How to Get a Car Loan from a Bank: Your Ultimate Step-by-Step Guide to Approval

How to Get a Car Loan from a Bank: Your Ultimate Step-by-Step Guide to Approval Carloan.Guidemechanic.com

Buying a car is often one of the most significant purchases you’ll make, second only to a home. For most people, securing a car loan is an essential part of making this dream a reality. While various financing options exist, obtaining a car loan directly from a bank offers numerous advantages, from competitive interest rates to transparent terms.

Navigating the world of auto financing can seem daunting, but with the right knowledge and preparation, you can confidently approach the process. This comprehensive guide will walk you through every crucial step, providing you with the insights and strategies needed to secure a bank car loan with a high chance of approval. Our goal is to empower you to make informed decisions, ensuring you drive away not just with a new car, but with a financing plan that perfectly suits your financial health.

How to Get a Car Loan from a Bank: Your Ultimate Step-by-Step Guide to Approval

Why Choose a Bank for Your Car Loan? Unpacking the Benefits

When considering a car loan, you have several avenues, including dealership financing, credit unions, and online lenders. However, banks often stand out as a preferred choice for many borrowers due to their unique benefits. Understanding these advantages can help you decide if a bank loan is the right fit for your needs.

Competitive Interest Rates

Banks typically offer some of the most competitive interest rates on the market. Their vast financial resources and established lending practices allow them to provide rates that can significantly reduce the total cost of your loan over its lifetime. This is particularly true if you have a strong credit history.

Lower interest rates mean smaller monthly payments and less money paid overall. This financial advantage makes bank loans very attractive, especially for those who prioritize long-term savings. Based on my experience, even a fraction of a percentage point difference in the interest rate can translate into hundreds or even thousands of dollars saved over the typical 5-7 year car loan term.

Transparent Terms and Conditions

One of the hallmarks of bank lending is the clarity and transparency of their loan terms. Banks are heavily regulated, which means their loan agreements are generally straightforward, with all fees, interest rates, and repayment schedules clearly outlined. You’ll typically find fewer hidden clauses or unexpected charges compared to some other lending sources.

This transparency provides peace of mind, allowing you to fully understand your obligations and the total cost of the loan before you commit. There’s no guessing game involved, which is crucial for responsible financial planning. Pro tips from us: Always read the fine print, but with banks, you can generally expect a higher degree of clarity.

Established Trust and Reliability

Banks have a long-standing reputation as stable and reliable financial institutions. When you secure a car loan from a bank, you’re partnering with an entity that has a proven track record in lending and customer service. This can offer a sense of security that might be less apparent with newer or less established lenders.

Their robust customer support systems and established processes mean you’ll have clear channels for communication if you have questions or encounter issues during your loan term. This level of reliability can be a significant comfort when managing a long-term financial commitment like an auto loan.

The Foundation: Preparing for Your Car Loan Application

Before you even think about stepping into a dealership or submitting an application, thorough preparation is key. This foundational work will not only increase your chances of getting approved but also help you secure the best possible terms on your bank car loan. Think of this as laying the groundwork for your financial success.

Understand Your Credit Score: The Gateway to Approval

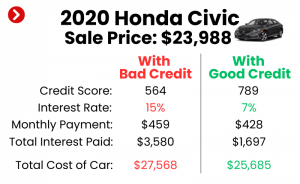

Your credit score is arguably the most critical factor banks consider when evaluating your loan application. It’s a numerical representation of your creditworthiness, reflecting your history of borrowing and repaying debt. A higher score signals to lenders that you are a low-risk borrower, making them more likely to offer you favorable interest rates and terms.

Understanding your credit score involves more than just knowing the number. It means knowing what makes up that score, such as your payment history, amounts owed, length of credit history, new credit, and credit mix. Each of these components plays a vital role in shaping your overall credit profile. Common mistakes to avoid are not checking your credit score before applying, as this leaves you unprepared for what lenders will see.

Pro tips from us: Obtain a copy of your credit report from all three major credit bureaus (Experian, Equifax, TransUnion) at least a few months before you plan to apply for a loan. Review it carefully for any errors or discrepancies. Disputing inaccuracies can take time but can significantly boost your score. Paying down existing debts and making all payments on time are the fastest ways to improve your credit health. for more detailed strategies.

Assess Your Financial Health: What Can You Truly Afford?

Beyond your credit score, banks want to see that you have a stable financial foundation capable of handling new debt. This involves assessing your income, existing debts, and overall financial stability. A crucial metric here is your Debt-to-Income (DTI) ratio, which compares your total monthly debt payments to your gross monthly income.

Lenders typically prefer a DTI ratio below 43%, though some may be more lenient. A lower DTI indicates that you have more disposable income to cover new loan payments, making you a more attractive borrower. This assessment is not just for the bank; it’s for you. It helps ensure you don’t overextend yourself financially.

Pro tips from us: Create a realistic budget that accounts for all your monthly expenses, including rent/mortgage, utilities, groceries, and existing loan payments. Factor in not just the car loan payment, but also insurance, fuel, maintenance, and registration fees. Overestimating your affordability is a common mistake that can lead to financial strain down the road. Be honest with yourself about what you can comfortably afford.

Save for a Down Payment: A Powerful Tool

A down payment is the initial amount of money you pay upfront towards the purchase of your car. While not always mandatory, making a significant down payment offers several compelling advantages that can greatly improve your chances of getting a car loan from a bank and securing better terms. It immediately reduces the amount you need to borrow, thereby lowering your monthly payments and the total interest paid over the life of the loan.

Furthermore, a substantial down payment signals to the bank that you are a serious and responsible borrower. It reduces the bank’s risk because you have more equity in the car from day one, meaning you’re less likely to default. In the event of an accident or if the car depreciates quickly, a larger down payment helps prevent you from owing more on the car than it’s worth (being "upside down" on your loan).

Pro tips from us: Aim for at least 10-20% of the car’s purchase price as a down payment. If you can manage more, even better. This shows financial discipline and can unlock lower interest rates, as the bank sees less risk. Saving diligently for this payment is an investment in your future financial stability.

Know Your Car’s Value and Your Budget: Research is Key

Before you even start shopping, it’s vital to research the market value of the cars you’re interested in. Websites like Kelley Blue Book (KBB) or Edmunds can provide excellent estimates of new and used car prices. This knowledge allows you to set a realistic budget for the vehicle itself, rather than just focusing on the loan payment.

Understanding the market value helps you negotiate better prices at the dealership and ensures you don’t overpay. It also helps you align your car choice with your pre-determined budget and the amount you anticipate a bank will be willing to lend you. A bank will assess the car’s value as collateral, so choosing a reasonably priced vehicle strengthens your application.

Step-by-Step Guide: How to Apply for a Car Loan From a Bank

Once your financial house is in order, you’re ready to embark on the application process. This structured approach will guide you efficiently towards securing your bank car loan. Each step is designed to optimize your chances of approval and ensure you get the best deal.

Step 1: Get Pre-Approved – Your Negotiating Powerhouse

Getting pre-approved for a car loan from a bank is arguably the most powerful step you can take before visiting a dealership. Pre-approval means a bank has reviewed your financial information and tentatively agreed to lend you a specific amount of money at a certain interest rate, subject to final verification and the choice of vehicle. It’s essentially a commitment from the bank.

Based on my experience: Pre-approval is a game-changer. It transforms you from a regular shopper into a cash buyer in the eyes of the dealership. You walk in knowing exactly how much you can spend and what your interest rate will be, which eliminates much of the stress and uncertainty from the car-buying process. It also gives you leverage to negotiate the car’s price more effectively, as you’re not reliant on the dealership’s financing options.

Step 2: Gather Required Documents – Be Prepared

Banks require a specific set of documents to verify your identity, income, and financial stability. Having these readily available will streamline your application process and demonstrate your preparedness. Delaying the submission of documents can hold up your approval.

Typically, you’ll need:

- Proof of Identity: Government-issued ID (driver’s license, passport).

- Proof of Income: Recent pay stubs (usually 2-3 months), W-2 forms, tax returns (if self-employed), or bank statements showing regular deposits.

- Proof of Residence: Utility bill, lease agreement, or mortgage statement with your current address.

- Bank Statements: Recent statements to show financial activity and cash flow.

- Social Security Number: For credit checks.

- Vehicle Information (if already chosen): Make, model, year, VIN (Vehicle Identification Number), and purchase price.

Ensure all your documents are current and accurately reflect your financial situation. Any discrepancies could cause delays or even lead to a denial.

Step 3: Compare Loan Offers – Don’t Settle for the First One

Even after pre-approval from one bank, it’s wise to compare offers from several different banks. Interest rates and loan terms can vary significantly between lenders, and a little comparison shopping can save you a substantial amount of money over the life of the loan. Don’t just look at the monthly payment; delve into the Annual Percentage Rate (APR), total loan cost, and any associated fees.

Pro tips from us: When comparing, pay close attention to the APR, which includes both the interest rate and any fees. A lower APR means a cheaper loan overall. Also, consider the loan term – a longer term means lower monthly payments but more interest paid over time. Common mistakes to avoid are focusing solely on the monthly payment without considering the total cost of the loan.

Step 4: Choose Your Car Wisely – Stick to Your Budget

With your pre-approval in hand, you now have a clear budget for your car purchase. This empowers you to shop for a vehicle that fits comfortably within your financial limits. Remember, your pre-approval amount is the maximum you can spend, not necessarily what you should spend.

Consider factors beyond the sticker price, such as fuel efficiency, insurance costs, maintenance, and potential resale value. Choosing a car that aligns with your budget and lifestyle is crucial for long-term satisfaction and financial health. for a detailed guide on vehicle selection.

Step 5: Finalize the Loan and Purchase – The Closing Process

Once you’ve chosen your car, the final step is to finalize the loan agreement with your bank and complete the purchase. This involves signing all necessary paperwork with the bank, which will then typically disburse the funds directly to the dealership (or to you, if you’re buying privately).

Carefully review all documents one last time before signing. Ensure the interest rate, loan term, and all other conditions match what you were offered and agreed upon. This final review is your last opportunity to catch any potential errors or misunderstandings.

Key Factors Banks Consider for Loan Approval

Banks employ a comprehensive evaluation process to determine your eligibility for a car loan. Understanding these key factors can help you optimize your application and increase your chances of approval. Each element contributes to a holistic picture of your financial risk profile.

Your Credit Score and History

As mentioned, your credit score is paramount. Banks use it as a quick indicator of your past financial behavior. A FICO score of 660 or higher is generally considered good for securing favorable auto loan rates, with scores above 720 often unlocking the best offers. Your credit report also shows your payment history, types of credit accounts, and any derogatory marks like bankruptcies or foreclosures.

A history of on-time payments across all your accounts demonstrates reliability. Banks want to see consistency and responsibility. They’ll look for any late payments, collections, or charge-offs, as these can signal a higher risk.

Income and Employment Stability

Banks need assurance that you have a reliable source of income to make your monthly payments. They’ll assess your current employment status, length of employment, and income level. Stable employment with a consistent income stream for at least a year or two makes you a more attractive borrower.

If you’ve recently changed jobs or are self-employed, you might need to provide more extensive documentation to prove your income stability. Lenders want to see a predictable income that comfortably covers your existing debts plus the new car loan payment.

Debt-to-Income (DTI) Ratio

Your DTI ratio is a crucial metric that directly impacts your ability to take on new debt. It represents the percentage of your gross monthly income that goes towards debt payments. Banks prefer a lower DTI ratio, as it indicates you have sufficient income left over after covering your current obligations.

A high DTI suggests you might be overextended, making it riskier for the bank to lend you more money. Reducing your existing debt before applying can significantly improve this ratio and your chances of approval.

Down Payment Amount

The size of your down payment directly influences the bank’s risk assessment. A larger down payment reduces the loan amount, thereby decreasing the bank’s exposure. It also shows your commitment to the purchase and your financial discipline.

Banks view a substantial down payment favorably, often rewarding borrowers with lower interest rates or more flexible terms. It acts as a cushion against the car’s depreciation, especially in the early years of ownership.

Age and Condition of the Car (Collateral)

The car you intend to purchase serves as collateral for the loan. This means if you default on the loan, the bank can repossess and sell the car to recover their losses. Therefore, banks assess the car’s value, age, and condition.

Newer cars with lower mileage typically hold their value better, making them more desirable collateral. Older or higher-mileage vehicles may be deemed riskier, potentially leading to higher interest rates or a requirement for a larger down payment. Banks want to ensure the car’s value is sufficient to cover the loan amount.

Common Mistakes to Avoid When Applying for a Car Loan

Navigating the car loan application process can be complex, and it’s easy to fall into common traps. Being aware of these pitfalls can help you avoid unnecessary headaches, save money, and ensure a smoother experience.

Applying to Too Many Lenders at Once

While it’s crucial to compare offers, indiscriminately applying to numerous lenders within a short period can negatively impact your credit score. Each "hard inquiry" on your credit report can temporarily ding your score. While credit scoring models often group multiple auto loan inquiries within a 14-45 day window as a single inquiry (recognizing you’re rate shopping), applying beyond this window or for too many different types of credit can be detrimental.

Pro tips from us: Do your research to identify a few strong contenders for lenders based on their reputation and advertised rates. Focus your applications on these select few within a concentrated timeframe to minimize credit score impact.

Not Getting Pre-Approved

As previously emphasized, skipping pre-approval is a significant misstep. Without it, you walk into a dealership blind, unsure of your borrowing power or interest rate. This puts you at a distinct disadvantage during negotiations, as you’re at the mercy of the dealership’s financing options, which may not always be the most competitive.

Pre-approval provides clarity and control, allowing you to focus on negotiating the car’s price rather than simultaneously figuring out the financing. It empowers you as a buyer.

Focusing Only on Monthly Payments

It’s tempting to fixate solely on achieving the lowest possible monthly payment. However, this often leads to extending the loan term for too long, which dramatically increases the total interest you pay over the life of the loan. A lower monthly payment over 7 or 8 years can result in paying significantly more interest than a slightly higher payment over 4 or 5 years.

Always consider the total cost of the loan, including the principal and all interest charges. A seemingly affordable monthly payment might mask an expensive overall loan.

Ignoring the Total Cost of the Loan

Beyond the monthly payment and interest, consider all associated costs: origination fees, documentation fees, and any optional add-ons like extended warranties or GAP insurance (which, while useful, should be purchased knowingly and not hidden). These can inflate the total amount you finance and the overall cost of your car.

Ensure you understand every line item in your loan agreement and the purchase contract. Don’t be afraid to ask questions until you’re completely clear on what you’re paying for.

Buying More Car Than You Can Afford

One of the most common and damaging mistakes is letting emotion override financial prudence. Dealerships are skilled at upselling, and it’s easy to get caught up in the excitement of a newer, fancier model. However, buying a car that stretches your budget too thin can lead to financial stress, missed payments, and even repossession.

Stick to the budget you established during your financial health assessment. Remember, the car loan is just one part of car ownership; insurance, fuel, maintenance, and registration also add up.

What If Your Car Loan Application is Denied?

A car loan denial can be disheartening, but it’s not the end of the road. It’s an opportunity to understand what went wrong and improve your financial standing for future applications. Don’t panic; instead, take a proactive approach.

Understand the Reason for Denial

By law, lenders are required to provide you with an Adverse Action Notice explaining why your application was denied. This notice is crucial as it pinpoints the specific issues that led to the rejection. Common reasons include:

- Low credit score: Indicating a history of poor credit management.

- High Debt-to-Income (DTI) ratio: Too much existing debt relative to your income.

- Insufficient income: The bank believes your income isn’t enough to comfortably cover payments.

- Limited credit history: Not enough credit accounts or a short credit history to assess risk.

- Errors on your credit report: Inaccuracies that unfairly lower your score.

- Issues with the collateral: The car’s value or condition is not suitable for the loan amount.

Review this notice carefully. It provides a roadmap for what you need to address.

Improve Your Financial Situation

Once you know the reason, you can take concrete steps to improve your financial profile.

- Boost Your Credit Score: If your score was the issue, focus on making all payments on time, reducing credit card balances, and avoiding new credit inquiries for a few months.

- Lower Your DTI: Pay down existing debts, especially high-interest ones. You might also look for ways to increase your income, if possible.

- Save for a Larger Down Payment: A bigger down payment reduces the loan amount and the bank’s risk, making you a more attractive borrower.

- Address Credit Report Errors: If there were inaccuracies, dispute them with the credit bureaus immediately.

This process takes time, but it’s an investment in your future financial health.

Consider Alternatives

If immediate approval from a bank isn’t possible, explore other options:

- Consider a Co-signer: If you have a trusted friend or family member with excellent credit, they might co-sign the loan. Their strong credit history can help you get approved, but it also makes them equally responsible for the debt.

- Look at Different Lenders: Credit unions often have more flexible lending criteria and may be more willing to work with applicants who have less-than-perfect credit. Online lenders also cater to a wider range of credit profiles.

- Choose a Less Expensive Car: A more affordable vehicle means a smaller loan amount, which reduces the risk for lenders and makes approval easier.

- Wait and Reapply: Sometimes, the best strategy is to wait a few months, actively work on improving your credit and financial situation, and then reapply when you’re in a stronger position.

Remember, a denial is a setback, not a permanent roadblock. Use it as motivation to build a stronger financial foundation. offers additional resources on understanding auto loans and your rights.

Beyond Approval: Managing Your Car Loan Responsibly

Securing your car loan from a bank is a significant achievement, but it’s just the beginning. Responsible loan management is crucial for maintaining good financial health and ensuring a positive borrowing experience. Your actions during the loan term will impact your credit history and future financial opportunities.

Making On-Time Payments

This might seem obvious, but consistently making your car loan payments on time is the single most important aspect of responsible loan management. Each on-time payment positively contributes to your credit history, strengthening your credit score over time. Conversely, even a single late payment can negatively impact your score and incur late fees.

Pro tips from us: Set up automatic payments from your bank account to ensure you never miss a due date. If your financial situation changes and you anticipate difficulty making a payment, contact your bank immediately to discuss potential options. Open communication is always better than missing a payment without notice.

Considering Refinancing Your Car Loan

After a year or two, your financial situation might have improved significantly. Perhaps your credit score has increased, or interest rates have dropped. In such cases, you might consider refinancing your car loan. Refinancing involves taking out a new loan, often with a lower interest rate, to pay off your existing car loan.

This can lead to lower monthly payments, reduced total interest paid, or a shorter loan term. Before refinancing, compare the new offer to your current loan, including any fees associated with the new loan, to ensure it truly benefits you.

Understanding Early Payoff Options

Many car loans allow you to pay off the loan early without penalty. If you find yourself with extra cash, paying off your loan ahead of schedule can save you a substantial amount in interest. It also frees up your monthly budget sooner.

However, always check your loan agreement for any prepayment penalties. While rare with bank auto loans, some lenders might impose them. If there are no penalties, making extra principal payments can be a smart financial move.

Conclusion: Drive Away with Confidence

Securing a car loan from a bank doesn’t have to be a stressful ordeal. By thoroughly preparing, understanding the application process, and being aware of common pitfalls, you can significantly increase your chances of approval and secure favorable terms. From building a strong credit score and saving for a down payment to getting pre-approved and comparing offers, each step is a building block toward a successful outcome.

Remember, the goal isn’t just to get a car; it’s to get a car with a financing plan that supports your overall financial well-being. By following the expert advice and practical strategies outlined in this guide, you are now equipped to navigate the world of bank car loans with confidence and clarity. Start your preparation today, and soon you’ll be driving away in your new vehicle, knowing you’ve made a smart financial decision.