How to Find a Car Loan: Your Ultimate Guide to Driving Away with Confidence

How to Find a Car Loan: Your Ultimate Guide to Driving Away with Confidence Carloan.Guidemechanic.com

Embarking on the journey to purchase a new or used vehicle is an exciting prospect. However, for many, the financing aspect can feel like navigating a complex maze. Securing the right car loan isn’t just about finding the lowest interest rate; it’s about understanding the entire process, your financial standing, and the options available to you.

As an expert blogger and SEO content writer with years of experience in consumer finance, I’ve seen countless individuals struggle with the complexities of car loans. My mission with this comprehensive guide is to demystify the process, providing you with actionable insights and proven strategies to find a car loan that fits your budget and financial goals. We’ll cover everything from preparing your finances to understanding loan terms and securing the best deal, ensuring you drive away with confidence.

How to Find a Car Loan: Your Ultimate Guide to Driving Away with Confidence

The Foundation: Preparing Your Finances Before You Even Look at Cars

Before you even step foot in a dealership or browse online listings, the most crucial step is to get your financial house in order. This preparation will not only save you time but also potentially thousands of dollars over the life of your loan. It’s about empowering yourself with knowledge.

Understanding Your Financial Standing

Knowing where you stand financially is the bedrock of a successful car loan application. Lenders will scrutinize several aspects of your financial history to assess your risk. By understanding these factors, you can proactively address any weaknesses.

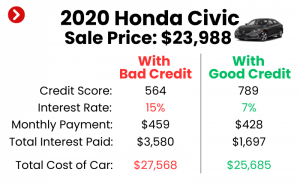

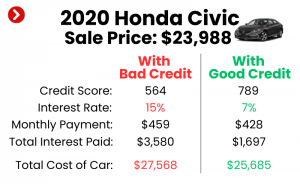

Your credit score is arguably the most significant factor in determining the interest rate you’ll be offered. A higher score signals less risk to lenders, leading to more favorable terms. Scores generally range from 300 to 850, with anything above 670 typically considered "good."

Based on my experience, many people are unaware of their credit score until they apply for a loan. This can lead to unwelcome surprises. You should check your credit report from all three major bureaus (Equifax, Experian, and TransUnion) at least once a year. You can obtain a free report from each annually at AnnualCreditReport.com. Reviewing these reports allows you to identify any errors that might be dragging your score down.

Beyond your credit score, lenders also look at your debt-to-income (DTI) ratio. This ratio compares your total monthly debt payments to your gross monthly income. A low DTI indicates you have sufficient income to manage additional debt, like a car loan. Lenders typically prefer a DTI ratio of 36% or lower, though some might go up to 43%.

Pro tips from us: Calculate your DTI before applying. Add up all your monthly debt payments (credit cards, student loans, mortgage, etc.) and divide that by your gross monthly income. This gives you a clear picture of how much more debt you can realistically take on.

Finally, creating a realistic budget is paramount. Don’t just consider the monthly car payment; factor in other costs like insurance, fuel, maintenance, and registration. A car is more than just its purchase price. An honest assessment of what you can truly afford each month ensures you don’t overextend yourself.

Improving Your Credit Score for Better Loan Terms

If your credit score isn’t where you’d like it to be, don’t despair. There are concrete steps you can take to improve it, which will directly translate into better car loan offers. Even a slight improvement can lead to significant savings on interest over the loan term.

The most fundamental step is to pay all your bills on time, every time. Payment history is the largest component of your credit score. Missing payments, even by a few days, can have a detrimental effect. Set up automatic payments or reminders to ensure you never miss a due date.

Another effective strategy is to reduce your existing debt, especially on credit cards. High credit utilization (the amount of credit you’re using compared to your total available credit) can negatively impact your score. Aim to keep your credit card balances below 30% of your credit limit. Paying down balances shows lenders you can responsibly manage debt.

Common mistakes to avoid are closing old credit accounts once they’re paid off. While it might seem counterintuitive, closing accounts can reduce your overall available credit, thus increasing your utilization ratio. It also shortens your credit history, which is another factor in your score.

Regularly checking your credit report for errors is also critical. Incorrect late payments, fraudulent accounts, or wrong balances can all unfairly depress your score. If you find an error, dispute it immediately with the credit bureau. This proactive approach can significantly bolster your creditworthiness. For more details on managing your budget, check out our guide on .

Saving for a Down Payment

While it might be tempting to finance 100% of your car’s purchase price, making a substantial down payment offers numerous advantages. It’s a strategic move that benefits you in both the short and long term.

A larger down payment immediately reduces the amount you need to borrow. This translates directly into lower monthly payments, making your car loan more manageable. It also means you’ll pay less in total interest over the life of the loan, saving you money.

Beyond the immediate financial benefits, a significant down payment also reduces your loan-to-value (LTV) ratio. A lower LTV makes you a less risky borrower in the eyes of lenders, potentially qualifying you for better interest rates and more favorable terms. This is especially important for used cars, which depreciate quickly.

Furthermore, a down payment helps prevent you from being "upside down" on your loan, where you owe more than the car is worth. This situation, often called negative equity, can create financial headaches if you need to sell or trade in your car prematurely. Aim for at least 10-20% of the car’s purchase price as a down payment if possible. If you’re curious about improving your financial health further, read our article on .

Exploring Your Car Loan Options

Once your finances are in order, the next step is to understand the various avenues available for securing a car loan. Not all loans are created equal, and knowing your choices will help you make an informed decision.

Types of Car Loans

While the basic premise of a car loan remains the same – borrowing money to buy a car and repaying it with interest – there are subtle differences in the types of loans you might encounter. Understanding these nuances can help you align the loan with your specific vehicle choice and financial situation.

The most common distinction is between new car loans and used car loans. New car loans typically come with lower interest rates due to the vehicle’s higher value and lower risk of mechanical issues. Used car loans often have slightly higher rates because the vehicle’s value is lower and depreciation has already occurred, making them a higher risk for lenders. The loan terms for used cars might also be shorter.

Another way to categorize loans, though less common for car loans, is secured versus unsecured. Almost all car loans are secured loans, meaning the car itself acts as collateral. If you default on the loan, the lender has the right to repossess the vehicle. Unsecured loans, like personal loans, don’t require collateral but are much riskier for lenders and thus come with significantly higher interest rates, making them generally unsuitable for car purchases.

Finally, it’s crucial to understand the difference between direct lending and dealership financing. Direct lending involves getting a loan directly from a bank, credit union, or online lender before you go car shopping. Dealership financing, on the other hand, means applying for a loan through the dealership, which then works with its network of lenders.

Where to Find Car Loans

The landscape of car loan providers is diverse, each offering unique advantages. Exploring all your options will ensure you find the most competitive rates and terms. Don’t limit yourself to the first offer you receive.

Traditional banks are a common source for car loans. They often offer competitive rates, especially if you’re an existing customer with a good banking relationship. The application process can be straightforward, and you might benefit from in-person guidance. However, their rates might not always be the absolute lowest, and their approval criteria can sometimes be strict.

Credit unions are member-owned financial cooperatives known for offering some of the most competitive car loan rates. Because they are non-profit organizations, their primary goal is to serve their members, often passing savings on through lower interest rates and fewer fees. You usually need to become a member to apply, which often involves a small deposit or meeting specific eligibility criteria.

In recent years, online lenders have emerged as a popular option. They offer unparalleled convenience, allowing you to apply for and compare loans from the comfort of your home. Many online platforms provide quick pre-approvals and tools to compare multiple offers simultaneously. This can be a great way to efficiently shop around for the best rates without visiting multiple physical locations.

Dealerships also offer financing, often promoting special rates or incentives directly from the manufacturer. This can be a convenient one-stop shop, allowing you to choose and finance your car in the same location. However, be cautious: while dealerships can sometimes offer great deals, they also act as intermediaries and might mark up interest rates. It’s always wise to arrive at the dealership with a pre-approved loan offer from an external lender so you have a benchmark for comparison.

The Pre-Approval Process: Your Secret Weapon

Pre-approval is arguably the most powerful tool you have when searching for a car loan. It transforms you from a casual browser into a confident buyer, armed with a clear understanding of your budget and borrowing power.

What is Pre-Approval?

Car loan pre-approval is when a lender reviews your financial information and tentatively agrees to lend you a specific amount of money at a certain interest rate, pending final verification. It’s not a final commitment, but it’s very close.

The benefits of getting pre-approved are numerous. Firstly, it provides you with a clear budget. You’ll know exactly how much you can afford, preventing you from falling in love with a car outside your price range. This financial clarity helps you focus your search.

Secondly, pre-approval gives you significant negotiation power at the dealership. Instead of discussing payments, you can negotiate the car’s price as if you were a cash buyer. You already have your financing secured, so the dealership knows you’re a serious buyer. This shifts the focus away from the loan terms they might offer and onto the vehicle’s price, often leading to a better deal.

Lastly, pre-approval streamlines the car-buying process. When you arrive at the dealership with financing already in hand, you can focus on test drives and vehicle features, significantly reducing the time spent in the finance office. This makes the entire experience much smoother and less stressful.

How to Get Pre-Approved

The pre-approval process is straightforward and typically doesn’t take long. Being prepared with the necessary documentation will make it even quicker.

When applying for pre-approval, you’ll generally need to provide personal information (name, address, Social Security number), employment details (income, employer), and financial information (assets, existing debts). Having these documents readily accessible will expedite the application.

It’s important to understand the difference between a "soft inquiry" and a "hard inquiry" on your credit report. Many pre-approval processes involve a soft inquiry, which doesn’t affect your credit score. This allows you to shop around with multiple lenders without concern. However, once you proceed with a full application for a loan, a hard inquiry will be made.

Based on my experience, it’s beneficial to apply for pre-approval with 2-3 different lenders within a short period (typically 14-45 days, depending on the credit scoring model). Multiple hard inquiries for the same type of loan within this "shopping window" are usually counted as a single inquiry, minimizing the impact on your credit score. This allows you to compare offers effectively without harming your credit.

Comparing Loan Offers and Understanding the Terms

Once you have multiple pre-approval offers, the real work of comparing them begins. It’s essential to look beyond just the monthly payment and delve into the underlying terms and conditions.

Key Loan Terms to Understand

Navigating the jargon of loan agreements can be intimidating, but understanding a few key terms will empower you to make an informed decision. These terms directly impact the total cost of your loan.

The Annual Percentage Rate (APR) is perhaps the most critical number to consider. It represents the total cost of borrowing money annually, expressed as a percentage. The APR includes not only the interest rate but also any fees associated with the loan. Therefore, comparing APRs is the most accurate way to compare the true cost of different loan offers. A lower APR means less money paid over the life of the loan.

The loan term, or duration, refers to the length of time you have to repay the loan, typically expressed in months (e.g., 36, 48, 60, 72 months). A shorter loan term generally means higher monthly payments but less total interest paid because you’re borrowing the money for a shorter period. Conversely, a longer loan term results in lower monthly payments but more total interest paid.

Common mistakes to avoid are focusing solely on the monthly payment. While it’s important for budgeting, a low monthly payment achieved through a very long loan term can end up costing you significantly more in interest over time. Always consider the total amount you will pay back.

Finally, be aware of any fees associated with the loan. These can include origination fees, documentation fees, or prepayment penalties. While many reputable lenders don’t charge prepayment penalties on car loans, it’s always wise to check. These fees can add to the overall cost, so factor them into your comparison.

How to Compare Offers Effectively

With several pre-approval offers in hand, it’s time to put on your analytical hat. A thorough comparison will reveal the best fit for your financial situation.

Don’t just eyeball the numbers. Create a simple spreadsheet or use an online loan calculator to compare each offer side-by-side. Focus on the APR, the total amount to be repaid (principal + interest + fees), and the monthly payment for the same loan term. If offers have different terms, adjust your calculations to standardize them for a fair comparison.

Pro tips from us: Pay close attention to any additional conditions or clauses in the loan agreement. Are there any restrictions on mileage? Are there specific insurance requirements? Understanding the fine print now can prevent headaches later.

Also, remember that pre-approval is not a commitment. You are not obligated to accept any offer until you sign the final loan documents. This gives you the flexibility to decline offers that don’t meet your expectations or to use a better offer as leverage for negotiation with another lender or the dealership. Never feel pressured to accept the first offer.

Applying for the Car Loan and Sealing the Deal

Once you’ve chosen your car and secured your preferred loan offer, the final steps involve completing the application and understanding the closing process. This stage requires attention to detail to ensure everything aligns with your expectations.

The Application Process

Even after pre-approval, there are still a few formal steps to take to finalize your car loan. This ensures all information is accurate and legally binding.

You’ll need to gather all required documents for the final loan application. This typically includes proof of income (pay stubs, tax returns), proof of residence (utility bills, lease agreement), proof of identity (driver’s license, Social Security card), and details about the vehicle you intend to purchase (VIN, purchase agreement). Having these ready will make the process swift.

When filling out the application, accuracy is paramount. Double-check all personal and financial information. Any discrepancies could lead to delays or, in some cases, denial of the loan. Be honest and thorough in your responses.

Pro tips from us: If you’re applying for a car loan at the dealership, be prepared to present your pre-approval letter. This signals that you’re a serious buyer with financing already secured, which can streamline the dealership’s process and prevent them from trying to push their own, potentially less favorable, financing options.

What Happens After Application

After submitting your final application, the lender will typically conduct a final review and verification process. This step is known as underwriting.

During underwriting, the lender verifies all the information you provided in your application. They might call your employer to confirm employment or review bank statements. This is their final check to ensure everything is in order before approving the loan.

You will then receive a decision: approval, conditional approval, or denial. If approved, congratulations! You’re ready to finalize the purchase. Conditional approval means the lender will approve the loan if you meet certain conditions, such as providing additional documentation or making a larger down payment.

Common mistakes to avoid are changing your financial situation between pre-approval and final application. Don’t open new credit accounts, take on new debt, or make large purchases. These actions can alter your credit profile and potentially jeopardize your final loan approval.

Common Reasons for Loan Denial

While thorough preparation significantly increases your chances of approval, sometimes a loan might still be denied. Understanding the common reasons can help you address issues or prepare for future applications.

Based on my experience, the most frequent reason for car loan denial is a low credit score or a poor credit history. Lenders view these as indicators of high risk. If your score is low, focus on the strategies discussed earlier to improve it before reapplying.

Another common reason is a high debt-to-income (DTI) ratio. If your existing debt obligations are too high relative to your income, lenders may worry about your ability to manage additional monthly payments. Consider paying down other debts before seeking a new car loan.

Unstable employment history or insufficient income can also lead to denial. Lenders want to see a steady source of income to ensure you can make consistent payments. If you’ve recently changed jobs or have irregular income, you might need to provide additional documentation or a larger down payment.

If your loan is denied, don’t give up. Ask the lender for the specific reasons for the denial. They are legally required to provide this information. Use this feedback to improve your financial situation and reapply in the future, perhaps with a co-signer or a larger down payment.

Post-Approval and Beyond

Getting your car loan approved is a significant achievement, but the journey doesn’t end there. Understanding your responsibilities post-approval and knowing your options for the future are crucial for long-term financial health.

What to Do After Approval

Once your car loan is approved and you’ve driven off the lot, there are a few important steps to take to ensure a smooth repayment period.

First and foremost, read your entire loan agreement carefully. Even if you’ve reviewed the terms during the application process, the final document might contain specific details about payment schedules, late fees, and other important clauses. Understand every aspect of what you’ve signed.

Familiarize yourself with your payment schedule and methods. Know your due date, how to make payments (online, mail, phone), and what penalties apply for late payments. Setting up automatic payments can be a great way to ensure you never miss a deadline, which helps maintain your credit score.

Pro tips from us: Keep all your loan documents organized and accessible. This includes your contract, payment schedule, and any correspondence from the lender. This will be invaluable if you ever have questions or need to reference the terms of your agreement.

Refinancing Your Car Loan

Life circumstances and financial situations can change. What was a good loan initially might not be the best fit down the road. Refinancing your car loan is a valuable option to consider in certain scenarios.

Refinancing means replacing your existing car loan with a new one, often with different terms. There are several reasons why refinancing might make sense. If your credit score has significantly improved since you first took out the loan, you might qualify for a lower interest rate, saving you money over the remaining term.

Another reason to refinance is to lower your monthly payments. This can be achieved by extending the loan term, though remember this will likely increase the total interest paid. Conversely, you might refinance to shorten your loan term and pay off the car faster, reducing overall interest.

The process for refinancing is similar to applying for your initial car loan. You’ll research lenders, apply for pre-approval, compare offers, and then finalize the new loan. Be sure to compare the APRs and total cost of the new loan against your current loan to ensure it’s truly a beneficial move. Don’t forget to factor in any potential fees associated with the new loan.

Conclusion: Drive Away with Confidence

Finding a car loan doesn’t have to be a source of stress. By approaching the process systematically, preparing your finances, understanding your options, and carefully comparing offers, you can secure a loan that aligns perfectly with your budget and financial goals. Remember, knowledge is power, and taking the time to educate yourself will pay dividends in the long run.

From understanding your credit score and making a solid down payment to exploring various lenders and leveraging pre-approval, each step brings you closer to a smart financial decision. Always read the fine print, ask questions, and never feel rushed into a decision. With this comprehensive guide in hand, you are now equipped to navigate the world of car loans with confidence and drive away knowing you’ve made the best choice for your future. Start your journey today and enjoy the open road ahead!