How Much Can You Get For A Car Loan? Unlocking Your Auto Financing Potential

How Much Can You Get For A Car Loan? Unlocking Your Auto Financing Potential Carloan.Guidemechanic.com

Securing a car loan is a significant financial step, and one of the first questions on every prospective buyer’s mind is inevitably: "How much can I actually get for a car loan?" This isn’t a simple question with a single, universal answer. Instead, the amount you can borrow for a vehicle is a complex interplay of various personal financial metrics, the specific car you’re eyeing, and the prevailing market conditions.

As an expert blogger and SEO content writer with years of experience navigating the intricacies of auto financing, I’ve seen firsthand how understanding these factors can empower you to make informed decisions. This comprehensive guide will peel back the layers, revealing precisely what influences your car loan amount and how you can maximize your borrowing power while ensuring a smooth approval process. Our ultimate goal here is to equip you with the knowledge to confidently approach any lender, knowing exactly what to expect and how to secure the best possible deal.

How Much Can You Get For A Car Loan? Unlocking Your Auto Financing Potential

Understanding the Fundamentals: It’s Not a One-Size-Fits-All Answer

The idea that there’s a fixed maximum amount everyone can get for a car loan is a common misconception. In reality, lenders assess each applicant individually. They’re primarily interested in your ability and willingness to repay the loan. This assessment involves looking at a snapshot of your financial health, which then dictates the principal loan amount they are comfortable extending to you.

Think of it this way: a car loan is essentially a lender’s investment in your future payments. They want to minimize their risk. Therefore, the "how much" depends entirely on how reliable they perceive you to be as a borrower. This is why two different individuals looking at the exact same car might be offered vastly different loan amounts and interest rates.

Key Factors That Determine Your Car Loan Amount

Let’s dive deep into the specific elements that lenders scrutinize when determining how much car loan you can get. Each factor plays a crucial role, and understanding their individual impact is vital for anyone seeking auto financing.

A. Your Credit Score: The Cornerstone of Loan Approval

Your credit score is arguably the most influential factor in determining not just the amount you can borrow, but also the interest rate you’ll pay. This three-digit number, generated by credit bureaus, is a quick summary of your creditworthiness. It reflects your history of borrowing and repaying debt.

Lenders use your credit score to gauge your financial responsibility. A higher score (generally 670 and above) signals to lenders that you are a low-risk borrower, making them more willing to offer you a larger loan amount at more favorable interest rates. Conversely, a lower score might lead to smaller loan offers, higher interest rates, or even outright denial. Based on my experience, even a difference of 50 points in your credit score can translate into thousands of dollars in interest over the life of a car loan.

Pro tips from us: Before even stepping foot in a dealership, check your credit score. You can get free access to your score and report through various online services. If your score isn’t where you want it to be, take steps to improve it, such as paying down existing debts or correcting any errors on your credit report. A little preparation here can significantly increase the maximum car loan you can secure.

B. Your Debt-to-Income (DTI) Ratio: Your Financial Breathing Room

Your Debt-to-Income (DTI) ratio is another critical metric lenders use to assess your capacity to take on new debt. It’s calculated by dividing your total monthly debt payments by your gross monthly income. This ratio essentially tells lenders how much of your income is already committed to existing debts, leaving a clearer picture of how much "financial breathing room" you have for a new car payment.

Lenders prefer a low DTI ratio because it indicates you have sufficient income to manage your current financial obligations plus a new car loan payment. Generally, a DTI ratio of 36% or less is considered ideal, though some lenders may approve loans for individuals with slightly higher ratios, especially if they have an excellent credit score. If your DTI is too high, lenders might limit the car loan amount they offer or decline your application altogether, fearing you’re overextended.

Common mistakes to avoid are: Underestimating your existing debt. Remember to include all monthly payments – credit cards, student loans, mortgages, personal loans, and any other regular debt obligations. Failing to account for these can lead to a miscalculation of your DTI and potentially an unexpected denial.

C. Your Income and Employment Stability: Proving Your Repayment Capacity

Your income is, naturally, a direct indicator of your ability to make monthly car loan payments. Lenders will want to verify that you have a consistent and sufficient income stream to comfortably cover the proposed car payment in addition to your other living expenses and debts. They typically require proof of income, such as pay stubs, tax returns, or bank statements.

Beyond the sheer amount, the stability of your employment also plays a significant role. A long history with the same employer or a consistent work history in a particular field demonstrates reliability. For self-employed individuals, lenders usually look for at least two years of consistent income to establish a stable earning pattern. The more stable your income and employment, the more confident a lender will be in offering you a substantial car loan amount.

D. The Car Itself: New vs. Used, Value, and Age

Believe it or not, the vehicle you intend to purchase significantly impacts how much you can get for a car loan. Lenders consider the car’s value, age, mileage, and condition, as these factors determine its collateral value. The car serves as collateral for the loan; if you default, the lender repossesses and sells the car to recoup their losses.

New cars generally qualify for larger loan amounts and better terms because they hold their value better initially and pose less risk. Used cars, especially older models or those with high mileage, might be subject to stricter lending criteria or lower maximum loan amounts. Lenders might also impose limits on the loan-to-value (LTV) ratio, meaning they will only finance a certain percentage of the car’s appraised value. For instance, if a car is valued at $20,000 and the lender has an 80% LTV cap, the maximum they will lend for that specific car is $16,000, irrespective of your personal financial strength. You can research car values on trusted external sources like Kelley Blue Book.

E. Your Down Payment: Reducing Your Loan Burden

Making a down payment is one of the most effective ways to influence how much car loan you can get and improve your overall loan terms. A down payment is the initial amount of money you pay upfront for the car, reducing the total amount you need to borrow. The larger your down payment, the less risk the lender takes on.

A substantial down payment can lead to a lower principal loan amount, which in turn means lower monthly payments and less interest paid over the life of the loan. It can also help you qualify for a loan even if your credit isn’t perfect, as it signals your commitment to the purchase. Based on my experience, aiming for at least 10-20% of the car’s purchase price as a down payment is a strong strategy. For those looking to secure a new car loan, a 20% down payment is often considered ideal.

F. The Loan Term (Length): Balancing Payments and Total Cost

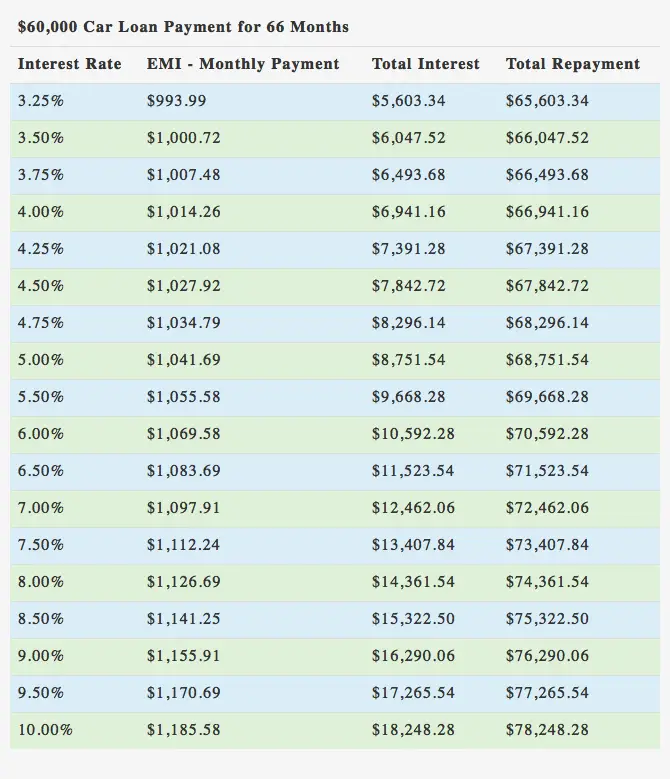

The loan term, or the length of time you have to repay the loan, also plays a role in determining how much car loan you can afford. Longer loan terms typically result in lower monthly payments, making a more expensive car seem "affordable" on a monthly basis. However, a longer term also means you’ll pay significantly more in total interest over the life of the loan.

While a longer term might allow you to borrow a larger principal amount due to lower monthly payments, it’s crucial to consider the total cost. Lenders are often willing to extend loans for up to 72 or even 84 months, but stretching the repayment period too far can lead to negative equity (owing more than the car is worth) and excessive interest charges. Pro tips from us: Always balance the monthly payment with the total cost of the loan. Don’t let a low monthly payment blind you to the overall expense.

G. Current Interest Rates: The Cost of Borrowing

The prevailing interest rates at the time of your application directly impact the total cost of your car loan and, consequently, how much car loan you can truly afford. A lower interest rate means more of your monthly payment goes towards the principal balance, reducing the overall cost of borrowing. Conversely, higher interest rates increase your monthly payments for the same principal amount, limiting how much you can realistically borrow without straining your budget.

Interest rates are influenced by various factors, including the economy, the Federal Reserve’s policies, and the competitive landscape among lenders. Your credit score also heavily influences the interest rate you’ll be offered. Shopping around for the best interest rates from multiple lenders can make a substantial difference in your overall car loan amount and affordability.

Beyond the Loan Amount: Don’t Forget the "Hidden" Costs

While the primary focus is often on "how much can you get for a car loan," it’s crucial to remember that the purchase price of a car is only part of the overall cost. Overlooking additional expenses can quickly derail your budget.

These "hidden" costs include:

- Sales Tax: Varies by state, but can add thousands to the total price.

- Registration and Licensing Fees: Required to legally operate your vehicle.

- Insurance: A mandatory and ongoing expense that can vary widely based on the car, your driving history, and location.

- Extended Warranties and Add-ons: Often offered by dealerships, these can significantly increase the total amount financed if rolled into your loan.

When budgeting for a car loan, ensure you account for all these additional expenses. Sometimes, lenders will allow you to roll some of these costs into your auto loan, but this increases your principal, your monthly payment, and the total interest you’ll pay.

Maximizing Your Car Loan Potential and Approval Chances

Now that we’ve explored the factors, let’s talk strategy. Here’s how you can position yourself for the best possible car loan amount and approval:

- Know Your Credit Score and Report: Obtain copies of your credit report from all three major bureaus (Equifax, Experian, TransUnion) and review them for accuracy. Dispute any errors. Improving your credit score is one of the most impactful steps you can take. For more detailed advice, check out our article on How to Improve Your Credit Score for a Car Loan (hypothetical internal link).

- Save for a Down Payment: The more you put down upfront, the less you need to borrow, improving your loan-to-value ratio and reducing the lender’s risk. This often translates to better loan terms and a higher likelihood of approval.

- Pay Down Other Debts: Reducing your existing debt obligations will lower your Debt-to-Income ratio, making you a more attractive borrower. Focus on high-interest debts first.

- Get Pre-Approved: This is a game-changer. Pre-approval gives you a clear idea of how much car loan you qualify for and at what interest rate before you even set foot in a dealership. It empowers you to negotiate like a cash buyer.

- Shop Around for Lenders: Don’t settle for the first offer. Banks, credit unions, and online lenders all have different rates and terms. Apply to several to compare offers and find the most affordable car loan for your situation. All applications within a short window (typically 14-45 days) will count as a single inquiry on your credit report, so comparison shopping won’t harm your score.

- Be Realistic About the Car: Choose a car that aligns with your financial capabilities. While you might qualify for a large loan, it doesn’t mean you should take it. Consider the car’s ongoing costs (insurance, fuel, maintenance) alongside the loan payment.

The Pre-Approval Process: Your Strategic Advantage

Understanding and utilizing the pre-approval process is a professional tip I cannot emphasize enough. Pre-approval means a lender has reviewed your financial information and provisionally agreed to lend you a specific amount of money at a certain interest rate, subject to final verification and the vehicle meeting their criteria.

Why is this a strategic advantage?

- Clarity on Loan Amount: You’ll know precisely how much car loan you can get before you start shopping, allowing you to focus on cars within your budget.

- Negotiating Power: Walking into a dealership with a pre-approval letter is like having cash in hand. Dealers know you’re a serious buyer with financing already secured, which often leads to better negotiation terms on the car’s price.

- Focus on the Car, Not the Financing: It separates the car-buying process from the loan-securing process, making both less stressful.

- Benchmarking: You can use your pre-approved rate as a benchmark against any financing offers from the dealership. If the dealership can beat your pre-approval, great! If not, you have a solid backup.

For a deeper dive into this crucial step, read our detailed guide: Understanding Car Loan Pre-Approval: A Complete Guide (hypothetical internal link).

Common Pitfalls to Avoid When Securing a Car Loan

Even with all the right information, it’s easy to stumble into common traps. Here are some critical mistakes to steer clear of:

- Not Checking Your Credit Report: As mentioned, errors can exist. Don’t let someone else’s mistake cost you a better loan.

- Focusing Only on Monthly Payments: This is perhaps the biggest pitfall. Dealers often try to "sell the payment," stretching the loan term to make a high-priced car seem affordable. Always ask for the total cost of the loan and the interest rate.

- Ignoring the Total Cost of the Loan: Factor in interest, fees, taxes, and insurance. A "low" monthly payment might hide a significantly higher total cost over several years.

- Falling for Unnecessary Add-ons: Resist the pressure to purchase extended warranties, paint protection, or VIN etching if you don’t truly need or want them. If you do, consider purchasing them separately or negotiating their price fiercely.

- Not Understanding the Loan Agreement: Read every line of your loan document before signing. Understand the interest rate, term, prepayment penalties (if any), and all fees.

Real-World Scenario: Putting It All Together

Let’s consider two hypothetical individuals, Sarah and Mark, both earning $60,000 annually and looking for a $25,000 car.

- Sarah: Has an excellent credit score (780), a low DTI of 20%, and has saved a $5,000 down payment. She’s pre-approved for a $20,000 loan at 3.5% APR over 60 months. She has strong repayment capacity.

- Mark: Has a fair credit score (620), a high DTI of 45% due to student loans and credit card debt, and no down payment. He might only be approved for a $15,000 loan at 9% APR over 72 months, or even less. The lender perceives him as a higher risk due to his existing debt burden and credit history.

This example clearly illustrates how your individual financial profile directly dictates how much car loan you can get, and the terms associated with it. Even with similar incomes, the other factors create vastly different borrowing scenarios.

Conclusion: Empowering Your Car Loan Journey

Understanding "how much can you get for a car loan" is not just about a number; it’s about understanding your financial power and how to leverage it. We’ve delved into the critical factors—your credit score, DTI, income, the car’s value, your down payment, loan term, and interest rates—that collectively determine your auto loan eligibility and the maximum car loan amount you can secure.

By taking proactive steps such as checking your credit, saving for a down payment, reducing existing debt, and getting pre-approved, you can significantly improve your chances of approval and secure an affordable car loan with favorable terms. Remember, an informed borrower is an empowered borrower. Don’t rush the process; take the time to prepare and shop around. This diligence will not only help you get the car you want but also ensure that your car loan fits comfortably within your financial landscape. Start planning your car loan journey today with confidence!