How Much Is Left On My Car Loan? The Ultimate Guide to Tracking Your Auto Debt

How Much Is Left On My Car Loan? The Ultimate Guide to Tracking Your Auto Debt Carloan.Guidemechanic.com

Understanding the full scope of your financial commitments is a cornerstone of smart money management. For many, a car loan represents one of their most significant debts outside of a mortgage. Whether you’re planning to sell your vehicle, looking to refinance, or simply want to take control of your finances, knowing exactly "How Much Is Left On My Car Loan?" is a critical piece of information.

This isn’t just a simple number; it’s a dynamic figure that impacts your budget, your credit, and your future financial decisions. In this comprehensive guide, we’ll dive deep into various methods for uncovering your remaining auto loan balance, explain the crucial distinction between current balance and payoff amount, and empower you with strategies to manage and even accelerate the repayment of your car debt. Get ready to gain clarity and confidence in your auto loan journey.

How Much Is Left On My Car Loan? The Ultimate Guide to Tracking Your Auto Debt

Unpacking the Basics: What Defines Your Car Loan?

Before we jump into finding your remaining balance, it’s essential to grasp the fundamental components that make up your car loan. A solid understanding here will make tracking your progress much clearer.

A car loan is essentially an installment loan, where you borrow a specific amount of money from a lender to purchase a vehicle. You then agree to repay this amount, plus interest, over a predetermined period through regular monthly payments.

Key Components of Your Car Loan:

- Principal: This is the original amount of money you borrowed to buy the car. Every payment you make chipping away at this principal amount is reducing your actual debt.

- Interest Rate: This is the cost of borrowing money, expressed as a percentage. It determines how much extra you pay back on top of the principal. A lower interest rate means less money spent over the life of the loan.

- Loan Term: This refers to the duration over which you’ve agreed to repay the loan, typically measured in months (e.g., 36, 48, 60, 72, or even 84 months). A longer term usually means lower monthly payments but more interest paid overall.

- Monthly Payment: This is the fixed amount you pay to your lender each month. It’s calculated to cover a portion of both the principal and the interest, ensuring the loan is fully repaid by the end of the term.

Based on my experience, many people overlook these fundamental elements once they’ve signed the papers. However, truly understanding how each component interacts is the first step toward effectively managing your car loan and ultimately knowing how much is left. This foundational knowledge empowers you to make informed decisions down the road.

Why Knowing Your Remaining Balance Is Non-Negotiable

Beyond mere curiosity, there are several compelling reasons why staying informed about your remaining car loan balance is crucial for your financial well-being. This isn’t just about a number; it’s about financial foresight.

Firstly, it’s vital for accurate budgeting and financial planning. Knowing your precise debt allows you to allocate funds effectively, avoid unexpected shortfalls, and plan for other financial goals. You can’t properly manage your money if you don’t know your liabilities.

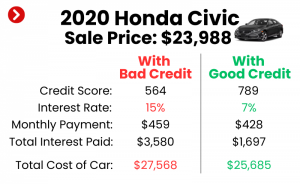

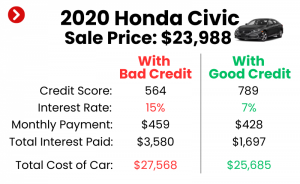

Secondly, it opens doors to potential refinancing opportunities. If interest rates have dropped or your credit score has improved, knowing your balance is the first step in determining if refinancing could save you money. A lower interest rate can significantly reduce your total cost of borrowing.

Thirdly, for those considering selling their car, the remaining loan balance dictates whether you have positive equity (the car is worth more than you owe) or negative equity (you owe more than it’s worth). This is a critical factor in setting a fair selling price and avoiding financial loss.

Finally, it provides the clarity needed to make informed strategic decisions about your loan. You might decide to make extra payments, pay it off early, or simply stick to the payment schedule. All these decisions hinge on having an up-to-date figure.

Pinpointing the Answer: Methods to Find Your Remaining Car Loan Balance

Finding out how much is left on your car loan doesn’t have to be a scavenger hunt. There are several reliable methods you can use, ranging from the immediate to the slightly more involved. Each method offers a different level of detail and convenience.

Let’s explore the most effective ways to get that crucial number.

Method 1: Accessing Your Online Account (The Easiest Route)

In our digital age, your lender’s online portal or mobile app is typically the quickest and most convenient way to find your car loan balance. Most financial institutions offer robust online platforms designed for customer self-service.

How to Access Your Information:

- Log In: Navigate to your lender’s official website or open their dedicated mobile application. You’ll need your username and password, which you should have set up when you initiated the loan.

- Locate Loan Details: Once logged in, look for sections like "My Loans," "Account Summary," "Loan Details," or "Statements." Your current principal balance is usually prominently displayed on the main dashboard or within the loan-specific section.

- Look for Payoff Information: Many online portals will also provide a "payoff quote" or a "current payoff amount" directly. This is a crucial distinction we’ll elaborate on shortly, but it’s often available with a click or two.

Pro Tip from Us: Set up email or text alerts within your online account for payment reminders, statement availability, and even low balance notifications. This keeps you continually connected to your loan status without active effort. Regularly checking your online account helps you stay on top of your debt and spot any discrepancies quickly.

Method 2: Contacting Your Lender Directly (For Specific Details)

While online access is great for a quick glance, sometimes you need more detailed or personalized information. A direct conversation with your lender can provide specific answers to nuanced questions.

How to Connect with Your Lender:

- Phone Call: Find your lender’s customer service number on your monthly statement or their website. Be prepared to provide your account number and verify your identity.

- What to Ask: Clearly state you want to know "How much is left on my car loan?" but also specifically ask for the payoff amount for a specific date. Inquire about the "per diem interest," which is the amount of interest that accrues daily. This helps you calculate an exact payoff for any given day.

- Email or Secure Message: Many online portals offer a secure messaging system. This method provides a written record of your inquiry and the lender’s response, which can be beneficial for documentation purposes.

- Visiting a Branch: If your lender has physical branches, you can visit in person. This offers the advantage of face-to-face interaction and the ability to ask follow-up questions immediately.

Common Mistake to Avoid: A frequent error is simply asking for your "current balance." While useful, this number doesn’t account for interest that accrues between your last payment and the exact day you wish to pay off the loan. Always ask for the payoff amount for a specific future date to get the most accurate figure for full repayment.

Method 3: Reviewing Your Monthly Statements (A Historical Perspective)

Your monthly loan statements, whether paper or electronic, are a treasure trove of information about your car loan. They provide a detailed breakdown of your account activity.

What to Look For:

- Current Principal Balance: This figure is typically listed prominently on your statement, showing how much principal remains after your last payment.

- Payment Breakdown: Statements usually show how much of your last payment went toward principal and how much went toward interest. This helps you understand the amortization schedule.

- Interest Accrued: Some statements detail the interest accrued since your last statement or the interest applied with your last payment.

- Due Date: Keep an eye on this to ensure timely payments and avoid late fees.

From years of analyzing financial statements, I’ve seen how valuable these documents are for understanding the trajectory of a loan. They provide a clear historical record and can help you identify any potential errors or unexpected charges. Make it a habit to review them thoroughly each month.

Method 4: Utilizing a Loan Amortization Schedule (DIY Tracking)

An amortization schedule is a table detailing each payment made on a loan, showing how much of each payment is applied to interest and principal, and the remaining loan balance. While your lender might provide one, you can also create your own.

How it Works:

- What it Is: It’s a comprehensive breakdown of every single payment you will make over the life of your loan. It shows how the principal is gradually paid down and how interest charges diminish over time.

- How to Create One: You can use a spreadsheet program (like Excel or Google Sheets) or numerous free online amortization calculators. You’ll need your original loan amount, interest rate, and loan term.

- Benefits: Creating your own schedule allows you to visualize the impact of extra payments. You can adjust the numbers to see how paying an additional $50 each month changes your payoff date and total interest paid.

Pro Tip: An amortization schedule is a fantastic tool for visualizing how interest is front-loaded in many loans. It helps you see how making extra principal payments early in the loan term can have a dramatic effect on your total interest paid and accelerate your debt freedom. However, remember it won’t account for late fees or other charges, so it’s an estimate unless updated regularly.

Method 5: Checking Your Credit Report (An Indirect Indicator)

Your credit report is a record of your financial history, and it includes details about your outstanding loans, including your car loan. While not the most immediate or precise method for an exact payoff quote, it provides a general overview.

How it Reflects Your Loan:

- Loan Status: Your credit report will list your car loan, the original loan amount, the lender, and your current balance as reported by the lender.

- Reporting Lag: Be aware that credit bureaus might not have the absolute most up-to-date balance. Lenders typically report to credit bureaus once a month, so the balance shown might be a few weeks behind your actual current balance.

- Accuracy Check: Regularly checking your credit report (which you can do for free annually) is a good practice not only for monitoring your loan but also for ensuring accuracy and protecting against identity theft. If you spot a discrepancy in your car loan balance, you can dispute it with the credit bureau.

External Link: You can obtain a free copy of your credit report annually from each of the three major credit bureaus (Experian, Equifax, and TransUnion) at AnnualCreditReport.com. This is a trusted and government-authorized source.

The Crucial Distinction: Current Balance vs. Payoff Amount

This is perhaps the most critical concept to grasp when asking, "How much is left on my car loan?" Many people confuse their current balance with their payoff amount, leading to potential miscalculations and frustration.

The current balance is simply the principal amount remaining on your loan as of a specific date, usually right after your last payment has been processed. It’s the raw amount of money you still owe on the principal, not including any interest that has accrued since your last payment or any potential fees.

The payoff amount, on the other hand, is the total amount you need to pay today (or on a specified future date) to completely satisfy and close out your loan. This figure includes:

- The remaining principal balance.

- Any interest that has accrued since your last payment up to the payoff date.

- Any outstanding fees (e.g., late fees, administrative charges).

- Sometimes, a per diem interest rate, which is the daily interest charge.

Why the Difference? Interest on loans typically accrues daily. So, even if you check your online account and see a principal balance, by the time you actually send in a payment a few days later, additional interest will have accumulated. The payoff amount accounts for this daily accrual.

Based on my expertise in auto finance, this is one of the most misunderstood aspects of loan management. Failing to ask for a payoff quote can lead to sending an insufficient amount, leaving a small residual balance, and preventing your loan from being fully closed. Always request a payoff quote that is valid for a specific period (e.g., 7-10 days) to ensure accuracy when making a full payment.

Factors That Constantly Shift Your Remaining Loan Balance

Your car loan balance isn’t a static number; it’s constantly in flux due to several interacting factors. Understanding these dynamics helps you appreciate how your balance changes over time.

Firstly, regular payments are the primary driver. Each monthly payment you make reduces both your principal and the interest due. Early in the loan term, a larger portion of your payment goes towards interest, gradually shifting to more principal reduction as the loan matures.

Secondly, extra payments or prepayments can significantly accelerate the reduction of your remaining balance. When you pay more than your minimum, that extra money is typically applied directly to the principal, unless otherwise specified. This not only reduces the principal faster but also decreases the total interest you’ll pay over the loan’s life.

Thirdly, your interest rate plays a critical role in how quickly your principal balance decreases relative to your payments. A higher interest rate means a larger portion of your payment covers interest, leaving less to chip away at the principal. Conversely, a lower rate helps you reduce the principal faster.

Fourthly, the loan term also dictates the pace. A shorter loan term means higher monthly payments, but you pay off the principal much faster and incur less overall interest. A longer term stretches out payments, making them smaller but ultimately slowing down principal reduction and increasing total interest.

Lastly, fees and penalties can also increase your outstanding balance. Late payment fees, returned payment fees, or other administrative charges can be added to your loan, effectively increasing how much you owe.

– Understanding these factors empowers you to make strategic decisions about how you manage your car loan.

Why Proactive Loan Tracking Empowers Your Financial Future

Knowing precisely "how much is left on my car loan" isn’t just about satisfying curiosity; it’s about gaining a powerful lever in your financial planning. This knowledge equips you to make smarter, more strategic decisions.

For budgeting and financial planning, an accurate loan balance allows you to see the true picture of your liabilities. You can then confidently allocate funds, plan for future expenses, or assess your capacity for other investments without underestimating your car debt. It’s the foundation of a realistic financial outlook.

When considering refinancing opportunities, your current balance is the first piece of information a new lender will need. It helps determine your loan-to-value ratio, which is crucial for securing a better interest rate or a more favorable term. Knowing this figure empowers you to shop around effectively and potentially save thousands.

If you’re contemplating selling your car, understanding your remaining balance is absolutely critical. It dictates whether you have positive equity (you can sell the car for more than you owe) or negative equity (you owe more than the car is worth). This directly impacts your selling strategy and avoids unexpected financial shortfalls.

Ultimately, it enables you to make informed decisions about your debt. Should you prioritize paying off your car loan early? Is it wise to consolidate debt? Or are you comfortable sticking to your current payment schedule? These questions can only be answered accurately when you have a clear understanding of your outstanding balance.

– Armed with this knowledge, you transform from a passive borrower into an active manager of your debt.

Strategies to Accelerate Your Car Loan Payoff (and Reduce Your Remaining Balance)

If you’re looking to reduce how much is left on your car loan faster and save money on interest, there are several effective strategies you can employ. These methods are designed to chip away at your principal more aggressively.

One of the most straightforward methods is making extra principal payments. Whenever you have extra cash – from a bonus, a tax refund, or just finding some wiggle room in your budget – make an additional payment specifically designated for the principal. Always confirm with your lender that these extra funds will be applied directly to the principal, not just advanced to the next payment.

Another popular strategy is bi-weekly payments. Instead of making one full payment monthly, you make half of your payment every two weeks. Because there are 52 weeks in a year, this results in 26 half-payments, which equates to 13 full monthly payments annually instead of 12. That "extra" payment goes entirely towards reducing your principal.

Consider rounding up your monthly payments. If your payment is $347, round it up to $350 or even $375. While seemingly small, these consistent extra amounts add up over the life of the loan and can shave months off your term and significant interest costs.

Refinancing to a shorter term or lower rate can also be a game-changer. If your financial situation has improved, you might qualify for a lower interest rate, which means more of each payment goes to principal. Alternatively, refinancing to a shorter term (if you can afford the higher monthly payments) will drastically accelerate your payoff.

Finally, strategically using windfalls like tax refunds, work bonuses, or unexpected inheritances to make a lump-sum payment directly to your principal can have a huge impact. This single action can immediately reduce your remaining balance and save you a substantial amount of interest over the remaining term.

Pro Tip from Us: Always double-check with your lender that any extra payments you make are applied directly to the principal balance. Some lenders, by default, might apply extra funds to future interest or even prepay your next scheduled payment, which doesn’t achieve the same debt-reduction benefits. Clear communication is key.

Common Mistakes to Avoid When Tracking Your Car Loan

While finding out "how much is left on my car loan" might seem straightforward, there are several common pitfalls that borrowers often encounter. Being aware of these can save you time, money, and frustration.

A primary mistake is confusing the current balance with the payoff amount. As discussed, these are two different figures. Relying solely on your current balance for a full repayment can lead to an insufficient payment, leaving a small amount of interest still owed and preventing your loan from being officially closed. Always request a specific payoff quote.

Another oversight is ignoring your monthly statements. These documents contain vital information, including your principal balance, payment breakdown, and any fees. Neglecting to review them means you could miss errors, unauthorized charges, or simply lose track of your loan’s progress.

Not checking for errors on your statements or credit report is also a common pitfall. Lenders and credit bureaus are not infallible. Mistakes can happen, leading to incorrect balances or payment histories. Regularly reviewing your records allows you to catch and rectify these errors promptly.

Finally, assuming the interest rate will stay the same (if you have a variable-rate loan) can lead to surprises. While most car loans are fixed-rate, some might be variable. If yours is, changes in the prime rate could alter your interest charges and, consequently, the proportion of your payment going to principal. Always confirm your loan type.

In my professional experience, these oversights can lead to significant financial headaches. A proactive approach to monitoring your car loan will ensure you stay on track and avoid unexpected issues.

Conclusion: Take the Driver’s Seat of Your Car Loan

Knowing "How Much Is Left On My Car Loan?" is more than just a piece of data; it’s a fundamental aspect of effective financial management. By understanding your loan’s components, actively tracking your balance through various methods, and distinguishing between current and payoff amounts, you gain invaluable control over your auto debt.

We’ve explored how simple online access, direct communication with your lender, regular statement reviews, and even personal amortization schedules can provide the clarity you need. We’ve also highlighted the critical factors that influence your balance and powerful strategies to accelerate your path to debt freedom.

Don’t let your car loan be a mystery. Take the initiative to regularly check your balance, understand its nuances, and apply strategies to pay it down efficiently. This proactive approach not only frees up your financial resources sooner but also provides immense peace of mind. By staying informed and engaged, you put yourself firmly in the driver’s seat of your financial future.