How Much Can I Borrow for a Car Loan? Your Ultimate Guide to Unlocking Your Automotive Dreams

How Much Can I Borrow for a Car Loan? Your Ultimate Guide to Unlocking Your Automotive Dreams Carloan.Guidemechanic.com

Dreaming of a new set of wheels? Whether it’s a sleek sedan, a rugged SUV, or an eco-friendly electric vehicle, one of the first and most critical questions that comes to mind is often: "How much can I borrow for a car loan?" This isn’t just a simple number; it’s a complex interplay of personal financial factors, market conditions, and lender policies.

As an expert blogger and professional SEO content writer, I understand the importance of not just getting a car, but getting the right car for your budget. This comprehensive guide will demystify the process, helping you understand the key determinants of your car loan borrowing power. We’ll dive deep into each factor, offering practical advice, insider tips, and common pitfalls to avoid, ensuring you approach your car purchase with confidence and clarity.

How Much Can I Borrow for a Car Loan? Your Ultimate Guide to Unlocking Your Automotive Dreams

Beyond the Sticker Price: Understanding Your True Borrowing Power

When you start exploring car loans, it’s easy to focus solely on the vehicle’s price tag. However, your ability to secure a loan, and more importantly, an affordable loan, hinges on several critical components. Lenders assess your financial health to determine how much risk you represent, which directly impacts the loan amount they are willing to offer and the interest rate they’ll charge.

Knowing your borrowing capacity before you step onto a dealership lot is a game-changer. It empowers you to negotiate effectively, prevents you from falling in love with a car you can’t truly afford, and ultimately saves you money in the long run. Let’s break down the core factors that influence how much you can borrow for a car loan.

1. Your Credit Score: The Cornerstone of Your Loan Application

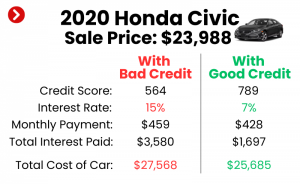

Your credit score is arguably the most significant factor lenders consider. It’s a three-digit number that represents your creditworthiness, essentially a snapshot of how reliably you’ve managed debt in the past. A higher score signals to lenders that you are a lower risk borrower, making them more inclined to offer you a larger loan at a more favorable interest rate.

Why It Matters So Much: Lenders use your credit score to predict the likelihood of you repaying your loan on time. A strong credit history, reflected by a high score (generally 700+), often translates into lower interest rates, which can save you thousands of dollars over the life of the loan. Conversely, a lower score might lead to higher interest rates or even a rejection of your loan application.

What’s Considered a Good Score? While scores range from 300 to 850, a FICO score of 670-739 is generally considered "good," 740-799 is "very good," and 800+ is "exceptional." Based on my experience, aiming for at least a "good" score can significantly improve your car loan terms. If your score is lower, it doesn’t mean you can’t get a loan, but you might pay a premium in interest.

How to Improve Your Credit Score: Before applying for a car loan, take steps to boost your score. Pay bills on time, reduce existing debt, and avoid opening new credit accounts. Regularly check your credit report for errors, as even small inaccuracies can negatively impact your score.

2. Your Income and Employment Stability

Lenders need assurance that you have a consistent source of income to make your monthly car loan payments. Your income level and the stability of your employment history play a crucial role in determining how much you can borrow. They want to see that you have the financial capacity to comfortably manage the new debt.

Proof of Income: You’ll typically need to provide proof of income, such as recent pay stubs, tax returns, or bank statements. Self-employed individuals might need more extensive documentation to demonstrate stable earnings. The higher and more stable your income, the more comfortable lenders will be in extending a larger loan amount.

Employment History: Lenders also look at your employment history. A long, consistent work history with the same employer or within the same industry signals stability. Frequent job changes, especially within a short period, might raise concerns about your income consistency, potentially limiting your borrowing options.

3. Your Debt-to-Income (DTI) Ratio

Your Debt-to-Income (DTI) ratio is a crucial metric that lenders use to assess your ability to manage additional debt. It’s calculated by dividing your total monthly debt payments by your gross monthly income. This ratio helps lenders understand how much of your income is already committed to existing debts, such as mortgage, student loans, or credit card payments.

How to Calculate Your DTI: Sum up all your monthly debt payments (e.g., rent/mortgage, minimum credit card payments, student loans, personal loans). Then, divide that total by your gross monthly income (your income before taxes and deductions). For example, if your monthly debt payments are $1,000 and your gross monthly income is $4,000, your DTI is 25% ($1,000 / $4,000).

Why It’s Crucial: Lenders prefer a lower DTI ratio because it indicates you have more disposable income to cover new loan payments. A high DTI suggests you might be overextended financially, making you a higher risk. Most lenders prefer a DTI ratio below 36% to 43%, though this can vary.

Pro Tip from Us: If your DTI is on the higher side, focus on paying down existing debts before applying for a car loan. Even reducing a small credit card balance can positively impact your DTI and improve your borrowing power. This strategic move can make a significant difference in the loan terms you qualify for.

4. The Down Payment: Your Upfront Investment

A down payment is the initial amount of money you pay upfront towards the purchase of the car. It directly reduces the amount you need to borrow, which has several significant benefits. Lenders often view a substantial down payment favorably, as it demonstrates your commitment to the purchase and reduces their risk.

Impact on Loan Amount and Interest: The larger your down payment, the less you need to finance. This means your monthly payments will be lower, and you’ll pay less interest over the life of the loan. For example, putting down 20% on a $30,000 car means you only need to borrow $24,000.

Benefits of a Larger Down Payment: Beyond reducing your loan amount, a larger down payment can help you secure a lower interest rate, especially if your credit isn’t perfect. It also reduces your loan-to-value (LTV) ratio, which is another metric lenders consider. Furthermore, it helps you avoid being "upside down" on your loan, where you owe more than the car is worth, a common mistake to avoid.

5. The Loan Term: How Long Will You Be Paying?

The loan term is the length of time you have to repay the loan, typically expressed in months (e.g., 36, 48, 60, or 72 months). This choice significantly impacts your monthly payment and the total amount of interest you’ll pay over time.

Shorter vs. Longer Terms: A shorter loan term means higher monthly payments but less total interest paid because you’re paying off the principal faster. Conversely, a longer loan term offers lower monthly payments, making the car seem more affordable in the short term. However, you’ll end up paying significantly more in total interest over the life of the loan.

Finding the Balance: The ideal loan term strikes a balance between manageable monthly payments and minimizing overall interest costs. Based on my experience, while a 72-month loan might offer very low payments, the total interest can be surprisingly high. Consider what you can comfortably afford each month without stretching your budget too thin, but also be mindful of the long-term cost.

6. Interest Rates: The Cost of Borrowing

The interest rate is the percentage charged by the lender for the money you borrow. It’s a critical component of your monthly payment and the overall cost of your car loan. Your credit score, DTI, loan term, and even the current economic climate all influence the interest rate you’re offered.

How They Are Determined: Lenders assess your risk profile (credit score, DTI, income) to determine your personalized interest rate. Those with excellent credit and stable finances typically receive the lowest rates. Market conditions, like the prime rate set by the Federal Reserve, also play a role.

Fixed vs. Variable: Most car loans come with a fixed interest rate, meaning your rate and monthly payment remain the same throughout the loan term. Variable rates, while less common for car loans, can fluctuate, potentially altering your monthly payments. Pro tips from us: always opt for a fixed rate for predictability and peace of mind.

Shopping Around: Never take the first interest rate you’re offered. Shop around with multiple lenders – banks, credit unions, and online lenders – to compare rates and terms. This simple step can save you hundreds, even thousands, of dollars over the life of the loan.

7. Vehicle Specifics: The Car Itself Matters

Believe it or not, the specific vehicle you intend to purchase can also influence how much a lender is willing to loan you. Lenders consider the car’s value, age, make, model, and even its projected depreciation. They want to ensure that the collateral (the car) is sufficient to cover the loan in case of default.

Lenders’ Risk Assessment: Newer, more reliable models from reputable manufacturers often represent less risk to lenders. They hold their value better, making them more desirable as collateral. Older vehicles or those with a history of significant depreciation might be harder to finance, or come with higher interest rates.

Depreciation: Cars begin to depreciate the moment they leave the dealership lot. Lenders factor this in. If a car depreciates rapidly, it increases the risk of the loan exceeding the car’s value, particularly if you have a small down payment. This is why a substantial down payment is often advised for vehicles known for rapid depreciation.

8. Trade-in Value: Your Old Car as a Down Payment

If you’re replacing an existing vehicle, its trade-in value can act just like a cash down payment. Trading in your old car reduces the amount you need to finance for your new one, directly impacting how much you can borrow for a car loan.

Maximizing Your Trade-in: To get the best trade-in value, ensure your car is clean, well-maintained, and has all its service records. Research its market value using online tools like Kelley Blue Book or Edmunds before heading to the dealership. Knowing its worth empowers you in negotiations.

The Pre-Approval Process: Your Secret Weapon

Before you even start test driving, getting pre-approved for a car loan is one of the smartest moves you can make. Pre-approval means a lender has reviewed your financial information and tentatively agreed to lend you a specific amount at a particular interest rate, subject to final verification.

What It Is and Why It’s Vital: It’s essentially a commitment from a lender, giving you a clear upper limit on what you can borrow. This empowers you with significant bargaining power at the dealership. You walk in knowing your budget and your interest rate, allowing you to focus on the car’s price rather than getting swayed by monthly payment tricks.

Benefits:

- Know Your Limit: You’ll know exactly how much you can afford, preventing you from overspending.

- Bargaining Power: You become a cash buyer in the eyes of the dealership, giving you leverage to negotiate the car’s price.

- Faster Process: It streamlines the buying process, as much of the financing paperwork is already done.

- Compare Rates: You can compare the pre-approved rate with any financing offers from the dealership, ensuring you get the best deal.

Pro tips from us: Apply for pre-approval with a few different lenders within a short timeframe (usually 14-45 days) to minimize the impact on your credit score. This allows you to compare offers effectively. For a deeper dive into the benefits of pre-approval, you might find our guide on The Power of Car Loan Pre-Approval insightful.

Calculating Your Affordability: Beyond the Loan Amount

While understanding "how much can I borrow for a car loan" is essential, true affordability extends beyond just the loan amount and monthly payment. You need to consider the total cost of car ownership. Common mistakes to avoid are focusing solely on the monthly payment without considering these additional expenses.

Total Cost of Ownership:

- Insurance: Car insurance is mandatory and can vary significantly based on the vehicle, your driving record, and location. Get quotes before you buy.

- Maintenance and Repairs: All cars require maintenance. Newer cars might have warranties, but older cars will likely incur more repair costs.

- Fuel: Factor in your daily commute and the car’s fuel efficiency.

- Registration and Taxes: These are recurring costs that vary by state.

- Depreciation: While not an out-of-pocket expense, it’s a real loss of value over time.

Budgeting for a Car: Create a comprehensive budget that includes all these factors. A good rule of thumb is that your total car expenses (loan payment, insurance, fuel, maintenance) should not exceed 10-15% of your gross monthly income. This ensures your car doesn’t become a financial burden.

Common Mistakes to Avoid When Applying for a Car Loan

Based on years of helping individuals navigate car financing, I’ve seen some recurring errors. Avoiding these pitfalls can save you stress and money.

- Not Checking Your Credit Score: Many people apply for a loan without knowing their credit standing. This puts you at a disadvantage as you don’t know what rates you genuinely qualify for.

- Applying to Too Many Lenders at Once (Without Strategy): While shopping around is good, multiple hard inquiries on your credit report over a short period can temporarily lower your score. Group your applications within a 14-45 day window to have them count as a single inquiry for scoring purposes.

- Focusing Only on Monthly Payments: Dealerships often use this tactic. They might extend the loan term to lower the monthly payment, making a car seem affordable when the total cost is much higher. Always ask for the total price, including all fees and interest.

- Ignoring the Total Cost of Ownership: As discussed, a car is more than just a loan payment. Neglecting insurance, fuel, and maintenance costs can quickly lead to financial strain.

- Not Reading the Fine Print: Always read your loan agreement thoroughly before signing. Understand all terms, conditions, fees, and penalties for late payments or early payoff. If something is unclear, ask for clarification.

Pro Tips for Boosting Your Car Loan Borrowing Power

Want to maximize how much you can borrow for a car loan and secure the best possible terms? Here are some actionable strategies:

- Improve Your Credit Score: This is fundamental. Pay bills on time, reduce credit card balances, and address any errors on your credit report. A higher score unlocks better rates.

- Save for a Larger Down Payment: Even an extra few hundred or thousand dollars can make a significant difference in your monthly payment and overall interest paid.

- Pay Down Existing Debt: Lowering your DTI ratio by paying off other loans or credit cards makes you a more attractive borrower.

- Shop Multiple Lenders: Don’t just rely on the dealership’s financing. Compare offers from banks, credit unions, and online lenders before you commit. Credit unions often have very competitive rates.

- Consider a Co-signer (With Caution): If your credit isn’t stellar, a co-signer with excellent credit can help you qualify for a better loan. However, ensure both parties understand the responsibility, as the co-signer is equally liable for the debt.

- Be Realistic About the Car: Sometimes, the best way to "borrow more" is to simply need to borrow less. Re-evaluate if you truly need the most expensive model or if a slightly less option meets your needs and budget better.

Conclusion: Empowering Your Car Loan Journey

Determining "how much can I borrow for a car loan" is a journey that requires self-assessment, diligent research, and strategic planning. It’s not just about a lender’s decision; it’s about understanding your financial landscape and making informed choices. By focusing on your credit score, managing your debt, securing a healthy down payment, and understanding the full cost of ownership, you empower yourself to navigate the car buying process with confidence.

Remember, the goal isn’t just to get approved for a loan, but to get approved for a loan that aligns with your financial goals and won’t become a burden. Take the time to prepare, get pre-approved, and compare offers. Your dream car is within reach, and with this comprehensive guide, you have the tools to make that dream a financially sound reality. For more detailed information on responsible borrowing and personal finance, consider visiting a trusted external resource like the Consumer Financial Protection Bureau’s website (www.consumerfinance.gov).