How to Get a Car Loan: Your Ultimate Guide to Approval and Smart Auto Financing

How to Get a Car Loan: Your Ultimate Guide to Approval and Smart Auto Financing Carloan.Guidemechanic.com

The dream of a new car, or even a reliable used one, often begins with the exciting process of browsing models and envisioning your drives. Yet, for most people, that dream car isn’t paid for with a stack of cash. Instead, it’s purchased with a car loan – a financial commitment that can feel daunting if you don’t know where to start.

Securing a car loan is a significant financial decision, and navigating the world of auto financing can be complex. From understanding your credit score to comparing interest rates and dealing with dealerships, there are many layers to peel back. But don’t worry, you’re in the right place.

How to Get a Car Loan: Your Ultimate Guide to Approval and Smart Auto Financing

This comprehensive guide is designed to empower you with the knowledge and strategies needed to not only get a car loan but to get one on the best possible terms. We’ll break down every step, offering expert insights, practical tips, and common pitfalls to avoid, ensuring your journey to car ownership is smooth and financially sound. Let’s get started on the road to your next vehicle!

Understanding the Landscape of Car Loans

Before diving into the application process, it’s crucial to understand what a car loan entails and the various avenues available for securing one. A car loan is essentially an agreement where a lender provides you with funds to purchase a vehicle, and you agree to repay that amount, plus interest, over a set period. This period is known as the loan term, and it typically ranges from 36 to 84 months.

The reason car loans are so prevalent is simple: accessibility. Very few individuals have the upfront capital to buy a vehicle outright. Auto financing makes car ownership a reality for millions, allowing them to spread the cost over several years in manageable monthly payments. However, not all car loans are created equal, and understanding your options is the first step towards making a smart financial choice.

Different Types of Lenders and What They Offer

The financial marketplace offers a diverse range of lenders, each with its own advantages and disadvantages. Knowing who they are and what they specialize in can significantly impact your car loan experience and the terms you receive.

- Traditional Banks: Large, established banks like Chase, Wells Fargo, or Bank of America are common sources for auto loans. They often provide competitive interest rates for borrowers with strong credit histories. If you already have a banking relationship, you might find the application process straightforward, and sometimes even qualify for preferential rates.

- Credit Unions: These member-owned financial institutions are renowned for their customer-centric approach and often offer some of the most competitive interest rates on car loans. Because they are not-for-profit, credit unions tend to pass savings onto their members in the form of lower rates and fees. If you meet their membership criteria, exploring a credit union is often a smart move.

- Dealership Financing: When you buy a car from a dealership, they will often offer to arrange financing for you. This can be convenient, as it’s a one-stop shop for both buying the car and securing the loan. Dealerships work with a network of various lenders, and they might even offer special promotional rates through "captive finance" companies (e.g., Toyota Financial Services, Ford Credit). While convenient, it’s crucial to compare their offers with pre-approvals you’ve secured elsewhere, as they may mark up interest rates.

- Online Lenders: The digital age has brought forth a host of online-only lenders, such as LightStream or Capital One Auto Navigator. These platforms often offer quick application processes, fast approval decisions, and the ability to compare multiple loan offers from the comfort of your home. They can be particularly useful for those looking to cast a wide net and find the best possible rate without visiting multiple physical locations.

Each of these lender types has its strengths, and the best option for you will depend on your personal financial situation, credit score, and preferences. It’s always a good strategy to explore multiple avenues to ensure you’re getting the most favorable terms available.

The Cornerstone: Your Credit Score

Your credit score is arguably the single most important factor in securing a car loan and determining the interest rate you’ll pay. Lenders use this three-digit number to assess your creditworthiness – essentially, how likely you are to repay your loan on time. A higher score signals less risk to lenders, translating into better loan terms, lower interest rates, and easier approval.

What is a Credit Score and How Does it Impact Your Loan?

A credit score, most commonly the FICO score or VantageScore, is a numerical summary of the information contained in your credit report. It’s calculated based on several key factors, each weighted differently. Understanding these factors can help you appreciate why your score is what it is, and how to improve it.

- Payment History (35%): This is the most crucial factor. Consistently making on-time payments on all your credit accounts (credit cards, mortgages, previous auto loans) demonstrates reliability. Late payments, collections, or bankruptcies will severely damage your score.

- Amounts Owed (30%): This refers to how much debt you currently carry relative to your available credit. A high credit utilization ratio (using a large percentage of your available credit) can negatively impact your score. Keeping balances low is key.

- Length of Credit History (15%): The longer your credit accounts have been open and in good standing, the better. This shows lenders you have a proven track record over time.

- New Credit (10%): Opening multiple new credit accounts in a short period can be seen as risky behavior. Each new credit application results in a "hard inquiry" on your report, which can temporarily dip your score.

- Credit Mix (10%): Having a healthy mix of different types of credit (e.g., installment loans like mortgages or car loans, and revolving credit like credit cards) can positively impact your score, showing you can manage various forms of debt responsibly.

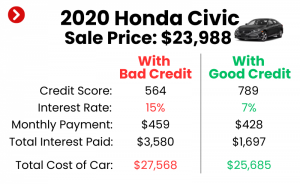

The impact of your credit score on a car loan is direct and substantial. Someone with an excellent credit score (typically 780+) might qualify for interest rates as low as 0-3%, while a borrower with a fair or poor score (below 620) could face rates of 10% or even higher. Over the life of a 60-month loan, this difference can amount to thousands of dollars in extra interest paid.

Checking Your Credit Report: A Crucial First Step

Before you even think about applying for a car loan, it is absolutely essential to check your credit report. This allows you to understand your current standing and identify any potential errors that could unfairly impact your ability to get approved or secure a favorable rate.

- Based on my experience, one of the most impactful steps you can take before even thinking about a car loan is to thoroughly review your credit report. You are entitled to a free copy of your credit report from each of the three major bureaus (Experian, Equifax, and TransUnion) once every 12 months. You can obtain these reports securely through AnnualCreditReport.com. This is the only authorized website for free reports.

- Carefully scrutinize each report for inaccuracies, such as accounts that don’t belong to you, incorrect payment statuses, or outdated information. If you find errors, dispute them immediately with the credit bureau and the creditor. Correcting mistakes can significantly boost your score.

Tips for Improving Your Credit Score Before Applying

If your credit score isn’t where you want it to be, taking steps to improve it before applying for an auto loan can save you a lot of money in the long run.

- Pay All Bills On Time: This is the most fundamental and effective strategy. Set up automatic payments or reminders to ensure you never miss a due date.

- Reduce Credit Card Debt: Pay down your credit card balances to lower your credit utilization ratio. Aim to keep it below 30% of your available credit.

- Avoid Opening New Credit Accounts: Resist the temptation to open new credit cards or take out other loans in the months leading up to your car loan application. Each new hard inquiry can temporarily lower your score.

- Keep Old Accounts Open: Even if you don’t use an old credit card much, keeping it open can help your "length of credit history" and "amounts owed" factors.

- Be Patient: Building credit takes time and consistent responsible behavior. Start early if you know you’ll need a loan in the future.

Preparing Your Finances for a Car Loan

A successful car loan application isn’t just about your credit score; it’s also about demonstrating financial readiness. This involves careful budgeting, understanding the power of a down payment, and knowing how lenders view your overall debt.

Budgeting: How Much Can You Truly Afford?

Many people make the mistake of focusing solely on the monthly payment when considering a car loan. However, the true cost of car ownership extends far beyond that single number.

- Pro tips from us: When budgeting for a car, think holistically. Beyond the monthly loan payment, factor in:

- Car Insurance: Get quotes for the specific vehicles you’re considering. This can vary wildly based on the car’s value, your driving record, and where you live.

- Fuel Costs: Estimate your weekly or monthly fuel expenses based on your commute and driving habits.

- Maintenance and Repairs: All cars need maintenance. Newer cars might have less, but older cars could require significant repairs. Budget an emergency fund for this.

- Registration and Taxes: Annual fees and sales tax (if applicable) are recurring costs.

- Parking Fees/Tolls: If applicable to your daily routine.

Only after accounting for all these expenses can you accurately determine a comfortable monthly loan payment that fits within your overall budget. To help you crunch the numbers, our detailed article on can be an invaluable resource.

The Power of a Down Payment

A down payment is the initial amount of money you pay upfront for the car, reducing the total amount you need to borrow. While it might seem like a hurdle, making a significant down payment offers several powerful advantages.

- Lower Monthly Payments: A smaller loan amount directly translates to lower monthly payments, easing the strain on your budget.

- Reduced Total Interest Paid: By borrowing less, you’ll pay interest on a smaller principal, significantly reducing the overall cost of the loan over its term.

- Improved Loan-to-Value (LTV) Ratio: Lenders look favorably on a lower LTV ratio (the loan amount compared to the car’s value). A strong down payment shows you’re invested in the purchase, making you a less risky borrower.

- Protection Against Negative Equity: Cars depreciate rapidly. A good down payment can prevent you from owing more on the car than it’s worth, also known as being "upside down" or having negative equity. This is particularly important if you need to sell or trade in the car sooner than expected.

- Better Interest Rates: Lenders may offer more attractive interest rates to borrowers who make larger down payments, especially if your credit score is less than perfect. Aim for at least 10-20% of the car’s purchase price, and even more for a used car.

Understanding Your Debt-to-Income (DTI) Ratio

Beyond your credit score, lenders also scrutinize your debt-to-income (DTI) ratio. This ratio compares your total monthly debt payments to your gross monthly income (before taxes and deductions). It’s a crucial indicator of your ability to manage additional debt.

- How to Calculate DTI: Add up all your minimum monthly debt payments (credit cards, student loans, mortgage/rent, existing car loans, etc.). Then, divide that sum by your gross monthly income. For example, if your total debt payments are $1,000 and your gross income is $3,000, your DTI is 33%.

- Lender Preferences: Most lenders prefer a DTI ratio below 43%, though some might prefer even lower, especially for auto loans. A lower DTI indicates that you have plenty of income left to cover new debt obligations. If your DTI is high, consider paying down existing debts before applying for a car loan.

Interest Rates and APR: Knowing the True Cost of Borrowing

When comparing car loan offers, you’ll encounter two key terms: interest rate and Annual Percentage Rate (APR). While often used interchangeably, there’s an important distinction.

- Interest Rate: This is the percentage charged by the lender for borrowing the principal amount. It’s the cost of the money itself.

- Annual Percentage Rate (APR): This is the true annual cost of your loan, expressed as a percentage. The APR includes not only the interest rate but also any additional fees or charges associated with the loan, such as origination fees.

- Focus on APR: Always compare APRs when evaluating loan offers, as it gives you the most accurate picture of the total cost of borrowing. A loan with a slightly lower interest rate but higher fees could end up having a higher APR than a loan with a slightly higher interest rate but no fees.

The Application Process: Your Step-by-Step Guide

With your finances in order and a solid understanding of your credit, you’re ready to navigate the car loan application process. Following these steps systematically will put you in the best position to secure a favorable loan.

Step 1: Get Pre-Approved (Crucial for Empowerment!)

This is perhaps the most important step many car buyers overlook. Getting pre-approved means a lender has reviewed your credit and financial information and tentatively agreed to lend you a specific amount at a certain interest rate, pending a final vehicle choice.

- Benefits of Pre-Approval:

- Know Your Budget: You’ll know exactly how much you can borrow, allowing you to shop for cars within your budget with confidence.

- Stronger Negotiating Power: With a pre-approval letter in hand, you become a cash buyer in the eyes of the dealership. This means you can negotiate the car’s price separately from the financing, often leading to a better deal on the vehicle itself.

- Avoid Dealership Pressure: You won’t feel pressured to accept the dealership’s financing offer, as you already have a competitive rate from an outside lender.

- Faster Purchase Process: Pre-approval streamlines the buying process, as much of the paperwork is already done.

- Where to Get Pre-Approved:

- Banks and Credit Unions: Start with your current bank or credit union, as they may offer preferential rates to existing customers.

- Online Lenders: Use online platforms to compare offers from multiple lenders quickly. This allows you to gather several pre-approval offers within a short timeframe.

- Soft vs. Hard Inquiries: Getting pre-approved usually involves a "soft inquiry" on your credit, which doesn’t affect your score. Once you formally apply for a loan, it becomes a "hard inquiry," which might cause a slight, temporary dip. However, credit scoring models typically count multiple hard inquiries for the same type of loan within a short period (e.g., 14-45 days) as a single inquiry, so shop around for rates without fear of significant credit damage.

Pro tips from us: Always get pre-approved from at least two to three different lenders before stepping foot in a dealership. This gives you leverage and a clear benchmark to compare any offers the dealership might present.

Step 2: Gather Required Documents

Lenders will need specific documents to verify your identity, income, and residency. Having these ready will expedite the application process.

- Proof of Identity: Valid government-issued photo ID (driver’s license, passport).

- Proof of Income: Recent pay stubs (last 2-3 months), W-2 forms, tax returns (especially if self-employed), bank statements.

- Proof of Residency: Utility bill, lease agreement, or mortgage statement.

- Social Security Number: For credit checks.

- Vehicle Information (if applicable): For refinancing or specific vehicle loans, details like VIN, mileage, and title.

Step 3: Shop for Your Car (with Pre-Approval in Hand)

Now that you know your budget and have pre-approval, you can shop confidently. Focus on finding the right car at the right price.

- Negotiate the Car Price Separately: Remember, you’re a cash buyer. Negotiate the selling price of the vehicle first, before discussing any financing options the dealership might offer. This ensures you’re getting the best deal on the car itself.

- New vs. Used Car Loan Considerations:

- New Cars: Generally come with lower interest rates (especially promotional rates), but higher purchase prices and faster initial depreciation.

- Used Cars: Often have slightly higher interest rates due to perceived higher risk (older models, unknown history), but lower purchase prices. They also depreciate slower after the initial years. Carefully consider the vehicle’s history and condition.

Step 4: Compare Loan Offers

Once you’ve settled on a car and have your pre-approval offers, it’s time to compare them meticulously, including any financing options the dealership might present.

- Focus on the APR: As discussed earlier, the APR is the most accurate measure of the total cost of borrowing. Don’t be swayed by just the monthly payment.

- Evaluate the Loan Term:

- Shorter Terms (36-48 months): Higher monthly payments, but you’ll pay significantly less in total interest over the life of the loan. You’ll also build equity faster.

- Longer Terms (60-84 months): Lower monthly payments, making the car more "affordable" on a month-to-month basis. However, you’ll pay substantially more in total interest and risk going "upside down" on the loan (owing more than the car is worth) for a longer period.

- Common mistakes to avoid are focusing solely on the monthly payment. While important for your budget, a low monthly payment often comes with a longer loan term and a much higher total cost of the loan. Always prioritize the lowest APR and a loan term you’re comfortable with financially.

Step 5: Finalize the Loan and Read the Fine Print

Once you’ve chosen the best loan offer, it’s time to sign the dotted line. This final step requires diligence to ensure you understand everything you’re agreeing to.

- Read the Entire Contract: Do not rush this step. Read every page of the loan agreement carefully before signing. Ensure the APR, loan term, total loan amount, and monthly payment match what you agreed upon.

- Beware of Add-Ons: Dealerships often try to sell you various add-on products and services at the finance office (e.g., extended warranties, gap insurance, paint protection, anti-theft devices). Some of these might be valuable to you, but others might be unnecessary and significantly increase your total loan amount and monthly payment.

- Pro tips from us: If you’re interested in an extended warranty or gap insurance, research third-party providers or your own insurance company first. They often offer these products at a lower cost than the dealership. Never feel pressured to buy something you don’t need or understand.

- Understand Prepayment Penalties: While less common with auto loans, some lenders might charge a fee if you pay off your loan early. Always confirm if your loan has such a clause.

Special Situations in Car Loan Acquisition

Not everyone has a perfect credit score or a long history of credit management. Here’s how to approach car loans in less-than-ideal situations.

Getting a Car Loan with Bad Credit

Having a low credit score doesn’t necessarily mean you can’t get a car loan, but it does mean you’ll face higher interest rates and potentially stricter terms. Lenders view bad credit as a higher risk.

- Realistic Expectations: Be prepared for higher APRs, shorter loan terms (to reduce lender risk), and possibly a requirement for a larger down payment.

- Strategies for Bad Credit:

- Larger Down Payment: This is one of the most effective ways to mitigate risk for the lender. It reduces the amount you need to borrow and shows your commitment.

- Find a Co-Signer: A co-signer with good credit can significantly improve your chances of approval and help you secure a lower interest rate. However, understand that a co-signer is equally responsible for the loan, and their credit will be affected if you miss payments.

- Buy a Less Expensive Car: Opting for a more affordable vehicle reduces the overall loan amount, making it easier to qualify and manage payments.

- Work with Subprime Lenders: These lenders specialize in working with borrowers with poor credit. While they offer financing, their interest rates are typically much higher, reflecting the increased risk. Always compare offers carefully.

- Improve Your Credit First: If possible, dedicate a few months to improving your credit score before applying. Even a small increase can make a difference in your interest rate. For a deep dive into boosting your score, check out our guide: .

First-Time Car Buyer Loans

If you’re a first-time car buyer with little to no credit history, getting approved can be challenging but not impossible. Lenders have no track record to evaluate.

- Specific Programs: Some banks and credit unions offer special "first-time buyer" programs designed to help individuals establish credit. These often come with specific requirements, such as a minimum income, a down payment, or a co-signer.

- Co-Signer: As with bad credit, a co-signer with good credit can be a huge asset in securing your first auto loan.

- Secured Loan Option: Some lenders might offer a secured loan where the car itself acts as collateral.

- Build Credit with a Small Loan: If you’re not in an immediate rush, consider building some credit history with a small, secured credit card or a credit-builder loan first.

- Demonstrate Stability: Show proof of stable employment and residence to reassure lenders about your ability to make payments.

Post-Approval and Beyond: Managing Your Car Loan

Securing your car loan is a big step, but your financial journey doesn’t end there. Responsible management of your loan is crucial for building good credit and ensuring long-term financial health.

Making Timely Payments: The Key to a Healthy Credit Score

Once your car loan is finalized, your primary responsibility is to make every payment on time, every month.

- Impact on Credit: Timely payments are heavily weighted in your credit score calculation. Consistently making payments on time will significantly boost your credit history and improve your score over the loan term.

- Avoid Late Fees: Late payments not only damage your credit but also incur late fees, adding to your overall cost.

- Set Up Auto-Pay: Consider setting up automatic payments from your bank account to ensure you never miss a due date. This offers peace of mind and builds a strong payment history.

Refinancing Options: When and Why to Consider It

Circumstances change, and what was once a good car loan might not be the best option anymore. Refinancing means taking out a new loan to pay off your existing car loan, ideally with more favorable terms.

- When to Consider Refinancing:

- Improved Credit Score: If your credit score has significantly improved since you took out the original loan, you might qualify for a lower interest rate.

- Lower Interest Rates: If market interest rates have dropped, or if you initially had a high rate due to poor credit, refinancing can save you money.

- Change in Financial Situation: If you need to lower your monthly payments, refinancing to a longer term can achieve this (though you’ll pay more in total interest). Conversely, if you want to pay off the loan faster, you can refinance to a shorter term.

- Benefits: Lower monthly payments, lower total interest paid, or a shorter loan term.

- Process: Shop around for refinancing offers just as you did for your original loan. Compare APRs, terms, and any fees associated with the new loan.

Conclusion: Drive Away with Confidence

Getting a car loan doesn’t have to be a confusing or stressful experience. By understanding the fundamentals of credit, preparing your finances meticulously, and approaching the application process strategically, you can secure favorable terms and drive away with confidence.

Remember, the key lies in empowerment through knowledge. Check your credit, budget comprehensively, get pre-approved from multiple lenders, and always scrutinize the fine print. Your car loan is a significant financial commitment, and making an informed decision will not only save you money but also contribute positively to your long-term financial well-being.

So, take a deep breath, review these steps, and start your journey towards smart auto financing. Happy driving!