How To Find Interest Paid On Car Loan: Your Ultimate Guide to Unlocking Auto Loan Interest Details

How To Find Interest Paid On Car Loan: Your Ultimate Guide to Unlocking Auto Loan Interest Details Carloan.Guidemechanic.com

Understanding the true cost of your car loan goes far beyond the monthly payment. A significant portion of what you pay each month, especially in the early stages of your loan, is dedicated to interest. Knowing precisely how to find interest paid on car loan is not just a matter of curiosity; it’s a crucial step towards smarter financial management, potential tax benefits (in specific cases), and making informed decisions about your vehicle financing.

As an expert in personal finance and auto loans, I’ve guided countless individuals through the intricacies of vehicle financing. This comprehensive guide will equip you with all the knowledge and practical methods you need to confidently track and understand the interest you’ve paid on your auto loan. We’ll delve deep into various approaches, from scrutinizing official documents to leveraging online tools, ensuring you have a complete picture of your financial commitment.

How To Find Interest Paid On Car Loan: Your Ultimate Guide to Unlocking Auto Loan Interest Details

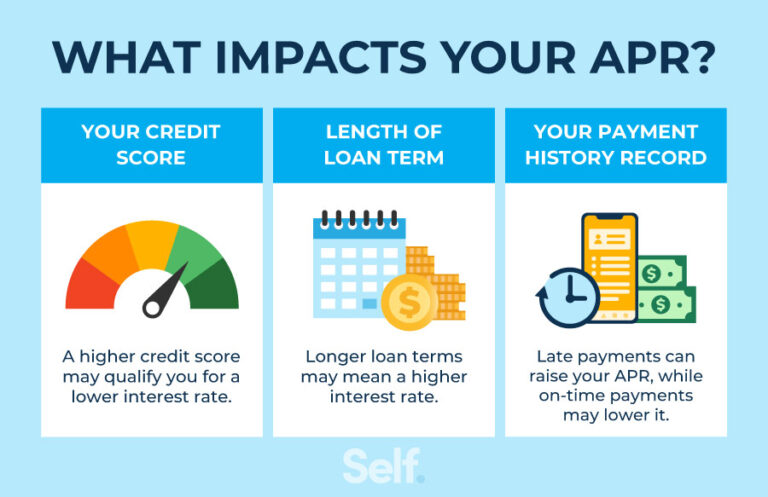

Why Knowing Your Auto Loan Interest Matters: More Than Just a Number

Before we dive into the "how," let’s explore the "why." Pinpointing the exact amount of car loan interest paid offers several significant advantages for your financial health and planning. This isn’t just about satisfying a numerical curiosity; it’s about empowerment.

1. Financial Planning and Budgeting:

Knowing how much interest you’ve paid helps you understand the true cost of borrowing. This insight is invaluable for creating realistic budgets and forecasting future expenses. It highlights how much of your hard-earned money is going towards the lender’s profit versus reducing your principal debt.

2. Tax Implications (Specific Scenarios):

While personal car loan interest is generally not tax-deductible, there are specific exceptions. If you use your vehicle for business purposes, a portion of the interest might be deductible. Understanding your total interest paid is the first step in determining any potential tax savings. We’ll explore these nuances later in the article.

3. Informed Refinancing Decisions:

If you’re considering refinancing your auto loan, knowing your past auto loan interest paid gives you a clear baseline. It helps you compare your current loan’s performance against potential new offers. You can evaluate if a new loan truly saves you money over the long term.

4. Understanding Your Loan’s Structure:

By tracking interest, you gain a deeper understanding of how your loan works. You’ll see how interest payments dominate the early stages of an amortization schedule, gradually shifting towards more principal payments as the loan matures. This knowledge is fundamental to effective debt management.

5. Debt Management and Accelerated Payoff Strategies:

When you understand how much interest you’re paying, you can develop strategies to pay down your principal faster. Making extra principal payments directly reduces the interest you’ll owe over the life of the loan. This knowledge fuels motivation and smart financial choices.

The Most Reliable Methods to Find Interest Paid On Your Car Loan

There are several reliable avenues to uncover the specific amount of interest paid on car loan. Each method offers a slightly different perspective or level of detail. Based on my experience, combining a few of these approaches often provides the most comprehensive understanding.

Method 1: Scrutinizing Your Monthly Loan Statements

Your monthly loan statement is a treasure trove of information, often overlooked by borrowers. It’s the most consistent and readily available record of your payment activity.

Every month, your lender sends a statement detailing your recent payment. This document typically breaks down how much of your payment went towards the principal balance and how much covered the interest. Look for sections labeled "Payment Breakdown," "Principal Applied," and "Interest Applied."

Carefully reviewing these statements each month allows you to track the cumulative interest paid over time. While it can be a bit tedious to manually sum these figures for an entire year or the loan’s duration, it provides an accurate, official record directly from your lender. Many lenders now provide these statements digitally, making them easier to access and store.

Method 2: Accessing Your Lender’s Online Portal or Website

In today’s digital age, your lender’s online portal is arguably the easiest and most efficient way to find your annual interest statement or a summary of interest paid on auto loan. Most financial institutions offer robust online platforms for their customers.

Here’s a typical step-by-step approach:

- Login: Access your lender’s official website and log in to your account using your credentials.

- Navigate: Look for sections such as "Account Summary," "Loan Details," "Statements," or "Documents."

- Find Year-End Summaries: Many lenders provide a year-end summary specifically designed for tax purposes or for a quick overview. This statement will typically show the total car loan interest paid for the entire calendar year. It might be labeled as "Annual Interest Statement" or similar.

- Download Statements: You can often download individual monthly statements or annual summaries as PDF files for your records.

Pro tips from us: Always ensure you are on the legitimate website of your lender to protect your personal and financial information. Bookmark the correct login page for easy access. If you can’t find the information, don’t hesitate to use their search function within the portal.

Method 3: Contacting Your Lender Directly

Sometimes, the simplest approach is the best. If you’re struggling to find the information online or prefer a direct conversation, reaching out to your lender’s customer service department is a highly effective method.

When you call, have your loan account number and personal identification ready. Clearly state that you need to know the total interest paid on your car loan for a specific period (e.g., the last calendar year or since the loan inception). They can often provide this information over the phone or email you an official statement.

Common mistakes to avoid are not having your account details readily available, which can delay the process. Also, be prepared for potential wait times, especially during peak hours. Some lenders also offer in-branch services where you can speak to a representative in person.

Method 4: Reviewing Your Annual Interest Statement (Year-End Summaries)

While the IRS Form 1098-E is specifically for student loan interest, many auto lenders provide their own version of an annual interest statement or a comprehensive year-end summary. This document is usually mailed to you or made available in your online portal around tax season (January/February).

This year-end summary is crucial because it consolidates all the interest paid on your car loan for the previous calendar year into a single, easy-to-read figure. It’s designed to simplify your financial record-keeping and is often the most straightforward way to get the total annual interest.

Pro tip from us: Always save these year-end statements, even if you don’t believe the interest is tax-deductible. They serve as excellent records for your personal finance archives and can be useful for future financial planning or refinancing discussions.

Method 5: Using an Amortization Schedule

An amortization schedule is a table detailing each payment made on a loan, breaking down how much goes towards interest and how much towards the principal. While it won’t tell you the actual interest you’ve paid if you’ve made extra payments or paid late, it’s an excellent tool for understanding and estimating.

You can create an amortization schedule using online calculators or spreadsheet software. You’ll need your original loan amount, interest rate, and loan term. The schedule will then show you the projected interest paid with each installment.

Based on my experience, an amortization schedule is a powerful planning tool. It illustrates how interest front-loads your payments in the early years of the loan. However, remember its limitation: it’s a projection. If you’ve made any payments beyond the scheduled amount, your actual interest paid will be lower than what the schedule indicates. It’s best used as an educational or estimative tool, not for precise historical figures if your payment behavior varied.

Method 6: Consulting Personal Financial Software and Apps

Many personal finance management tools, such as Mint, Quicken, YNAB (You Need A Budget), or even advanced banking apps, can track your spending and categorize payments. If you’ve linked your auto loan account to one of these platforms, they might automatically categorize your payments into principal and interest.

These tools offer a convenient dashboard view of your financial life. They can often generate reports that show how much you’ve spent on auto loan interest paid over a specific period. The accuracy largely depends on how well the software categorizes your transactions and whether it integrates directly with your loan servicer’s data.

Common pitfalls include incorrect categorization or an inability to distinguish between principal and interest portions of a single payment. Always cross-reference with official statements if you rely on these tools for precise figures.

Method 7: Reviewing Your Original Loan Agreement

While your original loan agreement won’t tell you how much interest you’ve already paid, it provides the foundational details of your loan. This includes the annual interest rate, the total amount financed, and often, the total interest expected to be paid over the life of the loan if all payments are made on schedule.

This document is invaluable for understanding the baseline cost of your loan. It helps you contextualize the interest figures you find through other methods. For instance, if your amortization schedule or lender’s statement shows you’re paying significantly more interest than you anticipated, reviewing the original agreement can help identify any discrepancies or misunderstandings about your loan terms.

Calculating Interest Paid Manually (When Other Options Fail)

In rare cases, you might need to calculate the interest paid manually. This method is more complex and typically less accurate than obtaining the figures directly from your lender, especially for loans with daily interest accrual or variable rates. However, for a basic understanding or estimation, it can be useful.

Most car loans use a simple interest method, meaning interest is calculated on the outstanding principal balance each day.

Here’s a simplified conceptual approach:

- For each payment:

- Find the daily interest rate (Annual Rate / 365).

- Multiply the daily rate by the number of days since your last payment.

- Multiply this by your outstanding principal balance before the current payment. This gives you the interest for that period.

- Subtract this interest amount from your total payment to find the principal portion.

- Update your principal balance.

- Sum it up: Add up all the interest amounts calculated for each payment over your desired period.

This method requires a bit more effort and meticulous record-keeping. It’s highly recommended to use this only as a last resort or for rough estimations, as slight variations in lender calculations or payment timings can lead to discrepancies. Always prioritize official statements from your lender for accuracy.

Common Mistakes and Pitfalls to Avoid

Navigating the world of car loan interest calculation can have its challenges. Being aware of common mistakes can save you time and prevent inaccuracies.

- Confusing Principal with Interest: A very common error is not understanding the distinction between the principal (the amount borrowed) and the interest (the cost of borrowing). Your monthly payment covers both, but the proportions change over time.

- Relying Solely on Initial Estimates: An initial loan quote or a basic online calculator provides an estimate. Your actual auto loan interest paid will reflect your precise payment history, including any extra payments or late fees.

- Ignoring Extra Payments: If you’ve made additional payments towards your principal, your actual interest paid will be lower than what a standard amortization schedule or initial projection suggests. These extra payments directly reduce your principal, leading to less interest accruing.

- Not Keeping Good Records: Failing to save monthly statements, year-end summaries, or even email correspondence with your lender can make it incredibly difficult to track interest paid later on.

- Assuming Tax Deductibility for Personal Loans: For most individuals, interest paid on auto loan for a personal vehicle is not tax-deductible. Making this assumption without verifying can lead to issues with the IRS.

Pro Tips for Smart Car Loan Management

Beyond just finding the interest paid, adopting smart strategies can significantly impact your overall loan experience and financial health.

- Keep Meticulous Records: Create a dedicated folder (digital or physical) for all your car loan documents. This includes the original loan agreement, monthly statements, and year-end summaries. This will be invaluable for quick reference.

- Understand Your Loan Terms from Day One: Before signing, ensure you fully grasp your interest rate, loan term, and any associated fees. This foundational knowledge makes tracking easier down the line.

- Consider Refinancing: If interest rates have dropped or your credit score has improved since you took out your loan, explore refinancing options. A lower interest rate can drastically reduce the total interest you pay over the loan’s life. Learn more about whether Is Refinancing Your Car Loan Right For You? (Internal Link Placeholder)

- Make Extra Principal Payments: Even small additional payments directed solely towards the principal can save you a substantial amount in interest over time. Check with your lender to ensure extra payments are applied correctly to the principal.

- Regularly Review Statements: Don’t just glance at your balance. Take a few minutes each month to review the principal and interest breakdown on your statement. This practice keeps you informed and can help spot any discrepancies early.

- Familiarize Yourself with Amortization: Understanding the concept of Understanding Car Loan Amortization (Internal Link Placeholder) can empower you to make more informed decisions about your payments.

Tax Implications of Car Loan Interest: What You Need to Know

It’s crucial to address the tax aspect of car loan interest paid with clarity. For the vast majority of personal vehicle owners, the interest paid on an auto loan is not tax-deductible. The IRS generally categorizes personal car loans as personal interest, which is not deductible.

However, there are specific exceptions:

- Business Use: If your vehicle is used for business purposes, a portion of the interest paid might be deductible as a business expense. The deduction amount will depend on the percentage of business use for the vehicle.

- Heavy Vehicles: In some cases, if the vehicle is a heavy truck or van (over 6,000 pounds gross vehicle weight rating) used for business, it might qualify for certain deductions, including interest.

- Car as Collateral for a Business Loan: If the car is used as collateral for a loan taken out specifically for business purposes, the interest might be deductible.

Important Note: These are complex areas of tax law. If you believe you qualify for an interest deduction, it is imperative to consult with a qualified tax professional or refer directly to IRS publications. For official guidance, you can always visit the Internal Revenue Service (IRS) website to research business expenses and interest deductions. (External Link Placeholder) Attempting to deduct interest without proper justification can lead to issues with tax authorities.

Conclusion: Empowering Your Financial Journey with Auto Loan Knowledge

Understanding how to find interest paid on car loan is a fundamental aspect of responsible financial management. It empowers you to see beyond the surface of your monthly payment and truly grasp the cost of your vehicle financing. Whether you’re using official lender statements, online portals, or personal finance software, the tools are readily available to give you this crucial insight.

By regularly tracking your auto loan interest paid, you position yourself to make smarter decisions about budgeting, refinancing, and accelerating your loan payoff. Don’t let the details of your loan remain a mystery. Take control, leverage the methods outlined in this comprehensive guide, and confidently navigate your financial journey. Start reviewing your statements today and gain a clearer picture of your auto loan.