How to Buy a Car with a Pre-Approved Loan: Your Ultimate Expert Guide to a Seamless Purchase

How to Buy a Car with a Pre-Approved Loan: Your Ultimate Expert Guide to a Seamless Purchase Carloan.Guidemechanic.com

Buying a new or used car can be an exhilarating experience, yet for many, it’s often fraught with stress, confusion, and the lingering fear of making a bad financial decision. The negotiation dance, the hidden fees, and the pressure from salespeople can turn an exciting prospect into a daunting ordeal. But what if there was a way to step into a dealership with confidence, armed with the knowledge and financial power to control the entire process?

There is, and it’s called a pre-approved car loan.

How to Buy a Car with a Pre-Approved Loan: Your Ultimate Expert Guide to a Seamless Purchase

Based on my extensive experience in the automotive and financial sectors, securing a pre-approved loan is arguably the single most powerful step you can take before even setting foot on a car lot. It transforms you from a vulnerable buyer into a savvy, informed negotiator. This comprehensive guide will walk you through every stage of buying a car with a pre-approved loan, ensuring you get the best deal, avoid common pitfalls, and drive away happy.

Let’s demystify the process and empower you to make your next car purchase truly seamless.

Why a Pre-Approved Loan is Your Secret Weapon in Car Buying

Imagine walking into a store knowing exactly how much you can spend, what your maximum budget is, and having your payment method ready. That’s the power a pre-approved car loan gives you. It shifts the dynamics of the negotiation squarely in your favor, offering a multitude of benefits that traditional financing often lacks.

1. Crystal-Clear Budgetary Clarity

One of the biggest advantages of a pre-approved loan is the definitive budget it provides. You’ll know precisely the maximum amount you’re approved to borrow, which helps you focus your car search on vehicles within your financial reach. This prevents the common mistake of falling in love with a car you can’t truly afford, saving you heartache and wasted time.

Knowing your spending limit upfront allows you to shop responsibly. You can prioritize features and models that align with your approved loan amount, ensuring your car purchase remains a joy, not a financial burden. This clarity is your first line of defense against overspending.

2. Unmatched Negotiating Power

When you have a pre-approved loan, you’re essentially a cash buyer in the eyes of the dealership. This puts you in a much stronger negotiating position because the dealer knows you’re ready to buy and don’t necessarily need their financing. They can focus solely on the price of the car, rather than trying to manipulate the financing terms to their advantage.

Pro tips from us: Always negotiate the "out-the-door" price of the vehicle first, before discussing any trade-in or financing options. Your pre-approval allows you to do exactly that, focusing the dealer’s attention on securing your business by offering a competitive vehicle price.

3. Streamlined and Faster Dealership Experience

Nobody enjoys spending hours, or even an entire day, at a car dealership. With a pre-approved loan, a significant portion of the typical car-buying process – the credit application and waiting for finance approval – is already complete. You can bypass the finance office bottleneck, allowing you to finalize the purchase much more quickly.

This efficiency not only saves you time but also reduces the opportunity for last-minute pressure tactics. You’ve already secured your funding, so the dealership’s primary goal becomes simply selling you the car, making the transaction smoother and more straightforward.

4. Avoid High-Pressure Sales Tactics

Dealerships often make a substantial profit from financing, sometimes even more than from the car itself. Without a pre-approval, you’re vulnerable to aggressive sales pitches for high-interest loans, extended warranties, and costly add-ons. Your pre-approval acts as a shield, allowing you to decline these extras with confidence.

You’re in control, and you can politely but firmly state that you have your own financing arranged. This immediately signals to the salesperson that their usual tactics won’t work, allowing you to maintain focus on the vehicle and its price.

5. Potentially Better Interest Rates

Lenders who offer pre-approved loans, such as banks and credit unions, often provide more competitive interest rates than dealership financing departments. This is because they specialize in lending and have a broader range of products. Shopping around for pre-approval ensures you secure the best possible rate based on your creditworthiness.

A lower interest rate over the life of your loan can save you thousands of dollars. Even a half-point difference can add up significantly, making the effort to secure a favorable pre-approval well worth it.

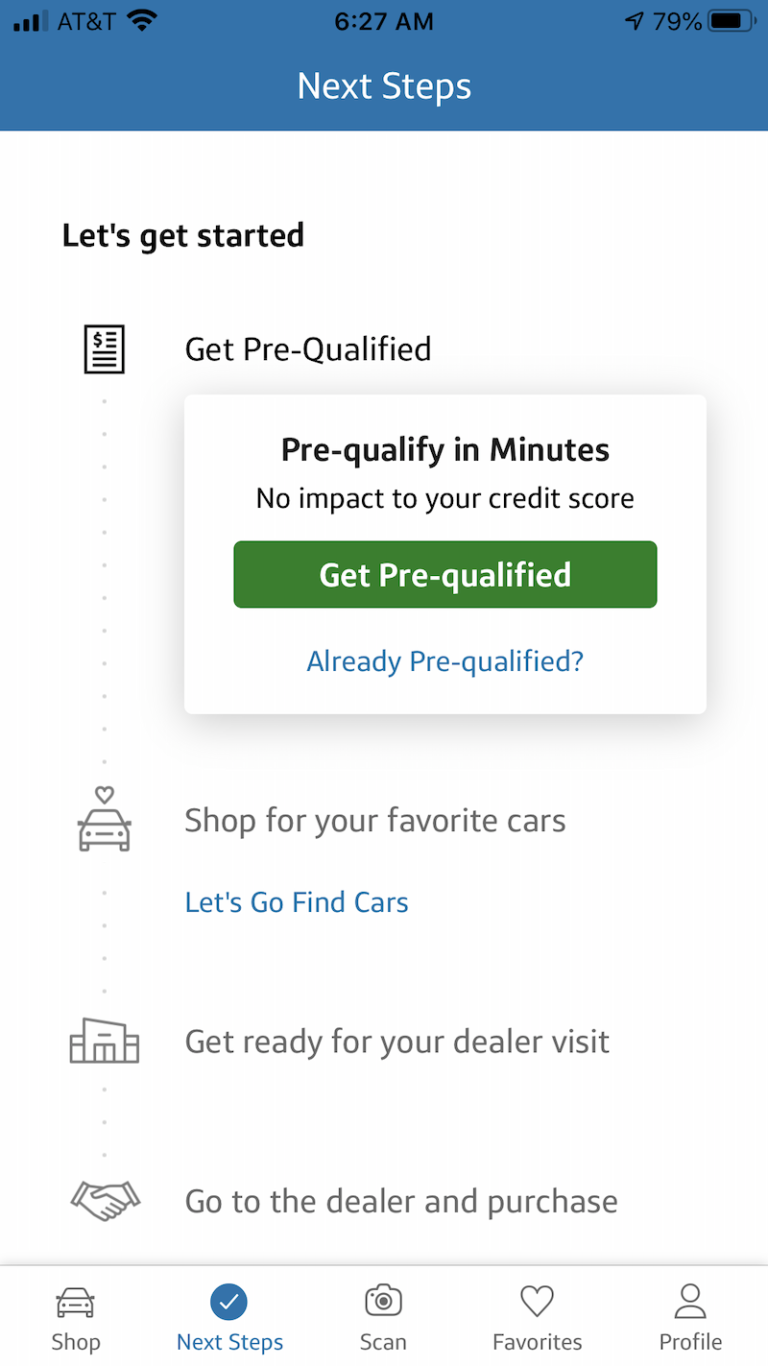

Your Step-by-Step Guide to Getting Pre-Approved for a Car Loan

Getting pre-approved isn’t complicated, but it does require a bit of preparation. Follow these steps to set yourself up for success.

Step 1: Understand Your Credit Score and Report

Your credit score is the single most important factor determining the interest rate you’ll receive on a car loan. Lenders use it to assess your creditworthiness and the risk associated with lending you money. A higher score typically translates to a lower interest rate, saving you money over the life of the loan.

Before applying for any loan, obtain a copy of your credit report from all three major bureaus (Equifax, Experian, TransUnion) and check your credit score. You can do this for free annually at AnnualCreditReport.com. Look for any inaccuracies or errors that could negatively impact your score and dispute them immediately. Understanding your score, whether it’s excellent, good, fair, or poor, will give you a realistic idea of the rates you can expect. For more detailed information on improving your financial standing, you might find our article on helpful. (Internal Link 1 Placeholder)

Step 2: Determine Your Realistic Budget and Down Payment

While your pre-approval will give you a maximum loan amount, your personal budget might dictate a lower figure. Consider not just the monthly loan payment, but also other costs of car ownership: insurance, fuel, maintenance, registration, and potential repairs. These "total cost of ownership" factors are crucial.

Based on my experience, a common mistake is only looking at the monthly payment. Calculate what you can truly afford each month without straining your finances. Also, consider how much you can comfortably put down as a down payment. A larger down payment reduces the loan amount, lowers your monthly payments, and can help you secure a better interest rate. Aim for at least 10-20% of the car’s value if possible.

Step 3: Gather Necessary Documentation

Lenders will require specific documents to process your pre-approval application. Having these ready beforehand will expedite the process. Typically, you’ll need:

- Proof of Identity: Driver’s license or state ID.

- Proof of Income: Recent pay stubs (usually 2-3 months), W-2 forms, or tax returns if self-employed.

- Proof of Residency: Utility bill or lease agreement.

- Social Security Number.

- Employer Information.

Having these documents organized will make the application process much smoother, whether you apply online, in person, or over the phone.

Step 4: Shop Around for Lenders (Don’t Settle for the First Offer!)

This is a critical step that many buyers overlook. Don’t just go to your current bank. Explore multiple options to find the best terms and interest rates. Lenders to consider include:

- Banks: Large national banks and smaller local banks.

- Credit Unions: Often offer highly competitive rates due to their member-focused structure.

- Online Lenders: Companies like LightStream, Capital One Auto Finance, and others specialize in online auto loans and can be very efficient.

Apply to several lenders within a short timeframe (typically 14-45 days, depending on the credit bureau model). This is crucial because multiple credit inquiries for the same type of loan within this window are usually counted as a single inquiry on your credit report, minimizing the impact on your score. This allows you to compare offers without penalty.

Step 5: Submit Your Application

Once you’ve chosen a few potential lenders, it’s time to submit your applications. Most lenders offer online applications that are quick and easy to complete. Be prepared to provide all the documentation you gathered in Step 3.

The application process typically involves a "hard inquiry" on your credit report, which will temporarily lower your score by a few points. However, as mentioned, applying to multiple auto lenders within a short period is usually treated as a single event for scoring purposes, so don’t let this deter you from rate shopping.

Step 6: Review and Understand Your Pre-Approval Offer

When you receive a pre-approval, carefully review all the terms and conditions. Key elements to look for include:

- Maximum Loan Amount: The highest amount you’re approved to borrow.

- Interest Rate (APR): This is the most important number, representing the true cost of borrowing.

- Loan Term: The length of the loan (e.g., 36, 48, 60, 72 months). Longer terms mean lower monthly payments but more interest paid over time.

- Any Conditions or Stipulations: Such as restrictions on the age or mileage of the vehicle, or a requirement for a specific down payment.

Ensure you understand every detail before proceeding. Don’t hesitate to ask the lender questions if anything is unclear. This is your money, and your responsibility to understand the agreement.

Navigating the Dealership with Your Pre-Approval in Hand

Now that you’re pre-approved, you’re ready to hit the car lot with confidence. Here’s how to make the most of your powerful position.

Step 1: Research Your Desired Vehicle Thoroughly

Before you even step foot in a dealership, have a clear idea of the make, model, and trim levels you’re interested in. Use online resources like Kelley Blue Book (KBB.com), Edmunds, and NADAguides to research fair market value, common features, and typical pricing for both new and used vehicles.

Knowing the market value of your target car will empower you during negotiations. You’ll be able to quickly identify if a dealer’s asking price is reasonable or inflated, and you’ll have data to back up your counter-offers.

Step 2: Test Drive and Conduct a Thorough Inspection

Never buy a car without a test drive. Drive it on various road types (city, highway) to get a real feel for its performance, handling, and comfort. Pay attention to any unusual noises, vibrations, or warning lights.

For used cars, consider having an independent mechanic conduct a pre-purchase inspection (PPI). This small investment can save you from costly repairs down the road. Common mistakes to avoid are rushing this step or feeling pressured to skip a thorough inspection; it’s your investment, so take your time.

Step 3: Disclose Your Pre-Approval Strategically

This is a key tactical move. Initially, when a salesperson asks how you plan to pay, simply state that you "have financing arranged." Do not immediately reveal the specific lender or the interest rate. This keeps the focus on the car’s price.

Once you’ve negotiated the best possible price for the vehicle itself, then you can present your pre-approval. This approach ensures the dealer doesn’t try to pad the car’s price, knowing they can make up the difference on financing.

Step 4: Negotiate the Car Price, Not the Monthly Payment

Based on my experience, this is where many buyers go wrong. Salespeople will often try to steer the conversation towards monthly payments. Resist this! Your pre-approval has already established your maximum loan amount. Your goal now is to get the lowest possible selling price for the car itself.

Focus on the "out-the-door" price, which includes the vehicle price, taxes, title, and registration fees. Only once this price is agreed upon should you consider how your pre-approved loan will be applied.

Step 5: Evaluate Dealership Financing Offers (If Any)

Even though you have a pre-approval, it’s worth seeing if the dealership can beat your rate. Sometimes, dealers have access to special manufacturer incentives or can offer highly competitive rates through their network of lenders.

Present your pre-approval offer and ask them if they can do better. If they can, congratulations – you’ve just saved even more money! If not, you simply proceed with your existing pre-approved loan. This comparison step ensures you’re getting the absolute best deal available.

Step 6: Handle Trade-Ins Separately (Pro Tip)

If you have a trade-in, avoid discussing it until you’ve firmly agreed on the purchase price of the new car. Combining these two negotiations can create confusion and allow the dealer to obscure the true value of your trade-in or the price of the new car.

Get a separate appraisal for your trade-in from multiple sources (online tools, other dealerships) before going in. Once the new car’s price is settled, then negotiate your trade-in as a separate transaction.

Step 7: Understand Add-ons and Extended Warranties

After agreeing on the car price, you’ll likely be sent to the finance office. This is where you’ll encounter pitches for extended warranties, paint protection, rust proofing, gap insurance, and other add-ons. While some of these might offer value, many are highly profitable for the dealership and may not be necessary.

Your pre-approval means you don’t need to feel pressured to buy these extras to "qualify" for financing. Carefully consider each offer, research its true value, and don’t be afraid to decline anything you don’t need or want. Remember, you can often purchase extended warranties or gap insurance from third parties at a lower cost.

Step 8: Review All Paperwork Carefully Before Signing

This is your final safeguard. Before signing any document, read everything thoroughly. Ensure the agreed-upon price, interest rate, loan term, and any other conditions are accurately reflected in the contract. Check for any added fees or products you didn’t agree to.

Common mistakes to avoid are signing quickly due to fatigue or pressure. Take your time, ask questions, and if something doesn’t look right, don’t sign until it’s corrected. Once you sign, the contract is legally binding.

Common Mistakes to Avoid When Buying with Pre-Approval

Even with a pre-approved loan, there are still pitfalls to navigate. Being aware of these common mistakes can save you stress and money.

- Not Sticking to Your Budget: Your pre-approval amount is a maximum, not a target. Don’t feel compelled to spend every dollar you’re approved for if a cheaper, suitable car fits your needs.

- Ignoring the Total Cost of Ownership: Beyond the monthly payment, factor in insurance, fuel, maintenance, and potential repairs. A cheap car to buy might be expensive to own. For more on this, check out our guide on . (Internal Link 2 Placeholder)

- Letting the Dealership Run Too Many Credit Checks: Some dealerships might insist on running their own credit checks even if you have a pre-approval, claiming they can "beat your rate." While it’s okay for them to check once to verify, politely decline if they try to run your credit multiple times through various lenders, as this can negatively impact your score.

- Forgetting About Insurance: Get insurance quotes before you finalize the purchase. Some vehicles are significantly more expensive to insure than others, which can drastically alter your overall car ownership costs.

- Rushing the Process: Car buying, especially with a significant investment, should not be rushed. Take your time to research, compare, test drive, and review all documents. Patience is your ally.

- Signing Without Reading: As mentioned, never sign anything you haven’t read and fully understood. Ask for clarification on any ambiguous terms.

Beyond the Purchase: What Comes Next?

Congratulations, you’ve bought your car with a pre-approved loan! But the journey doesn’t end there. Here are a few final steps:

- Set Up Insurance: You’ll need proof of insurance before you can drive your new car off the lot. Have your policy details ready.

- Registration and Tags: The dealership typically handles temporary tags and often the full registration process for you, but confirm the timeline and what you need to do.

- Make Your First Payment: Note your loan servicer, payment due date, and how to make payments. Set up automatic payments to avoid missing a due date.

- Maintain Your Credit: Continue to make all your loan payments on time. This will positively impact your credit score and make future financial endeavors easier.

Conclusion: Drive Away with Confidence

Buying a car with a pre-approved loan is not just a smart financial move; it’s a strategic approach that empowers you throughout the entire car-buying process. It transforms a potentially stressful negotiation into a confident, controlled transaction, allowing you to focus on finding the right car at the right price, with the right financing.

By understanding your credit, setting a realistic budget, shopping for the best loan terms, and strategically navigating the dealership, you put yourself in the driver’s seat. Remember, knowledge is power, and with a pre-approved loan, you hold all the cards. Drive away knowing you’ve made an informed decision, secured a great deal, and avoided the common pitfalls.

For more information on understanding consumer credit and loans, visit the Consumer Financial Protection Bureau’s website: https://www.consumerfinance.gov/.

Happy driving!