temporary stop on your journey, not a permanent burden.