How Much Interest Should I Pay On A Car Loan? A Comprehensive Guide to Saving Thousands

How Much Interest Should I Pay On A Car Loan? A Comprehensive Guide to Saving Thousands Carloan.Guidemechanic.com

Navigating the world of car loans can often feel like deciphering a complex financial puzzle. One of the most significant pieces of that puzzle, and often the most misunderstood, is interest. It’s not just a small number; it’s the extra cost you pay to borrow money, and it can add up to thousands of dollars over the life of your loan. So, how much interest should I pay on a car loan? This isn’t a question with a single, simple answer, but rather one that requires a deep dive into various factors that influence your borrowing costs.

As an expert blogger and SEO content writer with years of experience observing consumer finance trends, I’ve seen firsthand how understanding car loan interest can empower buyers to make smarter decisions. This comprehensive guide will break down everything you need to know, from the basics of interest rates to advanced strategies for securing the best possible deal. Our ultimate goal is to equip you with the knowledge to minimize your interest payments and keep more money in your pocket. Let’s embark on this journey to financial savvy.

How Much Interest Should I Pay On A Car Loan? A Comprehensive Guide to Saving Thousands

Understanding Car Loan Interest: The Fundamental Concepts

Before we can discuss what a "good" interest rate looks like, it’s crucial to grasp the foundational concepts of car loan interest. This isn’t just about a percentage; it’s about the very mechanism that determines the true cost of your vehicle.

What Exactly Is Interest?

In simple terms, interest is the cost of borrowing money. When a lender provides you with a car loan, they are taking a risk. Interest is their compensation for that risk, as well as the profit they make from lending you the capital. It’s expressed as a percentage of the principal loan amount.

This percentage is applied over the loan’s term, meaning the longer you borrow the money, the more interest you will typically pay overall. Understanding this basic principle is the first step toward controlling your car ownership costs.

APR vs. Interest Rate: Why the Distinction Matters

You’ll often hear the terms "interest rate" and "APR" (Annual Percentage Rate) used interchangeably, but there’s a critical difference, especially when comparing car loan offers. The interest rate is solely the cost of borrowing the principal amount. It doesn’t include any additional fees.

APR, on the other hand, provides a more complete picture of the total cost of borrowing. It includes the interest rate plus any other fees associated with the loan, such as origination fees, processing fees, or closing costs, spread out over the loan term. When comparing loan offers, always look at the APR, as it gives you the true annual cost of the loan. A lower APR always means a cheaper loan overall.

Why Interest Matters: The True Cost of Your Vehicle

Many car buyers focus solely on the monthly payment, often overlooking the total interest paid over the life of the loan. This is a common mistake that can cost you thousands. For example, a $30,000 car loan at 3% interest over 60 months will have a significantly lower total cost than the same loan at 7% interest.

The interest you pay directly impacts the overall price you pay for your car. It’s the "hidden" expense that can inflate your vehicle’s cost far beyond its sticker price. Understanding this makes optimizing your interest rate a top priority.

Factors That Determine Your Car Loan Interest Rate

Several key elements come into play when lenders calculate the interest rate they offer you. Knowing these factors can help you prepare and position yourself for the best possible terms.

Your Credit Score: The Ultimate Game Changer

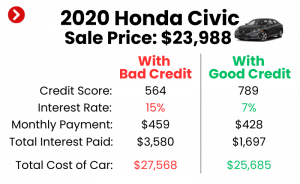

Your credit score is arguably the most significant factor influencing your car loan interest rate. Lenders use it as a primary indicator of your creditworthiness – your likelihood of repaying the loan. A higher credit score (typically 700 and above) signals lower risk to lenders, resulting in lower interest rates. Conversely, a lower score suggests higher risk, leading to higher rates.

Based on my experience, improving your credit score, even by a few points, before applying for a car loan can save you a substantial amount of money. It demonstrates financial responsibility and makes you a more attractive borrower.

The Loan Term: Shorter vs. Longer

The length of your loan, known as the loan term, directly impacts your interest rate. Shorter loan terms (e.g., 36 or 48 months) typically come with lower interest rates because the lender’s risk is reduced. They get their money back faster. However, shorter terms usually mean higher monthly payments.

Longer loan terms (e.g., 72 or 84 months) often have higher interest rates because the lender is taking on more risk over an extended period. While they offer lower monthly payments, you’ll end up paying significantly more in total interest over the life of the loan. It’s a trade-off between monthly affordability and total cost.

Your Down Payment: Showing Your Commitment

Making a substantial down payment can significantly reduce the amount you need to borrow, which in turn can lead to a lower interest rate. A larger down payment demonstrates your financial commitment to the purchase and reduces the lender’s exposure. It also helps to prevent you from being "upside down" on your loan, where you owe more than the car is worth.

Pro tips from us: Aim for at least 10-20% of the car’s purchase price as a down payment. This not only lowers your interest but also reduces your monthly payments and overall debt.

New vs. Used Car: Risk Assessment for Lenders

The type of car you’re financing also plays a role. New cars generally come with lower interest rates than used cars. This is because new cars hold their value better initially, making them less of a risk for lenders. If you default, the lender can recoup more of their investment by repossessing and selling a newer vehicle.

Used cars, especially older models, are considered higher risk due to depreciation, potential mechanical issues, and less predictable resale values. As a result, lenders often charge higher interest rates for used car loans to compensate for this increased risk.

Current Market Rates: The Economic Landscape

Economic conditions and the prevailing interest rate environment also influence car loan rates. When the Federal Reserve raises or lowers its benchmark interest rates, it impacts borrowing costs across the board, including auto loans. During periods of low interest rates, you’ll likely find more favorable car loan deals.

Conversely, in an environment of rising rates, car loans become more expensive. This is a factor largely beyond your control, but being aware of it helps set realistic expectations for the rates you might receive.

Lender Type: Shop Around for the Best Deal

The type of institution you borrow from can also affect your interest rate. Banks, credit unions, and dealership financing all have different structures and often offer varying rates. Credit unions, being not-for-profit organizations, are frequently known for offering some of the most competitive interest rates.

Dealership financing can be convenient, but their rates might not always be the best. It’s crucial to shop around and get quotes from multiple lenders before stepping foot in a dealership.

Debt-to-Income Ratio (DTI): Your Financial Capacity

Your debt-to-income (DTI) ratio is another metric lenders consider. It compares your total monthly debt payments to your gross monthly income. A lower DTI ratio indicates that you have more disposable income to cover your loan payments, making you a less risky borrower. Lenders prefer borrowers with a DTI of 36% or lower.

A high DTI might signal to lenders that you are already stretched financially, potentially leading to a higher interest rate or even loan denial. For more on this, check out our article on .

What’s a "Good" Car Loan Interest Rate? Averages and Benchmarks

Now that we understand the factors, let’s address the core question: how much interest should I pay on a car loan? While there’s no single "magic number," we can look at average rates and benchmarks based on credit scores to give you a strong indication.

Average Rates for New Cars (Based on Credit Tiers)

Generally, excellent credit scores command the lowest rates.

- Excellent Credit (780+): You could see rates as low as 3-5%. These are the prime rates, often reserved for the most creditworthy borrowers.

- Good Credit (670-739): Rates typically range from 5-7%. This is still a very competitive rate range, accessible to many consumers.

- Average Credit (600-669): Expect rates in the 8-12% range. Lenders see slightly more risk here, so rates increase.

- Subprime Credit (500-599): Rates can jump significantly, often 13-20% or even higher. This tier carries substantial risk for lenders.

These figures are averages and can fluctuate based on market conditions and specific lenders. Always aim to be in the excellent or good credit tiers for the best outcomes.

Average Rates for Used Cars (Based on Credit Tiers)

Used car loan rates are typically higher than new car rates across all credit tiers, reflecting the increased risk for lenders.

- Excellent Credit (780+): Rates might be in the 5-7% range.

- Good Credit (670-739): Expect rates around 7-10%.

- Average Credit (600-669): Rates often fall between 11-16%.

- Subprime Credit (500-599): You might face rates of 17-25% or even more.

Pro Tip: Don’t just compare to averages; aim for the best for you. Your unique financial situation, the car you choose, and the lender you select will all play a part. Always strive to get pre-approved to know your actual rate before you even visit a dealership.

Calculating Your Car Loan Interest: A Simplified Approach

Understanding how interest is calculated can demystify the process and help you compare loan offers more effectively. While lenders use complex algorithms, you can get a good estimate using a basic formula.

How Car Loan Interest is Typically Calculated

Most car loans use simple interest, meaning interest is calculated only on the principal balance that remains unpaid. Each month, a portion of your payment goes towards interest, and the rest reduces your principal. As your principal balance decreases, the amount of interest you pay each month also decreases.

This is different from compound interest, where interest is calculated on both the principal and previously accumulated interest. For car loans, simple interest is generally the standard.

Using Online Calculators for Accuracy

While you can do manual calculations, using an online car loan calculator is the easiest and most accurate way to estimate your monthly payments and total interest. These tools allow you to input the loan amount, interest rate (APR), and loan term to instantly see the financial breakdown.

I highly recommend using a reputable online calculator from a trusted financial source, like NerdWallet or Experian, before you start shopping. This empowers you with concrete numbers to compare offers.

A Simple Calculation Example

Let’s say you take out a $20,000 loan at 5% APR over 60 months.

- Calculate monthly interest rate: Divide the annual APR by 12 (5% / 12 = 0.004167).

- Estimate monthly payment: While complex, an online calculator would show this is approximately $377.42.

- Total paid: $377.42 * 60 months = $22,645.20.

- Total interest: $22,645.20 – $20,000 = $2,645.20.

This simple example highlights how even a seemingly small interest rate can add a significant amount to your total cost.

Strategies to Secure the Best Car Loan Interest Rate

The good news is that you’re not entirely at the mercy of lenders. There are proactive steps you can take to significantly improve your chances of getting a low interest rate.

Improve Your Credit Score Before Applying

This is perhaps the most impactful strategy. A higher credit score directly translates to a lower interest rate.

- Pay your bills on time: Payment history is the biggest factor in your score.

- Reduce your credit utilization: Keep credit card balances low, ideally below 30% of your credit limit.

- Check your credit report for errors: Dispute any inaccuracies immediately.

- Avoid opening new credit accounts: This can temporarily lower your score.

For a deeper dive into this, consider reading our article on . Taking these steps months before you need a car loan can pay off immensely.

Make a Larger Down Payment

As discussed, a larger down payment reduces the amount you need to borrow, which lowers the lender’s risk. This often results in a more favorable interest rate. It also helps you build equity in your car faster.

Pro tips from us: If you can’t afford a large down payment right away, consider saving for a few extra months. The savings in interest could outweigh the delay.

Shop Around for Lenders and Get Multiple Quotes

Never settle for the first loan offer you receive, especially from the dealership. Always compare offers from at least three different lenders:

- Your bank: They know your financial history.

- Credit unions: Often have competitive rates.

- Online lenders: Can offer quick approvals and good rates.

Getting pre-approved from multiple lenders within a short period (typically 14-45 days, depending on the credit scoring model) will usually count as only one hard inquiry on your credit report, minimizing the impact on your score.

Choose a Shorter Loan Term (If Affordable)

While a shorter term means higher monthly payments, it almost always results in less total interest paid. If your budget allows for a higher monthly payment, opting for a 36- or 48-month loan instead of a 60- or 72-month one can save you hundreds, if not thousands, in interest.

This is a powerful strategy to reduce your overall car ownership costs. Don’t let the allure of a low monthly payment overshadow the total cost of the loan.

Consider a Co-signer (Pros and Cons)

If your credit isn’t stellar, having a co-signer with excellent credit can help you qualify for a better interest rate. A co-signer legally agrees to be responsible for the loan if you default, reducing the lender’s risk.

However, this comes with significant pros and cons. While it can secure you a better rate, it also puts the co-signer’s credit at risk if you fail to make payments. Only consider this option if you are absolutely confident in your ability to repay.

Negotiate with the Dealership (But Know Your Pre-Approval First)

Once you have pre-approval offers from external lenders, you’re in a much stronger negotiating position at the dealership. They may try to beat your pre-approved rate to keep the financing in-house.

Never discuss your desired monthly payment first; focus on the total price of the car and then on the APR. Having a pre-approval in hand gives you leverage and a clear benchmark.

Refinancing Your Car Loan: When It Makes Sense

If you’ve already purchased a car and your credit score has improved, or if interest rates have dropped since you took out your original loan, refinancing could be a smart move. Refinancing replaces your current car loan with a new one, ideally with a lower interest rate and/or a more favorable term.

This can significantly reduce your monthly payments and the total interest you pay over the remaining life of the loan. It’s a strategy worth exploring a year or two into your loan term if your financial situation has improved.

Common Mistakes to Avoid When Taking Out a Car Loan

Even with the best intentions, car buyers often make mistakes that lead to higher interest payments. Being aware of these pitfalls can help you avoid them.

Focusing Only on the Monthly Payment

This is perhaps the most common and costly mistake. Dealerships often emphasize a "low monthly payment" without fully disclosing the extended loan term or the higher total interest paid. A lower monthly payment might be achieved by stretching the loan over 72 or 84 months, which dramatically increases the total cost of the car.

Always ask for the total price of the car, including all interest and fees, before committing to a monthly payment.

Not Getting Pre-Approved

Walking into a dealership without a pre-approval from an independent lender is like going into a negotiation blindfolded. You won’t know what a truly competitive interest rate looks like for your credit profile. This leaves you vulnerable to whatever rate the dealership offers, which may not be the best.

Pro tips from us: Get at least two or three pre-approvals before you start test driving. This gives you a baseline and negotiating power.

Ignoring the Total Cost of the Loan

Beyond just the interest rate, consider the total amount you will pay over the life of the loan. This includes the principal, all interest, and any associated fees. A slightly lower interest rate on a much longer loan term might still result in more total interest paid.

Always ask for the total cost of the loan and compare it across different offers. This holistic view is crucial for financial health.

Falling for Dealer Financing Tricks

Some dealerships might use tactics like "payment packing" (adding unnecessary products like extended warranties or GAP insurance into your loan without fully disclosing them) or manipulating trade-in values to make a deal seem better than it is.

Be vigilant, read all paperwork carefully, and question anything that seems unclear or too good to be true. Remember, the finance manager’s job is to maximize the dealership’s profit.

Extending the Loan Term Unnecessarily

While a longer loan term offers lower monthly payments, it’s almost always more expensive in the long run due to increased interest. If you can comfortably afford a shorter term, choose it. You’ll pay off your car faster and save a significant amount of money.

Common mistakes to avoid are automatically opting for the longest term just for the lowest monthly payment. Assess your budget realistically and prioritize saving on interest.

Based on My Experience: Insider Tips for Car Loan Success

Having worked extensively in consumer finance content, I’ve gathered some insights that can truly make a difference in your car loan journey.

The Power of Preparation

The single most important piece of advice I can offer is to be prepared. This means checking your credit score months in advance, understanding your budget (including insurance and maintenance costs), and researching average interest rates for your credit tier. The more informed you are, the less susceptible you are to pressure tactics.

Preparation is your shield and your sword in the car buying process. It empowers you to make decisions based on facts, not emotions.

Reading the Fine Print is Non-Negotiable

Every single document you sign related to your car loan should be read thoroughly. Don’t assume anything. Pay close attention to the APR, the total loan amount, the loan term, any prepayment penalties, and all fees. If you don’t understand something, ask for clarification.

Common mistakes to avoid are rushing through paperwork at the dealership when you’re tired or excited. Take your time, and don’t be afraid to ask for copies to review later.

Understanding Your Budget Beyond Just the Car Payment

A car loan is just one part of car ownership. Based on my experience, many buyers overlook the full financial picture. Remember to factor in:

- Car insurance: Can vary wildly based on the car, your age, and location.

- Fuel costs: A larger vehicle means more at the pump.

- Maintenance and repairs: Especially important for used cars.

- Registration and taxes: Annual costs that add up.

A low interest rate on a car you can’t afford to maintain or insure is not a good deal. Always consider the total cost of ownership.

Conclusion: Taking Control of Your Car Loan Interest

Determining how much interest should I pay on a car loan is not about finding a universal answer, but about understanding the levers you can pull to secure the most favorable terms for your specific situation. From diligently managing your credit score to strategically shopping for lenders and making informed decisions about loan terms, every step you take contributes to reducing your overall borrowing cost.

The true cost of your vehicle extends far beyond its sticker price, with interest often adding a significant amount to your total outlay. By empowering yourself with knowledge, employing smart strategies, and avoiding common pitfalls, you can navigate the car loan process with confidence. Don’t just accept the first offer; demand the best rate for your financial health. Your wallet will thank you for it.