How Many Points Will A Car Loan Lower My Credit? Unpacking the Real Impact on Your Score

How Many Points Will A Car Loan Lower My Credit? Unpacking the Real Impact on Your Score Carloan.Guidemechanic.com

Getting a new car is an exciting milestone. The thrill of picking out your dream vehicle, the smell of a fresh interior, and the anticipation of hitting the open road are all part of the experience. But before you drive off the lot, there’s a crucial question many prospective buyers ponder: "How many points will a car loan lower my credit?"

It’s a valid concern, and one that deserves a thorough, in-depth explanation. While it’s true that applying for a car loan can cause a temporary dip in your credit score, the exact number of points isn’t a fixed figure. Instead, it’s a dynamic interplay of various factors that determine the precise impact. As an expert in personal finance and credit, I’m here to demystify this process, help you understand what to expect, and show you how to navigate it smartly.

How Many Points Will A Car Loan Lower My Credit? Unpacking the Real Impact on Your Score

This comprehensive guide will not only answer your core question but also equip you with the knowledge to minimize negative effects and even use a car loan to improve your credit over time. Let’s dive in!

Demystifying Your Credit Score: The Foundation

Before we can discuss how a car loan affects your credit, it’s essential to understand what a credit score is and why it matters. Think of your credit score as your financial report card – a three-digit number that lenders use to assess your creditworthiness.

This score tells them how risky it might be to lend you money. A higher score indicates a lower risk, making you eligible for better interest rates and more favorable loan terms. Conversely, a lower score suggests higher risk, potentially leading to higher interest rates or even loan denial.

The Two Main Players: FICO and VantageScore

While you might hear "credit score" used generally, there are actually several different scoring models. The two most common are FICO Score and VantageScore. Both range from 300 to 850, with higher numbers indicating better credit.

- FICO Score: This is the most widely used scoring model, developed by the Fair Isaac Corporation. Most lenders rely on FICO scores for their lending decisions.

- VantageScore: This is a newer model created by the three major credit bureaus (Equifax, Experian, and TransUnion). It’s also gaining popularity and can be found on many free credit monitoring services.

While the exact algorithms differ, both models consider similar underlying factors. Understanding these factors is key to grasping how a car loan can influence your score.

The Initial Hit: The Hard Inquiry

The very first step in applying for a car loan that impacts your credit is the hard inquiry. When a lender checks your credit to decide if they’ll approve your loan, they initiate a "hard pull" on your credit report.

This action is recorded on your credit file and signals to other lenders that you are actively seeking new credit. It’s an essential part of the lending process, but it does carry a minor, temporary penalty.

How Many Points Does a Hard Inquiry Typically Drop?

Based on my experience, a single hard inquiry typically lowers your credit score by a small margin, usually between 2 to 5 points. For some individuals with very extensive credit histories, the impact might be even less, or even negligible.

The exact number isn’t fixed because it depends on your overall credit profile. If you have a long, pristine credit history with very few inquiries, a single new inquiry will likely have a minimal effect. However, if you already have several recent inquiries or a shorter credit history, the impact might be slightly more noticeable.

The "Shopping Window" for Auto Loans: A Crucial Detail

Here’s a crucial pro tip from us: credit scoring models understand that consumers shop around for the best interest rates on major loans like car loans and mortgages. To prevent your score from being unduly penalized for comparing offers, they’ve implemented a "shopping window."

This means that multiple hard inquiries for the same type of loan (e.g., auto loans) within a specific timeframe are often treated as a single inquiry. This window typically ranges from 14 to 45 days, depending on the scoring model (FICO models often use 45 days, while older versions might use 14). So, if you apply for five car loans within a two-week period, it will likely only count as one inquiry for scoring purposes. This is incredibly valuable for securing the best rates without tanking your score.

The Impact of New Credit: Beyond the Inquiry

While the hard inquiry is the immediate credit event, the new car loan itself, once approved, also influences your score in several ways. These effects are often more significant and longer-lasting than the initial inquiry.

1. New Account Opening

When you open a new credit account, like a car loan, it’s reflected on your credit report. This new account temporarily lowers the average age of all your credit accounts.

Credit scoring models generally favor a longer average age of accounts, as it demonstrates a proven track record of managing credit responsibly over time. A newer account can slightly dilute this average, leading to a small dip.

2. Credit Mix

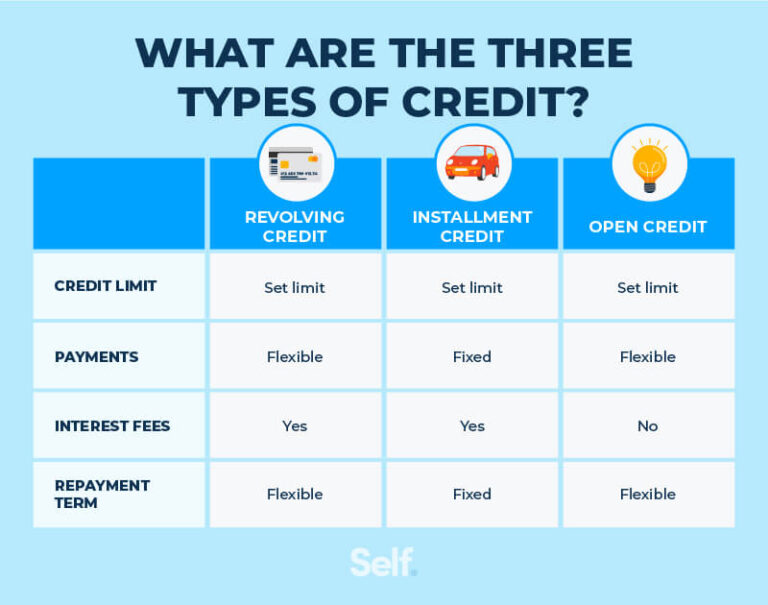

A car loan is typically an installment loan, meaning you borrow a fixed amount and repay it over a set period with regular, equal payments. If your credit history primarily consists of revolving credit (like credit cards), adding an installment loan can actually be beneficial for your credit mix.

Having a diverse mix of credit types (both revolving and installment) is viewed positively by credit scoring models. It shows you can handle different kinds of credit responsibly, which can eventually boost your score. However, this positive effect usually takes time to manifest, after you’ve demonstrated consistent payments.

3. Increased Debt Load

Taking on a car loan means you’re adding a new debt obligation to your financial profile. While not inherently negative, lenders look at your overall debt-to-income ratio.

A significant increase in your debt load, especially if your income hasn’t changed, could be seen as an increased risk. This factor is more about your ability to manage the payments rather than the loan itself, but it can subtly influence how future lenders view you.

The Five Pillars of Your Credit Score: Where a Car Loan Fits In

To truly understand how many points a car loan will lower your credit, we need to look at the five main components that make up your FICO score. These categories, and their approximate weighting, are:

- Payment History (35%): Your track record of paying bills on time.

- Amounts Owed (30%): How much debt you carry relative to your available credit.

- Length of Credit History (15%): How long your credit accounts have been open.

- New Credit (10%): The number of recent credit inquiries and new accounts.

- Credit Mix (10%): The types of credit accounts you have.

Let’s break down how a car loan specifically impacts each of these crucial categories.

1. Payment History (35%)

This is by far the most significant factor. When you take out a car loan, your ability to make on-time payments becomes paramount.

- Initial Impact: A new loan itself doesn’t affect your payment history initially.

- Long-Term Impact: Every on-time payment you make builds a positive payment history. This is where a car loan can dramatically improve your score over the long term. Conversely, a single missed payment can drop your score by dozens of points and severely damage your credit.

2. Amounts Owed (30%)

This category looks at your total debt and how much of your available credit you’re using. For revolving credit (like credit cards), this is your credit utilization ratio.

- Initial Impact: An installment loan like a car loan adds to your total outstanding debt but doesn’t directly factor into credit utilization in the same way revolving credit does. However, it does increase your overall debt burden.

- Long-Term Impact: As you pay down your car loan, the outstanding balance decreases. This reduction in your total debt can be viewed positively by scoring models over time, especially as you approach the end of the loan term.

3. Length of Credit History (15%)

Lenders like to see a long history of responsible credit use. The average age of your accounts is a key metric here.

- Initial Impact: Opening a brand new car loan account will decrease the average age of all your accounts. This is a common reason for a small, temporary dip in your score.

- Long-Term Impact: As the car loan ages and you continue to make payments, it contributes positively to the length of your credit history. The older your accounts, the better.

4. New Credit (10%)

This category specifically assesses how often you apply for and open new credit accounts.

- Initial Impact: This is where the hard inquiry and the opening of a new account have their primary negative effect. As mentioned, a hard inquiry can cause a small drop (2-5 points), and having a new account lowers your average account age.

- Long-Term Impact: The negative impact of new credit fades over time. Hard inquiries typically stay on your report for two years but only affect your score for about a year. As the new car loan ages, it transitions from "new credit" to an established account contributing to your history.

5. Credit Mix (10%)

This factor evaluates whether you have a healthy mix of different types of credit.

- Initial Impact: If you previously only had credit cards, adding an installment loan like a car loan can actually be a positive for your credit mix, potentially offsetting some of the other negative impacts.

- Long-Term Impact: A diversified credit portfolio is seen as a sign of financial maturity. A car loan helps build this diversity, especially if you manage it well.

The Aftermath: How a Car Loan Can Improve Your Credit (Eventually)

While the initial impact of a car loan on your credit score might be a slight decrease, the long-term potential for improvement is significant. A car loan, when managed responsibly, is an excellent tool for building a strong credit profile.

Consistent On-Time Payments

This is the most powerful way a car loan can boost your score. Every single payment you make on time, month after month, reinforces a positive payment history. This consistent behavior demonstrates reliability to lenders, which is precisely what credit scores are designed to measure.

Building a Positive Credit History

Over the years, as your car loan matures, it becomes a long-standing account with a history of on-time payments. This adds depth and stability to your credit file, signaling to future lenders that you are a dependable borrower. It becomes a valuable part of your credit story.

Diversifying Your Credit Mix

As discussed, adding an installment loan to a credit profile that might have primarily consisted of revolving credit (like credit cards) can be a positive step. It shows you can manage different types of debt responsibly, which is a big plus for your credit mix component.

Based on my experience, many individuals who diligently make their car loan payments see their scores rebound and even surpass their pre-loan levels within 6-12 months. This assumes no other negative credit events occur during that time.

Pro Tips for Minimizing the Credit Score Impact

You can’t completely avoid the initial credit score dip when getting a car loan, but you can certainly minimize it. Here are some strategies based on years of helping people navigate these waters:

- Check Your Credit Report Beforehand: Before you even step foot in a dealership, pull your free credit reports from AnnualCreditReport.com. Look for errors, identify areas for improvement, and understand your current standing. This empowers you to negotiate better.

- Shop Within a Short Window: Utilize the auto loan "shopping window" to your advantage. Get all your loan inquiries done within a 14-45 day period. This ensures multiple checks only count as a single hard inquiry.

- Know Your Budget and Borrow Responsibly: Only apply for a loan amount you are confident you can comfortably repay. Taking on too much debt is a common mistake that leads to missed payments and significant credit damage. Use online calculators to estimate your monthly payments.

- Avoid Applying for Other Credit Simultaneously: Try not to apply for a new credit card, personal loan, or mortgage around the same time you’re getting a car loan. Multiple inquiries for different types of credit will not be grouped and will have separate, individual impacts on your score.

- Make On-Time Payments from Day One: This is non-negotiable. Set up automatic payments or calendar reminders to ensure you never miss a due date. Even one late payment can cause a substantial drop in your score and incur late fees.

- Maintain Low Credit Card Utilization: Keep your credit card balances low (ideally below 30% of your credit limit) before and after applying for the car loan. This demonstrates responsible credit management and can help offset the new debt.

- Consider a Co-signer (If Necessary and Strategic): If your credit isn’t great, a co-signer with excellent credit might help you get approved or secure a better rate. However, remember that the co-signer is equally responsible for the debt, and any missed payments will affect their credit too.

Common Mistakes to Avoid When Getting a Car Loan

Understanding what to do is important, but knowing what not to do is equally vital for protecting your credit.

- Applying Everywhere: Don’t let every dealership "run your credit" just to see what they can offer. This leads to numerous hard inquiries that won’t be grouped and will collectively hurt your score more. Be strategic about where you apply.

- Missing Payments: This is the cardinal sin of credit management. A single missed payment can plummet your score by 50-100 points or more, and the negative mark stays on your report for seven years.

- Ignoring Your Credit Report: Don’t assume everything is accurate. Regularly monitor your credit report for errors or fraudulent activity. An incorrect late payment or an account you didn’t open can severely damage your score. (For more on this, check out our guide on How to Dispute Errors on Your Credit Report).

- Taking on More Debt Than You Can Handle: Just because you’re approved for a certain loan amount doesn’t mean you should take it. Overextending yourself financially increases the risk of missed payments and financial stress.

- Closing Old Credit Accounts: While a new car loan adds to your accounts, avoid closing old, unused credit cards, especially if they have a long history. Closing them can reduce your overall available credit and shorten your average account age, negatively impacting your score.

Real-World Scenarios: Visualizing the Impact

Let’s look at a few hypothetical scenarios to illustrate how the impact can vary.

Scenario 1: The Responsible Borrower with Good Credit

- Profile: FICO score 750, long credit history, low credit card utilization, few recent inquiries.

- Action: Applies for one car loan, gets approved.

- Initial Impact: Hard inquiry drops score by 2-3 points. New account slightly lowers average account age.

- Long-Term Outcome: After 6-12 months of consistent on-time payments, the score rebounds and likely increases to 760-770 as the payment history strengthens and credit mix improves.

Scenario 2: The Borrower with Fair Credit Seeking Improvement

- Profile: FICO score 650, shorter credit history, some revolving debt, perhaps one or two past late payments.

- Action: Applies for a car loan, gets approved, potentially with a higher interest rate.

- Initial Impact: Hard inquiry drops score by 5-7 points (due to a less robust history). New account has a more noticeable effect on average age.

- Long-Term Outcome: If the borrower makes all payments on time for a year or more, their score could significantly increase, potentially by 20-40 points, as the positive payment history outweighs the initial negative impacts and helps establish new, positive credit.

Scenario 3: The Uninformed Borrower Making Mistakes

- Profile: FICO score 700, moderate credit history.

- Action: Applies at five different dealerships over two months, then gets a car loan, and misses two payments in the first six months.

- Initial Impact: Multiple inquiries (not grouped due to extended time) drop score by 10-15 points. New account adds to this.

- Long-Term Outcome: The missed payments are devastating. Their score could drop by 50-100+ points, erasing any positive impact and significantly damaging their credit for years.

As you can see, the initial dip is generally minor. It’s your subsequent behavior that truly dictates the long-term trajectory of your credit score after securing a car loan.

External Resource: Understanding Your Rights

It’s crucial to understand your rights regarding credit reporting. The Consumer Financial Protection Bureau (CFPB) offers valuable resources and information on credit scores, reports, and how to protect yourself. You can learn more about your credit rights and how to get your free credit reports at their official website: Consumer Financial Protection Bureau (CFPB) – Credit Reports & Scores.

Conclusion: A Temporary Dip for Long-Term Gain

So, how many points will a car loan lower your credit? The short answer is typically a small, temporary dip of 2 to 7 points due to the hard inquiry and the opening of a new account. However, this is just the beginning of the story.

The more important takeaway is that a car loan is a powerful tool for credit building. By understanding how your credit score works, applying strategically within the shopping window, and most importantly, making every single payment on time, you can quickly recover any initial score dip and actually use the loan to significantly boost your credit over time.

Don’t let the fear of a minor credit score fluctuation deter you from securing a car loan that meets your needs. Instead, empower yourself with knowledge, act responsibly, and turn your car loan into a stepping stone towards a stronger, healthier financial future. Your credit score is a dynamic entity, and with careful management, you’re always in the driver’s seat. Remember, consistent financial discipline is the ultimate key to credit success.