How Much Interest Do I Really Pay On A Car Loan? Unmasking the True Cost of Your Vehicle

How Much Interest Do I Really Pay On A Car Loan? Unmasking the True Cost of Your Vehicle Carloan.Guidemechanic.com

The excitement of buying a new car is undeniable. The gleaming paint, the new car smell, the promise of freedom on the open road – it’s a powerful feeling. However, amidst this excitement, it’s all too easy to get swept up in the thrill and overlook one of the most significant financial aspects of your purchase: the interest you’ll pay on your car loan.

Many car buyers focus almost exclusively on the monthly payment, often neglecting the total cost of borrowing. This oversight can lead to paying thousands more than necessary over the life of the loan. Understanding "how much interest do I pay on a car loan" isn’t just a financial detail; it’s a critical component of smart vehicle ownership.

How Much Interest Do I Really Pay On A Car Loan? Unmasking the True Cost of Your Vehicle

This comprehensive guide is designed to pull back the curtain on car loan interest. We’ll demystify how it’s calculated, explore the factors that influence your rate, and provide actionable strategies to help you minimize your interest payments. By the end, you’ll be equipped with the knowledge to make informed decisions and save a substantial amount of money.

The Core of Car Loans: Understanding Interest

At its heart, interest is simply the cost of borrowing money. When you take out a car loan, a lender provides you with funds to purchase your vehicle, and in return, they charge you a percentage of that borrowed amount as interest. This charge is their profit for the service of lending you money.

Car loans are typically structured as simple interest loans that are amortized over a set period. This means that the interest you pay is calculated daily on your outstanding principal balance. As you make payments, a portion goes towards the interest accrued, and the rest reduces your principal balance.

Over time, as your principal decreases, the amount of interest calculated each day also goes down. This is why, in the early stages of your loan, a larger portion of your monthly payment goes towards interest, while later payments allocate more towards paying down the principal. Recognizing this structure is fundamental to understanding your total repayment obligation.

Decoding Your Interest Rate vs. APR

When discussing car loan costs, you’ll often hear two terms: the interest rate and the Annual Percentage Rate (APR). While closely related, they are not the same, and understanding the distinction is crucial.

Your interest rate is the percentage charged by the lender for borrowing the principal amount. It directly impacts how much extra money you pay on top of the car’s price. This is the figure that often grabs headlines and forms the basis of simple calculations.

The Annual Percentage Rate (APR), on the other hand, represents the total cost of borrowing money for a year, expressed as a percentage. It includes not only the interest rate but also any additional fees associated with the loan, such as origination fees, documentation fees, or administrative charges. Based on my experience, many borrowers overlook the distinction between these two figures, leading to an incomplete understanding of their true borrowing costs.

Why APR Matters More: When comparing loan offers, the APR is almost always the more accurate and useful figure. It provides a holistic view of the loan’s cost, allowing you to compare apples to apples across different lenders. A loan might have a slightly lower interest rate but a higher APR due to substantial fees, making it ultimately more expensive. Always ask for and compare the APR when shopping for a car loan.

Key Factors That Drive Your Car Loan Interest

The interest rate you qualify for on a car loan isn’t random; it’s a carefully calculated figure based on a variety of factors. Each element plays a significant role in how much interest you’ll ultimately pay.

Your Credit Score: The Ultimate Indicator of Risk

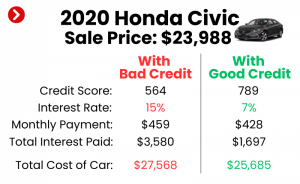

Your credit score is arguably the most influential factor in determining your car loan interest rate. Lenders use this three-digit number to assess your creditworthiness – essentially, how likely you are to repay your debt. A higher credit score signals to lenders that you are a responsible borrower with a history of timely payments, making you a lower risk.

Conversely, a lower credit score suggests a higher risk of default. To compensate for this increased risk, lenders will typically offer a higher interest rate. This higher rate serves as a buffer, ensuring they earn more money if the loan is repaid and covering potential losses if it isn’t. Pro tips from us: always check your credit score and report before applying for a car loan. This allows you to address any inaccuracies and understand where you stand.

Loan Term (Duration): The Time-Value of Money

The loan term refers to the length of time you have to repay the loan, usually expressed in months (e.g., 36, 48, 60, 72, or even 84 months). This factor has a dual impact: it affects both your monthly payment and the total interest paid.

A longer loan term will result in lower monthly payments, which can be appealing if you’re trying to keep your budget tight. However, extending the repayment period means you’re borrowing the money for a longer time, allowing more interest to accrue. This inevitably leads to a higher total amount of interest paid over the life of the loan.

Conversely, a shorter loan term will mean higher monthly payments, as you’re condensing the repayment into fewer installments. The significant benefit, however, is that you’ll pay substantially less in total interest because you’re paying off the principal faster. For example, a $25,000 loan at 5% APR over 60 months might cost you around $3,300 in total interest, while the same loan over 72 months could push that total interest past $4,000.

Down Payment Amount: Reducing Your Borrowed Principal

A down payment is the initial sum of money you pay upfront towards the purchase of the vehicle. This directly reduces the amount of money you need to borrow from the lender. The smaller the principal loan amount, the less interest will accrue over the loan term.

Beyond simply reducing the principal, a substantial down payment can also influence the interest rate you’re offered. Lenders often view a larger down payment as a sign of financial stability and commitment. This reduces their risk exposure, potentially qualifying you for a lower interest rate than someone financing the entire vehicle cost. Aim for at least 10-20% of the vehicle’s price if possible.

Vehicle Age & Type: Collateral Assessment

The type and age of the vehicle you’re financing can also subtly affect your interest rate. Lenders consider the car as collateral for the loan. If you default, they seize the car to recoup their losses.

New cars generally depreciate rapidly, but they tend to be seen as more reliable and less likely to require immediate costly repairs. Lenders might offer slightly lower rates on new cars because the collateral is perceived as more stable. Used cars, while often more affordable upfront, can sometimes carry slightly higher interest rates due to their age, mileage, and the potential for greater maintenance issues, which could impact their resale value as collateral.

Market Interest Rates (Economic Conditions): Beyond Your Control

Sometimes, factors entirely outside your personal financial situation influence car loan rates. Broader economic conditions, particularly decisions made by central banks (like the Federal Reserve in the U.S.), play a significant role. When the Federal Reserve raises its benchmark interest rate, it typically leads to higher interest rates across various lending products, including car loans.

Conversely, when the economy slows down, central banks might lower rates to stimulate borrowing and spending. While you can’t control these macro-economic forces, being aware of the general interest rate environment can help you decide if it’s a good time to buy or refinance.

Lender & Loan Product: The Importance of Shopping Around

Not all lenders are created equal, and their loan products can vary significantly. Banks, credit unions, and dealership financing all have different lending criteria, overhead costs, and target markets. This means that the same borrower with the same credit score could receive vastly different interest rate offers from different institutions.

Credit unions, for instance, are often known for offering more competitive rates to their members due to their non-profit cooperative structure. Dealerships might offer promotional rates through their captive finance arms, but these are often reserved for buyers with excellent credit. Common mistakes to avoid are accepting the first loan offer you receive, especially if it’s from the dealership without exploring other options.

How to Calculate the Interest You’ll Pay: The Amortization Schedule

Understanding the factors influencing your interest rate is one thing, but knowing how to calculate the actual interest you’ll pay is another crucial step. Car loans are typically amortized, meaning each monthly payment is structured to gradually pay down both the principal balance and the interest accrued.

Understanding Amortization

An amortization schedule breaks down each of your loan payments into the portions that go towards principal and interest over the entire loan term. In the early months of an amortizing loan, a larger percentage of your payment is allocated to interest. This is because your outstanding principal balance is at its highest, and therefore, the daily interest accrual is also at its peak.

As you continue to make payments, your principal balance decreases. Consequently, the amount of interest calculated each month also goes down. This shifts the allocation of your payment, so a progressively larger portion goes towards reducing your principal. This process is why paying extra principal can be so effective in saving interest.

The Formula (Simplified) for Monthly Interest

While lenders use complex systems, you can understand the basic calculation for the interest portion of a single month’s payment with a simple formula:

Monthly Interest Payment = (Outstanding Principal Balance × Annual Interest Rate) / 12

Let’s walk through an example:

- Loan Amount (Principal): $25,000

- Annual Interest Rate: 5% (or 0.05 as a decimal)

- Loan Term: 60 months

Month 1 Calculation:

- Interest for Month 1: ($25,000 × 0.05) / 12 = $104.17

- If your total monthly payment is, say, $471.78, then $104.17 goes to interest, and the remaining $367.61 ($471.78 – $104.17) goes to principal.

- Your new principal balance for Month 2 would be $25,000 – $367.61 = $24,632.39.

Month 2 Calculation:

- Interest for Month 2: ($24,632.39 × 0.05) / 12 = $102.63

- Now, a slightly smaller amount goes to interest, and more goes to principal.

This iterative process continues each month until the loan is fully repaid. While doing this manually for 60 months would be tedious, understanding the principle helps you see how interest accumulates.

Using Online Calculators

Fortunately, you don’t need to be a math wizard to figure out your total interest. There are numerous free, reliable online car loan calculators that can do the heavy lifting for you. These tools allow you to input the loan amount, interest rate, and term, and they will instantly generate an amortization schedule, showing you exactly how much interest you’ll pay each month and over the life of the loan.

Pro tips from us: utilize these calculators extensively when you’re shopping for a car. Try different scenarios (e.g., higher down payment, shorter term) to see the impact on your total interest paid. A trusted external source like Bankrate offers an excellent car loan calculator to help you visualize these costs.

Strategies to Significantly Reduce Your Car Loan Interest

Now that you understand how car loan interest works, the good news is you have several powerful strategies at your disposal to minimize the amount you pay. Implementing even one of these can lead to substantial savings over the life of your loan.

1. Boost Your Credit Score Before Applying

As we discussed, your credit score is king when it comes to interest rates. Taking steps to improve it before you apply for a car loan can significantly lower the rate you’re offered. Focus on:

- Paying all your bills on time, every time: Payment history is the biggest factor in your score.

- Reducing your credit card balances: This lowers your credit utilization ratio, a key scoring factor.

- Checking your credit report for errors: Disputing and correcting any inaccuracies can quickly boost your score.

Even a small improvement in your credit score can translate into a lower interest rate, saving you hundreds or even thousands of dollars. For a deeper dive into improving your credit, consider reading our article on .

2. Make a Larger Down Payment

This is one of the most straightforward ways to reduce interest. By paying more upfront, you directly decrease the principal amount you need to borrow. Less borrowed principal means less interest will accrue over the loan’s duration.

Beyond the direct reduction in interest, a larger down payment also signals to lenders that you are a less risky borrower. This can sometimes qualify you for an even lower interest rate than you might have received with a minimal down payment. Aim for 20% if possible to also mitigate the effects of rapid depreciation.

3. Choose a Shorter Loan Term

While a longer loan term offers lower monthly payments, it comes at the cost of significantly more interest paid. If your budget allows, opting for the shortest loan term you can comfortably afford will lead to substantial interest savings.

For instance, choosing a 48-month loan instead of a 72-month loan, even with slightly higher monthly payments, can drastically cut down on the total interest. It’s a trade-off between monthly affordability and overall cost, and prioritizing a shorter term is almost always financially advantageous in the long run.

4. Shop Around for the Best Rates

This cannot be stressed enough: do not simply accept the financing offered by the dealership. Dealerships often add a markup to the interest rates they secure from lenders, which becomes their profit.

Pro tips from us: get pre-approved for a loan from at least two or three different sources (banks, credit unions, online lenders) before you even step foot in a dealership. This gives you a benchmark rate and empowers you to negotiate. You can then use these pre-approvals to either secure a better rate from the dealership or simply go with the best offer you’ve already found.

5. Consider Refinancing Your Loan

If you’ve already purchased a car and your credit score has improved, or if market interest rates have dropped since you took out your initial loan, refinancing could be a smart move. Refinancing involves taking out a new loan to pay off your existing car loan, ideally at a lower interest rate.

This strategy can significantly reduce the total interest you’ll pay over the remaining life of the loan. It’s particularly effective if you had a lower credit score when you first bought the car but have since built a strong payment history. For a detailed guide on this, check out our article on .

6. Make Extra Payments or Pay Off Early

Even small extra payments can make a big difference. Since car loans are typically simple interest, any additional money you pay directly towards the principal reduces the amount on which future interest is calculated.

You can do this by:

- Adding a little extra to your regular monthly payment.

- Making an extra payment whenever you receive a bonus or tax refund.

- Paying bi-weekly instead of monthly (this effectively adds one extra payment per year).

Before making extra payments, always confirm with your lender that the additional funds will be applied directly to the principal and that there are no prepayment penalties. While rare for car loans, it’s always good to check your loan agreement.

Common Pitfalls and How to Avoid Them

Even with the best intentions, car buyers can fall into common traps that lead to paying more interest than necessary. Being aware of these pitfalls is your first line of defense.

1. Focusing Only on Monthly Payments

This is perhaps the most common mistake. Salespeople are adept at negotiating based on a target monthly payment, often extending the loan term to achieve it. While a lower monthly payment sounds appealing, it almost always means you’ll pay significantly more in total interest over the longer term. Always ask for the total cost of the loan, including all interest and fees.

2. Not Shopping Around for Lenders

As discussed, relying solely on dealership financing or the first offer you receive is a missed opportunity. Different lenders have different rates. Taking the time to compare pre-approvals from multiple sources can save you thousands of dollars in interest over the life of the loan.

3. Ignoring the APR

The interest rate is important, but the APR tells the whole story. If you only look at the interest rate and ignore other fees rolled into the APR, you might choose a seemingly cheaper loan that actually costs more. Always compare loan offers using their APR.

4. Financing Add-ons into the Loan

Dealerships often push add-ons like extended warranties, GAP insurance, paint protection, or undercoating. While some might be valuable, financing them into your car loan means you’re paying interest on these items for the entire loan term. If you want these add-ons, try to pay for them separately or negotiate a lower cash price.

5. Not Understanding Your Loan Agreement

Before signing any documents, read your loan agreement thoroughly. Understand the interest rate, APR, loan term, total amount financed, and any potential penalties (though prepayment penalties are rare for car loans, it’s good to be sure). Ask questions if anything is unclear. It’s your money, and you have the right to full clarity.

Conclusion

Understanding "how much interest do I pay on a car loan" is not just about crunching numbers; it’s about making financially savvy decisions that impact your long-term wealth. The interest you pay on your car loan represents a significant portion of your vehicle’s true cost, and with the right knowledge and strategies, you have the power to minimize it.

By improving your credit score, making a substantial down payment, choosing a shorter loan term, diligently shopping for the best rates, and even considering refinancing or making extra payments, you can dramatically reduce the total interest paid. Remember, a car purchase isn’t just about the vehicle itself; it’s about the financial journey you embark on to own it. Empower yourself with this knowledge, and drive away with confidence, knowing you’ve secured the best possible deal.