How Many Years Is A Typical Car Loan? Unpacking the Auto Financing Puzzle

How Many Years Is A Typical Car Loan? Unpacking the Auto Financing Puzzle Carloan.Guidemechanic.com

Buying a car is an exciting milestone, but navigating the world of auto financing can feel like a complex journey through a dense forest. One of the most common questions that car buyers grapple with is: "How many years is a typical car loan?" It’s a seemingly simple query with a surprisingly nuanced answer, one that profoundly impacts your monthly budget, the total cost of your vehicle, and your financial freedom.

As an expert blogger and professional SEO content writer who has spent years dissecting consumer finance, I’m here to demystify car loan terms for you. This comprehensive guide will not only tell you what’s typical but will also equip you with the knowledge to make the smartest decision for your unique financial situation. Our goal is to empower you to drive off the lot with confidence, knowing you’ve secured a deal that truly works for you. Let’s dive deep into the world of auto loan durations.

How Many Years Is A Typical Car Loan? Unpacking the Auto Financing Puzzle

The Evolving Landscape of Car Loan Terms

For decades, the standard car loan term hovered around 48 to 60 months, or four to five years. This was the widely accepted norm, striking a balance between manageable monthly payments and reasonable total interest paid. However, the automotive financing landscape has shifted considerably over the past few years, driven by a desire for lower monthly payments and the increasing cost of vehicles.

Based on my experience observing market trends, we’ve seen a noticeable lengthening of car loan terms. Lenders, in their effort to make more expensive vehicles accessible to a wider range of buyers, began offering longer repayment periods. What was once considered an extended term – say, 72 months – has become increasingly common, and even 84-month (seven-year) loans are now a regular feature in the market. This evolution is crucial to understand as you approach your own car purchase, as it directly influences what constitutes "typical" today.

So, How Many Years IS a Typical Car Loan?

Let’s get straight to the heart of the matter. While the term "typical" can be subjective and vary based on market conditions, vehicle type, and buyer creditworthiness, we can provide a clear range based on current industry data and common practice.

New Car Loans

For new cars, the most common loan terms currently fall within the 60 to 72 months (5 to 6 years) range. Many buyers are opting for these longer durations to keep their monthly payments more affordable, especially with the rising average price of new vehicles. While 48-month loans are still available and often advisable for those who can afford the higher monthly outlay, they are less "typical" in terms of sheer volume than their longer counterparts.

However, it’s not uncommon to see new car loans stretching out to 84 months (7 years). This extended term provides the lowest possible monthly payment, making higher-end models more accessible. The downside, as we’ll explore later, is a significantly higher total interest paid over the life of the loan.

Used Car Loans

When it comes to used cars, loan terms tend to be slightly shorter than for new vehicles, primarily due to the depreciation curve and the vehicle’s age. A typical used car loan term usually ranges from 48 to 60 months (4 to 5 years).

You might find some lenders offering 72-month terms for newer used cars, perhaps those that are only a year or two old. However, it’s rare to see 84-month terms on used vehicles, particularly older ones, because the risk of the car’s value declining faster than the loan balance (known as negative equity) becomes much higher for the lender. The older the car, the shorter the maximum loan term a lender is usually willing to offer.

The Critical Factors Influencing Your Car Loan Term

Choosing the right car loan term isn’t a one-size-fits-all decision. Several key factors play a pivotal role in determining what loan terms are available to you and which one makes the most financial sense. Understanding these elements is crucial for making an informed choice.

Your Credit Score

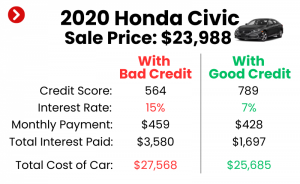

Your credit score is arguably the most significant factor influencing not only the interest rate you qualify for but also the range of loan terms available. Lenders view a higher credit score (generally 700+) as an indicator of lower risk. This means you’ll likely be offered the most favorable interest rates and a wider selection of loan terms, including shorter options with competitive rates.

Conversely, a lower credit score might limit your options. Lenders may offer higher interest rates and potentially restrict you to shorter terms to mitigate their risk, or conversely, push longer terms to make the high monthly payments associated with a higher interest rate more palatable. Pro tips from us: always check your credit score before applying for a car loan. It gives you leverage and helps you understand what to expect.

The Vehicle’s Age and Value

As touched upon earlier, the age and value of the car itself are significant determinants. New cars, with their higher price tags and slower initial depreciation, often qualify for longer loan terms. Lenders are more comfortable financing a brand-new vehicle for 72 or even 84 months because its value holds relatively well in the early years.

For used cars, especially older models, the loan terms tend to be shorter. This is because older vehicles depreciate faster, and the risk of mechanical issues increases. Lenders want to ensure that the loan balance doesn’t exceed the car’s market value for too long, protecting their investment. Common mistakes to avoid are trying to stretch a loan for an old car too long; you’ll likely end up "upside down" on your loan.

Your Financial Health and Budget

Ultimately, your personal financial situation should dictate your choice of loan term. Can you comfortably afford a higher monthly payment that comes with a shorter term, thus saving a substantial amount on interest? Or do you need the flexibility of a lower monthly payment, even if it means paying more overall?

Based on my experience helping countless individuals budget, it’s vital to assess your current income, fixed expenses, and any other debt obligations before committing to a car payment. Don’t just consider the car payment in isolation; think about how it fits into your entire financial picture. A car payment should not strain your budget to the point where it impacts your ability to save or cover other essential expenses.

Down Payment

The size of your down payment directly impacts the amount you need to borrow, which in turn influences the loan terms available and your monthly payments. A larger down payment reduces the principal loan amount, making it easier to qualify for a shorter term with a manageable monthly payment.

A significant down payment also helps reduce the risk of negative equity, where you owe more on the car than it’s worth. This financial cushion can give you more flexibility in choosing a term that benefits you, rather than one forced by a high loan amount.

Interest Rates

The prevailing interest rates at the time of your purchase will also factor into your decision. When interest rates are low, the impact of a longer loan term on total interest paid is less severe, making longer terms more attractive. Conversely, when rates are high, opting for a shorter term becomes even more financially advantageous to minimize the overall cost of borrowing. Always consider the interest rate in conjunction with the loan term.

Short vs. Long Car Loan Terms: A Deep Dive

The choice between a short and a long car loan term is one of the most critical decisions you’ll make in the financing process. Each option comes with its own set of advantages and disadvantages that can significantly impact your financial well-being. Let’s explore them in detail.

The Case for Shorter Loan Terms (e.g., 36-48 months)

Opting for a shorter loan term, typically between three and four years, is often the financially savviest choice if your budget allows for the higher monthly payments.

Pros of Shorter Loan Terms:

- Significantly Lower Total Interest Paid: This is the most compelling advantage. By paying off your loan quicker, you reduce the amount of time interest accrues, leading to substantial savings over the life of the loan. You could save thousands of dollars by choosing a 48-month term over a 72-month term, even with the same interest rate.

- Faster Equity Build-Up: Your car depreciates rapidly, especially in the first few years. With a shorter loan term, you pay down the principal balance much faster, meaning you build equity in your vehicle more quickly. This reduces the risk of being "upside down" on your loan.

- Less Risk of Negative Equity: Negative equity occurs when you owe more on your car than it’s worth. Shorter terms drastically reduce this risk, which is a major advantage if you need to sell or trade in your car before the loan is fully paid off. You’ll have more flexibility and less financial burden.

- Quicker Financial Freedom: Imagine having no car payment after three or four years! A shorter term means you’ll be debt-free sooner, freeing up a significant portion of your monthly budget for other financial goals, such as saving, investing, or paying down other debts.

- Reduced Long-Term Maintenance Costs: You’re more likely to pay off the car while it’s still under its manufacturer’s warranty. This means you’ll enjoy a period of ownership with no car payments and potentially fewer major repair costs.

Cons of Shorter Loan Terms:

- Higher Monthly Payments: This is the primary drawback. To pay off the loan quicker, your monthly payments will be significantly higher, which might strain your budget. This is why it’s crucial to assess your financial health realistically.

The Appeal of Longer Loan Terms (e.g., 60-84 months)

Longer loan terms, typically five to seven years, have become increasingly popular due to their perceived affordability. They make more expensive cars accessible by spreading the cost over a longer period.

Pros of Longer Loan Terms:

- Lower Monthly Payments: The most attractive feature of longer terms is the reduced monthly payment. This makes it easier to fit a car payment into a tight budget and allows buyers to afford more expensive vehicles or models with more features.

- Greater Affordability: For many, a longer term is the only way to afford the car they need or want, particularly with rising vehicle prices. It opens up options that would otherwise be out of reach.

- Flexibility in Budgeting: Lower monthly payments can free up cash flow for other expenses or savings, which can be beneficial if you have other financial priorities or an unpredictable income.

Cons of Longer Loan Terms:

- Significantly Higher Total Interest Paid: This is the biggest financial penalty. Over an extended period, the interest accrues for longer, leading to thousands of dollars in additional costs compared to a shorter term. This is often the hidden cost that buyers overlook.

- Slower Equity Build-Up and Higher Risk of Negative Equity: With a longer term, you’ll be "upside down" on your loan for a longer period. The car’s value depreciates faster than you pay down the principal, leaving you in a precarious position if you need to sell or trade in the car early.

- Potential for More Repairs After Warranty: Many longer loans extend beyond the typical manufacturer’s warranty period. This means you could still be making car payments while simultaneously facing costly out-of-pocket repairs, a common frustration for owners of older vehicles.

- Higher Insurance Costs (in some cases): If you’re in negative equity, your lender will likely require comprehensive and collision coverage, even if you might otherwise drop it on an older, fully paid-off car.

- Delayed Financial Freedom: You’ll be tied to a car payment for a much longer time, delaying your ability to allocate those funds to other important financial goals.

Common Mistakes to Avoid When Choosing a Loan Term

Based on my experience advising consumers, certain pitfalls consistently trip up car buyers. Steering clear of these common mistakes will save you money and stress in the long run.

Focusing Only on Monthly Payment

This is perhaps the biggest and most detrimental mistake. While a low monthly payment is appealing, fixating solely on it can lead you down a path of financial regret. Lenders often highlight the lowest possible monthly payment to make a deal seem attractive, but this usually involves stretching the loan term to its maximum.

Always ask to see the total cost of the loan, including all interest, over different terms. A slightly higher monthly payment for a shorter term can result in thousands of dollars saved over the life of the loan.

Ignoring Total Cost

Closely related to the above, many buyers fail to calculate the total amount they will pay over the entire loan term. It’s not just the sticker price of the car; it’s the principal amount plus all the interest. A $30,000 car financed over 84 months at a moderate interest rate can easily end up costing you well over $35,000 or even $40,000 in total.

Always perform this calculation or ask your lender to provide it clearly. This transparency is key to making an informed decision.

Overlooking Depreciation

Cars are depreciating assets, meaning their value decreases over time. Most cars lose a significant chunk of their value in the first few years. If your loan term is too long, you risk being "underwater" or having negative equity for a substantial period. This happens when the amount you owe on the car is more than its market value.

This becomes a major problem if your car is totaled, stolen, or if you need to sell or trade it in. You’ll still owe the difference, which can be a significant financial burden. Consider GAP (Guaranteed Asset Protection) insurance if you opt for a longer term, but ideally, avoid the situation altogether.

Not Shopping Around

Many buyers make the mistake of only getting financing offers from the dealership. While dealerships can sometimes offer competitive rates, it’s crucial to shop around with multiple lenders – banks, credit unions, and online lenders – before you even set foot on the lot.

This allows you to compare offers, understand the best interest rates and terms available to you, and walk into the dealership with pre-approval in hand. This gives you leverage and helps ensure you get the best possible deal.

Pro Tips for Choosing the Right Car Loan Term

Making the right decision about your car loan term requires careful consideration and a proactive approach. Here are some pro tips from us to guide you:

Assess Your Budget Realistically

Before you even start car shopping, sit down and honestly evaluate your financial situation. How much can you truly afford each month for a car payment without sacrificing other financial goals or necessities? Don’t just think about the payment; factor in insurance, fuel, maintenance, and potential repair costs.

Consider the Vehicle’s Lifespan

Think about how long you realistically plan to keep the car. If you typically trade in your vehicle every 3-4 years, then a 60-month or 72-month loan term might not make sense, as you’ll likely still owe money when you’re ready for a new one. Align your loan term with your ownership horizon.

Aim for a Sweet Spot

While shorter terms are generally better financially, a 36-month loan might result in unmanageably high payments. For many, a 48-to-60-month term offers a good balance between manageable monthly payments and reasonable total interest paid. It’s a common "sweet spot" that minimizes financial risk while keeping costs in check.

Factor in Resale Value

Some cars hold their value better than others. If you’re buying a vehicle known for strong resale value, you might have more flexibility with a slightly longer loan term, as the risk of negative equity is somewhat reduced. However, this shouldn’t be the sole determining factor.

Don’t Forget About Refinancing

Even if you initially take out a longer loan term for affordability, remember that you can often refinance your car loan later. If your credit score improves, or if interest rates drop, you might be able to secure a new loan with a lower interest rate or a shorter term, saving you money. For more insights on improving your financial standing, you might find our article on Understanding Your Credit Score: Your Key to Better Loans helpful.

Beyond the Term: Other Car Loan Considerations

While the loan term is a major piece of the puzzle, several other elements work in conjunction to determine the overall cost and suitability of your car loan.

Interest Rates and APR

The Annual Percentage Rate (APR) is the true cost of borrowing, encompassing the interest rate plus any other fees. A lower APR directly translates to less money paid over the life of the loan. Always compare APRs from different lenders, not just the quoted interest rate. Even a slight difference can save you hundreds, if not thousands, of dollars.

Down Payments

A robust down payment is your best friend in car financing. It reduces the amount you need to borrow, which lowers your monthly payments and the total interest paid. More importantly, it helps you establish equity in the vehicle from day one, mitigating the risk of being upside down. Aim for at least 10-20% of the vehicle’s purchase price, if possible.

Trade-Ins

If you have a vehicle to trade in, its value acts like a down payment. Ensure you research your current car’s trade-in value beforehand using reputable sources like Kelley Blue Book or Edmunds. Don’t let the dealership undervalue your trade-in, as this directly impacts your new loan.

Extended Warranties and Add-ons

Be extremely cautious with extended warranties, paint protection, fabric guards, and other add-ons offered by the dealership. While some might offer legitimate value, many are highly profitable for the dealer and can inflate your loan amount unnecessarily. If you roll these into your car loan, you’ll be paying interest on them for the entire loan term, significantly increasing their cost. Always evaluate them separately and negotiate fiercely.

For official guidance on consumer auto finance, you can consult trusted external resources like the Consumer Financial Protection Bureau (CFPB) at consumerfinance.gov.

Future-Proofing Your Car Purchase

A smart car purchase isn’t just about the present; it’s about setting yourself up for financial success in the future.

Building an Emergency Fund

Before committing to a car loan, ensure you have an adequate emergency fund. This fund can be a lifesaver if you face unexpected repairs, a job loss, or other financial setbacks. Without it, even a manageable car payment can quickly become a burden.

Regularly Reviewing Your Loan

Don’t just set it and forget it. Periodically review your car loan. Are interest rates lower now? Has your credit score improved? If so, consider refinancing to potentially reduce your interest rate or shorten your term. Even small changes can make a big difference over time. Also, being prepared before you even start the buying process can make a huge difference in the final price. Our article on Tips for Negotiating Car Prices Like a Pro offers valuable strategies.

Conclusion

Understanding "How many years is a typical car loan?" is more than just knowing an average; it’s about grasping the intricate financial implications behind that number. While 60 to 72 months for new cars and 48 to 60 months for used cars are currently the most common terms, "typical" doesn’t always mean "optimal" for your personal finances.

Making an informed decision requires looking beyond the allure of a low monthly payment. It demands a realistic assessment of your budget, a keen awareness of total interest costs, and an understanding of how loan terms impact equity and long-term financial health. By considering all the factors discussed, avoiding common mistakes, and leveraging our pro tips, you can choose a car loan term that aligns with your financial goals, ensuring you drive away with confidence and peace of mind. What’s your ideal car loan term? Share your thoughts in the comments below!