How Long Is A Car Loan Term: The Ultimate Guide to Choosing Your Auto Financing Duration

How Long Is A Car Loan Term: The Ultimate Guide to Choosing Your Auto Financing Duration Carloan.Guidemechanic.com

Navigating the world of car financing can feel like a complex journey, with various paths leading to your dream vehicle. One of the most critical decisions you’ll face, yet often overlooked beyond the monthly payment, is how long is a car loan term. This single choice has a profound impact on your financial well-being, influencing everything from the total cost of your car to your long-term budget flexibility.

As an expert blogger and professional in the automotive finance space, I’ve seen firsthand how choosing the right (or wrong) car loan term can significantly shape a borrower’s experience. This comprehensive guide is designed to demystify car loan terms, helping you make an informed decision that aligns with your financial goals and drives you towards smart car ownership. We’ll dive deep into the pros and cons, common pitfalls, and expert strategies to ensure you pick the optimal duration for your next auto loan.

How Long Is A Car Loan Term: The Ultimate Guide to Choosing Your Auto Financing Duration

Understanding Car Loan Terms: The Foundation

Before we explore the nuances, let’s establish a clear understanding of what a car loan term actually is. Simply put, the car loan term refers to the length of time you have to repay the borrowed amount for your vehicle, expressed in months.

This duration is fixed at the time you take out the loan, establishing a set schedule for your repayments. Each month, you’ll make a payment that covers a portion of the principal (the amount you borrowed) and the interest accrued.

The length of your auto loan term directly influences two major factors: your monthly payment and the total amount of interest you’ll pay over the life of the loan. A longer term generally means lower monthly payments but more interest paid overall, while a shorter term translates to higher monthly payments but less total interest. It’s a fundamental trade-off that every car buyer must consider carefully.

The Average Car Loan Term: What Do The Numbers Say?

The landscape of auto financing is constantly evolving, and so are the typical durations people choose for their loans. Understanding the current trends in average car loan terms can provide a helpful benchmark, though it’s crucial to remember that "average" doesn’t necessarily mean "ideal" for everyone.

Based on recent industry data, the average new car loan term in the U.S. has been trending upwards, often hovering around 68-72 months, with used car loans sometimes extending even longer. This shift towards extended terms is largely driven by rising vehicle prices. As cars become more expensive, consumers often opt for longer loan durations to keep their monthly payments manageable.

For instance, reports from industry analysts like Experian frequently highlight these trends, showing a clear preference for longer terms as a means to cope with higher sticker prices. This strategy allows more buyers to access new vehicles, but it also comes with significant financial implications that we’ll explore in detail.

The Pros and Cons of Shorter Car Loan Terms (e.g., 36-60 months)

Opting for a shorter car loan length, typically between 36 to 60 months, is often championed by financial advisors for good reason. While it demands a higher monthly commitment, the long-term financial benefits are substantial.

Pros of Shorter Car Loan Terms:

- Less Total Interest Paid: This is perhaps the biggest advantage. By paying off your loan quicker, you give the interest less time to accrue. Over the life of the loan, this can translate into significant savings, sometimes thousands of dollars.

- Faster Equity Build-Up: When your loan term is shorter, a larger portion of your monthly payment goes towards the principal balance. This means you build equity in your vehicle much faster, reducing the risk of being "upside down" on your loan.

- Reduced Risk of Negative Equity: Negative equity, or being "underwater," occurs when you owe more on your car than it’s worth. Shorter terms significantly mitigate this risk because you pay down the loan balance more rapidly, outpacing the car’s depreciation.

- Quicker Path to Debt Freedom: Imagine being car payment-free sooner! A shorter term means you’ll own your car outright much faster, freeing up a substantial amount in your monthly budget for other financial goals, like saving, investing, or paying off other debts.

- Potentially Lower Interest Rates: Lenders often view shorter loan terms as less risky. As a result, they may offer more competitive, lower annual percentage rates (APRs) for loans with durations of 36 or 48 months compared to 72 or 84 months.

Cons of Shorter Car Loan Terms:

- Higher Monthly Payments: The most obvious drawback is the increased financial strain each month. Spreading the principal over fewer payments means each payment will be larger, which might not be feasible for every budget.

- May Strain Your Budget: If your income isn’t robust or stable enough, a high monthly payment can lead to financial stress, making it difficult to cover other essential expenses or save for emergencies. This can make owning a car feel like a burden rather than a convenience.

- Requires Stronger Financial Position: To comfortably afford a shorter term, you generally need a healthy income, a good credit score, and possibly a larger down payment. It’s a commitment that requires a stable financial foundation.

The Pros and Cons of Longer Car Loan Terms (e.g., 60-84+ months)

In contrast to shorter terms, longer auto loan terms—stretching from 60 to 84 months or even beyond—have become increasingly prevalent. They offer a seemingly attractive solution to rising car prices, but it’s vital to understand the full scope of their implications.

Pros of Longer Car Loan Terms:

- Lower Monthly Payments: This is the primary appeal of extended terms. By spreading the loan amount over a greater number of months, each individual payment is significantly reduced, making higher-priced vehicles more "affordable" on a monthly basis.

- More Budget Flexibility: Lower monthly payments can free up cash flow, allowing you to allocate funds to other areas of your budget, such as savings, investments, or discretionary spending. This flexibility can be crucial for managing daily finances.

- Can Afford a More Expensive Car (Potentially): While not always advisable, a longer term might enable you to purchase a vehicle that would otherwise be out of reach with a shorter loan duration. This can be appealing if you have specific features or a certain model in mind.

- Free Up Cash for Other Investments/Savings: If you have high-return investment opportunities or other pressing financial goals, a lower car payment could theoretically free up capital to pursue those. However, this strategy only works if the investment returns outweigh the extra interest paid on the car loan.

Cons of Longer Car Loan Terms:

- Significantly More Total Interest Paid: This is the biggest hidden cost. Over an extended period, the cumulative interest can add up dramatically, sometimes thousands of dollars more than a shorter loan for the exact same vehicle. You’re paying for the convenience of lower monthly payments.

- Slower Equity Build-Up; Higher Risk of Negative Equity: With more of your initial payments going towards interest, your principal balance decreases very slowly. This leaves you vulnerable to being upside down on your loan for a much longer period, making it difficult to sell or trade in your car without owing money.

- Car Depreciates Faster Than You Pay It Off: Vehicles lose value rapidly, especially in the first few years. With a long loan term, your car’s market value can plummet faster than you’re able to pay down the loan, creating a persistent negative equity situation. Based on my experience, this is one of the most common traps borrowers fall into.

- Longer Commitment, Vehicle Reliability Concerns: An 84-month loan means you’re committed to that vehicle for seven years. Will the car still be reliable and meet your needs for that long? Maintenance costs tend to increase significantly as a car ages, potentially adding to your financial burden while you’re still making payments.

- Potentially Higher Interest Rates: Lenders often charge slightly higher interest rates for longer loan terms because they represent a greater risk over time. This further compounds the total cost of your loan.

Factors Influencing Your Ideal Car Loan Term

Choosing the optimal car loan term isn’t a one-size-fits-all decision. Several personal and financial factors should guide your choice. Thoughtful consideration of these elements will help you align your auto financing with your broader financial health.

- Your Budget & Monthly Payment Comfort: This is arguably the most immediate factor. You need to determine how much you can realistically afford to pay each month without straining your finances. Pro tips from us: Don’t just look at the maximum you can afford, but what you comfortably afford while still saving and meeting other obligations.

- Interest Rate & APR: The Annual Percentage Rate (APR) you qualify for will significantly impact your total cost. A lower APR can make a slightly higher monthly payment on a shorter term more palatable, as it saves you more in the long run. Conversely, a high APR on a long term can be a recipe for financial regret.

- Vehicle Depreciation: Cars are depreciating assets. Understanding how quickly your chosen vehicle loses value is crucial. If you opt for a long loan term on a car known for rapid depreciation, you’re almost guaranteeing a period of negative equity.

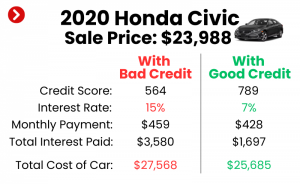

- Your Credit Score: Your creditworthiness plays a huge role in the interest rate you’ll be offered. A strong credit score (generally 700+) can unlock lower rates, making shorter terms more affordable and reducing the total interest paid. If your credit score needs a boost, consider working on it before applying for a loan. (For tips on improving your credit, check out our Guide to Boosting Your Credit Score – Internal Link Placeholder).

- Down Payment Amount: A larger down payment reduces the amount you need to borrow, which in turn lowers your monthly payments and total interest. It also helps you build equity faster, providing a buffer against depreciation.

- Vehicle Reliability & Longevity: For longer loan terms, it’s particularly important to choose a vehicle known for its durability and reliability. You don’t want to be making payments on a car that’s constantly in the shop or has lost most of its value.

- Your Future Financial Plans: Consider your life plans. Are you expecting a significant change in income, buying a house, or starting a family soon? A long car loan can restrict your financial flexibility for other major life events.

Common Mistakes to Avoid When Choosing a Car Loan Term

Based on my experience counseling countless car buyers, certain missteps are repeatedly made when selecting a car loan term. Avoiding these pitfalls can save you a great deal of money and stress in the long run.

- Focusing Only on the Monthly Payment: This is perhaps the most common mistake. Dealerships often emphasize the lowest possible monthly payment to make a car seem affordable. While the monthly payment is important for budgeting, it tells only half the story. Always ask for the total cost of the loan.

- Ignoring Total Interest Paid: The allure of a low monthly payment can blind buyers to the substantial extra interest they’ll pay over a longer term. Always compare the total interest paid across different term lengths. You might be surprised by the difference.

- Not Considering Depreciation: Many buyers overlook how quickly a new car loses value. Common mistakes to avoid are extending a loan so long that you’re underwater for most of its duration, making it impossible to sell or trade without a financial hit.

- Stretching the Term Too Long for a Car You Can’t Truly Afford: Using an 84-month loan to buy a car that’s genuinely out of your budget is a recipe for financial strain. It ties you to a depreciating asset for an excessive period, often leading to buyer’s remorse and financial stress.

- Not Shopping Around for Rates and Terms: Don’t just accept the first offer from the dealership. Always get pre-approved from multiple lenders (banks, credit unions, online lenders) before you even step onto the lot. This allows you to compare different rates and term options objectively.

- Forgetting About Insurance and Maintenance Costs: Your car payment isn’t your only car-related expense. Factor in the cost of insurance, fuel, and routine maintenance when determining your overall car budget. These costs can add up, especially for older vehicles or luxury models.

Strategies for Optimizing Your Car Loan Term

Making an informed decision about your car loan term requires proactive strategies. Here are some expert tips to help you secure the best possible financing for your next vehicle.

- Save for a Larger Down Payment: This is hands down one of the most effective strategies. A substantial down payment reduces the principal loan amount, which in turn lowers your monthly payments and the total interest you’ll pay. It also immediately gives you equity in the vehicle.

- Improve Your Credit Score: A higher credit score signals to lenders that you’re a responsible borrower, making you eligible for lower interest rates. Even a small improvement in your score can save you hundreds, if not thousands, of dollars over the life of a loan.

- Shop Around Aggressively for Lenders: Never settle for the first loan offer. Contact several banks, credit unions, and online lenders to compare their rates, terms, and conditions. This competitive shopping can reveal significantly better deals and help you negotiate more effectively.

- Consider a Shorter Term If Feasible: If your budget allows, opting for a shorter loan duration (e.g., 36 or 48 months) is almost always the financially smarter choice. You’ll pay less interest, build equity faster, and be debt-free sooner.

- Think About Refinancing Later: If you’re currently stuck with a longer term or a high-interest rate, remember that you might be able to refinance your car loan down the line. If your credit score improves or interest rates drop, refinancing can secure you a better rate or a shorter term. (To learn more, check out our Comprehensive Guide to Car Loan Refinancing – Internal Link Placeholder).

- Negotiate the Car Price, Not Just the Payments: Before you even discuss financing, negotiate the purchase price of the vehicle. A lower purchase price directly translates to a smaller loan amount, reducing both your monthly payments and total interest regardless of the term length.

When Is a Longer Term Acceptable (or Even Smart)?

While shorter terms are generally preferable, there are specific situations where a longer car loan term might be acceptable, or even a strategically smart move. These scenarios usually involve a borrower with a clear plan and financial discipline.

- When Interest Rates Are Exceptionally Low: In periods of very low interest rates, the additional interest paid over a longer term might be minimal. If you have a rock-bottom APR, the cost difference between a 60-month and 72-month loan might be less impactful, allowing you to prioritize cash flow.

- When You Plan to Pay It Off Early Without Penalty: If you intend to make extra payments or pay off the loan well before the term ends, a longer term with lower required monthly payments can offer flexibility. This allows you to pay less when finances are tight, but accelerate payments when you have extra cash, provided there are no prepayment penalties.

- When You Have a Very Reliable Vehicle and Strong Financial Discipline: If you’ve chosen a car known for its exceptional longevity and you are confident in your ability to manage your finances, a longer term might work. This is especially true if you plan to keep the car well beyond the loan term, essentially getting years of payment-free driving after it’s paid off.

- As a Temporary Measure with a Refinancing Plan: Sometimes, a longer term is necessary to secure a car in an emergency. If you’re confident your credit will improve significantly or your income will increase in the near future, you might take a longer term initially with the express intention of refinancing to a shorter term and better rate later on.

The Impact of Car Loan Term on Your Financial Health

The decision of how long is a car loan term extends far beyond just monthly payments; it significantly shapes your overall financial health. This choice can impact your debt-to-income ratio, your ability to save, and your long-term wealth-building potential.

A long car loan, especially one that stretches to 72 or 84 months, can tie up a substantial portion of your monthly income for an extended period. This directly affects your debt-to-income (DTI) ratio, a key metric lenders use to assess your ability to take on new debt, such as a mortgage. A high DTI due to a lengthy car loan could hinder your ability to secure other financing.

Furthermore, the opportunity cost of excessive interest payments cannot be overstated. Money spent on interest is money that could have been saved, invested, or used to pay down higher-interest debt. Building equity in your vehicle versus remaining underwater for years dictates whether your car is an asset (even a depreciating one) or a financial liability. Making a prudent choice about your car loan term is a foundational step in responsible financial planning.

Real-Life Scenarios and Examples

Let’s illustrate the impact with two simplified scenarios, highlighting the core concept without complex calculations.

Scenario A: The "Affordable Payment" Trap

Imagine Sarah needs a car and finds one she loves for $30,000. The dealer offers her a 72-month loan with a 6% APR, resulting in a monthly payment of about $498. This feels affordable to her. However, the total interest paid over those six years will be approximately $5,800. If she had opted for a 48-month loan at the same rate, her monthly payment would be higher, around $705, but her total interest would drop to about $3,800. The "affordable" payment cost her an extra $2,000 in interest.

Scenario B: The "Debt-Free Fast" Approach

Mark, on the other hand, prioritizes financial freedom. He finds a $25,000 car and, despite being offered a 60-month loan, he pushes for a 36-month term because his budget can handle the higher monthly payments. He pays more each month, but he’s debt-free in three years, having paid significantly less in interest. This frees up his budget to save for a down payment on a house, while Sarah is still making car payments.

These examples underscore that focusing solely on the monthly payment can lead to significant long-term costs, whereas a strategic approach can accelerate your financial goals.

Refinancing Your Car Loan: A Second Chance

Even if you’ve already committed to a car loan term that no longer feels right, all is not lost. Refinancing your car loan can provide a valuable opportunity to adjust your terms and potentially save money.

Refinancing involves taking out a new loan to pay off your existing car loan. People often choose to refinance to secure a lower interest rate, which can reduce their monthly payments and the total interest paid. Alternatively, refinancing can be used to shorten your loan term, helping you pay off the car faster, even if your monthly payment increases slightly.

This strategy is particularly beneficial if your credit score has improved since you first took out the loan, or if market interest rates have dropped. It’s a way to essentially get a "do-over" on your financing, aligning it better with your current financial situation and goals.

Conclusion

Deciding how long is a car loan term is a pivotal moment in your car buying journey, carrying implications that resonate throughout your financial life. It’s far more than just picking a monthly payment; it’s about understanding the delicate balance between immediate affordability and long-term financial health.

By thoroughly evaluating the pros and cons of both short and long loan durations, considering your personal financial situation, and diligently avoiding common mistakes, you can make a choice that empowers you. Remember to prioritize total cost over just the monthly payment, leverage a strong credit score, and always shop around for the best rates.

Your car is a significant investment, and how you finance it can determine whether it’s an asset that serves you well or a lingering financial burden. By applying the insights and strategies shared in this guide, you’re now equipped to drive away with confidence, knowing you’ve made a smart, informed decision about your auto financing duration. What term length are you considering for your next car? Share your thoughts in the comments below!