How To Get Out Of Credit Acceptance Car Loan: Your Comprehensive Roadmap to Financial Freedom

How To Get Out Of Credit Acceptance Car Loan: Your Comprehensive Roadmap to Financial Freedom Carloan.Guidemechanic.com

Are you currently burdened by a Credit Acceptance car loan? You’re not alone. Many individuals find themselves in a challenging position with these high-interest auto loans, often feeling trapped and overwhelmed. The good news is, there are pathways to financial freedom, and this comprehensive guide is designed to illuminate each step.

Based on my extensive experience in consumer finance and helping individuals navigate complex debt situations, I understand the unique pressures that come with a subprime auto loan. This article will not only explain how to get out but will also equip you with the knowledge to make informed decisions and build a more secure financial future. Let’s embark on this journey together.

How To Get Out Of Credit Acceptance Car Loan: Your Comprehensive Roadmap to Financial Freedom

Understanding Your Credit Acceptance Loan: The First Step to Escape

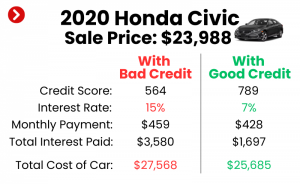

Before you can effectively strategize your exit, it’s crucial to understand the nature of your Credit Acceptance loan. These loans are specifically designed for individuals with less-than-perfect credit, often referred to as "subprime" borrowers. While they offer a vital opportunity for transportation, they typically come with significantly higher interest rates and less favorable terms compared to traditional auto loans.

From my vantage point, many borrowers overlook the finer details of their loan agreement, which can lead to unwelcome surprises down the line. Take the time to meticulously review your contract. Key elements to pinpoint include your Annual Percentage Rate (APR), the total amount financed, the total interest you’ll pay over the life of the loan, and any potential prepayment penalties. Understanding these figures is paramount.

The high APR means a substantial portion of your early payments often goes towards interest rather than reducing the principal balance. This can create a situation of negative equity, where you owe more on the car than it’s actually worth, making it harder to sell or refinance. Knowing your exact numbers empowers you to choose the most effective strategy.

Assessing Your Current Financial Situation: A Clear Picture is Power

You can’t plot an escape route without knowing your starting point. A thorough assessment of your current financial health is the bedrock of any successful plan to get out of your Credit Acceptance car loan. This isn’t just about looking at your car payment; it’s about understanding your entire financial landscape.

Pro tips from us: Start by creating a detailed budget. Document every dollar of your income and every single expense, no matter how small. This includes not just fixed costs like rent and utilities, but also variable spending on groceries, entertainment, and fuel. Many online tools and apps can help you track this effectively.

Next, check your credit score. A higher credit score opens up more options for refinancing at a lower interest rate. You can obtain a free credit report from each of the three major bureaus annually. Look for any inaccuracies and understand what factors are influencing your score.

Finally, evaluate your debt-to-income (DTI) ratio. This metric shows how much of your gross monthly income goes towards debt payments. A lower DTI ratio indicates you have more disposable income and are a less risky borrower, which is attractive to potential lenders if you decide to refinance. A clear financial snapshot is your first line of defense against high-interest debt.

Strategies to Get Out of Your Credit Acceptance Car Loan

Now that you understand your loan and your financial standing, let’s explore the concrete strategies available to you. Each option has its own set of requirements and implications, so consider them carefully in light of your personal circumstances.

1. Refinancing Your Loan: A Path to Lower Payments

Refinancing involves taking out a new loan to pay off your existing Credit Acceptance loan, ideally with a lower interest rate and more favorable terms. This is often the most desirable solution for many borrowers as it can significantly reduce your monthly payments and the total interest paid over time.

When is refinancing possible? Typically, you’ll need to demonstrate improved creditworthiness since you first took out the Credit Acceptance loan. This could mean your credit score has increased, you’ve consistently made your payments on time, or your debt-to-income ratio has improved. A stable employment history also helps.

Shop around aggressively for the best refinancing offers. Don’t just go with the first lender you find. Explore options with credit unions, traditional banks, and online lenders. Credit unions, in particular, are known for offering competitive rates to their members. Compare not just the interest rate, but also the loan term, any fees, and the overall total cost of the new loan.

A common mistake to avoid is refinancing without fully understanding the new terms. Ensure there are no hidden fees or extended loan terms that might make the new loan less beneficial in the long run. Sometimes, a slightly lower monthly payment comes at the cost of paying more interest over a longer period. Always do the math!

Pro Tip: Even a small improvement in your credit score can unlock significantly better refinancing options. For more detailed strategies on how to boost your credit, check out our comprehensive guide: .

2. Selling the Car: Eliminating the Debt Entirely

Selling your car is a direct way to get out from under your Credit Acceptance loan, especially if you no longer need the vehicle or if its value is close to or exceeds what you owe. This strategy requires careful planning, particularly if you’re facing negative equity.

There are several avenues for selling your car: a private sale, trading it in at a dealership, or selling it to an online car buying platform. From my vantage point, selling privately often yields more money for your vehicle, as dealerships need to factor in their profit margins. However, a private sale requires more effort on your part, including advertising, showing the car, and handling paperwork.

The biggest hurdle with selling, especially for subprime loans, is often negative equity. This means the outstanding balance on your loan is higher than the car’s market value. If this is the case, you’ll need to cover the difference out of pocket to satisfy the loan. Options for covering negative equity include using savings, taking out a small personal loan (if your credit allows), or a combination of both.

Before deciding to sell, get multiple appraisals for your car. Use resources like Kelley Blue Book (KBB) or Edmunds to estimate its value. This will give you a realistic expectation of what you can get for it and help you prepare for any potential negative equity you might need to cover.

3. Early Payoff: Accelerating Your Path to Ownership

If refinancing or selling isn’t feasible, accelerating your payments can significantly reduce the total interest you pay and get you out of your Credit Acceptance loan much faster. This strategy involves making extra payments directly towards the principal balance of your loan.

How does it work? Every dollar you pay beyond your minimum monthly payment, if designated for the principal, directly reduces the amount on which interest is calculated. Over time, this compounds, leading to substantial savings on interest and an earlier payoff date.

Methods for accelerating payments include making bi-weekly payments (which results in one extra payment per year), rounding up your monthly payment, or making lump-sum payments whenever you have extra cash, such as from a bonus or tax refund. Even an extra $20-$50 per month can make a noticeable difference over the life of the loan.

A common mistake to avoid is assuming extra payments automatically go to principal. Always specify to Credit Acceptance (or any lender) that any additional funds should be applied directly to the principal balance. Otherwise, they might be applied to future interest or even advanced payments, which doesn’t accelerate your payoff.

Pro Tip: Creating a small "debt snowball" by tackling your smallest debts first can build momentum and psychological wins, making it easier to stick to an early payoff plan for larger debts like your car loan. For more effective strategies on debt acceleration, check out our detailed post: .

4. Voluntary Repossession: A Difficult Last Resort

Voluntary repossession involves returning the vehicle to Credit Acceptance when you can no longer afford the payments. While it might seem like a straightforward solution to stop the financial bleeding, it carries severe consequences and should only be considered as an absolute last resort.

The immediate impact of voluntary repossession is significant damage to your credit score, which can linger for up to seven years. This makes it extremely difficult to obtain future loans, credit cards, or even housing. Furthermore, returning the car doesn’t necessarily mean the debt disappears.

Credit Acceptance will sell the vehicle, typically at auction, for less than its market value. The difference between the sale price and your outstanding loan balance is known as a "deficiency balance." You will still be legally responsible for paying this deficiency balance, along with any repossession and auction fees. They can pursue collection efforts, including lawsuits and wage garnishment, to recover this amount.

Based on my experience, I’ve advised clients on voluntary repossession only when all other options have been exhausted, and the borrower is facing extreme financial hardship with no other viable path forward. Always explore alternatives like selling the car (even at a loss), negotiating with the lender, or seeking credit counseling first.

5. Loan Modification or Debt Settlement: Direct Negotiation

If you’re experiencing severe financial hardship and can no longer make your Credit Acceptance payments, direct negotiation with the lender for a loan modification or debt settlement might be an option. This is a challenging path, as subprime lenders are often less flexible, but it’s worth exploring before considering voluntary repossession.

When contacting Credit Acceptance, be prepared. Have a clear understanding of your financial situation, including why you can’t make payments and what you can realistically afford. Document everything: names of representatives, dates, times, and summaries of conversations. Pro tip: Approach them with a clear plan and evidence of hardship, such as job loss or medical bills.

Potential outcomes of a loan modification are rare for subprime auto loans but could include a temporary payment deferral, a slight reduction in interest rate, or an extension of the loan term. Be wary of extending the term too much, as it could lead to paying significantly more interest over time.

Debt settlement involves negotiating to pay a lump sum that is less than the total amount you owe. This is often done with the help of a debt settlement company, but these services come with fees and can also negatively impact your credit score. If considering this, proceed with extreme caution and research any company thoroughly. It’s often more effective when the account is already delinquent.

6. Transferring the Loan: A Rare Opportunity

While extremely rare and often difficult with subprime loans, transferring your car loan to another individual is theoretically a way to get out of the debt. This typically involves finding a willing and qualified buyer who can take over your existing loan or secure a new loan in their name for the vehicle.

The conditions for such a transfer are stringent. The new buyer must have excellent credit and meet all of Credit Acceptance’s lending criteria, which is a high bar for a company that specializes in subprime lending. Moreover, Credit Acceptance would need to explicitly approve the transfer, which is not a common practice for auto loans.

This option is generally more feasible with private party sales where the new buyer secures their own financing, effectively paying off your loan. However, a direct loan transfer, where the lender simply swaps the borrower on the existing loan, is almost unheard of in the subprime auto lending world. Do not rely on this as a primary strategy.

Building a Stronger Financial Future: Beyond the Loan

Getting out of your Credit Acceptance car loan is a significant achievement, but it’s equally important to implement strategies that prevent you from falling into a similar situation again. This is about building a foundation for lasting financial health.

Firstly, continue focusing on improving your credit score. Consistent on-time payments, reducing credit card balances, and avoiding new debt will gradually elevate your score. A better credit score is your ticket to lower interest rates on all future loans.

Secondly, maintain and refine your budget. A robust budget isn’t just for crisis management; it’s a tool for ongoing financial control and wealth building. Understand where your money goes and consciously allocate funds to savings and debt reduction.

Thirdly, prioritize building an emergency fund. Aim for at least three to six months’ worth of living expenses. This fund acts as a financial buffer, preventing you from resorting to high-interest loans when unexpected costs arise, like car repairs or medical emergencies.

Finally, educate yourself on car buying and financing before your next vehicle purchase. Understand depreciation, negotiate prices effectively, and always pre-qualify for a loan before stepping onto the dealership lot. This empowers you to make smarter decisions and avoid predatory lending practices.

For expert guidance on budgeting and comprehensive financial planning, the Consumer Financial Planning Bureau (CFPB) offers excellent, unbiased resources and tools: .

Common Pitfalls and How to Avoid Them

The journey out of a Credit Acceptance car loan can be fraught with potential missteps. Being aware of these common pitfalls can help you navigate the process more smoothly.

One of the biggest mistakes is ignoring the problem. Hoping it will simply go away or avoiding communication with your lender will only escalate the situation, leading to late fees, credit damage, and potential repossession. My experience shows that proactive engagement is always better than avoidance.

Another pitfall is falling for "quick fix" scams. Be extremely wary of companies promising to magically erase your debt or offering solutions that sound too good to be true. Always research any third-party service thoroughly and understand their fees and potential impact on your credit.

Not reading the fine print is another common error. Whether it’s your original loan agreement or a new refinancing offer, every clause matters. Overlooking prepayment penalties, hidden fees, or unfavorable terms can negate the benefits of your chosen strategy.

Finally, making emotional decisions can derail your efforts. Financial decisions, especially those involving significant debt, should be based on careful analysis and logic, not panic or frustration. Take a deep breath, review your options, and consult trusted resources.

When to Seek Professional Help

Sometimes, the situation is complex enough that professional guidance becomes invaluable. Don’t hesitate to seek help if you feel overwhelmed or unsure about the best path forward.

Credit counselors are an excellent resource. Non-profit credit counseling agencies can help you review your finances, create a realistic budget, and explore debt management plans. They can also often act as an intermediary with lenders.

Financial advisors can provide broader guidance on long-term financial planning, investment strategies, and overall wealth management, helping you align your debt repayment with your future financial goals.

In severe cases, such as facing a lawsuit or contemplating bankruptcy, consulting with a qualified attorney specializing in consumer law or bankruptcy can protect your rights and help you understand your legal options.

Conclusion: Your Path to Automotive Freedom

Getting out of a Credit Acceptance car loan might seem like an uphill battle, but as this comprehensive guide demonstrates, it is absolutely achievable. By understanding your loan, meticulously assessing your finances, and strategically applying the methods outlined above, you can regain control of your financial destiny.

Remember, whether you choose to refinance, sell the car, accelerate payments, or explore other options, the key is to be proactive, informed, and persistent. Each step you take towards reducing this high-interest debt not only frees up your monthly budget but also builds a stronger foundation for your future financial health.

Don’t let the burden of a subprime auto loan define your financial journey. Take these steps, empower yourself with knowledge, and pave your way to automotive freedom and lasting financial stability. What strategies have you found most effective in managing challenging loans? Share your experiences and questions in the comments below – your insights could help others on a similar path!