How Long Of A Car Loan Can I Get? Unlocking the Secrets to Your Ideal Auto Financing Term

How Long Of A Car Loan Can I Get? Unlocking the Secrets to Your Ideal Auto Financing Term Carloan.Guidemechanic.com

Buying a car is an exciting milestone, but the financing aspect often feels like navigating a maze. One of the most critical decisions you’ll face is determining the length of your car loan, also known as the loan term. This choice impacts everything from your monthly budget to the total amount you’ll pay for your vehicle over its lifetime.

Many prospective car owners ask: "How long of a car loan can I get?" The answer isn’t a simple number, but rather a dynamic range influenced by several personal and market factors. As an expert blogger and professional SEO content writer, I’m here to demystify car loan terms and guide you through selecting the optimal financing plan for your next set of wheels. This comprehensive guide will arm you with the knowledge to make an informed, confident decision.

How Long Of A Car Loan Can I Get? Unlocking the Secrets to Your Ideal Auto Financing Term

Understanding Car Loan Terms: The Foundation

Before we dive into the specifics, let’s establish a clear understanding of what a car loan term actually is. Simply put, the loan term is the duration, usually expressed in months, over which you agree to repay the money borrowed to purchase your vehicle. This period includes both the principal amount (the car’s price minus any down payment) and the interest charged by the lender.

Common loan terms typically range from 36 months (3 years) to 84 months (7 years), though shorter or even longer options can sometimes be found. The initial impact of this term length is immediately apparent in your monthly payment. A longer term usually translates to lower monthly payments, while a shorter term means higher monthly payments. However, this initial convenience often comes with significant trade-offs, which we will explore in detail.

The Spectrum of Car Loan Lengths: What’s Available?

The car loan market offers a wide array of term lengths, each with its own set of advantages and disadvantages. Understanding these options is crucial for making a choice that aligns with your financial goals and lifestyle.

Short-Term Loans (e.g., 36-48 months)

Short-term car loans, typically spanning three to four years, are often favored by those who prioritize minimizing the total cost of their vehicle. These loans come with higher monthly payments compared to their longer counterparts, but they offer substantial savings on interest over the life of the loan.

Pros of Short-Term Loans:

- Lower Total Cost: You pay significantly less in interest because the principal is paid off more quickly.

- Faster Equity Build-Up: You gain ownership of your vehicle sooner, reaching a point of positive equity much faster. This means the car’s value will exceed what you owe on it.

- Reduced Risk of Negative Equity: The chances of owing more than your car is worth (being "upside down" on your loan) are greatly diminished.

- Quicker Debt Freedom: You’ll be debt-free sooner, freeing up your budget for other financial goals or future investments.

Cons of Short-Term Loans:

- Higher Monthly Payments: The most significant drawback is the increased financial burden each month, which might not be feasible for all budgets.

- Less Financial Flexibility: Higher payments can strain your cash flow, leaving less room for unexpected expenses or savings.

Based on my experience, many financially savvy buyers, especially those with stable incomes and strong savings, opt for shorter terms. They understand that the temporary pinch of higher monthly payments is well worth the long-term savings and financial freedom. It’s a strategic move to build equity quickly and avoid prolonged debt.

Medium-Term Loans (e.g., 60-72 months)

Medium-term loans, typically ranging from five to six years, represent the most popular choice for many car buyers. These terms strike a balance between manageable monthly payments and a reasonable total interest cost. They are often seen as the sweet spot for those seeking affordability without excessively extending their debt.

Pros of Medium-Term Loans:

- Manageable Monthly Payments: Payments are lower than short-term loans, making them more accessible for a wider range of budgets.

- Reasonable Total Interest: While you’ll pay more interest than with a 36-month loan, it’s considerably less than what you’d accrue on an 84-month term.

- Good Balance: They offer a practical compromise between the speed of repayment and monthly affordability.

Cons of Medium-Term Loans:

- Still Significant Interest: You’re still paying a notable amount in interest compared to a shorter loan.

- Potential for Negative Equity: Depending on your down payment and the car’s depreciation rate, you could still find yourself in a negative equity situation, especially during the early years of the loan.

Pro tips from us: This term often strikes a good balance for the average consumer. It allows for a comfortable monthly payment while not dragging out the debt for too long. However, always ensure your down payment is substantial enough to mitigate the risk of being upside down on your loan.

Long-Term Loans (e.g., 72-84+ months)

Long-term car loans, stretching seven years or even longer, have become increasingly common. Their primary appeal lies in offering the lowest possible monthly payments, making more expensive vehicles seem accessible to a broader market. However, this apparent affordability comes at a significant financial cost.

Pros of Long-Term Loans:

- Lowest Monthly Payments: This is the main draw, as it significantly reduces the immediate financial burden.

- Access to More Expensive Vehicles: Lower payments can allow buyers to afford vehicles that would be out of reach with shorter loan terms.

Cons of Long-Term Loans:

- Significantly Higher Total Interest: You will pay substantially more in interest over the life of the loan. The longer the money is borrowed, the more interest accrues.

- Prolonged Debt: You’re tied to a car payment for a much longer period, potentially limiting other financial opportunities or future car purchases.

- High Risk of Negative Equity: Depreciation typically outpaces principal payments, especially in the early years. This means you could owe far more than the car is worth for an extended period.

- Higher Insurance Costs: You’ll be required to carry comprehensive and collision insurance for the entire loan term, which can be expensive for a longer duration.

- Vehicle Longevity Concerns: Will the car reliably last for 7-8 years without major repair costs, especially once the warranty expires? You might still be paying off a car that needs significant maintenance.

Common mistakes to avoid are getting lured solely by low monthly payments without considering the total cost of ownership. From an expert’s perspective, while tempting, these loans demand careful consideration of the long-term financial implications. It’s easy to focus on the immediate relief of a low payment, but ignoring the accumulated interest and increased risk is a costly error.

Factors That Influence How Long Of A Car Loan You Can Get

The maximum car loan term you qualify for isn’t arbitrary. Several critical factors come into play, influencing both the length of the loan and the interest rate you’ll be offered. Understanding these elements empowers you to position yourself for the best possible financing terms.

1. Your Credit Score

Your credit score is arguably the most significant factor lenders consider. It’s a numerical representation of your creditworthiness and your history of managing debt.

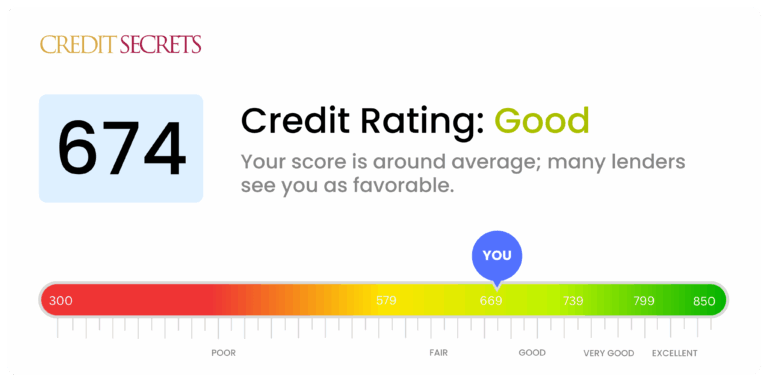

- Excellent Credit (780+): With a stellar credit score, you’re a low-risk borrower. Lenders will compete for your business, offering the most favorable interest rates and the widest range of loan terms, including the longest available options.

- Good Credit (670-779): You’ll still qualify for competitive rates and a good selection of loan terms, though perhaps not the absolute best.

- Fair Credit (580-669): Options start to narrow. You might face higher interest rates and a more limited choice of loan terms, with some lenders being hesitant to offer very long terms due to increased risk.

- Poor Credit (Below 580): Obtaining a car loan can be challenging. Lenders will perceive you as a high-risk borrower, resulting in significantly higher interest rates and often shorter loan terms to mitigate their exposure.

Lenders use your credit score to gauge your reliability. A higher score signals a greater likelihood of on-time payments, making them more comfortable extending a loan for a longer duration. If you’re unsure about your credit score, it’s wise to check it before applying for a loan. can provide more insights into improving this crucial number.

2. Your Down Payment

The amount of money you put down upfront on a car directly impacts the loan amount and, consequently, the loan term. A larger down payment reduces the principal amount you need to borrow.

- Larger Down Payment: This demonstrates your commitment and reduces the lender’s risk. With less to finance, you might qualify for a shorter loan term while maintaining a manageable monthly payment. It also helps you build equity faster and reduces the total interest paid.

- No or Small Down Payment: Financing 100% or nearly 100% of the vehicle’s cost increases the loan amount. This often necessitates a longer loan term to keep monthly payments affordable, but it significantly increases your total interest and the risk of negative equity.

A substantial down payment not only saves you money in the long run but can also open doors to better loan terms and interest rates, as lenders view you as a less risky borrower.

3. Vehicle Age & Type

The specific vehicle you’re purchasing also plays a role in how long of a car loan you can get. Lenders assess the risk associated with the car itself.

- New Cars: New vehicles typically qualify for the longest loan terms (e.g., 84 months) because they hold their value better initially and come with manufacturer warranties, reducing the risk of immediate mechanical issues.

- Used Cars: Loan terms for used cars are often shorter than for new cars. Lenders are more cautious with older vehicles due to higher depreciation rates and the increased likelihood of mechanical problems. The older the used car, the shorter the maximum loan term a lender is usually willing to offer.

- Luxury vs. Economy: While not a direct determinant of term length, the type of vehicle can influence the loan amount and thus the need for a longer term to keep payments low. Lenders might also have different policies for high-value luxury vehicles versus more standard economy cars.

4. Lender Policies

Not all lenders are created equal. Banks, credit unions, and dealership finance departments all have their own specific lending criteria, risk assessments, and maximum loan term policies.

- Banks: Often offer competitive rates and a wide range of terms, especially for well-qualified borrowers.

- Credit Unions: Known for potentially lower rates and more flexible terms, particularly for their members. They might be more willing to work with borrowers who have slightly less-than-perfect credit.

- Dealership Financing (Captive Lenders): These are finance companies owned by the car manufacturers (e.g., Ford Credit, Toyota Financial Services). They often have promotional rates and terms, sometimes including very long options, to move specific inventory. However, these attractive offers might only be available to top-tier credit applicants.

- Online Lenders: A growing option offering convenience and competitive rates, with various term lengths.

Based on my years in the industry, comparing lenders is crucial. Don’t assume the first offer you receive is the best. Shopping around can reveal significant differences in interest rates and available loan terms.

5. Debt-to-Income Ratio (DTI)

Your debt-to-income (DTI) ratio is a key metric lenders use to assess your ability to manage monthly payments. It compares your total monthly debt payments (including the proposed car payment) to your gross monthly income.

- Lower DTI: A lower DTI indicates that you have plenty of income to cover your existing debts and the new car payment. This makes you a more attractive borrower, potentially qualifying you for better terms, including longer ones if desired.

- Higher DTI: A high DTI suggests you might be stretched thin financially. Lenders might be hesitant to approve a loan, or they may offer less favorable terms, including shorter loan terms with higher payments, to minimize their risk.

Lenders typically prefer a DTI ratio below 36%, though some may go higher depending on other factors like your credit score and down payment.

6. Current Interest Rates

While not directly influencing the maximum term you can get, prevailing interest rates in the market can influence the desirability of a longer loan term.

- Low-Interest Rate Environment: When interest rates are low, the extra cost of a longer term (due to more interest paid) is less pronounced, making longer terms seem more appealing for their low monthly payments.

- High-Interest Rate Environment: When rates are high, the total interest paid on a long-term loan can become exorbitant. In such a scenario, borrowers might actively seek shorter terms to minimize the overall financial burden, even if it means higher monthly payments.

The True Cost of a Longer Car Loan: Beyond the Monthly Payment

It’s easy to get fixated on the lowest possible monthly payment. However, failing to look beyond this single figure is a common pitfall that can lead to significant financial disadvantages over the life of your loan. Understanding the true cost is essential for a responsible car purchase.

1. Total Interest Paid

This is perhaps the most significant hidden cost of a long-term loan. While the monthly payments are lower, you are paying interest for a much longer period. Even a small difference in the annual percentage rate (APR) can lead to thousands of dollars in extra interest over an extended term.

For example, financing $30,000 at 6% APR:

- 60-month term: Monthly payment around $580, total interest around $4,800.

- 84-month term: Monthly payment around $436, total interest around $6,600.

In this scenario, extending the loan by 24 months saves you about $144 per month but costs you an extra $1,800 in interest. For more expensive vehicles or higher interest rates, this difference can be even more dramatic. The convenience of a lower monthly payment often comes with a hefty price tag in the form of accumulated interest.

2. Negative Equity (Being "Upside Down")

Negative equity, or being "upside down" on your loan, means you owe more on your car than it is currently worth. This is a prevalent risk with long-term loans, especially if you made a small down payment or no down payment at all.

Cars depreciate rapidly, particularly in the first few years. With a long-term loan, your principal balance might decrease very slowly, especially initially, while the car’s value plummets. This creates a gap where your debt outstrips the vehicle’s market value.

Why is this problematic?

- Total Loss: If your car is stolen or totaled in an accident, your insurance payout will only cover the car’s actual cash value, not necessarily what you owe. You’d be left paying the difference out of pocket for a car you no longer have.

- Trade-in Difficulty: If you decide to sell or trade in your car before the loan is paid off, you’ll have to come up with the cash to cover the negative equity before you can get into a new vehicle.

A common mistake is not considering depreciation when choosing a loan term. Always aim to have your principal balance decrease faster than your car’s market value, or at least keep pace with it.

3. Extended Period of Debt

A longer loan term means you are tied to a car payment for a more extended period of your life. An 84-month loan means seven years of car payments. This can impact your financial flexibility and your ability to pursue other financial goals, such as saving for a down payment on a home, investing, or saving for retirement.

Being perpetually in debt for a depreciating asset can be a significant drain on your overall financial health. It can also complicate future vehicle purchases, as you might still be paying off your current car when you’re ready for a new one.

4. Higher Insurance Costs

As long as you have a loan on your vehicle, lenders typically require you to carry full-coverage insurance (comprehensive and collision) to protect their asset. This coverage is generally more expensive than liability-only insurance.

With a longer loan term, you’ll be paying for this more expensive full-coverage insurance for a greater number of years. This adds another layer to the total cost of ownership that is directly tied to the length of your loan.

Choosing Your Ideal Car Loan Term: A Strategic Approach

There’s no single "best" car loan term that fits everyone. The ideal length depends entirely on your individual financial situation, priorities, and tolerance for risk. Here’s a strategic approach to help you make the right choice:

1. Assess Your Budget Honestly

Before looking at any cars, sit down and thoroughly review your finances. Don’t just consider what you can afford for a monthly payment, but what you should afford.

- Income: What is your stable, after-tax monthly income?

- Expenses: List all your fixed and variable monthly expenses (rent/mortgage, utilities, food, existing debts, savings).

- Discretionary Income: How much money is left over after all essential expenses and savings contributions? Your car payment should comfortably fit within this, leaving room for unexpected costs.

Don’t let a low monthly payment lure you into a loan that strains your budget in other areas. Overstretching your budget for a car can lead to financial stress and compromise other important financial goals.

2. Consider Your Driving Habits & Vehicle Longevity

How long do you typically keep a car? What are your driving habits like?

- Short Ownership Cycle (3-5 years): If you like to upgrade frequently, a shorter loan term makes more sense. You’ll build equity faster and avoid being upside down when you’re ready to trade in.

- Long Ownership Cycle (7+ years): If you plan to drive your car until it falls apart, a longer term might be acceptable, but you must factor in the increased interest cost and potential for major repairs once the warranty expires. Ensure the car model you choose has a reputation for reliability.

3. Calculate Total Cost, Not Just Monthly Payment

This is a critical step that many buyers overlook. While a $400 monthly payment for 84 months looks appealing compared to $600 for 48 months, the total cost difference can be staggering.

Pro tips from us: Always use an online car loan calculator to compare total costs for different loan terms and interest rates. Most reputable lenders and financial websites offer these tools. Focus on the "total amount paid" figure, not just the monthly installment. This holistic view will prevent you from making a costly mistake.

4. Factor in Resale Value & Depreciation

Research the depreciation rates of the specific vehicle model you’re interested in. Some cars hold their value better than others. Aim to choose a loan term where you can maintain positive equity throughout most of the loan’s life. This provides financial flexibility if you need to sell the car unexpectedly.

5. Don’t Forget the Down Payment

A larger down payment is almost always beneficial. It reduces the amount you borrow, lowers your monthly payments, decreases the total interest paid, and helps you avoid negative equity. If possible, save up for a significant down payment (at least 10-20% of the vehicle’s price) before you even start shopping.

6. Explore Pre-Approval Options

Before you step foot in a dealership, get pre-approved for a car loan from a bank or credit union. This allows you to:

- Know Your Rate and Term: You’ll understand the best interest rate and longest term you qualify for based on your credit.

- Strengthen Your Negotiation Position: You can walk into the dealership with your own financing in hand, giving you leverage to negotiate on the car’s price rather than getting caught up in payment discussions.

- Avoid Pressure: You won’t feel pressured to accept the dealer’s financing offer if it’s not the best deal.

The Consumer Financial Protection Bureau offers excellent resources on understanding auto loans and the pre-approval process, which can be invaluable.

Strategies for Managing Your Car Loan, Regardless of Term

Even after you’ve secured your car loan, there are proactive steps you can take to manage it effectively and potentially save money.

1. Make Extra Payments

If your financial situation improves, consider making extra payments towards your principal. Even a small additional amount each month can significantly reduce the total interest paid and shorten your loan term. Ensure your loan agreement doesn’t have prepayment penalties, although these are rare for car loans.

- How it works: Extra payments directly reduce your principal balance. Since interest is calculated on the remaining principal, a lower principal means less interest accrues over time.

2. Refinancing Your Loan

If interest rates drop, your credit score improves significantly, or you want to adjust your loan term, refinancing might be a smart move. Refinancing involves taking out a new loan to pay off your existing car loan, often with a better interest rate or a more suitable term.

- When to consider it: If you can secure a lower interest rate, you’ll save money. If you initially took a long term for affordability but can now handle higher payments, refinancing to a shorter term can reduce your total interest cost. Conversely, if you need to lower your monthly payments, a longer refinanced term might provide temporary relief (but be mindful of increased total interest). offers a deeper dive into this topic.

3. Consider Gap Insurance

If you opt for a long-term loan, especially with a minimal down payment, Gap (Guaranteed Asset Protection) insurance is highly recommended. This insurance covers the "gap" between what your car is worth (and what your standard insurance would pay out in a total loss) and the amount you still owe on your loan.

Given the high risk of negative equity with longer terms, Gap insurance provides crucial financial protection in case of an accident or theft, preventing you from being responsible for a significant debt on a car you no longer possess.

Conclusion: Your Informed Decision

So, how long of a car loan can I get? The length of a car loan you can get truly depends on a multitude of personal and market factors, ranging from your credit score and down payment to the age of the vehicle and the lender’s policies. While 84-month terms are increasingly common, they come with substantial financial trade-offs that every buyer must carefully consider.

The ultimate goal isn’t to get the longest or shortest loan term, but the right loan term for your unique financial situation. By understanding the pros and cons of different loan lengths, recognizing the factors that influence your options, and strategically assessing the true cost beyond the monthly payment, you can make an empowered decision. Don’t let the excitement of a new car overshadow the importance of smart financing. Choose wisely, and drive confidently, knowing you’ve secured a loan that serves your long-term financial well-being.