How Much Interest Is Too Much For A Car Loan: Your Expert Guide to Smart Borrowing

How Much Interest Is Too Much For A Car Loan: Your Expert Guide to Smart Borrowing Carloan.Guidemechanic.com

Navigating the world of car loans can feel like driving through a dense fog. You know you need a vehicle, but the terms, especially the interest rate, can be confusing. For many, the big question isn’t just "What’s a good interest rate?" but rather, "How much interest is too much for a car loan?" This is a crucial distinction that can save you thousands of dollars over the life of your loan.

As an expert blogger and professional SEO content writer who has spent years dissecting financial products, I understand the anxiety and confusion borrowers often face. My mission with this comprehensive guide is to empower you with the knowledge to identify fair interest rates, avoid predatory practices, and secure a car loan that aligns with your financial well-being. We’ll delve deep into every factor, offering insights and actionable strategies to ensure you make an informed decision.

How Much Interest Is Too Much For A Car Loan: Your Expert Guide to Smart Borrowing

Understanding Car Loan Interest Rates: The Core Concepts

Before we can determine what constitutes "too much" interest, it’s essential to grasp the fundamental concepts of car loan interest rates. This isn’t just about a single number; it’s about understanding the mechanics behind it.

What is an Interest Rate, Really?

At its heart, an interest rate is the cost of borrowing money. When you take out a car loan, the lender provides you with funds to purchase a vehicle, and in return, you agree to pay back the principal amount (the money you borrowed) plus an additional percentage – the interest. This interest is how lenders make a profit.

The interest rate is typically expressed as an annual percentage. It directly impacts your monthly payment and, more significantly, the total amount you will pay over the entire loan term. A seemingly small difference in the interest rate can lead to substantial savings or extra costs over several years.

APR vs. Interest Rate: Why the Distinction Matters

You’ll often hear two terms used: "interest rate" and "APR" (Annual Percentage Rate). While related, they are not always the same, and understanding the difference is vital for a clear picture of your loan’s true cost.

The interest rate is the percentage you pay on the principal loan amount. It’s the core cost of borrowing. However, the APR includes not only the interest rate but also other fees associated with the loan, such as origination fees, documentation fees, and sometimes even credit report fees.

Pro tips from us: Always focus on the APR when comparing loan offers. It provides a more accurate representation of the total annual cost of your credit. A loan with a lower stated interest rate but a higher APR due to hidden fees might actually cost you more in the long run.

Why Interest Rates Aren’t Just Numbers on a Page

Beyond the mathematical calculation, interest rates are a reflection of risk. Lenders assess your creditworthiness, the car’s value, and market conditions to determine the risk involved in lending you money. A higher risk often translates to a higher interest rate, as the lender seeks more compensation for taking on that perceived risk.

Your goal as a borrower is to present yourself as a low-risk candidate. By doing so, you unlock access to more favorable interest rates, which directly translates into lower overall costs for your vehicle.

What Really Drives Your Car Loan Interest Rate?

Many factors contribute to the interest rate you’re offered. Understanding these elements is your first step towards negotiating a better deal and avoiding an excessively high rate. Based on my experience, overlooking any of these can lead to unnecessarily expensive borrowing.

Your Credit Score: The Ultimate Game Changer

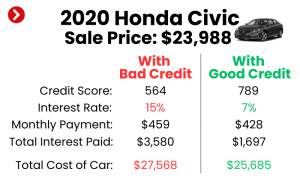

Undoubtedly, your credit score is the single most influential factor in determining your car loan interest rate. It’s a numerical representation of your financial responsibility and history of managing debt.

- Excellent Credit (780+): Borrowers in this category typically qualify for the lowest interest rates, often below 5% for new cars and sometimes even lower during promotional periods. Lenders view you as highly reliable.

- Good Credit (670-739): You’ll still receive competitive rates, usually in the 5-8% range for new cars. While not the absolute lowest, these are still very attractive offers.

- Fair Credit (580-669): Rates start to climb here, often ranging from 8-15% or more, particularly for used vehicles. Lenders perceive a slightly higher risk.

- Poor Credit (Below 580): This is where rates can become alarmingly high, potentially reaching 15-25% or even higher. Lenders are taking a significant risk, and their rates reflect that.

Common mistakes to avoid are: Not checking your credit score before applying for a loan. This leaves you blind to what kind of rates you should expect and makes you vulnerable to unfavorable offers. Always get a free copy of your credit report from AnnualCreditReport.com and understand your standing.

Loan Term Length: The Long and Short of It

The duration of your loan, known as the loan term, plays a significant role in your interest rate. Generally, longer loan terms (e.g., 72 or 84 months) come with higher interest rates than shorter terms (e.g., 36 or 48 months).

While a longer term means lower monthly payments, which can seem appealing, it significantly increases the total interest you pay over the life of the loan. Lenders charge more interest for longer terms because they are extending credit for a longer period, thus increasing their risk exposure and the time value of money.

Your Down Payment: Showing Your Commitment

Making a substantial down payment reduces the amount you need to borrow, which in turn lowers the lender’s risk. A larger down payment can often lead to a lower interest rate because you have more equity in the vehicle from day one.

A good rule of thumb is to aim for at least 10% for a used car and 20% for a new car. Beyond lowering your interest rate, a larger down payment can also help you avoid being "upside down" on your loan, meaning you owe more than the car is worth.

Vehicle Type: New vs. Used Car Dynamics

The type of vehicle you’re buying also influences the interest rate. New cars typically qualify for lower interest rates than used cars. This is because new cars hold their value better initially, are less prone to mechanical issues, and are less of a risk for the lender.

Used cars, on the other hand, depreciate faster, come with more potential for mechanical problems, and can be harder to repossess and sell if you default. These factors make them a higher risk for lenders, leading to higher interest rates.

Market Conditions: The Economy’s Ripple Effect

Broader economic factors and the prevailing market conditions also influence car loan interest rates. The Federal Reserve’s interest rate decisions, inflation, and the overall health of the economy can all cause rates to fluctuate.

When the economy is strong and the Fed raises rates, car loan interest rates tend to follow suit. Conversely, during economic downturns or periods of low inflation, rates might decrease to stimulate borrowing. While you can’t control these macro factors, being aware of them helps you understand why rates might be higher or lower at a given time.

Lender Type: Where You Borrow Matters

Not all lenders are created equal when it comes to interest rates. Different types of institutions have different business models and risk appetites.

- Banks: Often offer competitive rates, especially to customers with good credit.

- Credit Unions: Known for member-focused services and typically offer some of the best rates, as they are non-profit organizations.

- Dealerships (Captive Lenders): Can sometimes offer promotional rates (like 0% APR) on new cars, but their standard rates might be higher, especially for used cars or less-than-perfect credit. They also act as intermediaries, often adding their own markup to rates from other lenders.

- Online Lenders: Provide convenience and can offer competitive rates, but it’s crucial to research their reputation and terms carefully.

Pro tips from us: Always shop around and get pre-approved from multiple lenders before you step onto the dealership lot. This gives you leverage and a clear benchmark for what a fair rate looks like for your financial profile.

Defining "Too Much": Setting Your Car Loan Interest Rate Threshold

Now for the million-dollar question: How much interest is genuinely too much for a car loan? The answer isn’t a single number, but rather a range determined by your creditworthiness and the current market. However, we can establish clear thresholds that should raise immediate red flags.

Average Car Loan Interest Rates: A Benchmark

To know what’s too much, you first need to understand what’s considered average or good. These figures fluctuate with the market and your credit score, but here’s a general guideline based on recent trends:

- New Car Loan Rates:

- Excellent Credit (780+): 3.5% – 6% APR

- Good Credit (670-739): 5% – 8% APR

- Fair Credit (580-669): 8% – 14% APR

- Poor Credit (Below 580): 15% – 20%+ APR

- Used Car Loan Rates:

- Excellent Credit (780+): 4.5% – 7% APR

- Good Credit (670-739): 6% – 10% APR

- Fair Credit (580-669): 10% – 18% APR

- Poor Credit (Below 580): 18% – 25%+ APR

These ranges are averages and can vary significantly based on the loan term, down payment, and specific lender. However, they provide a solid starting point for comparison.

The "Red Flag" Zone: When to Pump the Brakes

Based on my experience, any interest rate significantly above the average for your credit tier should be considered a red flag. For example:

- If you have excellent credit (780+) and are offered anything above 7-8% APR for a new car loan, that’s likely too much. You should be able to secure a much lower rate.

- If you have good credit (670-739) and are offered anything above 10-12% APR for a new car, or 15% for a used car, it’s time to be very cautious. This indicates either a high markup or that the lender sees hidden risks.

- For anyone, an APR exceeding 20% for a standard car loan should almost always be considered too much. While those with very poor credit might face high rates, anything above this threshold often borders on predatory lending, making the car prohibitively expensive and difficult to pay off.

Predatory lenders often target vulnerable borrowers with high rates, excessive fees, and unfavorable terms. These loans can trap you in a cycle of debt, making it incredibly difficult to achieve financial stability.

Personal Financial Situation: Your Own "Too Much"

Beyond objective market averages, "too much" also depends on your personal financial situation. An interest rate that is technically "average" might still be too much for your budget if it pushes your monthly payments beyond what you can comfortably afford.

Always consider the total cost of the loan, not just the monthly payment. Use online car loan calculators to see how different interest rates impact the overall amount you’ll pay. A car loan payment should ideally not exceed 10-15% of your take-home pay, including insurance and fuel.

Strategies to Secure a Favorable Car Loan Interest Rate

Knowing what’s too much is only half the battle. The other half is implementing strategies to ensure you get the best possible rate. Here are proven methods to improve your chances.

1. Boost Your Credit Score

This is paramount. If your credit score isn’t in the "good" or "excellent" range, take steps to improve it before applying for a loan.

- Pay bills on time: Payment history is the biggest factor in your score.

- Reduce existing debt: Especially credit card debt, as high utilization hurts your score.

- Avoid new credit inquiries: Don’t open new credit accounts right before applying for a car loan.

- Correct errors on your credit report: Dispute any inaccuracies immediately.

Even a small bump in your score can significantly impact the interest rate you’re offered.

2. Save for a Larger Down Payment

As discussed, a larger down payment directly reduces the amount you need to borrow and signals financial responsibility to lenders. Aim for 20% for new cars and at least 10% for used cars if possible.

The more you put down upfront, the less interest you’ll pay over time, and the better your chances of securing a lower interest rate. It also helps mitigate the risk of being upside down on your loan.

3. Shop Around Extensively for Lenders

This is perhaps the most crucial actionable advice. Never accept the first loan offer you receive, especially from a dealership.

- Get pre-approved: Apply for pre-approval from multiple lenders (banks, credit unions, online lenders) within a short window (e.g., 14-30 days). Multiple inquiries for the same type of loan within this period are typically treated as a single hard inquiry on your credit report, minimizing impact.

- Compare offers: Line up your pre-approval offers and use the best one as leverage when negotiating with the dealership’s financing department. They may try to beat it.

- Consider credit unions: Based on my experience, credit unions consistently offer some of the most competitive rates due to their member-centric model.

4. Negotiate the Loan Terms

Don’t be afraid to negotiate. Everything is usually negotiable, including the interest rate, especially if you have competing offers.

- Focus on the APR: As mentioned, look at the full APR, not just the stated interest rate.

- Question fees: Ask about all fees included in the loan. Some might be negotiable or avoidable.

- Be prepared to walk away: If a lender isn’t willing to offer a fair rate, be ready to take your business elsewhere. This is where your pre-approvals come in handy.

5. Choose a Shorter Loan Term (If Affordable)

While a longer term offers lower monthly payments, it costs you more in total interest. If your budget allows, opt for the shortest loan term you can comfortably afford.

A 48- or 60-month loan will almost always have a lower interest rate than a 72- or 84-month loan, and you’ll pay significantly less overall. It’s a trade-off between monthly payment comfort and total cost.

6. Consider Refinancing Later

If you’re stuck with a high interest rate due to poor credit or market conditions at the time of purchase, don’t despair. Once your credit score improves or market rates drop, you might be able to refinance your car loan for a lower rate.

Refinancing involves taking out a new loan to pay off your old one, ideally with more favorable terms. This can save you money on interest and potentially lower your monthly payments.

Common Car Loan Interest Rate Mistakes to Sidestep

Even savvy consumers can fall into traps when financing a car. Based on my years observing lending practices, here are some common mistakes to actively avoid to ensure you don’t end up paying too much interest.

1. Focusing Solely on the Monthly Payment

Dealerships often try to steer conversations around the "affordable" monthly payment. While your budget is important, fixating only on this number can lead to an extended loan term, a higher interest rate, and a much larger total cost over time.

Always ask for the full price of the car, the interest rate (APR), and the total amount you will pay over the loan term. Don’t let a low monthly payment distract you from a bad overall deal.

2. Not Understanding All the Fees and Add-ons

Car loans can come with various fees, and dealerships might try to bundle in expensive add-ons like extended warranties, GAP insurance, or anti-theft protection without clearly explaining them. These add-ons are often financed into the loan, increasing your principal and, consequently, the interest you pay.

Carefully review every line item on the contract. Ask what each fee is for and if it’s mandatory. Decline any add-ons you don’t need or can get cheaper elsewhere.

3. Believing "Zero Percent APR" Deals are Always the Best Option

While 0% APR sounds fantastic, these offers are usually reserved for buyers with impeccable credit scores (780+) and often on specific new car models. They also typically involve shorter loan terms.

Furthermore, opting for 0% APR might mean forfeiting other incentives, such as cash rebates or discounts. Sometimes, taking a slightly higher interest rate with a significant cash rebate can actually save you more money overall. Do the math!

4. Letting the Dealership Run Multiple Credit Checks

When you apply for financing at a dealership, they might send your application to multiple lenders. Each "hard inquiry" can slightly ding your credit score. While inquiries for the same type of loan within a short period (typically 14-30 days) are usually grouped, excessive checks outside this window can be detrimental.

This is another reason why getting pre-approved from one or two lenders yourself is a superior strategy. It limits inquiries and gives you control.

5. Ignoring Your Debt-to-Income Ratio

Lenders look at your debt-to-income (DTI) ratio to assess your ability to take on more debt. If your DTI is too high, even with a good credit score, you might be offered a higher interest rate or denied the loan altogether.

Keep your DTI below 40% if possible. This shows lenders you have enough disposable income to comfortably manage your car payments.

When to Say No: Recognizing Unacceptable Car Loan Offers

Sometimes, despite your best efforts, you might receive a car loan offer that is simply not in your best interest. Knowing when to walk away is a powerful negotiation tool and a crucial part of smart borrowing.

High Rates Despite Good Credit

If your credit score is strong (e.g., 700+) and you’re being offered an APR in the double digits, it’s a clear sign to walk away. This could indicate an opportunistic lender trying to take advantage, or that you haven’t shopped around enough. Revisit your pre-approvals and consider other lenders.

Pressure Tactics and Lack of Transparency

Any lender or dealership that pressures you to sign immediately, refuses to provide clear answers, or makes you feel uncomfortable is a major red flag. A reputable lender will be transparent about all terms and fees and give you time to review the contract.

Pro tips from us: Never sign a contract you don’t fully understand. If you feel rushed or confused, simply say "no" and leave. There will always be another car and another loan.

Unreasonable Loan Terms

Be wary of excessively long loan terms (e.g., 84 months or more), especially for used cars. While they offer low monthly payments, they expose you to more interest and a higher risk of being upside down on your loan for a significant period.

Similarly, if the loan includes a balloon payment at the end or requires excessively high fees, it’s likely an unfavorable offer.

Financing Unnecessary Add-ons

If a dealership insists on financing add-ons you don’t want or need, and won’t remove them from the loan, this is a deal-breaker. You shouldn’t pay interest on things that don’t add value to you.

Remember, the goal is to get a car loan that is fair, affordable, and sustainable for your financial future. Don’t let the excitement of a new vehicle cloud your judgment.

Conclusion: Empowering Your Car Loan Journey

Determining "how much interest is too much for a car loan" is not about finding a magic number, but rather about understanding the variables, leveraging your financial health, and being an informed consumer. By comprehending the factors that influence interest rates, proactively improving your credit, shopping around for the best offers, and meticulously reviewing loan terms, you empower yourself to make smart decisions.

Never settle for an interest rate that feels excessive for your financial profile. Always compare APRs, question fees, and prioritize the total cost of the loan over just the monthly payment. Your diligence today can save you thousands of dollars and significant financial stress tomorrow.

Armed with this comprehensive guide, you are now better equipped to navigate the complexities of car financing. Go forth, research, compare, and secure a car loan that truly works for you, ensuring your journey on the road ahead is smooth and financially sound. If you want to learn more about managing car expenses, check out our article on Smart Budgeting for Your First Car. For broader financial literacy, explore resources from the Consumer Financial Protection Bureau.