How To Get A Car Loan With Bad Credit: Your Ultimate Guide to Approval

How To Get A Car Loan With Bad Credit: Your Ultimate Guide to Approval Carloan.Guidemechanic.com

Getting a car is often more than just a convenience; it’s a necessity for work, family, and daily life. But what if your credit score isn’t as shiny as a new car’s paint job? For many, the idea of securing a car loan with bad credit feels like an uphill battle. The good news? It’s not impossible.

Based on my extensive experience in the financial and automotive sectors, I can tell you that millions of people successfully obtain car loans every year, even with less-than-perfect credit. The key is knowing the right strategies, understanding the process, and approaching it with confidence and preparation. This comprehensive guide will walk you through every essential step, equipping you with the knowledge to navigate the journey and drive away with the car you need.

How To Get A Car Loan With Bad Credit: Your Ultimate Guide to Approval

Understanding Bad Credit and Its Impact on Car Loans

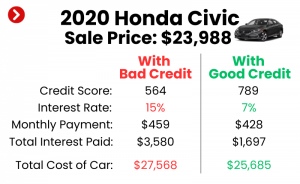

Before we dive into the "how-to," it’s crucial to understand what "bad credit" means in the eyes of a lender and why it poses a challenge. Your credit score is a numerical representation of your creditworthiness, derived from your credit history. FICO scores, for instance, typically range from 300 to 850, with scores below 600-620 generally considered "subprime" or "bad credit."

Lenders use this score to assess the risk of lending you money. A low credit score signals a higher likelihood of default, making lenders hesitant. This hesitation often translates into less favorable loan terms for you. You might face higher interest rates, stricter repayment conditions, or even a requirement for a larger down payment.

The impact of bad credit isn’t just about whether you get approved; it’s also about the long-term cost of your loan. A higher interest rate means you’ll pay significantly more over the life of the loan compared to someone with excellent credit. This is why understanding your credit situation and proactively addressing it is your first and most vital step.

Step 1: Know Your Credit Score and Report Inside Out

You can’t fix a problem until you understand its root cause. The very first action you should take is to obtain and thoroughly review your credit report and score. This isn’t just about seeing a number; it’s about understanding the factors contributing to it.

You are legally entitled to a free copy of your credit report from each of the three major credit bureaus—Experian, Equifax, and TransUnion—once every 12 months. The most reliable place to access these reports is AnnualCreditReport.com. This official site allows you to pull all three reports in one go.

Once you have your reports, scrutinize every detail. Look for any inaccuracies, such as accounts that aren’t yours, incorrect payment statuses, or outdated information. Errors are more common than you might think, and they can negatively impact your score. If you find any discrepancies, dispute them immediately with the respective credit bureau. Correcting these errors can sometimes give your score a quick boost.

Beyond errors, understanding the contents of your report helps you identify areas for improvement. Are there late payments? High credit utilization? A diverse credit mix? Knowing these details empowers you to speak confidently with lenders and address any concerns they might have. Pro tips from us: don’t just skim it; read every line.

Step 2: Assess Your Financial Situation Realistically

Before you even start browsing cars, take a hard, honest look at your personal finances. This step is critical for preventing financial strain down the road. What can you truly afford to pay each month for a car, not just the loan payment, but the total cost of ownership?

Beyond the monthly loan payment, consider insurance, fuel costs, routine maintenance, and potential repairs. These often overlooked expenses can quickly add up, turning an affordable car payment into an overwhelming financial burden. Create a detailed budget that accounts for all your income and expenditures.

Lenders will also look at your debt-to-income (DTI) ratio. This ratio compares your total monthly debt payments (including the prospective car loan) to your gross monthly income. A high DTI indicates that you’re already stretched thin, making you a higher risk. Aim for a DTI below 40%, ideally even lower, to present a more favorable financial picture.

Based on my experience, many people get excited about a car’s price tag and forget the hidden costs. Don’t fall into this trap. A realistic budget ensures you can comfortably make your payments, which is essential for rebuilding your credit.

Step 3: Save Up for a Substantial Down Payment

For borrowers with bad credit, a significant down payment is one of your most powerful tools. It signals to lenders that you are serious, committed, and have some "skin in the game." A larger down payment directly reduces the amount you need to borrow, which in turn lowers your monthly payments and the total interest paid over the life of the loan.

More importantly, a substantial down payment reduces the lender’s risk. If you put down a sizable sum, the loan-to-value (LTV) ratio decreases, meaning the amount you owe is less than the car’s value. This provides a buffer for the lender in case of default. Lenders are much more willing to approve a bad credit car loan when their risk is mitigated.

Aim for at least 10% to 20% of the car’s purchase price, if possible. Even a smaller down payment is better than none. Every dollar you put down upfront can significantly improve your chances of approval and secure more favorable terms. Common mistakes to avoid include thinking you don’t need a down payment with bad credit; it’s almost always a requirement or a massive advantage.

Step 4: Explore Different Lender Types

Not all lenders are created equal, especially when it comes to financing a car with poor credit. You’ll want to explore a variety of options to find the best possible terms. Each type of lender has its own niche and criteria.

Subprime Lenders / Special Finance Dealerships: These lenders specialize in working with borrowers who have bad credit. Many dealerships have "special finance" departments dedicated to helping customers with credit challenges. They are often more lenient with approval criteria but typically charge higher interest rates to offset the increased risk. While they can be a good starting point, always compare their offers.

Credit Unions: Often overlooked, credit unions can be excellent options. As member-owned institutions, they are typically more flexible and willing to work with individuals facing credit issues. They often offer more competitive interest rates and personalized service compared to traditional banks. Membership requirements are usually straightforward, sometimes just requiring residency in a specific area or association with an employer.

Online Lenders: The digital age has brought a plethora of online lenders specializing in bad credit auto loans. These platforms offer convenience, quick pre-approvals, and the ability to compare multiple offers from different lenders without leaving your home. They can be a great way to shop around efficiently and find competitive rates. Just ensure they are reputable and check their reviews.

Buy Here, Pay Here (BHPH) Dealerships: These dealerships act as both the seller and the lender. They approve virtually anyone, regardless of credit, because they assume all the risk in-house. While this sounds appealing, BHPH loans often come with extremely high interest rates, short repayment terms, and little to no reporting to credit bureaus. This means making on-time payments might not help rebuild your credit. Based on my experience, BHPH dealerships should be a last resort. Always exhaust other options first due to their often predatory terms.

Step 5: Consider a Co-signer (If Applicable)

If you’re struggling to get approved or are only offered extremely high interest rates, a co-signer can significantly improve your chances. A co-signer is someone with good credit who agrees to take on the legal responsibility for the loan if you fail to make payments. Their strong credit profile essentially mitigates the risk associated with your bad credit.

Having a co-signer can lead to approval for a loan you otherwise wouldn’t get, and potentially at a much lower interest rate. This can save you thousands of dollars over the life of the loan. However, choosing a co-signer is a serious decision that carries significant risks for them. If you miss payments, it negatively impacts their credit score, and they will be legally obligated to repay the entire loan.

Pro tips from us: only ask someone you trust implicitly and who understands the full implications. Ensure you are absolutely confident in your ability to make every payment on time. This is not a decision to take lightly, as it can strain personal relationships if things go wrong.

Step 6: Get Pre-Approved Before You Shop

One of the most powerful strategies for anyone, especially those with bad credit, is to get pre-approved for a car loan before you step foot on a dealership lot. Pre-approval gives you a firm offer of credit, detailing the maximum loan amount, estimated interest rate, and loan terms you qualify for.

The benefits of pre-approval are manifold. First, it clarifies what you can realistically afford, preventing you from falling in love with a car outside your budget. Second, it transforms you into a cash buyer in the eyes of the dealership. With financing already secured, you can focus solely on negotiating the car’s price, rather than being swayed by monthly payment figures that might hide unfavorable loan terms.

Remember, there’s a difference between pre-qualification and pre-approval. Pre-qualification is a soft inquiry that gives you an estimate without impacting your credit score. Pre-approval, on the other hand, involves a hard inquiry, which will temporarily ding your score but provides a concrete offer. Aim for pre-approval from one or two lenders within a short window (typically 14-45 days) to minimize the impact on your credit score, as multiple hard inquiries for the same type of loan within this period are often treated as a single inquiry by credit scoring models.

Step 7: Choose the Right Car (Focus on Affordability)

When you have bad credit, choosing the right vehicle is paramount. This isn’t the time to splurge on luxury or brand-new models. Your priority should be a reliable, affordable car that meets your essential needs.

Used cars are often a much better choice for bad credit borrowers. They are significantly less expensive than new cars, meaning you’ll need to borrow less and face lower monthly payments. Depreciation hits new cars hardest in their first few years, so buying a slightly used vehicle allows someone else to absorb that initial loss.

Focus on reliability. A breakdown or major repair can quickly derail your budget and ability to make loan payments. Research makes and models known for their longevity and low maintenance costs. Websites like Consumer Reports or J.D. Power can offer valuable insights into vehicle reliability. Common mistakes to avoid include buying a car that’s too expensive or too old/unreliable, leading to financial distress.

Step 8: Negotiate Smartly (Beyond the Price Tag)

Once you have your pre-approval in hand, you’re in a much stronger negotiating position. Approach the dealership with confidence, knowing your financing is already secured. Don’t let them push you into their financing options if your pre-approved rate is better.

When negotiating, always focus on the total cost of the car, not just the monthly payment. Dealerships often try to distract buyers by adjusting loan terms (like extending the loan length) to lower the monthly payment, which ultimately means you pay more in interest over time. Be wary of this tactic.

Also, scrutinize any add-ons or extended warranties. While some might offer value, many are overpriced and can be declined. Be prepared to walk away if the deal isn’t right. There are always other dealerships and other cars. For an in-depth look at negotiation tactics, check out our guide on How to Negotiate a Car Deal Like a Pro.

Step 9: Understand Your Loan Terms Fully

Before you sign any document, ensure you completely understand every aspect of your car loan terms. This is crucial for protecting your financial well-being. Don’t be afraid to ask questions until everything is crystal clear.

The most important terms to review are the Annual Percentage Rate (APR), the loan term, and the total cost of the loan. The APR includes the interest rate plus any fees, giving you the true cost of borrowing. A longer loan term might mean lower monthly payments, but it also means you’ll pay more in interest over time. Calculate the total amount you will pay back, including interest, to see the true cost of the vehicle.

Also, check for any prepayment penalties. While less common with auto loans, some lenders might charge a fee if you pay off your loan early. This is an important detail if you plan to refinance or pay down your loan aggressively. Pro tips from us: Never rush the signing process. Read the fine print, and if something doesn’t make sense, ask for clarification. The Consumer Financial Protection Bureau (CFPB) offers excellent resources on understanding auto loans, which can be a valuable external resource to consult.

Step 10: Use Your Car Loan to Rebuild Credit

Securing a car loan with bad credit isn’t just about getting a vehicle; it’s a golden opportunity to rebuild and improve your credit score. This loan can serve as a powerful tool to demonstrate responsible financial behavior.

The most important action you can take is to make every single payment on time, every time. Payment history is the single largest factor influencing your credit score (35% of your FICO score). Consistent, timely payments will steadily improve your credit score over the life of the loan. Ensure your lender reports your payments to all three major credit bureaus. Most legitimate auto lenders do, but it’s worth confirming.

As your credit score improves, you may even have the option to refinance your car loan for a lower interest rate in the future, further reducing your total cost. This initial bad credit car loan can be a stepping stone towards a healthier financial future. To learn more about boosting your financial standing, read our article on Strategies to Quickly Improve Your Credit Score.

Common Mistakes to Avoid When Getting a Car Loan with Bad Credit

Navigating the world of bad credit car loans can be tricky. Here are some common pitfalls that many borrowers encounter, and how you can avoid them:

- Not Checking Your Credit Report: As discussed, this is foundational. Without knowing your credit standing, you’re going in blind. Don’t let errors or unknowns dictate your loan terms.

- No Down Payment: While some lenders might offer zero-down options, it’s almost always a bad idea with bad credit. It leads to higher monthly payments, more interest, and immediate negative equity (owing more than the car is worth).

- Applying Everywhere: Each loan application results in a "hard inquiry" on your credit report, which can temporarily lower your score. Spreading applications across many lenders in a short period can hurt you. Focus on getting pre-approved by a couple of well-researched lenders.

- Focusing Only on Monthly Payment: This is a classic dealer trick. A lower monthly payment might sound appealing, but it often comes with a much longer loan term and significantly more interest paid over time. Always consider the total cost of the loan.

- Ignoring Total Loan Cost: Beyond the monthly payment, understand the full amount you’ll repay, including all interest and fees. This provides a clearer picture of the loan’s true expense.

- Settling for the First Offer: Never accept the first loan offer you receive, especially with bad credit. Shop around, compare rates, and use pre-approvals to leverage better terms. Competition among lenders benefits you.

- Not Factoring in All Car Expenses: Remember, a car loan is just one part of car ownership. Insurance, fuel, maintenance, and registration can add hundreds of dollars to your monthly outlay. A common mistake is getting approved for a loan but then struggling to afford the car’s overall running costs.

Conclusion: Your Path to Car Ownership, Despite Bad Credit

Getting a car loan with bad credit is undoubtedly more challenging than with a pristine credit history, but as we’ve explored, it is far from impossible. By understanding your credit situation, preparing your finances, exploring the right lending avenues, and approaching the process strategically, you can significantly increase your chances of approval and secure reasonable terms.

Remember, this isn’t just about getting a car; it’s about taking control of your financial future. Use this opportunity to make timely payments and actively rebuild your credit score. Each successful payment is a step towards greater financial freedom and better opportunities down the road.

Don’t let past credit mistakes define your present needs. Arm yourself with knowledge, follow these steps diligently, and embark on your journey to car ownership with confidence. Your new car, and an improved credit score, await! Start your preparation today and drive towards a brighter financial tomorrow.