How To Add Someone To A Car Loan: Your Ultimate Guide to Navigating Joint Car Financing

How To Add Someone To A Car Loan: Your Ultimate Guide to Navigating Joint Car Financing Carloan.Guidemechanic.com

Embarking on the journey of car ownership is exciting, but the financing aspect can often feel like a complex maze. Sometimes, circumstances arise where adding another individual to your existing car loan becomes a consideration. Perhaps you want to improve your chances of approval, secure a better interest rate, share financial responsibility, or even help a loved one establish their credit. Whatever the motivation, understanding "how to add someone to a car loan" is crucial, as it’s a decision with significant financial and legal implications for all parties involved.

This comprehensive guide will demystify the process, explain the nuances, and provide you with expert insights to make an informed decision. We’ll dive deep into the differences between co-borrowers and co-signers, walk you through the most common methods, highlight essential considerations, and even explore alternatives. Our goal is to equip you with all the knowledge needed to navigate this important financial step confidently.

How To Add Someone To A Car Loan: Your Ultimate Guide to Navigating Joint Car Financing

Understanding the "Why": Reasons to Consider Adding Someone to Your Car Loan

Before we delve into the "how," let’s explore the common motivations behind adding another person to a car loan. Understanding these reasons will help you determine if this path aligns with your specific financial goals and needs.

Improving Approval Chances or Securing Better Rates

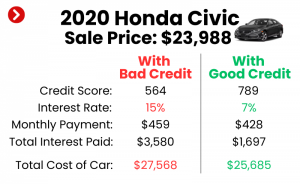

One of the primary reasons individuals consider adding someone to a car loan is to strengthen their application. If your credit score is less than ideal, or your income-to-debt ratio is a concern for lenders, a co-borrower or co-signer with a strong financial profile can significantly boost your eligibility. Lenders view a joint application with a higher combined income and better credit history as less risky, potentially leading to approval or even a lower interest rate. A lower interest rate translates directly into saving hundreds, if not thousands, of dollars over the life of the loan.

Sharing Financial Responsibility

For many couples, families, or roommates who share a vehicle, adding both names to the loan simply makes practical sense. It formally acknowledges the shared financial commitment to the car. This arrangement ensures that both parties are equally responsible for making the monthly payments, fostering a sense of joint ownership and accountability. It can simplify budgeting and ensure that the burden doesn’t fall squarely on one person’s shoulders.

Building Credit for Another Person

Adding a person to a car loan, particularly as a co-borrower, can be an excellent way to help them build or rebuild their credit history. By consistently making on-time payments, both individuals listed on the loan will see positive reporting to credit bureaus. This can be invaluable for someone just starting their financial journey or for an individual looking to improve a less-than-stellar credit score. It’s a significant financial commitment, but one that can yield substantial benefits for future borrowing.

Adapting to Life Changes

Life is full of changes, and your financial arrangements often need to adapt. A marriage, for instance, might lead a couple to consolidate their finances and share ownership of a vehicle. Similarly, if a partner moves in and begins contributing to household expenses, formalizing their role in car payments through the loan can be a logical step. These life transitions often necessitate a reevaluation of financial responsibilities and how assets are owned and financed.

Co-Borrower vs. Co-Signer: What’s the Critical Difference?

Before proceeding, it’s absolutely vital to understand the distinction between a co-borrower and a co-signer. While both roles involve taking on responsibility for the loan, their legal and ownership implications differ significantly. Common mistakes often stem from not fully grasping these two distinct roles.

The Co-Borrower: Joint Ownership and Joint Responsibility

A co-borrower, also known as a joint applicant, is someone who applies for the car loan alongside the primary borrower. Both individuals are considered equal owners of the vehicle and are equally responsible for the debt. Their names will appear on the loan agreement and, crucially, on the vehicle’s title. This means they both have a legal claim to the car.

From a lender’s perspective, both co-borrowers’ income and credit history are assessed during the application process. If one co-borrower defaults on payments, the other is 100% legally obligated to cover the entire amount. Their credit reports will reflect the loan and its payment history, impacting both individuals equally.

The Co-Signer: Responsibility Without Ownership

A co-signer, on the other hand, agrees to be legally responsible for the loan if the primary borrower fails to make payments. The key difference here is that a co-signer typically does not have an ownership interest in the vehicle. Their name will appear on the loan agreement, but generally not on the car’s title. They are essentially a guarantor, providing their creditworthiness as collateral.

While a co-signer doesn’t own the car, their credit score is just as affected by the loan’s payment history as the primary borrower’s. A missed payment or default will negatively impact both credit reports. Pro tips from us: Becoming a co-signer is a serious commitment. You’re taking on significant financial risk without gaining any ownership rights to the asset. It’s a purely supportive role with high stakes.

The Process: How to Add Someone to an Existing Car Loan

Here’s a crucial piece of information: you generally cannot simply "add" someone to an existing car loan in the same way you might add someone to a bank account. Most lenders do not offer a simple amendment to an active loan agreement for this purpose. The most common and often only way to formally add another person to a car loan is through a process called refinancing.

Option 1: Refinancing – The Most Common Path

Refinancing involves taking out a brand new loan to pay off your current one. When you refinance, you have the opportunity to include a new co-borrower or co-signer on the new loan application. This is the primary method used to achieve your goal.

Step 1: Assess Your Current Loan and Credit Scores

Before you do anything, gather all the details about your existing car loan: the outstanding balance, current interest rate, and remaining term. Next, both you and the person you wish to add should check your credit scores and review your credit reports. Understanding your combined credit profile is essential, as it will dictate the terms of any new loan you might qualify for. This step allows you to identify any potential red flags or areas for improvement before applying.

Step 2: Gather Required Documents

Lenders will require a range of documents from both applicants. This typically includes:

- Proof of Identity: Valid driver’s licenses, Social Security numbers.

- Proof of Income: Pay stubs, tax returns, bank statements.

- Proof of Residence: Utility bills, lease agreements.

- Vehicle Information: Current registration, title (or lienholder information), VIN (Vehicle Identification Number), mileage, make, and model.

- Current Loan Details: Account number, payoff amount.

Having these documents ready will streamline the application process.

Step 3: Apply for a New Joint Loan

With all your information in hand, it’s time to shop around for a new loan. Contact various lenders – banks, credit unions, and online auto loan providers. Clearly state that you are applying for a joint refinancing loan with a co-borrower or co-signer. Provide all the requested financial information for both individuals. Each application will involve a hard credit inquiry, which can temporarily ding your credit score, so try to apply to a few lenders within a short timeframe (usually 14-45 days) to minimize the impact.

Step 4: Loan Approval and Signing

If approved, the lender will present you with a new loan offer detailing the interest rate, term, and monthly payments. Carefully review all terms and conditions with the person you are adding. Ensure both parties fully understand their obligations and the repayment schedule. Once you both agree, you will sign the new loan agreement. Based on my experience, this is the point where many people rush. Take your time, read the fine print, and ask questions.

Step 5: Pay Off the Old Loan

Upon signing the new loan, the funds will be used to pay off your original car loan. The old loan will be closed, and the lienholder will be removed from the title. A new title will then be issued, typically listing both names if you’ve added a co-borrower. This officially transfers the debt and ownership (if applicable) to the new joint arrangement.

- Common Mistakes to Avoid: Not comparing multiple offers. Settling for the first approval you receive could mean missing out on a significantly better interest rate or more favorable terms. Always shop around. Another common mistake is failing to verify that the old loan has been fully paid off and the lien removed.

Option 2: Loan Modification (Rare and Lender-Specific)

While refinancing is the standard route, some lenders might offer a loan modification under very specific circumstances. This is exceedingly rare for adding a new party to a car loan. Loan modifications are typically reserved for borrowers experiencing financial hardship and looking to adjust payment terms, not to introduce a new financially responsible party. You would need to directly contact your current lender to inquire about this, but be prepared for them to direct you towards refinancing.

Key Considerations Before Adding Someone to Your Car Loan

Adding someone to a car loan is a major financial decision with far-reaching consequences. It’s not something to be taken lightly. Pro tips from us: Always consider the "what ifs" before committing.

Financial Implications for Both Parties

Impact on Credit Scores (Positive and Negative)

For both the primary borrower and the added individual, the loan will appear on their credit reports. Consistent, on-time payments will positively impact both scores, building a stronger credit history. However, even a single late payment or default will negatively affect both credit scores, regardless of who was supposed to make the payment. This shared credit destiny requires a high level of trust and financial discipline.

Joint Responsibility for Payments

When someone is added to a car loan, they become equally and fully responsible for the entire debt. This means if one person cannot or will not make their share of the payments, the other person is legally obligated to cover the full amount. The lender doesn’t care who pays; they just want the payment made. This shared liability is why strong communication and trust are paramount.

Debt-to-Income Ratio

Adding a new loan to someone’s financial profile will increase their overall debt. This can impact their debt-to-income (DTI) ratio, which lenders use to assess their ability to take on additional debt. A higher DTI could make it more challenging for either individual to qualify for other loans (e.g., a mortgage or personal loan) in the future.

Legal and Ownership Implications

Vehicle Title & Registration

If you add someone as a co-borrower through refinancing, their name will typically be added to the vehicle’s title. This signifies joint ownership. In some states, this might be listed as "and" (requiring both signatures for sale) or "or" (allowing either person to sell). Understand your state’s specific titling laws. If they are a co-signer, their name usually won’t be on the title, meaning they have no ownership rights, only liability.

Potential for Disputes

Based on my experience, this is often overlooked in the excitement of getting the loan. What happens if your relationship sours? If a couple breaks up, or friends have a falling out, who keeps the car? Who is responsible for payments? Without clear agreements, these situations can lead to bitter legal disputes, damaged credit, and significant financial loss. This is why clear communication and even a written agreement are vital.

Relationship Implications

Trust and Communication

Adding someone to a car loan hinges entirely on trust. You are entrusting your financial future to another person, and they are doing the same for you. Open, honest, and ongoing communication about finances, payment schedules, and any potential difficulties is non-negotiable. Without it, the arrangement is highly vulnerable to stress and conflict.

"What If" Scenarios

It’s uncomfortable, but essential, to discuss potential worst-case scenarios upfront. What if one person loses their job? What if the relationship ends? What if one person wants to sell the car and the other doesn’t? Having these difficult conversations beforehand, and ideally documenting the agreed-upon resolutions, can save immense heartache and financial ruin down the line.

Required Documents and Eligibility

To add someone to a car loan via refinancing, both individuals will need to meet the lender’s eligibility criteria and provide a range of documentation.

- Identification: Valid government-issued photo ID (driver’s license), Social Security Number (SSN) or Individual Taxpayer Identification Number (ITIN).

- Proof of Income: Recent pay stubs (typically 2-3 months), W-2s, tax returns (if self-employed), bank statements. Lenders want to see stable and sufficient income to cover the new loan payments.

- Credit History Information: While you’ll get your credit reports, lenders will pull their own. Good credit scores from both applicants are usually key to securing favorable rates.

- Vehicle Information: The car’s VIN, make, model, year, and current mileage. Lenders will assess the car’s value to ensure it aligns with the loan amount.

- Current Loan Details: The exact payoff amount for your existing loan, account number, and your current lender’s contact information.

Eligibility typically requires both parties to be 18 years or older, have a valid driver’s license, and meet the lender’s minimum credit score and income requirements.

Alternatives to Adding Someone to Your Loan

Sometimes, adding someone to a car loan might not be the best solution or even possible. It’s always wise to explore alternatives.

For the Primary Borrower (If you wanted to add someone to improve your own chances):

- Improving Your Own Credit: Focus on paying down existing debts, making all payments on time, and disputing any errors on your credit report. Over time, a stronger credit score will allow you to qualify for better rates independently.

- Exploring Different Lenders: Not all lenders have the same criteria. Credit unions, for example, often have more flexible lending standards than traditional banks and may offer competitive rates to members. Online lenders also provide a wide array of options.

- Consider a Smaller Loan Amount or Less Expensive Car: If your primary goal was to get approved, perhaps reconsidering the vehicle’s price point could make an independent loan more feasible.

For the Person Needing Credit Help (If you wanted to add them to build their credit):

- Becoming an Authorized User on a Credit Card: This can be a less risky way to help someone build credit. As an authorized user, they get a card in their name linked to your account. Your good payment history can then reflect positively on their credit report. Crucially, they are not legally responsible for the debt, though you should still have clear agreements on spending.

- Secured Loans or Credit Builder Loans: These are designed specifically to help individuals build credit. A secured loan is backed by collateral (like a savings account), making it less risky for lenders. Credit builder loans typically involve a small loan that is held in a savings account while you make payments, which are then reported to credit bureaus.

- Building Credit Independently: Encourage the individual to get a secured credit card or a very small starter credit card. By making small purchases and paying them off in full and on time each month, they can gradually build their own credit history without the entanglement of a major car loan.

Pro Tips for a Smooth Process

Navigating the complexities of joint car financing requires diligence and foresight. Here are some expert recommendations to ensure a smoother experience:

- Open Communication is Key: This cannot be stressed enough. Discuss expectations, financial responsibilities, and "what if" scenarios thoroughly before you even apply. Keep lines of communication open throughout the loan’s term.

- Review All Terms and Conditions Carefully: Don’t just skim the paperwork. Understand the interest rate, loan term, payment schedule, penalties for late payments, and any other clauses. Ensure both parties are fully aware of what they’re agreeing to.

- Consider a Written Agreement (Even for Family): While it might feel awkward, a simple written agreement outlining who is responsible for what payments, who gets the car if the relationship ends, and how major repairs will be handled can prevent future disputes. This is particularly vital for co-signers who have liability without ownership.

- Shop Around for the Best Refinancing Rates: Don’t just go with your current lender or the first offer you receive. Different lenders have different rates and terms. Use online comparison tools and get quotes from at least three to five lenders to ensure you’re getting the most competitive deal.

- Factor in All Costs: Remember that refinancing might come with fees, such as title transfer fees or administrative charges. Factor these into your overall cost analysis to ensure the new loan is truly beneficial.

- Understand Your State’s Laws: Vehicle titling and ownership laws vary by state. Research how joint ownership is handled in your specific location, especially concerning selling the vehicle or removing a name from the title later.

For more in-depth information on improving your financial health before applying for loans, explore our comprehensive guide on and learn about different . You might also find valuable insights on consumer finance at trusted external resources like the Consumer Financial Protection Bureau (CFPB) website (e.g., ).

Conclusion

Adding someone to a car loan is a significant financial maneuver that, when executed thoughtfully, can provide numerous benefits – from improved approval odds and better rates to shared responsibility and credit building. However, it’s a decision that demands meticulous planning, open communication, and a thorough understanding of the financial and legal implications for all parties involved.

By understanding the difference between a co-borrower and a co-signer, recognizing that refinancing is the primary pathway, and carefully considering all the "what ifs," you can navigate this process with confidence. Always prioritize clear communication, review every detail, and explore all alternatives to ensure that this financial step strengthens, rather than strains, your relationships and financial well-being. Make an informed decision that drives you towards a more secure financial future.