How to Determine Your Car Loan Payment: The Ultimate Guide to Smart Auto Financing

How to Determine Your Car Loan Payment: The Ultimate Guide to Smart Auto Financing Carloan.Guidemechanic.com

Buying a car is an exciting milestone, but navigating the world of auto loans can feel like deciphering a complex code. For many, the monthly car loan payment is a significant financial commitment that directly impacts their budget for years to come. Understanding precisely how this payment is calculated isn’t just about numbers; it’s about empowering yourself to make informed decisions, negotiate effectively, and secure a deal that truly aligns with your financial well-being.

As an expert blogger and SEO content writer with years of experience in personal finance, I’ve seen firsthand how a lack of understanding around car loan payments can lead to financial strain or missed opportunities. This comprehensive guide will demystify the process, breaking down every factor that influences your auto loan payment. Our ultimate goal is to equip you with the knowledge to confidently determine your car loan payment and navigate the auto financing landscape like a pro.

How to Determine Your Car Loan Payment: The Ultimate Guide to Smart Auto Financing

Why Understanding Your Car Loan Payment is Crucial for Every Buyer

Before we dive into the mechanics, let’s establish why this knowledge is non-negotiable. Your car loan isn’t just a number on a statement; it’s a long-term financial obligation. Being able to accurately determine your car loan payment before you even step onto a dealership lot puts you in a powerful position.

Firstly, it’s fundamental for budgeting. Knowing your exact monthly commitment allows you to assess if it fits comfortably within your existing financial framework, preventing future stress. A payment that’s too high can quickly derail other financial goals.

Secondly, understanding the components of your loan empowers you during negotiations. When you know how changes in interest rates, loan terms, or down payments affect the total cost, you can spot a good deal and challenge unfavorable terms. You’re not just accepting what’s offered; you’re actively shaping your financial future.

Finally, a deep understanding of your auto loan payments contributes to your overall financial health. It helps you avoid common pitfalls like overpaying for interest or getting stuck in a loan you can’t comfortably afford, ensuring your car purchase remains an asset, not a burden.

The Core Components That Determine Your Car Loan Payment

Several key variables come together to formulate your monthly car loan payment. Each plays a significant role, and a change in any one of them can substantially alter the final figure. Let’s break down these critical elements one by one.

1. The Vehicle’s Price (Principal Amount)

This might seem obvious, but the starting price of the vehicle forms the foundation of your loan. This isn’t just the sticker price you see; it’s the negotiated price you agree upon with the dealer, plus additional costs.

These additional costs typically include sales tax, registration fees, and various dealer processing fees. These can add hundreds, sometimes thousands, to the total amount you need to finance. Based on my experience, many buyers overlook these extra charges, only focusing on the car’s price. Always ask for an "out-the-door" price to get a true understanding of the principal.

If you have a trade-in vehicle, its value will be deducted from this principal amount, effectively reducing how much you need to borrow. A higher trade-in value means a smaller loan, which directly translates to lower monthly payments and less interest paid over the life of the loan.

2. Your Down Payment

A down payment is the initial amount of money you pay upfront towards the purchase of your car. This sum directly reduces the amount of money you need to borrow. The impact of a substantial down payment on your auto loan payment cannot be overstated.

When you put more money down, your principal loan amount decreases. This, in turn, results in lower monthly payments because you’re financing less over the same period. Crucially, it also means you’ll pay less in total interest over the life of the loan, saving you a significant amount of money.

Pro tips from us: Aim for at least a 10-20% down payment on a new car, and potentially more for a used car. A larger down payment can also help you secure a better interest rate, especially if your credit score isn’t perfect, as it signals less risk to lenders. It also helps mitigate the impact of depreciation, preventing you from being "upside down" on your loan (owing more than the car is worth).

3. The Loan Term (Length of the Loan)

The loan term refers to the duration over which you agree to repay the loan, typically expressed in months (e.g., 36, 48, 60, 72, or even 84 months). This factor has a direct and significant influence on your monthly payment.

A shorter loan term, such as 36 or 48 months, means you’ll pay off the loan quicker. While your monthly payments will be higher, the total amount of interest you pay over the life of the loan will be considerably less. This is because the lender has less time to accrue interest on the principal.

Conversely, a longer loan term (e.g., 72 or 84 months) will result in lower monthly payments, making the car seem more affordable on a month-to-month basis. However, this comes at a significant cost: you’ll pay much more in total interest over the life of the loan. Common mistakes to avoid are extending terms too long just to get a lower monthly payment, as this can lead to being upside down on your loan for a longer period and paying substantially more overall. It’s often a trade-off between monthly affordability and total cost.

4. The Interest Rate (APR – Annual Percentage Rate)

The interest rate, often expressed as an Annual Percentage Rate (APR), is essentially the cost of borrowing money. It’s a percentage of the principal loan amount that lenders charge you for the privilege of financing your vehicle. A lower interest rate means less money paid back to the lender beyond the principal.

APR is more comprehensive than just the interest rate; it includes certain fees associated with the loan, providing a more accurate representation of the total annual cost of borrowing. Factors influencing your APR include your credit score, the current market interest rates, the specific lender you choose, and even the loan term itself.

Pro tips from us: Even a small difference in APR can translate to hundreds, or even thousands, of dollars saved over the life of the loan. This is why shopping around for the best interest rate is paramount. Don’t just accept the first offer; compare rates from multiple lenders, including banks, credit unions, and online lenders. For more insights on how your credit score plays into this, check out our article on Improving Your Credit Score for Better Rates (simulated internal link).

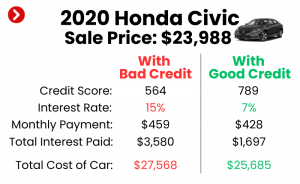

5. Your Credit Score

Your credit score is a numerical representation of your creditworthiness, reflecting your history of borrowing and repaying debt. It is one of the most critical factors lenders consider when determining your interest rate and, consequently, your car loan payment.

Borrowers with excellent credit scores (typically 720+) are considered low-risk and usually qualify for the lowest interest rates available. This translates to significantly lower monthly payments and less total interest paid. As your credit score decreases, lenders perceive you as a higher risk, and they compensate for that risk by offering higher interest rates.

Understanding your credit score before you apply for a car loan is a powerful advantage. It allows you to anticipate the rates you might qualify for and gives you time to address any issues. For a deeper dive into boosting your credit, read our comprehensive guide: The Ultimate Guide to Boosting Your Credit Score (simulated internal link). Knowing where you stand can literally save you thousands of dollars over the life of your car loan.

How to Determine Your Car Loan Payment: The Calculation Methods

Now that we understand the individual components, let’s explore how to put them all together to determine your car loan payment. While the underlying formula can be complex, modern tools make the process straightforward.

1. Using Online Car Loan Calculators

For most people, online car loan calculators are the easiest and most efficient way to estimate monthly payments. These tools are widely available on financial institution websites, reputable financial news sites, and even many dealership websites.

The benefits of using these calculators are numerous: they are quick, user-friendly, and allow you to instantly see how changes in different variables affect your payment. You’ll typically input the vehicle price, your desired down payment, the loan term (in months), and an estimated interest rate (APR). Some advanced calculators might also allow for trade-in value and sales tax.

Pro tips from us: Always use a few different calculators from various sources to cross-reference your estimates. This helps ensure accuracy and gives you a broader perspective. For a reliable starting point, you can try calculators from trusted financial institutions or sites like Bankrate’s auto loan calculator (simulated external link). Experiment with different scenarios (e.g., higher down payment, shorter term) to understand the impact on your budget.

2. The Manual Formula (For Deeper Understanding)

While online calculators handle the heavy lifting, understanding the manual formula can provide a deeper appreciation of how your car loan payment is structured. The standard formula for calculating a fixed-rate loan payment is:

M = P /

Where:

- M = Monthly Payment

- P = Principal Loan Amount (Vehicle Price – Down Payment + Taxes/Fees)

- i = Monthly Interest Rate (Annual Interest Rate / 12)

- n = Number of Payments (Loan Term in Months)

While solving this manually might be cumbersome, knowing what each variable represents reinforces your understanding of how each component directly influences your monthly outgoing. It highlights the exponential power of interest and the impact of the loan term.

Beyond the Monthly Payment: The True Cost of Your Car Loan

Focusing solely on the monthly payment can be a trap. While it’s crucial for budgeting, it doesn’t tell the whole story of what your car truly costs you over time. To genuinely understand your auto financing, you need to look at the bigger picture.

The most significant "hidden" cost is often the total interest paid over the life of the loan. A lower monthly payment achieved by extending the loan term usually means you’ll pay substantially more in interest. Always ask lenders for the total cost of the loan, not just the monthly payment.

Beyond the loan itself, remember that car ownership involves other substantial expenses. These include insurance premiums, fuel costs, routine maintenance, and potential repairs. Common mistakes to avoid are neglecting to budget for these ongoing costs, which can quickly turn an "affordable" monthly car loan payment into an unsustainable burden. Always factor in these additional costs when determining if a vehicle truly fits your budget.

Strategies for Getting the Best Car Loan Deal

Securing a favorable car loan goes beyond just knowing how to calculate payments; it involves strategic planning and savvy negotiation. Here are some expert strategies to help you get the best deal:

First and foremost, get pre-approved for a loan before you visit the dealership. This means applying for a loan with a bank, credit union, or online lender beforehand. Having a pre-approval in hand gives you a clear understanding of the interest rate and loan terms you qualify for, essentially providing you with a benchmark.

Secondly, shop around for lenders. Don’t limit yourself to the financing offered by the dealership. While dealership financing can sometimes be competitive, it’s often not the best option. Compare offers from at least three different lenders to ensure you’re getting the most favorable terms.

Thirdly, negotiate the car price first, separate from financing. When you’re at the dealership, focus on getting the best possible purchase price for the vehicle before discussing financing. Once you’ve agreed on a price, then you can discuss the loan. This prevents the dealer from manipulating numbers between the car price and loan terms.

Finally, read the fine print carefully. Before signing any loan documents, scrutinize every detail. Understand all fees, the exact APR, and any prepayment penalties. If something doesn’t make sense, ask for clarification. Don’t be afraid to walk away if the terms aren’t right for you.

When to Consider Refinancing Your Car Loan

Even after you’ve secured a car loan, your financial journey isn’t necessarily set in stone. There are situations where refinancing your car loan can be a smart move, potentially leading to lower monthly payments or significant savings on total interest.

One primary reason to consider refinancing is if your credit score has significantly improved since you first took out the loan. A higher credit score makes you eligible for lower interest rates, which a new loan could capitalize on.

Another scenario is if market interest rates have dropped since your original loan. Even if your credit hasn’t changed, a general downturn in rates could mean you qualify for a better deal now.

Finally, some people refinance to achieve a lower monthly payment. This is often done by extending the loan term. While it provides immediate relief to your budget, be cautious, as extending the term will likely increase the total interest you pay over the life of the loan. Always weigh the short-term benefit against the long-term cost before making such a decision.

Conclusion: Empowering Your Auto Financing Decisions

Understanding how to determine your car loan payment is more than just a financial exercise; it’s a critical skill for any car buyer. By thoroughly understanding the impact of the principal amount, your down payment, the loan term, the interest rate (APR), and your credit score, you gain the power to make informed choices that align with your financial goals.

We’ve explored everything from the core components that shape your payment to practical calculation methods and smart strategies for securing the best possible deal. Remember, a lower monthly payment isn’t always the best deal if it means paying significantly more in total interest. The ultimate goal is to find a balance that fits your budget comfortably while minimizing your overall cost of borrowing.

Armed with this knowledge, you are now well-prepared to approach your next car purchase with confidence and clarity. Take the time to plan, compare, and negotiate, and you’ll drive away not just with a new car, but with a sound financial decision. Start by using an online calculator today to see how these variables impact your potential monthly payments!