How Much Down For A Car Loan: Your Ultimate Guide to Smart Car Financing

How Much Down For A Car Loan: Your Ultimate Guide to Smart Car Financing Carloan.Guidemechanic.com

Buying a car is an exciting milestone, but navigating the world of auto financing can feel like a complex journey. One of the most common questions that arise, and perhaps the most crucial for your financial well-being, is: "How much down for a car loan?" This isn’t just a simple number; it’s a strategic decision that impacts your monthly payments, the total cost of your vehicle, and even your eligibility for a loan.

As an expert blogger and professional in SEO content, I’ve seen countless individuals struggle with this very question. My goal today is to provide you with a super comprehensive, in-depth guide that demystifies car loan down payments. We’ll explore why they matter, how much you should aim for, and practical strategies to help you secure the best financing terms possible. Get ready to transform your car buying experience!

How Much Down For A Car Loan: Your Ultimate Guide to Smart Car Financing

The Core Question: How Much Down For A Car Loan? (General Guidance)

When considering a car loan, the concept of a down payment can seem daunting. However, understanding its role is the first step towards smart financing. A down payment is essentially the upfront cash you pay towards the purchase of a vehicle, reducing the amount you need to borrow.

The "Ideal" Scenario: The 10-20% Rule

Based on my experience in the automotive finance industry, a widely accepted guideline for a car loan down payment is 10% to 20% of the vehicle’s purchase price. This range serves as a solid starting point for most buyers. For instance, if you’re looking at a $30,000 car, a down payment between $3,000 and $6,000 is generally recommended.

This isn’t a hard and fast rule, but rather a benchmark that helps you secure favorable loan terms and protect your financial health. Falling within this range often signals to lenders that you’re a responsible borrower. It also helps you avoid common pitfalls associated with minimal or no down payment options.

New vs. Used Cars: Does the Down Payment Differ?

The type of car you purchase—new or used—can influence the recommended down payment. For new cars, a larger down payment, typically closer to 20%, is often advisable. New vehicles depreciate rapidly the moment they leave the dealership lot. A substantial down payment helps cushion this initial depreciation, reducing the risk of owing more than the car is worth (negative equity).

For used cars, a down payment of 10% is often sufficient. While used cars still depreciate, their initial value drop is less steep than new vehicles. However, a larger down payment can still provide significant benefits, such as lower monthly payments and reduced total interest. Ultimately, the best down payment amount will depend on various factors we’ll explore shortly.

Factors Influencing Your Optimal Down Payment

The "ideal" down payment isn’t a one-size-fits-all figure. Several personal and financial factors play a critical role in determining what’s right for you. These include your credit score, the car’s price, your personal budget, and the specific requirements of the lender. Understanding these elements will empower you to make an informed decision tailored to your unique circumstances.

Why a Down Payment Matters: Beyond Just the Numbers

The benefits of making a substantial down payment on a car loan extend far beyond simply reducing the initial sticker shock. It’s a strategic financial move that can save you money, improve your loan terms, and provide greater peace of mind throughout your ownership period.

Lower Monthly Payments

One of the most immediate and tangible benefits of a larger down payment is significantly reduced monthly payments. When you put more money down upfront, you borrow less. A smaller principal loan amount directly translates to lower installments each month, making your car more affordable to own on a day-to-day basis.

This can free up valuable cash flow in your budget, allowing you to allocate funds to other financial goals or simply enjoy more discretionary spending. It provides a comfortable buffer, especially if unexpected expenses arise during the life of your loan.

Reduced Total Interest Paid

While lower monthly payments are great, the long-term financial advantage lies in the total interest saved over the life of the loan. Interest is calculated on the principal amount borrowed. By reducing that principal with a larger down payment, you’re paying interest on a smaller sum. This effect compounds over several years, leading to substantial savings.

Even a slight increase in your down payment can shave hundreds, if not thousands, of dollars off the total cost of your car. It’s a direct way to make your money work harder for you, rather than for the lender.

Better Loan Terms & Interest Rates

Lenders view a significant down payment as a sign of financial responsibility and reduced risk. When you have more equity in the vehicle from day one, the lender’s exposure to potential loss is lower. This favorable perception often translates into better loan terms and lower interest rates.

Based on my experience, borrowers with solid down payments frequently qualify for the most competitive Annual Percentage Rates (APRs). A lower interest rate means even more savings on top of the reduced principal, further decreasing your total repayment amount. It’s a powerful bargaining chip in your favor.

Avoiding Negative Equity (Being Upside Down)

This is a critical point, especially for new car buyers. Negative equity, also known as being "upside down" on your loan, occurs when you owe more on your car than its current market value. Since new cars depreciate rapidly, a small or no down payment makes you highly susceptible to this situation.

A healthy down payment helps create a buffer against depreciation. It ensures that your equity in the car grows faster than its value declines, protecting you if you need to sell or trade in the vehicle before the loan is fully paid off. Being upside down can make it very difficult to sell or trade your car without rolling the negative balance into a new loan, which is a common mistake to avoid.

Easier Loan Approval

For individuals with less-than-perfect credit scores, a substantial down payment can be a game-changer for loan approval. Lenders are often more willing to take a chance on a borrower with a lower credit score if they’ve demonstrated a significant financial commitment upfront. The down payment mitigates some of the risk associated with a weaker credit profile.

It shows the lender that you have skin in the game and are serious about your financial obligations. This can be the difference between getting approved for a loan and being denied, or between receiving a high-interest rate and a more manageable one.

Potentially Lower Insurance Premiums

While not universally true, some auto insurance providers may offer slightly lower premiums if you have a larger down payment. This is because your equity in the vehicle is higher, reducing the insurer’s potential payout in the event of a total loss. Check with your insurance provider to see if this applies to your policy, as every little bit helps in reducing overall car ownership costs.

Factors Determining Your Optimal Down Payment

Deciding on the "right" down payment isn’t just about picking a percentage. It involves a personalized assessment of your financial health and the specifics of the car you’re buying. Let’s delve into the key factors that will guide your decision.

Your Credit Score

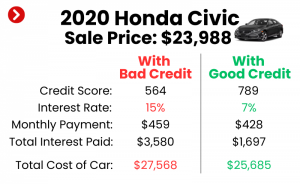

Your credit score is arguably one of the most significant factors influencing your down payment needs.

- Excellent/Good Credit (700+): If you have a strong credit history, you’ll generally have more flexibility. Lenders perceive you as a low-risk borrower, making them more likely to offer favorable terms even with a smaller down payment, or in some cases, a no-down-payment option. However, even with great credit, a down payment is still beneficial for the reasons discussed above.

- Average/Poor Credit (Below 670): For those with lower credit scores, a higher down payment is often essential. Lenders will view you as a higher risk. A substantial down payment reduces their risk exposure, significantly increasing your chances of loan approval and helping you secure a more reasonable interest rate. Pro tip from us: Always check your credit report and score before you start car shopping. Knowing where you stand empowers you to negotiate better.

The Car’s Price and Type

The total price of the vehicle directly impacts the dollar amount of your down payment. A 10% down payment on a $50,000 luxury SUV is $5,000, whereas on a $20,000 economy sedan, it’s $2,000. Consider the absolute cash outlay. Additionally, new cars typically warrant a larger down payment (closer to 20%) due to rapid initial depreciation, while used cars might be fine with 10%.

Your Budget & Financial Situation

Before committing to a down payment, take an honest look at your overall financial health. How much cash do you comfortably have available without depleting your emergency savings? You should never drain your emergency fund for a down payment. Ensure you have enough left over for unexpected expenses, and to cover other initial costs like sales tax, registration, and insurance.

Loan Term

The length of your loan (e.g., 36, 60, 72, or 84 months) can also play a role. A longer loan term typically results in lower monthly payments but higher total interest paid. If you opt for a shorter loan term to save on interest, you might need a larger down payment to keep your monthly payments manageable. Conversely, if you choose a longer term, a smaller down payment might lead to very high total interest.

Interest Rate

A higher interest rate makes a larger down payment even more appealing. With a high rate, every dollar you borrow costs you more over time. By increasing your down payment, you reduce the principal subject to that high interest, significantly mitigating the overall cost. Conversely, with a very low interest rate, the urgency for a massive down payment might lessen, allowing you to keep more cash liquid.

Lender Requirements

Some lenders have minimum down payment requirements, especially for certain types of vehicles or for borrowers with specific credit profiles. Always ask about these requirements upfront. What one lender accepts, another might not, so it pays to shop around for both the car and the loan.

Trade-in Value

If you’re trading in your current vehicle, its value can effectively act as a down payment. The agreed-upon trade-in value is deducted from the new car’s price, reducing the amount you need to finance. This is an excellent way to boost your down payment without using additional cash. Ensure you get a fair trade-in value by doing your research beforehand.

The "No Down Payment" Car Loan: Is It Ever a Good Idea?

The allure of driving off the lot without putting any money down is strong, and "zero down" car loans are indeed available. But are they ever a wise financial move?

Explanation: How It Works

A no-down-payment car loan means the lender finances 100% of the vehicle’s purchase price. This might seem like a dream come true for those short on cash or wanting to preserve their savings. Essentially, you’re borrowing the entire cost of the car from the bank or dealership.

Risks Associated with Zero Down Payments

While convenient, no-down-payment loans come with significant risks:

- Higher Monthly Payments: Since you’re financing the entire cost, your principal loan amount is higher, leading to substantially larger monthly payments. This can strain your budget and increase the risk of missing payments.

- More Total Interest Paid: A larger principal means you’ll pay more interest over the life of the loan. This can add thousands of dollars to the total cost of the car, making it a much more expensive purchase in the long run.

- Immediate Negative Equity: As discussed, new cars depreciate quickly. With no money down, you’re almost guaranteed to be "upside down" on your loan from day one. If your car is totaled or stolen, your insurance payout might not cover the outstanding loan balance, leaving you to pay the difference out of pocket.

- Harder Loan Approval (for some): Lenders view no-down-payment loans as higher risk. They are generally reserved for borrowers with excellent credit scores and stable financial histories. If your credit isn’t stellar, securing such a loan can be challenging or come with very high interest rates.

When It Might Make Sense (Rare Exceptions)

In very specific, rare circumstances, a no-down-payment loan might be considered:

- Exceptional Credit and Special Offers: If you have a pristine credit score (800+) and a dealership is offering a special 0% APR, no-down-payment deal, it could be financially sound. In this scenario, you’re not paying interest, so keeping your cash liquid might be preferable.

- Strategic Investment: If you have other investments or opportunities that can yield a higher return than the interest rate on your car loan, it might make sense to keep your cash in those investments. However, this strategy requires sophisticated financial planning and carries its own risks.

- Emergency Need with Excellent Financial Standing: In an absolute emergency where you need a car immediately and have excellent credit, but your cash is tied up, a zero-down loan might be a temporary solution. However, even then, I’d advise finding a way to make a payment as soon as possible.

Common mistakes to avoid are jumping into a 0-down payment without fully understanding these long-term financial implications. For most people, a down payment is a wise investment in their financial future.

Strategies for Coming Up With a Down Payment

If you’re committed to making a solid down payment but aren’t sure how to accumulate the funds, don’t worry. There are several effective strategies you can employ to build your savings.

Saving Systematically

The most straightforward approach is to save systematically. Create a dedicated savings goal for your car down payment. Budget meticulously, identify areas where you can cut back on discretionary spending (e.g., dining out, subscriptions), and set up automatic transfers from your checking to a separate savings account each payday. Even small, consistent contributions add up significantly over time.

Selling an Old Car (Trade-in or Private Sale)

If you have an existing vehicle, its value can be your primary source for a down payment. You can trade it in at the dealership, which offers convenience and potential tax savings (in some states, you only pay sales tax on the difference between the new car price and trade-in value). Alternatively, selling your old car privately often yields a higher price than a trade-in, giving you more cash for your down payment. Weigh the effort of a private sale against the convenience of a trade-in.

Utilizing Tax Refunds or Bonuses

Lump sums like tax refunds, work bonuses, or inheritance money can be excellent catalysts for your down payment fund. Instead of using these windfalls for immediate gratification, earmark them specifically for your car purchase. This accelerates your savings goal without impacting your regular budget.

Temporary Sacrifices

Consider making temporary sacrifices in your spending habits. This might mean pausing expensive hobbies, reducing entertainment costs, or opting for more budget-friendly alternatives for a few months. Think of it as a short-term investment in your long-term financial health. These sacrifices are temporary, but the benefits of a larger down payment will last for years.

Negotiating the Car Price

Every dollar you save on the purchase price of the car is effectively like adding a dollar to your down payment. Negotiate fiercely on the vehicle’s price. Research fair market value, be prepared to walk away, and don’t be afraid to ask for a better deal. The lower the total price, the less you’ll need to finance, and the smaller your overall down payment requirement will feel.

Pro tips from us: Start saving early, be disciplined with your budget, and explore all avenues to boost your down payment. The effort you put in now will pay dividends for years to come.

Calculating Your Ideal Down Payment: A Practical Guide

Now that we understand the "why" and "how" of down payments, let’s walk through a practical approach to calculating what might be ideal for you.

Step-by-Step Approach

- Determine Your Target Car Price: Research the specific make, model, and year of the car you want. Get an estimate of its fair market value. For example, let’s say your dream car is $25,000.

- Assess Your Financial Health:

- Credit Score: Check your credit score. If it’s excellent, you might be comfortable with 10%. If it’s average or poor, aim for 15-20% or more.

- Savings: How much cash do you currently have available without touching your emergency fund?

- Monthly Budget: What’s the maximum comfortable monthly payment you can afford?

- Use a Car Loan Calculator: Online car loan calculators are invaluable tools. You can input various down payment amounts, interest rates, and loan terms to see how they impact your monthly payment and total interest. (External Link Placeholder: Check out this Car Loan Payment Calculator from Bankrate to help you crunch the numbers.)

- Consider the 10-20% Rule as a Starting Point: For our $25,000 car, 10% is $2,500, and 20% is $5,000. This gives you a tangible range to aim for.

- Factor in Your Trade-in: If you have a trade-in, get an estimated value for it. Subtract this from the car’s price before calculating your cash down payment. If your trade-in is worth $5,000, and the car is $25,000, you now only need to finance $20,000, significantly reducing your cash down payment requirement.

Example Scenario:

Let’s say you’re buying a $25,000 car.

- You have a good credit score (720).

- You have $3,000 in cash savings that you’re comfortable putting down.

- Your old car is worth $2,000 as a trade-in.

Calculation:

- Car Price: $25,000

- Trade-in Value: -$2,000

- New Loan Amount Before Cash Down: $23,000

- Your Cash Down Payment: -$3,000

- Actual Amount to Finance: $20,000

In this scenario, your total "down payment" (cash + trade-in) is $5,000, which is exactly 20% of the original car price. This is an excellent position to be in, likely qualifying you for a great interest rate and keeping your monthly payments very manageable.

Common Mistakes to Avoid When Making a Down Payment

Even with the best intentions, car buyers can sometimes make missteps when it comes to their down payment. Being aware of these common mistakes can help you steer clear of financial headaches.

Draining Your Emergency Fund

This is perhaps the most critical error. Your emergency fund is there for genuine crises – unexpected job loss, medical emergencies, or home repairs. Never deplete your emergency savings to make a car down payment, no matter how good the deal seems. You risk putting yourself in a vulnerable position should an unforeseen event occur, potentially leading to debt or even defaulting on your loan.

Borrowing for a Down Payment

It might sound tempting to take out a personal loan or use a credit card to cover your down payment, but this is almost always a bad idea. You’re essentially borrowing money to borrow more money. Personal loans often come with higher interest rates than car loans, and credit card interest rates are significantly higher. This will dramatically increase the total cost of your car and could create an unmanageable debt cycle.

Ignoring Other Upfront Costs

A down payment isn’t the only money you’ll need upfront. Don’t forget to budget for sales tax, registration fees, license plates, and your first insurance premium. These costs can easily add thousands of dollars to your initial outlay. Failing to account for them can leave you short on cash or force you to dip into your emergency fund.

Focusing Only on the Monthly Payment

While a low monthly payment is appealing, it shouldn’t be your sole focus. A dealer might offer you a low monthly payment by extending the loan term to 72 or 84 months, or by reducing your down payment. This often leads to paying significantly more in total interest over the life of the loan and increases your risk of negative equity. Always consider the total cost of the vehicle and your total interest paid.

Not Shopping Around for Loans

Just as you shop for the best car deal, you should also shop for the best loan. Don’t automatically accept the financing offered by the dealership. Get pre-approved by a few different banks, credit unions, or online lenders before you visit the dealership. This allows you to compare interest rates and terms, ensuring you get the most competitive offer. Common mistakes we often see are people getting excited about a car and forgetting to secure competitive financing.

Boosting Your Chances of Loan Approval (Beyond Down Payment)

While a solid down payment is a major factor, it’s just one piece of the puzzle for loan approval. To further strengthen your application and secure the best terms, consider these additional strategies.

Improve Your Credit Score

Your credit score is a numerical representation of your creditworthiness. A higher score signals to lenders that you’re a responsible borrower. To improve it:

- Pay all bills on time, every time: Payment history is the biggest factor.

- Reduce outstanding debt: Especially credit card balances, to lower your credit utilization ratio.

- Avoid opening new credit accounts just before applying for a car loan.

- Check your credit report for errors: Dispute any inaccuracies.

For a deeper dive into improving your credit score, check out our guide on How to Improve Your Credit Score for a Car Loan.

Stabilize Your Income

Lenders want to see a consistent and reliable source of income. This demonstrates your ability to make regular loan payments. If you’ve recently changed jobs or are self-employed, be prepared to provide extensive documentation of your income stability, such as pay stubs, tax returns, and bank statements.

Reduce Your Debt-to-Income Ratio (DTI)

Your debt-to-income (DTI) ratio is a crucial metric for lenders. It compares your total monthly debt payments to your gross monthly income. A lower DTI indicates that you have more disposable income available to cover a new car payment. Aim for a DTI below 36%, with less than 20% dedicated to housing. Reduce existing debt (like credit card balances or personal loans) before applying for a car loan.

If you’re interested in understanding more about debt-to-income ratios, read our comprehensive article: Understanding Your Debt-to-Income Ratio for Loan Approval.

Provide All Required Documentation

Be prepared with all necessary paperwork. This typically includes:

- Proof of identity (driver’s license)

- Proof of income (pay stubs, tax returns)

- Proof of residence (utility bill)

- Social Security number

- Information about your trade-in (if applicable)

Having everything organized and ready streamlines the application process and shows lenders you are serious and organized.

Conclusion: Making an Informed Decision About Your Car Loan Down Payment

Deciding "how much down for a car loan" is one of the most significant financial decisions you’ll make during the vehicle purchasing process. It’s not just about getting approved; it’s about securing the most favorable terms, minimizing your total costs, and ensuring your financial stability throughout the life of your loan.

We’ve explored the general guidelines of 10-20% down, the crucial benefits of a substantial down payment – from lower monthly payments and reduced interest to avoiding negative equity – and the factors that shape your personal optimal amount. We also delved into the risks of zero-down loans and provided practical strategies for building your down payment fund.

Based on my experience, taking the time to plan your down payment is an investment that pays dividends. It empowers you to negotiate from a position of strength, secure better loan terms, and ultimately enjoy your new vehicle without unnecessary financial stress. Remember to assess your credit, budget wisely, and avoid common pitfalls. Start planning your down payment today, and drive away with confidence!