How to Build Credit with a Car Loan: Your Ultimate Guide to a Strong Financial Future

How to Build Credit with a Car Loan: Your Ultimate Guide to a Strong Financial Future Carloan.Guidemechanic.com

Building a solid credit history can feel like a classic "chicken or the egg" dilemma. You need credit to get credit, but how do you get started when you have none, or very little? It’s a common challenge faced by young adults, newcomers to a country, or anyone who hasn’t actively managed credit before. But what if we told you that a significant purchase, like a car, could be one of the most effective tools to unlock your financial potential?

Based on my extensive experience in personal finance and credit management, an auto loan, when handled correctly, offers a powerful pathway to establishing and improving your credit score. This isn’t just about getting from point A to point B; it’s about strategically leveraging a necessary expense to build a robust financial foundation.

How to Build Credit with a Car Loan: Your Ultimate Guide to a Strong Financial Future

In this comprehensive guide, we’ll dive deep into how a car loan impacts your credit, the strategic steps to secure one, and how to maximize its credit-building potential. Our ultimate goal is to equip you with the knowledge to make informed decisions, avoid common pitfalls, and set yourself on the road to a stronger financial future.

The Credit Conundrum: Why Building Credit Matters

Before we explore the specifics of car loans, let’s understand why credit is so crucial. Your credit score is essentially a numerical representation of your creditworthiness, a three-digit report card that lenders, landlords, and even some employers use to assess your financial reliability. A good credit score opens doors.

It means you’re more likely to be approved for loans, credit cards, mortgages, and even apartment rentals. Furthermore, a strong credit score often translates into lower interest rates, saving you thousands of dollars over the lifetime of various loans. Conversely, a poor or non-existent credit history can make life significantly more expensive and limit your options.

Many individuals find themselves in a challenging situation: they need a loan to build credit, but lenders are hesitant to approve loans without an existing credit history. This is where a car loan can serve as an excellent entry point into the world of credit. It’s often more accessible than a mortgage and provides a tangible asset as collateral, reducing the risk for lenders.

How a Car Loan Impacts Your Credit Score: The Mechanics Explained

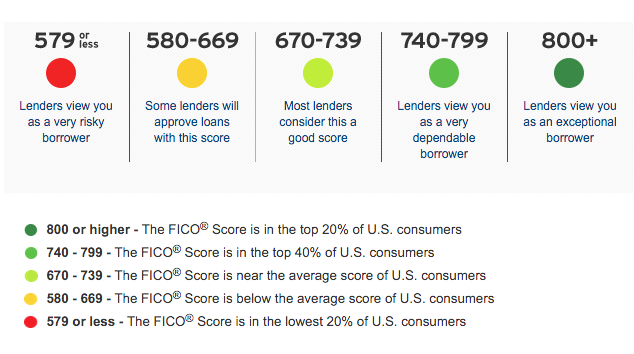

Understanding how your credit score is calculated is key to leveraging a car loan effectively. Most credit scores, like the widely used FICO score, are composed of several key factors, each weighted differently. A car loan, as an installment loan, interacts with all these components in unique ways.

Payment History (35% of Your FICO Score)

This is, without a doubt, the single most critical factor in your credit score. It reflects whether you pay your bills on time. When you take out a car loan, you commit to making regular, fixed payments over a set period.

Every single on-time payment you make is a positive mark on your credit report. It demonstrates to lenders that you are reliable and responsible. Conversely, even one late payment can have a significant negative impact, potentially dropping your score by several points and staying on your report for up to seven years. Based on my experience, consistency here is paramount; perfect payment history is the bedrock of excellent credit.

Amounts Owed / Credit Utilization (30% of Your FICO Score)

This factor looks at how much credit you’re currently using compared to your total available credit. While this is primarily focused on revolving credit (like credit cards), an installment loan like a car loan also plays a role. With a car loan, the initial loan amount is high, but as you make payments, the amount owed decreases.

This steady reduction of your principal balance shows responsible debt management. Unlike credit cards where high utilization can signal financial distress, a car loan’s balance naturally diminishes over time, reflecting positively on your debt management capabilities. It shows you’re systematically paying down a significant debt.

Length of Credit History (15% of Your FICO Score)

This component considers how long your credit accounts have been open and how long it’s been since you used certain accounts. A car loan, especially one with a typical term of 3 to 6 years, provides a long-standing account that consistently reports to credit bureaus.

The longer your oldest accounts are open and in good standing, the better this looks on your credit report. This extended history demonstrates sustained financial responsibility over time. Pro tips from us: don’t close your oldest accounts, even if they’re paid off, unless absolutely necessary, as it can shorten your average credit age.

New Credit (10% of Your FICO Score)

This factor examines how many new credit accounts you’ve recently opened and the number of hard inquiries on your credit report. When you apply for a car loan, the lender performs a "hard inquiry" to check your creditworthiness.

While a single hard inquiry can temporarily dip your score by a few points, its impact is usually minor and fades over time (typically within a year). The key is to apply for credit strategically and not open too many new accounts in a short period. For car loans, FICO scores often treat multiple inquiries for the same type of loan within a 14-45 day window as a single inquiry, recognizing that consumers shop for the best rates.

Credit Mix (10% of Your FICO Score)

This factor assesses the variety of credit accounts you have. Lenders like to see that you can responsibly manage different types of credit, such as revolving credit (credit cards) and installment credit (car loans, mortgages, student loans).

A car loan introduces an installment loan into your credit profile, diversifying your credit mix. This demonstrates your ability to handle different financial commitments, which can be a positive signal to future lenders. It shows a well-rounded approach to borrowing.

Strategic Steps to Get a Car Loan for Credit Building

Securing a car loan, especially when your credit is thin or non-existent, requires a strategic approach. It’s not just about walking into a dealership and picking a car; it’s about preparing yourself financially to increase your chances of approval and secure favorable terms.

Step 1: Understand Your Current Credit Situation

Before you even think about looking at cars, you need to know where you stand. Access your free credit reports from all three major bureaus—Experian, Equifax, and TransUnion—at AnnualCreditReport.com. This is your legal right once every 12 months from each bureau.

Review these reports meticulously for any errors or discrepancies. Incorrect information can unfairly drag down your score. If you find errors, dispute them immediately with the credit bureau. Understanding your current standing, even if it’s "no credit," helps you set realistic expectations and prepare for the application process.

Step 2: Save for a Down Payment

Making a significant down payment is one of the most powerful steps you can take. It reduces the total amount you need to borrow, which in turn lowers your monthly payments and the total interest you’ll pay over the life of the loan.

More importantly, a substantial down payment signals to lenders that you are a serious and responsible borrower. It reduces their risk, making them more likely to approve your loan, even with limited credit history. Common mistakes to avoid are not saving enough, or using your entire savings for the down payment without considering other immediate financial needs. Aim for at least 10-20% of the car’s purchase price if possible.

Step 3: Set a Realistic Budget

Beyond the car’s purchase price and monthly loan payment, owning a car involves numerous other expenses. These include insurance, fuel, maintenance, repairs, and registration fees. These costs can quickly add up and strain your budget if not accounted for.

Pro tips from us: create a detailed monthly budget that includes all potential car-related expenses. Don’t overextend yourself on the car loan itself, as struggling to make payments will negate any credit-building benefits. Ensure you can comfortably afford the total cost of ownership without stress.

Step 4: Explore Loan Options

Not all car loans are created equal, and where you get your loan can significantly impact your terms and approval chances.

- Dealership Financing: Convenient, but not always the best rates, especially for those with thin credit. They may offer specific programs for first-time buyers.

- Banks and Credit Unions: Often offer competitive rates and more personalized service. It’s wise to get pre-approved from a bank or credit union before visiting a dealership; this gives you negotiating power.

- Co-signer Option: If your credit is very limited, a co-signer with good credit can significantly improve your chances of approval and secure better terms. However, common mistakes include not understanding that the co-signer is equally responsible for the debt. If you miss payments, it impacts their credit too. This option requires immense trust and clear communication.

- Subprime Auto Loans: These are loans for individuals with poor or limited credit. While they come with higher interest rates, they can be a stepping stone. The key is to ensure you can afford the payments and plan to refinance once your credit improves.

Step 5: Apply Strategically

Once you’ve done your research and prepared, it’s time to apply. Remember the "new credit" factor we discussed? To minimize the impact of hard inquiries, aim to submit all your loan applications within a concentrated period, typically 14 to 45 days.

FICO’s scoring model often treats multiple inquiries for the same type of loan within this window as a single inquiry, recognizing that you’re shopping for the best rate, not seeking multiple lines of credit. Be prepared to provide necessary documentation, such as proof of income, residency, and identification.

Maximizing Your Car Loan’s Credit-Building Potential

Getting the car loan is just the first step. The real work—and the real credit-building—happens during the loan’s term. Consistent, responsible management is the key to transforming this loan into a credit-building powerhouse.

Pay On Time, Every Time

This cannot be stressed enough. Your payment history is the most influential factor in your credit score. Missing even one payment can set back your credit-building efforts significantly.

To ensure you never miss a due date, set up automatic payments from your checking account. Alternatively, set multiple reminders on your phone or calendar a few days before the payment is due. Pro tips from us: if your payment due date doesn’t align with your pay schedule, ask your lender if you can adjust it. Consistency is king here; make it a habit you never break.

Consider Making Extra Payments (Wisely)

If your budget allows, making slightly larger payments than required, or an extra payment whenever you can, can be highly beneficial. This reduces your principal balance faster, meaning you pay less in total interest over the life of the loan and pay off the debt sooner.

Before doing so, always check your loan agreement for any prepayment penalties. Some lenders charge a fee if you pay off your loan early. Common mistakes include assuming all loans allow penalty-free early payments. If there are no penalties, paying extra is an excellent financial move.

Avoid Defaulting or Repossession

Defaulting on your car loan or having your car repossessed is one of the most damaging events for your credit score. It can drop your score by hundreds of points, remain on your report for seven years, and make it extremely difficult to secure credit in the future.

If you ever find yourself in financial difficulty and foresee missing a payment, immediately contact your lender. They may be able to offer solutions like deferment, forbearance, or a modified payment plan. Communication is crucial; don’t wait until you’ve missed a payment.

Monitor Your Credit Report Regularly

While your car loan is active, it’s essential to keep an eye on your credit reports. Continue to check them annually (or more frequently if your credit monitoring service allows) to ensure that your payments are being reported accurately and that there are no unauthorized accounts or errors.

This vigilance ensures that your credit-building efforts are properly reflected and helps you catch any fraudulent activity early. For a deeper dive into understanding your credit report, consider reading our article on How to Read Your Credit Report Effectively.

Maintain a Good Credit Mix (Over Time)

While your car loan is doing its job building your installment credit history, don’t neglect other aspects of your credit profile. Once you’ve established a few months of on-time car payments, you might consider applying for a secured credit card or a low-limit, unsecured card.

This introduces revolving credit to your mix, further diversifying your profile. Pro tips from us: always use credit cards responsibly, keeping balances low (under 30% utilization) and paying them off in full each month to avoid interest and maximize their credit-building potential.

Common Pitfalls and How to Avoid Them When Using a Car Loan to Build Credit

Even with the best intentions, it’s easy to stumble when navigating the world of credit. Awareness of common pitfalls can help you steer clear of significant setbacks.

Taking on Too Much Debt

The allure of a new car can be strong, but overspending on a vehicle you can’t comfortably afford is a recipe for disaster. A car loan that strains your budget increases the likelihood of missed payments, which, as we’ve discussed, devastates your credit.

Common mistakes include focusing solely on the monthly payment without considering the total cost, interest, and other car-related expenses. Always stick to your budget and prioritize affordability over luxury.

Missing Payments

This is the cardinal sin of credit building. Even one late payment can cause your credit score to plummet and overshadow months of responsible behavior.

The solution is proactive payment management: set up auto-pay, use reminders, and communicate with your lender before a payment is due if you anticipate difficulties. Never assume a missed payment will go unnoticed or that you can simply "catch up" later without consequences.

Ignoring Your Credit Report

Many people only check their credit report when applying for new credit. This is a common mistake. Errors can creep in, identity theft can occur, or payments might be misreported.

Regularly reviewing your credit report ensures accuracy and allows you to dispute any incorrect information promptly. This proactive approach safeguards your credit-building efforts.

Not Understanding Loan Terms

Before signing any loan agreement, read every single line. Understand the interest rate, the total amount you will pay over the loan term, any fees, and crucially, whether there are prepayment penalties.

Common mistakes include rushing through paperwork or trusting verbal assurances without seeing them in writing. If something isn’t clear, ask for clarification until you fully understand your obligations.

Prepayment Penalties

As mentioned, some loans include clauses that charge you a fee if you pay off your loan early. While paying off debt faster is generally a good thing, a prepayment penalty could negate some of the financial benefits.

Always confirm whether your loan has such a penalty before making extra payments or planning to pay off the loan ahead of schedule. Knowing this upfront helps you make an informed decision about accelerating your payments.

What Comes Next? Beyond the Car Loan for Credit Improvement

Once you’ve successfully managed your car loan for a significant period, you’ll likely see a positive impact on your credit score. But the journey doesn’t end there. Your car loan can be a powerful springboard to further financial growth.

Refinancing Your Car Loan

After 12-18 months of consistent, on-time payments, and with an improved credit score, you might be eligible to refinance your car loan. Refinancing means taking out a new loan, often with a different lender, to pay off your existing car loan.

The primary benefit is securing a lower interest rate, which can significantly reduce your monthly payments and the total interest paid over the life of the loan. It’s also another opportunity to demonstrate responsible borrowing if you continue to make timely payments on the new loan. Pro tips from us: always compare refinancing offers to your current loan to ensure it’s truly a better deal.

Diversifying Your Credit Portfolio

With a successfully managed car loan on your record, you’ll be in a much better position to access other types of credit. This is where you can truly diversify your credit mix.

Consider applying for a traditional, unsecured credit card (if you haven’t already), a small personal loan, or eventually, a mortgage. Each successfully managed account further strengthens your credit profile and demonstrates your ability to handle various financial responsibilities. For more advanced strategies to elevate your credit, check out our article on Advanced Strategies for Improving Your Credit Score.

Conclusion

Building credit from scratch or improving a thin credit file can feel daunting, but a car loan presents a tangible and effective path forward. By understanding how installment loans impact your credit score, taking strategic steps to secure favorable loan terms, and diligently managing your payments, you can transform a necessary purchase into a powerful credit-building tool.

Remember, the cornerstone of good credit is consistent, on-time payments. Combine this with smart financial planning, strategic debt management, and regular credit monitoring, and you’ll be well on your way to a robust financial future. Don’t just get a car; leverage it to build the credit you deserve. Start responsibly, stay vigilant, and watch your financial doors open.