How Much Down For Car Loan? Your Ultimate Guide to Smart Auto Financing

How Much Down For Car Loan? Your Ultimate Guide to Smart Auto Financing Carloan.Guidemechanic.com

Buying a car is an exciting milestone, whether it’s your first set of wheels or an upgrade to a newer model. However, the financial aspect, particularly the down payment, often leaves many potential buyers scratching their heads. "How much down for a car loan?" isn’t just a simple question; it’s a critical financial decision that can impact your budget for years to come.

As an expert in auto financing and a seasoned professional, I’ve seen countless car deals unfold. Understanding the role of a down payment is paramount to securing not just a car, but a smart car loan. This comprehensive guide will demystify the down payment process, offering insights, strategies, and pro tips to help you make an informed choice. Let’s dive deep and ensure your next car purchase puts you in the financial driver’s seat.

How Much Down For Car Loan? Your Ultimate Guide to Smart Auto Financing

What Exactly Is a Car Loan Down Payment?

At its core, a car loan down payment is an initial upfront cash payment you make towards the purchase price of a vehicle. It’s the portion of the car’s cost that you pay out of pocket, reducing the amount you need to borrow from a lender. Think of it as your direct investment in the car before the financing even begins.

This initial contribution isn’t just about reducing your loan size; it signals your commitment to the lender. When you make a down payment, you’re immediately building equity in the vehicle. This equity is the difference between what the car is worth and what you owe on it.

Why Does a Down Payment Matter So Much?

The down payment isn’t just a formality; it’s a powerful tool in your car financing arsenal. It can significantly influence the terms of your loan, your monthly budget, and your overall financial health. Understanding its importance is the first step toward making a wise decision.

1. It Reduces Your Loan Amount

This is perhaps the most obvious benefit. The more you put down upfront, the less money you need to borrow. For instance, if a car costs $30,000 and you put down $5,000, you only need to finance $25,000. This directly translates into a smaller principal loan amount.

A smaller loan principal means less financial burden over the life of the loan. It simplifies your repayment schedule and makes the overall process more manageable.

2. It Lowers Your Monthly Payments

With a reduced loan amount, your monthly payments will naturally be lower. This can free up significant cash flow in your budget, making it easier to meet other financial obligations or save for future goals. Lower payments provide greater financial flexibility.

Based on my experience, many buyers focus solely on the monthly payment. A larger down payment is one of the most effective ways to achieve a comfortable monthly figure without extending your loan term too much.

3. It Reduces the Total Interest Paid

Lenders charge interest on the amount you borrow. A smaller loan principal means you’ll pay interest on a lower sum over the life of the loan. Even a seemingly small reduction in the principal can lead to substantial savings on interest charges over several years.

This is a crucial point many people overlook. The total cost of the car isn’t just its sticker price plus the down payment; it includes all the interest you accrue. A larger down payment directly cuts into that interest cost.

4. It Builds Equity Faster

Equity is the portion of an asset you truly own. When you make a down payment, you immediately establish equity in your vehicle. This is particularly important because cars depreciate rapidly. Building equity quickly helps you stay ahead of depreciation, reducing the risk of owing more than the car is worth.

Pro tips from us: Aim to always have positive equity. This gives you options down the line if you need to sell or trade in your vehicle.

5. It Improves Your Loan Approval Chances and Terms

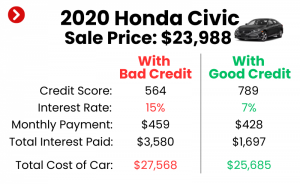

Lenders view a substantial down payment as a sign of financial responsibility and lower risk. It demonstrates that you’re committed to the purchase and have a vested interest in the vehicle. This can lead to better interest rates, more favorable loan terms, and a higher likelihood of loan approval, especially if your credit score isn’t perfect.

A larger down payment essentially acts as collateral for the lender. It reduces their exposure, making them more willing to offer you attractive conditions.

6. It Protects Against Negative Equity (Being Upside Down)

Negative equity, often called being "upside down" on your loan, occurs when you owe more on your car than its current market value. This is a common problem due to rapid depreciation, especially with new cars. A significant down payment creates a buffer against this, helping you maintain positive equity from the start.

Common mistakes to avoid are underestimating how quickly cars lose value. A good down payment is your best defense against negative equity.

How Much Down For Car Loan? The Golden Rule & Reality

Now for the million-dollar question: "How much down for a car loan?" While there’s no single magic number that fits everyone, financial experts often recommend a benchmark to aim for.

The "20% Rule" for New Cars

For new vehicles, the widely cited "golden rule" is to put down 20% of the purchase price. This percentage is generally considered ideal for several reasons:

- It significantly reduces your loan amount.

- It helps you avoid negative equity as the car depreciates.

- It usually qualifies you for better interest rates.

For a $30,000 new car, a 20% down payment would be $6,000. While this might seem like a lot, the long-term benefits are substantial.

For Used Cars: Aim for 10% or More

Used cars typically depreciate at a slower rate than new cars, as much of their initial depreciation has already occurred. For this reason, a down payment of 10% or more is often recommended for used vehicles.

However, the more you can put down, the better. Any amount above 10% for a used car will further enhance your financial position and provide the benefits discussed earlier.

The Reality: Average Down Payments

While 20% is the ideal, many people put down less. According to industry data, the average down payment on a new car in recent years has hovered around 11-12%, and for a used car, it’s typically around 6-7%. This disparity highlights that while the ideal is high, affordability often dictates a lower initial payment for many buyers.

This isn’t to say a lower down payment is always bad. It simply means you need to be more aware of the associated risks and plan accordingly.

Key Factors Influencing Your Ideal Down Payment

The "perfect" down payment for you will depend on several personal financial factors and the specifics of the car you’re buying. Let’s break down these critical considerations.

1. Your Credit Score

Your credit score plays a massive role in auto financing.

- Excellent Credit (720+): If you have a stellar credit score, lenders view you as a low-risk borrower. You might qualify for attractive interest rates even with a smaller down payment, or even a zero-down loan. However, putting more down can still further reduce your overall costs.

- Good to Average Credit (660-719): A solid down payment here can significantly improve your chances of approval and help you secure a better interest rate than you might otherwise get. It compensates for any perceived slight risk.

- Poor Credit (Below 660): If your credit score is low, a larger down payment becomes even more critical. It can be the difference between getting approved or denied, and it will almost certainly help you get a more reasonable interest rate than if you put nothing down. Lenders see it as a strong commitment.

2. The Car’s Price & Value

The more expensive the car, the larger your down payment will ideally be. A 20% down payment on a $50,000 luxury car is $10,000, whereas on a $20,000 economy car, it’s $4,000.

Consider the car’s depreciation rate. Some vehicles hold their value better than others. If you’re buying a car known for rapid depreciation, a larger down payment offers more protection against negative equity.

3. Your Budget & Financial Health

Before deciding on a down payment, take a hard look at your overall financial picture.

- Monthly Payment Comfort: How much can you comfortably afford each month without straining your budget? A larger down payment directly lowers this figure.

- Emergency Fund: Never deplete your emergency savings to make a down payment. You need a financial safety net for unexpected expenses.

- Other Debts: If you have high-interest debts, prioritize paying those down first. It might be smarter to make a slightly smaller down payment and tackle credit card debt.

- Future Goals: Are you saving for a house, retirement, or another big expense? Ensure your down payment doesn’t derail these goals.

4. Loan Term

The length of your loan (e.g., 36, 60, 72 months) also impacts your down payment decision.

- Shorter Loan Terms: These generally mean higher monthly payments but less interest paid overall. A larger down payment can help make a shorter loan term more affordable.

- Longer Loan Terms: While offering lower monthly payments, longer terms mean you pay more in interest over time and stay in debt longer. A substantial down payment can mitigate some of these drawbacks by reducing the principal amount from the start.

Based on my experience, opting for the shortest loan term you can comfortably afford, coupled with a good down payment, is often the most financially sound strategy.

5. Interest Rates

Current interest rates significantly influence the total cost of your loan.

- High-Interest Rates: If rates are high, a larger down payment becomes even more valuable. It reduces the amount subject to those high rates, saving you considerable money over the life of the loan.

- Low-Interest Rates: Even with low rates, a down payment still reduces your total interest paid and lowers your monthly obligation.

6. Dealer Incentives & Promotions

Sometimes dealerships or manufacturers offer special promotions, such as "zero down" deals or cash back incentives.

While these can be tempting, always read the fine print. Zero-down loans often come with higher interest rates or require excellent credit. A cash-back incentive might be better used as part of your down payment rather than spent elsewhere.

The Benefits of Making a Larger Down Payment

Let’s reiterate why committing to a substantial down payment is almost always a winning strategy for car buyers.

- Lower Monthly Payments: This frees up cash for other necessities or savings.

- Less Interest Paid Over Time: A direct reduction in the overall cost of your car.

- Faster Equity Build-Up: You own more of your car sooner, protecting you from depreciation.

- Better Loan Terms (Rate & Approval): Lenders reward lower risk with better offers.

- Reduced Risk of Negative Equity: Essential protection against being upside down on your loan.

- Peace of Mind: Knowing you have a smaller debt and more equity provides financial comfort.

The Risks of a Small or No Down Payment

While appealing on the surface, opting for a minimal or zero down payment carries several significant risks. These can lead to long-term financial strain and make your car purchase more expensive than necessary.

- Higher Monthly Payments: Borrowing more means paying more each month, which can strain your budget.

- More Interest Paid: A larger principal loan amount means you’ll accrue and pay significantly more in interest over the life of the loan.

- Increased Risk of Negative Equity: You’re more likely to owe more than your car is worth, especially in the early years. This can be problematic if you need to sell or trade in the car prematurely.

- Difficulty with Loan Approval: Lenders may be hesitant to approve loans with no down payment, particularly for buyers with less-than-perfect credit.

- Potential for Higher Insurance Costs (GAP Insurance): If you’re upside down on your loan, your standard auto insurance might not cover the full difference if your car is totaled or stolen. You might need to purchase Guaranteed Asset Protection (GAP) insurance, an additional cost, to cover this gap.

- Longer Loan Term: To make monthly payments affordable with a zero down payment, you might be pushed into a longer loan term, meaning you’re in debt for more years.

Pro Strategies for Saving for Your Down Payment

Saving for a down payment doesn’t have to be an insurmountable challenge. With a little planning and discipline, you can build up a significant sum.

- Set a Clear Goal: Determine the exact amount you want to save for your down payment. Use the 20% rule for new cars or 10% for used cars as your starting point.

- Create a Dedicated Savings Account: Open a separate savings account specifically for your car down payment. This makes it easier to track your progress and avoids accidentally spending the money.

- Cut Unnecessary Expenses: Review your monthly budget and identify areas where you can cut back. Even small sacrifices, like eating out less or canceling unused subscriptions, can add up quickly.

- Sell Unused Items: Declutter your home and sell items you no longer need or use. Online marketplaces make this easier than ever. This provides an immediate boost to your savings.

- Consider a Side Hustle: Take on a part-time job or freelance work to earn extra income specifically for your down payment. Every extra dollar goes a long way.

- Automate Savings: Set up automatic transfers from your checking account to your down payment savings account each payday. "Pay yourself first" ensures you’re consistently contributing to your goal.

Common Mistakes to Avoid When Planning Your Down Payment

Even with the best intentions, buyers can fall into common traps when it comes to their car down payment. Being aware of these pitfalls can save you money and stress.

- Not Saving Enough: Rushing into a purchase without a sufficient down payment can lead to higher monthly costs and greater risk of negative equity. Take your time to save properly.

- Ignoring the Total Cost: Focusing solely on the monthly payment or the sticker price can be misleading. Always consider the total amount you’ll pay over the life of the loan, including interest, when evaluating your down payment.

- Draining Your Emergency Fund: Your emergency fund is crucial for unexpected life events. Do not use it for a car down payment, no matter how tempting it is to get a lower monthly payment.

- Falling for "Zero Down" Traps Without Understanding Terms: While zero-down offers exist, they often come with trade-offs like higher interest rates or extended loan terms. Always compare the total cost of a zero-down loan versus a loan with a down payment.

- Underestimating Depreciation: Cars lose value quickly. Failing to account for this rapid depreciation can leave you in a negative equity situation, especially with a low down payment.

Frequently Asked Questions About Car Loan Down Payments

Let’s address some common questions that arise when considering how much to put down for a car loan.

Is a down payment always required?

No, a down payment is not always required. Many lenders offer "zero down" car loans, especially for buyers with excellent credit. However, as discussed, these often come with higher overall costs and risks.

Can I use my trade-in as a down payment?

Absolutely! Using your current vehicle as a trade-in is a very common and smart way to fund your down payment. The value of your trade-in is subtracted from the new car’s price, reducing the amount you need to finance. This is often the easiest way for many people to meet down payment recommendations.

What if I have bad credit?

If you have bad credit, a larger down payment becomes even more critical. It acts as a significant mitigating factor for lenders, demonstrating your commitment and reducing their risk. It can often be the difference between approval and denial, and it will almost certainly help you secure a better interest rate than if you put nothing down.

Does a down payment affect my car insurance?

While a down payment doesn’t directly affect your car insurance premiums, it can indirectly influence your coverage needs. If you have a large down payment and significant equity, you might opt for higher deductibles or choose not to carry GAP insurance. Conversely, a small or no down payment often means you’ll want GAP insurance to protect against negative equity, adding to your overall cost.

Is 10% a good down payment on a car?

For a new car, 10% is a decent start, but it’s below the ideal 20%. It will reduce your monthly payments and interest, but you might still face a higher risk of negative equity in the early years. For a used car, 10% is generally considered a good and solid down payment.

Conclusion: Drive Away with Confidence

Deciding "how much down for a car loan" is one of the most impactful financial choices you’ll make during your car buying journey. While the idea of a large upfront payment might seem daunting, the benefits of making a substantial down payment – from lower monthly payments and reduced interest to building equity faster and gaining peace of mind – are undeniable.

Based on my experience, a well-planned down payment is the foundation of a healthy auto loan. It sets you up for financial success, protects you from common pitfalls like negative equity, and ultimately makes your car ownership experience far more enjoyable and affordable. Don’t just focus on the shiny new car; focus on the smart financing that gets you there. Start saving today, research your options, and drive away not just in a new car, but with a smart financial decision under your belt.

For more insights into managing your car finances, explore our article on to fully grasp how interest impacts your total cost. You might also find valuable resources on car financing at reputable sites like Experian’s Auto Loan Resources.