How Long Of A Car Loan Can You Get: Your Ultimate Guide to Smart Auto Financing

How Long Of A Car Loan Can You Get: Your Ultimate Guide to Smart Auto Financing Carloan.Guidemechanic.com

Navigating the world of car loans can feel like deciphering a complex puzzle. One of the most critical pieces of this puzzle, and often the most misunderstood, is the loan term – essentially, how long you have to pay back the money you borrow. The length of your car loan profoundly impacts your monthly budget, the total amount you’ll pay, and your overall financial health.

So, how long of a car loan can you get? While there’s no single answer, loan terms typically range from 24 months to an increasingly common 84 months, and sometimes even longer. This comprehensive guide will break down everything you need to know about car loan lengths, helping you make an informed decision that aligns with your financial goals.

How Long Of A Car Loan Can You Get: Your Ultimate Guide to Smart Auto Financing

Understanding the right auto loan duration for your circumstances is paramount. It’s not just about securing the lowest possible monthly payment; it’s about making a strategic choice that considers both immediate affordability and long-term financial implications. Let’s dive deep into the intricacies of car loan terms and empower you to drive away with confidence.

Understanding Car Loan Terms: The Basics

Before we explore the typical lengths, let’s clarify what a car loan term actually represents. Simply put, the loan term is the agreed-upon period over which you will repay the money borrowed to purchase your vehicle, plus interest. It’s usually expressed in months.

This duration directly influences two major aspects of your auto loan: your monthly payments and the total amount of interest you’ll pay over the life of the loan. A shorter repayment period generally means higher monthly payments but less interest overall. Conversely, a longer loan term typically results in lower monthly payments, but you’ll end up paying significantly more in interest over time.

Think of it as a financial seesaw. One side holds your monthly burden, the other, your total cost. Changing the loan length shifts the balance dramatically, making it crucial to understand the trade-offs involved.

The Typical Spectrum of Car Loan Lengths

The landscape of car loan lengths has evolved considerably over the years. What was once considered a "long" loan term is now quite common. Here’s a breakdown of the typical auto loan duration options you’ll encounter:

Short-Term Loans (24-48 Months)

These are the speed demons of car loans. Short-term loans, typically ranging from two to four years, are favored by buyers who prioritize paying off their vehicle quickly and minimizing interest costs. They come with a definite set of advantages and disadvantages.

Pros:

- Significantly Less Interest: Because you’re paying off the principal balance faster, there’s less time for interest to accrue. This translates to substantial savings over the life of the loan.

- Quicker Equity Build-Up: You’ll build equity in your vehicle much faster, meaning you’ll own more of it sooner. This reduces the risk of being "upside down" on your loan, where you owe more than the car is worth.

- Faster Path to Debt Freedom: You’ll be debt-free from your car payment in a relatively short period, freeing up your monthly budget for other financial goals.

Cons:

- Higher Monthly Payments: The most significant drawback is the elevated monthly payment. Spreading the same loan amount over fewer months naturally increases the installment amount, which can strain some budgets.

- Stricter Qualification: Lenders might require a stronger credit profile or a larger down payment to approve a short-term loan, as the higher monthly payments represent a greater risk for them.

Medium-Term Loans (48-60 Months)

Often considered the "sweet spot" for many car buyers, medium-term loans strike a balance between affordability and manageable interest. These loans, spanning four to five years, have long been a popular choice.

This range offers a good compromise. Monthly payments are more approachable than short-term options, yet the total interest paid isn’t as exorbitant as with longer terms. It’s a common default for many dealerships and lenders when first presenting options.

For many buyers, a 60-month car loan term provides a comfortable balance, allowing them to afford a reliable vehicle without committing to an overly extended repayment period.

Long-Term Loans (60-84+ Months)

The trend towards longer car loan terms, particularly 72-month and 84-month options, has become increasingly prevalent. Some lenders even offer terms up to 96 months. These extended auto loan durations are primarily driven by the rising cost of vehicles and consumers’ desire for lower monthly payments.

Pros:

- Lower Monthly Payments: This is the primary appeal. Spreading the cost over a longer period drastically reduces the amount you pay each month, making more expensive vehicles seem affordable.

- Greater Financial Flexibility (Initially): The reduced monthly burden can free up cash flow for other expenses or savings in the short term.

- Access to More Expensive Vehicles: For many, a longer term is the only way to afford the car they truly want, as it brings the monthly payment into their budget.

Cons:

- Significantly More Interest Paid: This is the biggest financial hit. The longer you take to pay off the loan, the more interest accrues. You could end up paying thousands of dollars more in interest compared to a shorter term.

- Higher Risk of Negative Equity (Upside Down): Cars depreciate quickly. With a long-term loan, your car’s value can fall faster than you pay down the principal, leaving you owing more than the car is worth. This makes selling or trading in the vehicle problematic.

- Outliving the Car’s Reliability: An 84-month loan means you’ll be paying for the car for seven years. By that point, the vehicle might be experiencing significant wear and tear, requiring costly repairs while you’re still making payments.

- Prolonged Debt: Being tied to a car payment for seven or eight years can feel like an eternity, hindering your ability to save for other major life events or invest.

Based on my experience, while the lower monthly payment of a long-term loan can be tempting, it’s crucial to calculate the total cost over the loan’s life. Often, the apparent savings each month are dwarfed by the extra interest paid in the long run.

Factors That Determine Your Car Loan Length

Lenders don’t just pull loan terms out of a hat. Several key factors influence how long of a car loan you can get and the terms you’ll be offered. Understanding these elements can help you prepare and potentially secure a better deal.

Your Credit Score

Your credit score is arguably the most influential factor. It’s a numerical representation of your creditworthiness, telling lenders how likely you are to repay your debts.

- Excellent Credit (720+): With a high credit score, you’ll have access to the widest range of loan terms and the most competitive interest rates. Lenders view you as a low-risk borrower, offering greater flexibility, including options for both short and long terms.

- Good Credit (660-719): You’ll still qualify for favorable terms, though perhaps not the absolute best rates. Loan length options will still be broad.

- Fair Credit (620-659): Your options may become slightly more limited, and interest rates will be higher. Lenders might be more cautious with very long terms due to increased risk.

- Poor Credit (Below 620): Securing a car loan can be challenging. You might be offered higher interest rates and potentially shorter loan terms (to reduce lender risk) or, paradoxically, longer terms with very high rates (to make payments "affordable").

Based on my experience, a strong credit score is your best leverage. Before even stepping foot in a dealership, check your credit report and score. If it’s not where you want it to be, taking a few months to improve it can save you thousands in interest over the life of the loan.

Your Financial Health (Income & Debt-to-Income Ratio)

Lenders need to be confident that you can comfortably afford your monthly payments. They’ll look at your income and your existing debt obligations.

Your debt-to-income (DTI) ratio is particularly important. This ratio compares your total monthly debt payments (including your prospective car payment) to your gross monthly income. A high DTI suggests you’re already stretched thin, making lenders hesitant to approve a long-term loan with substantial payments. They want to see that you have enough disposable income to handle the new payment without undue financial stress.

Pro tips from us: Lenders typically prefer a DTI ratio below 43%, though some may go higher for strong applicants. Knowing your DTI beforehand can help you set realistic expectations for your loan amount and term.

The Age and Value of the Car

The vehicle itself plays a significant role in determining the maximum loan length. Lenders are wary of financing older cars for very long terms because:

- Depreciation: Cars lose value over time. Financing an older car for an extended period increases the risk of negative equity.

- Reliability: Older cars are more prone to mechanical issues. A lender doesn’t want you to default on a loan because you’re spending all your money on repairs.

For new cars, 72 or 84 months are common. For used cars, especially those over 5 years old or with high mileage, lenders may cap the loan term at 60 months or even 48 months. They often have rules like "vehicle age plus loan term cannot exceed 10-12 years."

Common mistakes to avoid are trying to secure an 84-month loan on a very old car. Most lenders will simply not approve it, or if they do, the interest rate will be prohibitive due to the perceived risk.

Your Down Payment

A larger down payment signals financial responsibility and reduces the amount you need to borrow. This can give you more flexibility in choosing your loan term.

By putting down a substantial amount, you immediately reduce the principal, which in turn lowers your monthly payments. This might allow you to opt for a shorter loan term without feeling the pinch of excessively high monthly installments. It also reduces the lender’s risk, potentially making them more amenable to longer terms if that’s your preference, or offering better rates on shorter ones.

Interest Rates

While not directly determining the length, the prevailing interest rates can influence your choice of loan length. If interest rates are high, you might be tempted to opt for a longer term to keep your monthly payments manageable. However, as discussed, this will significantly increase the total interest paid.

Conversely, if rates are low, a shorter term becomes even more appealing as the interest savings are maximized. Always consider the interest rate in conjunction with the loan term, not in isolation.

Lender Policies

Different lenders (banks, credit unions, dealership financing, online lenders) have varying policies and maximum loan terms they are willing to offer. Some credit unions, known for their consumer-friendly approaches, might offer slightly more flexible terms or better rates. Dealerships often work with a network of lenders, presenting a range of options.

It’s crucial to shop around. Don’t just settle for the first offer. Exploring different lender types can uncover more favorable loan lengths and interest rates tailored to your financial profile. For insights into securing the best financing, you might find our article on Mastering Car Loan Negotiations helpful.

The Pros and Cons of Shorter Car Loan Terms (24-48 Months)

Choosing a shorter car loan term can be a financially savvy move for those who can manage the higher monthly payments. Let’s delve into why.

Pros of Shorter Terms:

- Less Total Interest Paid: This is the most significant advantage. By paying off the loan quicker, you give the interest less time to accumulate, saving you a substantial amount of money over the life of the loan.

- Faster Ownership and Equity Build-Up: You gain full ownership of your vehicle much sooner. This also means you build equity more rapidly, reducing the risk of being "underwater" on your loan (owing more than the car is worth).

- Reduced Risk of Negative Equity: With faster principal reduction, the chances of your car depreciating below your outstanding loan balance are significantly lower. This provides financial security, especially if you need to sell the car unexpectedly.

- Quicker Path to Debt Freedom: Eliminating a car payment from your monthly budget sooner frees up funds for other financial goals, such as saving for a home, investing, or simply enjoying more disposable income.

Cons of Shorter Terms:

- Higher Monthly Payments: The primary drawback is the larger monthly installment. This requires a comfortable budget and consistent income to manage without strain.

- Potentially Harder to Qualify: Lenders assess your ability to make these higher payments. You might need a stronger credit score, a lower debt-to-income ratio, or a larger down payment to qualify for a shorter term.

The Pros and Cons of Longer Car Loan Terms (72-84+ Months)

Longer loan terms have become increasingly popular, particularly as vehicle prices continue to rise. While they offer immediate relief in terms of monthly payments, they come with substantial long-term financial trade-offs.

Pros of Longer Terms:

- Lower Monthly Payments: This is the main attraction. By stretching out the repayment period, each monthly installment becomes smaller, making more expensive vehicles seem affordable within a tight budget.

- Greater Initial Affordability: Lower payments can free up immediate cash flow for other expenses or savings, which can be appealing for those managing multiple financial commitments.

- Access to More Expensive Vehicles: For many, a long-term loan is the only viable path to purchasing a newer or more luxurious vehicle that would otherwise be out of reach with a shorter term.

Cons of Longer Terms:

- Significantly More Interest Paid: This is the most crucial financial disadvantage. The extended repayment period means interest accrues for much longer, leading to thousands of dollars in additional costs over the life of the loan. You’re effectively paying a premium for the convenience of lower monthly payments.

- Higher Risk of Negative Equity (Upside Down): Cars depreciate rapidly, especially in the first few years. With a long-term loan, your car’s value can easily fall below your outstanding loan balance, leaving you "upside down." This makes selling or trading in the vehicle difficult without coming up with extra cash.

- Potential for Costly Repairs While Still Paying: If you’re paying for a car for seven or eight years, there’s a high probability that the vehicle will require significant maintenance or repairs before the loan is fully paid off. You could be making car payments on a vehicle that is increasingly unreliable or expensive to maintain.

- Prolonged Debt Burden: Being tied to a car payment for many years can limit your financial flexibility, impacting your ability to save for other goals like a down payment on a home, retirement, or educational expenses.

Pro tips from us: Always weigh the initial payment against the long-term financial burden. A car is a depreciating asset, and extending its financing for too long can turn it into a financial liability rather than a convenience. While an 84-month car loan can make a luxury car seem affordable, the extra interest could buy you another decent used car over time.

Finding Your Ideal Car Loan Length: A Strategic Approach

There’s no one-size-fits-all answer to the question of how long of a car loan can you get or should you get. The ideal car loan length is deeply personal and depends on your unique financial situation and goals. Here’s a strategic approach to finding what works for you:

1. Assess Your Budget Honestly

Before looking at cars or loan terms, sit down and review your monthly income and expenses. What can you truly afford for a car payment without stretching yourself too thin? Be realistic. Don’t just consider the loan payment but also factor in insurance, fuel, maintenance, and potential repair costs.

A payment that feels manageable today might become a burden if unexpected expenses arise or your income changes. Aim for a payment that allows you to comfortably save and meet other financial obligations.

2. Consider the Total Cost, Not Just the Monthly Payment

This is perhaps the most crucial piece of advice. It’s easy to get fixated on the lowest monthly payment, but this can be a costly mistake. Always ask for the total amount you will pay over the life of the loan, including all interest.

Compare the total cost of a 48-month loan versus a 72-month loan for the same amount. The difference in total outlay can be startling, sometimes thousands of dollars. Prioritizing the lowest total cost will save you money in the long run.

3. Think About Your Future Plans

How long do you typically keep your cars? If you tend to trade in your vehicle every three to four years, a very long loan term might not be suitable. You could end up with negative equity when you’re ready to upgrade, making your next purchase more complicated.

If you plan to drive the car until it falls apart, a longer loan term might seem more palatable, but you still need to consider the cumulative interest and potential repair costs while still making payments.

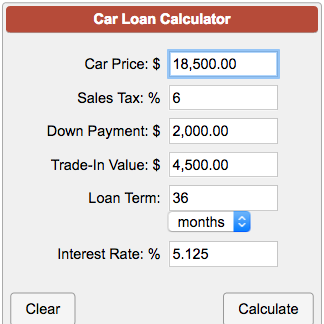

4. Run the Numbers with Online Calculators

Take advantage of the many free online car loan calculators available. These tools allow you to input different loan amounts, interest rates, and loan terms to see how they impact your monthly payment and total interest paid.

Experiment with various scenarios. For example, compare a 60-month loan at 5% interest with a 72-month loan at the same rate. This hands-on approach helps visualize the financial impact of your choices. A reliable tool for this can be found on sites like Bankrate’s Car Loan Calculator.

5. Negotiate Wisely

Remember that the advertised loan terms are not always set in stone. Your ability to negotiate on price, interest rate, and even the loan term can significantly impact your final deal. Be prepared with your own financing pre-approval from a bank or credit union before you even talk to the dealership’s finance department. This gives you leverage.

For more in-depth strategies on securing the best possible deal, consider reading our post on Unlocking the Best Car Loan Rates.

Common Mistakes to Avoid When Choosing Your Loan Term

Even with the best intentions, it’s easy to fall into common traps when deciding on a car loan length. Being aware of these pitfalls can save you from significant financial headaches down the road.

- Focusing Only on the Lowest Monthly Payment: This is by far the most prevalent mistake. While a low payment is attractive, it often comes at the expense of paying much more in interest over an extended period. Always look at the total cost of the loan.

- Ignoring the Total Interest Paid: Many buyers overlook this critical figure. The difference in total interest between a 60-month loan and an 84-month loan can be thousands of dollars, effectively adding the cost of another used car to your purchase.

- Not Considering Future Financial Changes: Life happens. A payment that seems affordable today might become a struggle if you face unexpected job loss, medical expenses, or other life changes. Building a little buffer into your budget is always wise.

- Extending the Loan Term Just to Afford a More Expensive Car: This is a classic trap. If you need an 84-month loan to afford the monthly payment on a car, it’s likely that the car is simply beyond your true budget. Opting for a less expensive car with a shorter, more manageable term is often a smarter financial decision.

- Not Shopping Around for Different Lenders: Accepting the first loan offer, especially from a dealership, can cost you. Different lenders have different rates and terms based on their risk assessment and business models. Always get pre-approvals from at least two to three different sources (banks, credit unions, online lenders) before finalizing your purchase.

- Believing a Longer Loan Protects Against Depreciation: Some people think that by extending the loan, they’re somehow cushioning the blow of depreciation. In reality, a longer loan term exacerbates the problem, increasing the likelihood of negative equity.

Common mistakes to avoid are falling into the trap of "payment shopping," where you only compare monthly payments without looking at the bigger financial picture. This can lead to a long-term financial burden that outweighs any initial convenience.

Pro Tips for Optimizing Your Car Loan

Beyond choosing the right loan length, there are several strategies you can employ to ensure you get the best possible car loan terms.

- Boost Your Credit Score Before Applying: A higher credit score translates directly into lower interest rates and more flexible loan terms. Pay down existing debts, make all payments on time, and avoid opening new credit accounts in the months leading up to your car purchase.

- Save for a Significant Down Payment: Aim for at least 10-20% of the car’s purchase price. A larger down payment reduces the amount you need to borrow, lowers your monthly payments, builds equity faster, and makes you a more attractive borrower to lenders.

- Get Pre-Approved from Multiple Lenders: Don’t wait until you’re at the dealership to think about financing. Get pre-approved by several banks, credit unions, or online lenders beforehand. This gives you a concrete offer to compare against dealer financing and provides leverage in negotiations.

- Consider Refinancing if Your Financial Situation Improves: If you initially took out a long-term loan with a higher interest rate due to credit issues or a small down payment, you might be able to refinance your car loan later. If your credit score has improved or interest rates have dropped, refinancing can secure you a lower rate or a shorter term, saving you money.

- Understand All Fees and Charges: Beyond the interest rate and principal, be aware of any origination fees, documentation fees, or other charges that can add to the total cost of your loan. Ask for a full breakdown of all costs.

Conclusion

Determining how long of a car loan you can get and, more importantly, should get is a critical decision that impacts your financial well-being for years. While extended loan terms offer the allure of lower monthly payments, they often come at a significant cost in the form of increased total interest and a higher risk of negative equity.

The ideal car loan length strikes a balance between manageable monthly payments and minimizing the total cost of ownership. It requires an honest assessment of your budget, a clear understanding of your financial goals, and a willingness to shop around for the best terms. Remember, a car is a depreciating asset, and thoughtful financing ensures it remains a convenience, not a long-term financial burden.

By applying the strategies and insights shared in this guide, you can confidently navigate the complexities of car financing and choose a loan term that puts you on the road to financial success. Drive smart, not just far!